UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-8748 |

|

Wanger Advisors Trust |

(Exact name of registrant as specified in charter) |

|

One Financial Center, Boston, Massachusetts | | 02111 |

(Address of principal executive offices) | | (Zip code) |

|

James R. Bordewick, Jr., Esq. Columbia Management Advisors, LLC One Financial Center Boston, MA 02111 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-617-426-3750 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2008 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Wanger International Select

2008 Annual Report

| NOT FDIC INSURED | | May Lose Value | |

|

| NOT BANK ISSUED | | No Bank Guarantee | |

|

Wanger International Select

2008 Annual Report

Table of Contents

| | 1 | | | Understanding Your Expenses | |

|

| | 2 | | | The Population Bust | |

|

| | 4 | | | Performance Review | |

|

| | 6 | | | Statement of Investments | |

|

| | 10 | | | Statement of Assets and Liabilities | |

|

| | 10 | | | Statement of Operations | |

|

| | 11 | | | Statement of Changes in Net Assets | |

|

| | 12 | | | Financial Highlights | |

|

| | 13 | | | Notes to Financial Statements | |

|

| | 17 | | | Report of Independent Registered Public Accounting Firm | |

|

| | 18 | | | Federal Income Tax Information | |

|

| | 19 | | | Management Fee Evaluation of the Senior Officer | |

|

| | 23 | | | Board Approval of the Advisory Agreement | |

|

| | 25 | | | Board of Trustees and Management of Wanger Advisors Trust | |

|

Columbia Wanger Asset Management, L.P. ("CWAM") is one of the leading global small- and mid-cap equity managers in the United States with more than 37 years of small- and mid-cap investment experience. As of December 31, 2008, CWAM manages $19.3 billion in assets and is the investment advisor to Wanger USA, Wanger International, Wanger Select, Wanger International Select (together, the "Wanger Advisors Trust Funds") and the Columbia Acorn Family of Funds. Columbia Management Group, LLC ("Columbia Management") is the investment management division of Bank of America Corporation. Columbia Management entities furnish investment management services and products for institutional and individual investors. The Wanger Advisors Trust Funds and the Columbia Acorn Family of Funds (together with other funds advised by Columbia Management affiliates, the "Columbia Funds") are distributed by Columbia Management Distributors, Inc., member of FINRA, SIPC, part of Columbia Management and an affiliate of Bank of America Corporation. CWAM is a registered investment advisor and an indirect, wholly owned subsidiary of Bank of America Corporation. CWAM is part of Columbia Management.

Please consider the investment objectives, risks, charges and expenses for the Fund carefully before investing. Contact 1-888-4-WANGER for a prospectus, which contains this and other important information about the Fund. You should read it carefully before you invest.

The views expressed in "The Population Bust" and in the Performance Review reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Fund. References to specific company securities should not be construed as a recommendation or investment advice.

Wanger International Select 2008 Annual Report

Understanding Your Expenses

As a Fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption or exchange fees. There are also ongoing costs, which generally include investment advisory fees and other Fund expenses. The information on this page is intended to help you understand your ongoing costs of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund's expenses

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in the Fund during the period. The information in the following table is based on an initial, hypothetical investment of $1,000, which is invested at the beginning of the period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using actual operating expenses and total return for the Fund. The amount listed in the "Hypothetical" column assumes that the return each year is 5% before expenses and then applies the Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See the "Compare with other fu nds" information for details on using the hypothetical data.

Estimating your actual expenses

To estimate the expenses that you actually paid over the period, first you will need your account balance at the end of the period.

1. Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6.

2. In the section of the table below titled "Expenses paid during the period," you will find a dollar amount in the column labeled "Actual." Multiply this amount by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period.

July 1, 2008 – December 31, 2008

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid during

the period ($) | | Fund's annualized

expense ratio (%)* | |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | |

| Wanger International Select | | | 1,000.00 | | | | 1,000.00 | | | | 577.10 | | | | 1,018.50 | | | | 5.23 | | | | 6.70 | | | | 1.32 | | |

*For the six months ended December 31, 2008.

Expenses paid during the period are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 366.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Fund. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate account. The hypothetical example provided is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing cost of investing in a fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees that may be incurred by shareholders of other funds. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate accounts.

1

Wanger International Select 2008 Annual Report

The Population Bust

Important socio-economic predictions are based on demographics. For example, virtually all of the people who will retire in 2058 are living today and retirement age, immigration and mortality trends are utilized to create assumptions that will be used to predict the number of future retirees. The labor force of 2028 and the military age population of 2025 are similarly predictable. These factors are major drivers of government burdens, GDP growth and military potential. Demographics indicate that the world is unlikely to age gracefully.

World Demographic Trends

Richard Jackson and Neil Howe's, The Graying of the Great Powers provides an excellent summary of current demographic trends. Its authors conclude that, "The world is entering a demographic transformation of unprecedented dimensions...a fundamental demographic shift with no parallel in the history of humanity.... There is almost no chance that it will not happen—or that it will be reversed in our lifetime."1

The world's current great powers2 are aging at remarkably divergent rates. The United States is barely aging and has a fertility rate of 2.0 to 2.1 births per woman during child-bearing years, very near long-term zero population growth. This country is one of the youngest developed nations, and the age gap between the United States and other developed countries is projected to widen. "By the mid-2020's, the United States will be the only major developed country with more children under age 20 than elderly over age 65—and the only one whose working-age population will still be growing," write Jackson and Howe. The U.S. work force is projected to grow 14% between 2005 and 2030.3 & nbsp;

Russian fertility rates plunged through the 1980s and rest today at 1.2 to 1.3 births. Risky lifestyles and a poor health care system have caused mortality rates to soar. Life expectancy for a Russian male has dropped to 59 years, lower than that of Bangladeshi males! Russia's working age population (those aged 20 to 64) will plunge 17% from 2005 to 2030.4 Prime Minister Vladimir Putin termed Russia's lack of births as "the most acute problem facing our country today."5

Jackson and Howe note that Japan is ground zero for demographic aging. Like Russia, its fertility rate has fallen to an average of 1.3 children per woman. In 1980, Japan was the youngest developed country, with only 9% of its population over age 65. By 2005, its elderly (those aged 65 and over) accounted for 20% of its population, making it one of the oldest developed countries. Japan's working-age population started shrinking in 2000 and from 2005 to 2030 it is expected to drop 18%.6

China's one-child policy collapsed fertility rates, which have since rebounded to 1.7 to 1.8. But China's pre-one-child-policy population bulge is aging rapidly. China's working age population will fall after 2015 and China's ratio of workers to retirees will triple from 2005 to 2030. The Chinese have relied on family rather than the government for old age support and, with shrunken families, China by 2030 could have over 100 million indigent seniors. The Asian Tigers' fertility rates range from 0.9 to 1.4, and the Tigers also are rapidly aging.7,8

There are two demographic categories of Western European countries: those with likely slow population declines and those with likely fast population drops. Slow decliners have fertility rates of around 1.8 and include the United Kingdom, France and northern Europe, except Germany. Fast decliners have fertility rates of 1.3 and include Germany and southern Europe. The working age population of Europe is projected to shrink 6% by 2030. Public pensions already cost Europe twice the percentage of GDP as compared to the United States, and will get worse. Europe's elderly will account for over 25% of its population in 2030, up from 17% in 2005.9

The image of rapidly growing populations all over the developing world is outdated. Only a few areas of the world, including sub-Saharan Africa and some Muslim countries (Iraq, Yemen, Somalia, Sudan, Afghanistan and Pakistan) have fertility rates of 4.0 or higher. Fertility has trended down in most other developing countries. In non-Muslim South Asia, including India, fertility has fallen to about 3.0. Latin America fertility has dropped to 2.5 from 6.0 in the 1960s. Turkey and Iran have current fertility rates around 2.1. However, many developing countries have high percentages of women in childbearing ages, so despite declining fertility rates, their absolute numbers of youths and working age populations will grow rapidly for several decades.10

Immigration will impact the numbers in the United States and Europe. Migration is at or near records in many countries. Some 13% of the U.S. population consists of immigrants, as does 8% to 13% of France, the United Kingdom and Germany. Hispanics are the primary immigrants into the United States; most are employed and data indicates that second generation Hispanics have higher incomes than their parents. That in turn suggests higher productivity and some degree of assimilation. Muslims are the primary immigrants in many European countries; their unemployment rates are high and most of their second generation seems to be making little economic progress; many are not assimilating. This suggests future productivity problems in much of Europe, and possibly diverging national interests.11

Jackson and Howe cite numerous geopolitical implications from demographic changes. Within the developed world, only the United States will likely have the capacity to remain a great power. It was the third most populous country in the world in 1950 and is forecasted to remain so in 2050. Germany, the United Kingdom, Italy and France had populations among the top dozen countries in the world in 1950, but of them,

2

Wanger International Select 2008 Annual Report

Germany will be the leader at 26th in 2050. Western Europe and Japan will be aged and Western Europe especially will have huge public pension costs. While the United States and Western Europe each accounted for 37% of the developed world's economy in the 1980s, the U.S. will likely grow to 54% and Western Europe is projected to shrink to 23% by 2050.12 The United States' increasing relative strength will likely mean that it will need to provide for an even greater proportion of the developed world's security.

Though the U.S. share of the developed world's population and economy will rise, its share of the total world's population and economy will fall. Howe and Jackson note that 90% of the world's population growth to 2050 will occur in sub-Saharan Africa, Muslim countries and South Asia, in nations largely troubled by poverty, religious conflict or both.13

Due to the characteristics of population segments, security risks are likely to rise and peak in the 2020s. This will come at a time when most of the historically great powers are likely to have military recruiting challenges along with budget problems. Jackson and Howe also worry about the effects of aging on savings rates and creativity. In a book by Mark Steyn titled America Alone,14 the author writes that the United States should do a better job exporting its values of liberty, women's rights, freedom of speech, self reliance, decentralization and responsibility. He believes this is one way the U.S. influence can make a posi tive impact.

Investment Implications

Change creates investment risks and opportunities. Recognizing these powerful trends and understanding when they are likely to occur could mitigate the risks and result in profitable investments.

Studies indicate that an individual's creativity, as measured by works of art, peaks between the ages of 30 and 50 and that Nobel achievements peak when people are in their 30s.15 An aging worldwide population may make innovation more scarce and consequently more highly rewarded. Innovative companies may become less subject to competition and be more highly valued in financial markets.

Small- and mid-cap companies tend to be innovative and adaptable. Many existing companies provide goods and services to growing population segments and more will emerge in the future to do so. Our analysts will continue to pursue these opportunities around the world.

The United States has excellent prospects compared to much of the rest of the developed world. Many investment analysts have tracked the baby boomer and echo baby boomer age segments, and as a result have predicted demand for goods and services such as toys, school books, automobiles, housing, leisure items and health care. Long-term demand for leisure and health care continues to appear promising, and additional opportunities may include companies producing labor saving devices and military technology. The United States stands to benefit from woes elsewhere, as highly productive people migrate here for employment and entrepreneurial opportunities, lower taxes and, in some cases, less strife.

There will continue to be investment opportunities overseas. In developed countries, companies that provide products or services to aging populations should benefit. Once the world economy recovers, capital goods suppliers to developing countries should resume growing. Developing countries that have moderate population growth and attractive climates for capitalism are likely to increase their share of world GDP and provide investment opportunities. Companies that participate in domestic growth within these countries should especially benefit.

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, L.P.

The information and data provided in this analysis are derived from sources that we deem to be reliable and accurate. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. The views/opinions expressed in this essay are those of the author and not of the Columbia Wanger Trust Board, are subject to change at any time based upon economic, market or other conditions, may differ from views expressed by other Columbia Management associates or other divisions of Bank of America and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund.

1 Jackson, Richard and Howe, Neil, The Graying of the Great Powers, (Washington, D.C., Center for Strategic & International Studies, 2008), pg. 1.

2 By popular definition, the "great powers" are the worlds most powerful countries based on wealth, military strength and population.

3 Jackson, Richard and Howe, Neil, op. cit., pgs. 39-40.

4 Ibid, pg. 179.

5 "Vladimir Putin on Raising Russia's Birth Rate," Population and Development Review 32, no. 2 (June 2006).

6 Jackson, Richard and Howe, Neil, op. cit., pg. 44.

7 The Asian Tiger countries include Hong Kong, Singapore, South Korea and Taiwan.

8 Jackson, Richard and Howe, Neil, op. cit., pgs. 155, 171, 175.

9 Ibid, pg. 42.

10 Ibid, pgs. 163-176.

11 Ibid, pgs. 122-126.

12 Ibid, pgs. 191-192.

13 Ibid, pg. 194.

14 Steyn, Mark, America Alone: The End of the World As We Know It, (Washington, D.C., Regnery Publishing, Inc., 2006), pgs. 173, 205.

15 Jackson, Richard and Howe, Neil, op. cit., pg. 111.

3

Wanger International Select 2008 Annual Report

Performance Review Wanger International Select

Christopher J. Olson

Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Performance may reflect any voluntary waiver and reimbursement of fund expenses by the advisor or affiliates. Absent these fee waivers, or expense reimbursements, performance results may be lower. For daily and most recent month-end performance updates, please call 1-888-4-WANGER.

All results shown assume reinvestment of distributions and do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption of fund shares.

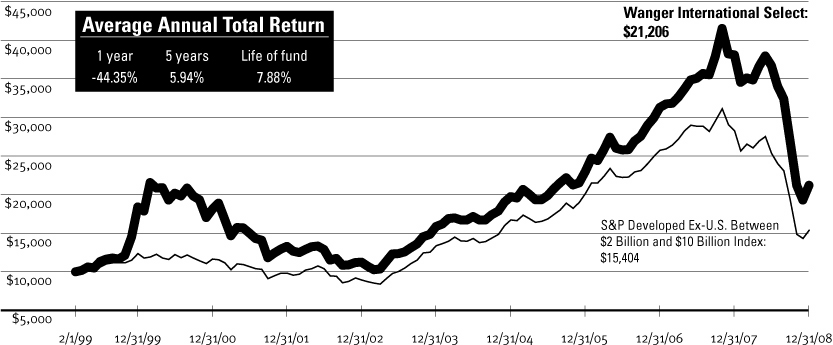

Wanger International Select ended the year down 44.35%, outperforming the 45.57% drop of its benchmark, the S&P Developed Ex-U.S. Between $2 Billion and $10 Billion Index.* It was an abysmal investment environment as equity markets throughout the world dropped in response to the deleveraging of the global economy.

During the fourth quarter we more than doubled the Fund's exposure to Japan. At the end of the third quarter, the Fund had a roughly 12% weighting in Japan and, by year end, we had raised that weighting to 25%. Valuations in Japanese stocks have improved and, having dealt with a deleveraging economy over the past 20 years already, the country and its companies appear better able to weather this current storm. Jupiter Telecommunications is the largest cable service provider in Japan and was the Fund's top contributor for the year, up 25%. Jupiter is enjoying continued subscriber growth and is benefiting from smart acquisitions. Several of our new Japanese names also went right to work, posting gains ranging from 17% to 39%. Daito Trust Construction, an apartment builder, has a strong niche business, good cash flow and recently started buying back shares. Office building real estate investment trust Nippon Building Fund's discount to net asset value appeared overdone when we purchased the stock in the fourth quarter and the market seemed to agree. Its strong funding position should enable it to manage through this more difficult period. Kamigumi was also added in the fourth quarter. A port cargo handling and logistics company, Kamigumi rose as investors began to appreciate its more stable business model, which is focused on consumer staple imports.

Outside of Japan, QIAGEN, a Dutch life science company, gained 20% as the company continued to demonstrate solid organic revenue growth driven by diverse product offerings in genetic analysis and diagnostics. Chilean fertilizer producer Sociedad Quimica y Minera de Chile ended the year with a solid gain as the late year drop in fertilizer price expectations was not enough to offset the gains we made from purchasing the stock at a much cheaper valuation. The Fund's investment in the stock was up 35% for the year.

The Fund's greatest losses in the year came from Hexagon, Intralot, Lenovo Group and Ibiden. Declines in these stocks ranged from 49% to 78%. Sweden's Hexagon, a maker of measurement equipment and polymers, fell on fears a drop in construction projects globally would hurt its business. Greek lottery and gaming systems and services provider Intralot dropped after renegotiating its Turkish contract at much reduced rates. Chinese PC vendor Lenovo Group was adversely affected by the slowdown in global PC demand and intensifying competition. Restructuring costs also dampened earnings. Ibiden, a Japanese manufacturer of electronic parts and ceramics, fell due to production issues and a weaker demand for its semiconductor packaging.

2008 was definitely a punishing year for world equity markets and Fund shareholders. The adjustments we are facing in the global economy are likely to continue and as a result the Fund continues to shy away from those areas still most exposed to economic distress (financials, consumer stocks) and is focused on less cyclical areas (health care, business services and others). While valuations have become much more attractive, we are awaiting further signs that economic fundamentals have begun to improve before returning to more economically sensitive investments.

International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investing in emerging markets may involve greater risks than investing in more developed countries.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

*Effective October 1, 2008, Standard & Poor's implemented a new naming convention for its family of indexes. Prior to the renaming, the S&P Developed Ex-U.S. Between $2 Billion and $10 Billion Index was known as the S&P/Citigroup World ex-US Cap Range $2-10B Index. This index name change was not expected to result in any alterations to the constitution or calculation of the index and does not in any way affect the manner in which the Fund is managed or the investment objective or principal investment strategy of the Fund, which remain unchanged.

4

Wanger International Select 2008 Annual Report

Growth of a $10,000 Investment in Wanger International Select

Total return for each period,

February 1, 1999 (inception date) through December 31, 2008

This graph compares the results of $10,000 invested in Wanger International Select on February 1, 1999 (the date the Fund began operations) through December 31, 2008, to the S&P Developed Ex-U.S. Between $2 Billion and $10 Billion Index, with dividends and capital gains reinvested. Performance results reflect any fee waivers or reimbursements of Fund expenses by CWAM or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower. Performance shown here is past performance, which cannot guarantee future results. Current performance may be higher or lower. The investment return and principal value of an investment in the Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Performance changes over time. Current returns for the Fund may be different than that shown. For daily and most recent month-end p erformance updates, please contact us at 1-888-4-WANGER.

Results to December 31, 2008

| | | 4th quarter | | 1 year | |

| Wanger International Select | | | -21.76 | % | | | -44.35 | % | |

S&P Developed Ex-U.S.

Between $2 Billion and

$10 Billion Index | | | -20.82 | | | | -45.57 | | |

| MSCI EAFE Index | | | -19.95 | | | | -43.38 | | |

NAV as of 12/31/08: $12.01

Performance numbers reflect all Fund expenses but do not include any insurance charge imposed by your insurance company's separate accounts. If performance included the effect of these additional charges, it would be lower.

The Fund's annual operating expense ratio is 1.18%. The annual operating expense ratio is as stated in the Fund's prospectus that is current as of the date of this report. Differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and expense reimbursements as well as different time periods used in calculating the ratios.

All results shown assume reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

The S&P Developed Ex-U.S. Between $2 Billion and $10 Billion Index, which is the Fund's primary benchmark, is a subset of the broad market selected by the index sponsor representing the mid-cap developed market, excluding the United States. The Morgan Stanley Capital International Europe, Australasia, Far East (MSCI EAFE) Index is a capitalization-weighted index that tracks the total return of common stocks in 21 developed market countries within Europe, Australia and the Far East. Indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings.

Top 5 Countries

As a percentage of net assets, as of 12/31/08

| Japan | | | 25.0 | % | |

| United Kingdom | | | 16.1 | | |

| United States | | | 10.2 | | |

| Germany | | | 6.2 | | |

| France | | | 6.1 | | |

Top 10 Holdings

As a percentage of net assets, as of 12/31/08

1. Jupiter Telecommunications (Japan)

Largest Cable Service Provider in Japan | | | 6.7 | % | |

2. Cephalon (United States)

Specialty Pharmaceuticals for Pain,

Central Nervous System & Oncology | | | 4.9 | | |

3. Serco (United Kingdom)

Facilities Management | | | 4.2 | | |

4. Rhoen-Klinikum (Germany)

Health Care Services | | | 4.1 | | |

5. Capita Group (United Kingdom)

White Collar, Back Office Outsourcing | | | 4.0 | | |

6. SES Global (France)

Satellite Broadcasting Services | | | 3.8 | | |

7. Intertek Testing (United Kingdom)

Testing, Inspection & Certification Services | | | 3.6 | | |

8. Red Electrica de Espana (Spain)

Spanish Power Grid | | | 3.3 | | |

9. Synthes (Switzerland)

Products for Orthopedic Surgery | | | 3.0 | | |

10. Nintendo (Japan)

Entertainment Software & Hardware | | | 3.0 | | |

5

Wanger International Select 2008 Annual Report

Wanger International Select

Statement of Investments December 31, 2008

Number of

Shares | | | | Value | |

| | | Common Stocks – 96.8% | |

| | | Europe – 50.1% | |

| | | United Kingdom – 16.1% | |

| | 190,000 | | | Serco

Facilities Management | | | $1,236,614

| | |

| | 110,000 | | | Capita Group

White Collar, Back Office Outsourcing | | | 1,172,050

| | |

| | 93,000 | | | Intertek Testing

Testing, Inspection & Certification Services | | | 1,053,431

| | |

| | 260,000 | | | RPS Group

Environmental Consulting & Planning | | | 527,686

| | |

| | 125,000 | | | Informa Group

Global Publisher & Event Organizer | | | 443,509

| | |

| | 26,594 | | | Standard Chartered

UK Bank with Main Operations in Asia | | | 339,959

| | |

| | | | | | | | 4,773,249 | | |

| | | Germany – 6.2% | |

| | 50,000 | | | Rhoen-Klinikum

Health Care Services | | | 1,201,688

| | |

| | 13,400 | | | Wincor Nixdorf

Retail POS Systems & ATM Machines | | | 638,885

| | |

| | | | | | | | 1,840,573 | | |

| | | France – 6.1% | |

| | 58,000 | | | SES Global

Satellite Broadcasting Services | | | 1,116,533

| | |

| | 7,600 | | | Neopost

Postage Meter Machines | | | 687,902

| | |

| | | | | | | | 1,804,435 | | |

| | | Switzerland – 6.0% | |

| | 7,100 | | | Synthes

Products for Orthopedic Surgery | | | 897,484

| | |

| | 9,400 | | | Kuehne & Nagel

Freight Forwarding/Logistics | | | 609,460

| | |

| | 2,000 | | | Swatch Group

Watch & Electronics Manufacturer | | | 279,371

| | |

| | | | | | | | 1,786,315 | | |

| | | Ireland – 5.0% | |

| | 260,000 | | | United Drug

Irish Pharmaceutical Wholesaler & Outsourcer | | | 805,717

| | |

| | 21,000 | | | Aryzta (a)

Baked Goods | | | 672,475

| | |

| | | | | | | | 1,478,192 | | |

Number of

Shares | | | | Value | |

| | | Netherlands – 3.5% | |

| | 50,000 | | | QIAGEN (a)

Life Science Company; DNA/RNA Purification | | $ | 873,774 |

| |

| | 21,000 | | | Aalberts Industries

Flow Control & Heat Treatment | | | 150,015 |

| |

| | | | | | | | 1,023,789 | | |

| | | Spain – 3.2% | |

| | 19,000 | | | Red Electrica de Espana

Spanish Power Grid | | | 962,587 |

| |

| | | Sweden – 1.5% | |

| | 90,000 | | | Hexagon

Measurement Equipment & Polymers | | | 440,868 |

| |

| | | Denmark – 1.3% | |

| | 4,700 | | | Novozymes

Industrial Enzymes | | | 374,443 |

| |

| | | Greece – 1.2% | |

| | 82,000 | | | Intralot

Lottery & Gaming Systems & Services | | | 342,461 |

| |

| | | | | Total Europe | | | 14,826,912 | | |

| | | Asia – 29.4% | |

| | | Japan – 25.0% | |

| | 1,900 | | | Jupiter Telecommunications

Largest Cable Service Provider in Japan | | | 1,980,121 |

| |

| | 2,300 | | | Nintendo

Entertainment Software & Hardware | | | 883,648 |

| |

| | 16,900 | | | Benesse

Education Service Provider | | | 738,624 |

| |

| | 130,000 | | | Kansai Paint

Paint Producer in Japan, India,

China & Southeast Asia | | | 664,394 |

| |

| | 39,900 | | | Rohto Pharmaceutical

Health & Beauty Products | | | 554,622 |

| |

| | 85 | | | Orix JREIT

Diversified REIT | | | 405,501 |

| |

| | 45,000 | | | Kamigumi

Port Cargo Handling & Logistics | | | 402,995 |

| |

| | 7,600 | | | Daito Trust Construction

Apartment Builder | | | 397,946 |

| |

See accompanying notes to financial statements.

6

Wanger International Select 2008 Annual Report

Wanger International Select

Statement of Investments December 31, 2008

Number of

Shares | | | | Value | |

| | | Japan – 25.0% (cont) | |

| | 35 | | | Nippon Building Fund

Office REIT | | | $384,156

| | |

| | 8,100 | | | Ryohin Keikaku

Specialty Retail | | | 384,007

| | |

| | 14,000 | | | Aeon Mall

Suburban Shopping Mall Developer,

Owner & Operator | | | 270,282

| | |

| | 23,000 | | | Suruga Bank

Regional Bank | | | 227,787

| | |

| | 5,000 | | | Ain Pharmaciez

Dispensing Pharmacy/Drugstore Operator | | | 110,668

| | |

| | | | | | | | 7,404,751 | | |

| | | South Korea – 2.2% | |

| | 30,600 | | | Woongjin Coway (a)

South Korean Household Appliance

Rental Service Provider | | | 657,435

| | |

| | | Hong Kong – 1.6% | |

| | 30,500 | | | Hong Kong Exchanges and Clearing

Hong Kong Equity & Derivatives

Market Operator | | | 292,413

| | |

| | 1,200,000 | | | NagaCorp

Monopoly Casino in Central Cambodia | | | 166,107

| | |

| | | | | | | | 458,520 | | |

| | | Singapore – 0.6% | |

| | 180,000 | | | ComfortDelGro

Taxi & Mass Transit Service | | | 182,213

| | |

| | | | | Total Asia | | | 8,702,919 | | |

| | | Other Countries – 16.3% | |

| | | United States – 10.2% | |

| | 19,000 | | | Cephalon (a)

Specialty Pharmaceuticals for Pain,

Central Nervous System & Oncology | | | 1,463,760

| | |

| | 8,100 | | | Diamond Offshore

Contract Driller | | | 477,414

| | |

| | 24,400 | | | BioMarin (a)

Biotech Focused on Orphan Diseases | | | 434,320

| | |

Number of

Shares | | | | Value | |

| | 11,100 | | | Alexion Pharmaceuticals (a)

Biotech Focused on Orphan Diseases | | | $401,709

| | |

| | 7,800 | | | Bristow (a)

Largest Provider of Helicopter

Services to Offshore

Oil & Gas Producers | | | 208,962

| | |

| | 1,100 | | | Oceaneering International (a)

Provider of Sub-sea Services &

Manufactured Products | | | 32,054

| | |

| | | | | | | | 3,018,219 | | |

| | | South Africa – 2.4% | |

| | 39,000 | | | Naspers

Media & Education in Africa &

Other Emerging Markets | | | 708,905

| | |

| | | Australia – 1.6% | |

| | 135,000 | | | Sino Gold (a)

Gold Mining in The People's Republic of China | | | 473,054

| | |

| | | Israel – 1.5% | |

| | 66,000 | | | Israel Chemicals

Producer of Potash, Phosphates,

Bromine & Specialty Chemicals | | | 461,437

| | |

| | | Canada – 0.6% | |

| | 92,050 | | | Pacific Rubiales Energy (a)(b) | | | 161,664 | | |

| | 46,025 | | | Pacific Rubiales Energy-Warrants (a)(b) | | | 12,180 | | |

| | 450 | | | Pacific Rubiales Energy (a)

Oil Production & Exploration in Colombia | | | 798

| | |

| | | | | | | | 174,642 | | |

| | | | | Total Other Countries | | | 4,836,257 | | |

| | | Latin America – 1.0% | |

| | | Chile – 1.0% | |

| | 12,000 | | | Sociedad Quimica y Minera de Chile - ADR

Producer of Specialty Fertilizers,

Lithium & Iodine | | | 292,680

| | |

| | | | | Total Latin America | | | 292,680 | | |

| Total Common Stocks (Cost: $33,074,992) – 96.8% | | | 28,658,768 | | |

See accompanying notes to financial statements.

7

Wanger International Select 2008 Annual Report

Wanger International Select

Statement of Investments December 31, 2008

Principal

Amount | | | | Value | |

| | | Short-Term Obligation – 2.5% | |

| | | >Repurchase Agreement – 2.5% | |

| $ | 731,000 | | | Repurchase Agreement with Fixed

Income Clearing Corp., dated 12/31/08,

due 1/02/09 at 0.010%, collateralized

by a U.S. Government Agency Obligation,

maturing 11/17/15, market value $750,619 (repurchase proceeds $731,000) | | $ | 731,000 | | |

| | | | 731,000 | | |

| Total Short-Term Obligation (Cost: $731,000) | | | 731,000 | | |

| Total Investments (Cost: $33,805,992) – 99.3% (c)(d) | | | 29,389,768 | | |

| Cash and Other Assets Less Liabilities – 0.7% | | | 214,666 | | |

| Total Net Assets – 100.0% | | $ | 29,604,434 | | |

Notes to Statement of Investments:

(a) Non-income producing security.

(b) Denotes a restricted security, which is subject to restrictions on resale under federal securities laws. These securities are valued at their fair value determined in good faith under consistently applied procedures established by the Board of Trustees. At December 31, 2008, these securities amounted to $173,844 which represents 0.59% of total net assets.

Additional information on these securities is as follows:

Security | | Acquisition

Date | |

Shares | |

Cost | |

Value | |

Pacific Rubiales

Energy | | 7/12/2007 | | | 92,050 | | | $ | 369,594 | | | $ | 161,664 | | |

Pacific Rubiales

Energy - Warrants | | 7/12/2007 | | | 46,025 | | | | 78,779 | | | | 12,180 | | |

| | | | | | | $ | 448,373 | | | $ | 173,844 | | |

(c) At December 31, 2008, for federal income tax purposes cost of investments was $34,191,506 and net unrealized depreciation was $4,801,738 consisting of gross unrealized appreciation of $3,696,427 and gross unrealized depreciation of $8,498,165.

(d) On December 31, 2008, the Fund's total investments were denominated in currencies as follows:

| Currency | | Value | | Percentage of

Net Assets | |

| Euro | | $ | 7,452,037 | | | | 25.2 | | |

| Japanese Yen | | | 7,404,751 | | | | 25.0 | | |

| British Pound | | | 4,773,249 | | | | 16.1 | | |

| U.S. Dollar | | | 4,041,899 | | | | 13.7 | | |

| Swiss Franc | | | 1,786,315 | | | | 6.0 | | |

Other currencies less than 5%

of total net assets | | | 3,931,517 | | | | 13.3 | | |

| Cash and other assets less liabilities | | | 214,666 | | | | 0.7 | | |

| | | $ | 29,604,434 | | | | 100.0 | | |

ADR = American Depositary Receipts

See accompanying notes to financial statements.

8

Wanger International Select 2008 Annual Report

Wanger International Select

Portfolio Diversification December 31, 2008

At December 31, 2008, the Fund's portfolio investments as a percentage of net assets was diversified as follows:

| | |

Value | | Percentage

of Net Assets | |

| Industrial Goods & Services | |

| Outsourcing Services | | $ | 2,408,664 | | | | 8.2 | | |

| Industrial Materials & Specialty Chemicals | | | 1,792,954 | | | | 6.1 | | |

| Other Industrial Services | | | 1,662,891 | | | | 5.6 | | |

| Machinery | | | 687,902 | | | | 2.3 | | |

| Construction | | | 397,946 | | | | 1.3 | | |

| Conglomerates | | | 150,015 | | | | 0.5 | | |

| | | | 7,100,372 | | | | 24.0 | | |

| Information | |

| CATV | | | 1,980,121 | | | | 6.7 | | |

| Satellite Broadcasting & Services | | | 1,116,533 | | | | 3.8 | | |

| Consumer Software | | | 883,648 | | | | 3.0 | | |

| TV Broadcasting | | | 708,905 | | | | 2.4 | | |

| Computer Hardware & Related Equipment | | | 638,885 | | | | 2.1 | | |

| Business Information & Marketing Services | | | 527,686 | | | | 1.8 | | |

| Publishing | | | 443,509 | | | | 1.5 | | |

| Instrumentation | | | 440,868 | | | | 1.5 | | |

| Financial Processors | | | 292,413 | | | | 1.0 | | |

| | | | 7,032,568 | | | | 23.8 | | |

| Health Care | |

| Pharmaceuticals | | | 2,269,477 | | | | 7.7 | | |

| Medical Equipment & Devices | | | 1,299,193 | | | | 4.4 | | |

| Health Care Services | | | 1,201,688 | | | | 4.0 | | |

| Medical Supplies | | | 873,774 | | | | 2.9 | | |

| Biotechnology & Drug Delivery | | | 434,320 | | | | 1.5 | | |

| | | | 6,078,452 | | | | 20.5 | | |

| | |

Value | | Percentage

of Net Assets | |

| Consumer Goods & Services | |

| Other Consumer Services | | $ | 1,396,059 | | | | 4.7 | | |

| Retail | | | 764,956 | | | | 2.6 | | |

| Food & Beverage | | | 672,475 | | | | 2.3 | | |

| Nondurables | | | 554,622 | | | | 1.9 | | |

| Casinos & Gaming | | | 508,568 | | | | 1.7 | | |

| Other Durable Goods | | | 279,371 | | | | 0.9 | | |

| | | | 4,176,051 | | | | 14.1 | | |

| Other Industries | |

| Regulated Utilities | | | 962,587 | | | | 3.2 | | |

| Real Estate | | | 789,657 | | | | 2.7 | | |

| Transportation | | | 585,208 | | | | 2.0 | | |

| | | | 2,337,452 | | | | 7.9 | | |

| Energy & Minerals | |

| Oil Services | | | 718,430 | | | | 2.4 | | |

| Mining | | | 473,054 | | | | 1.6 | | |

| Oil & Gas Producers | | | 174,642 | | | | 0.6 | | |

| | | | 1,366,126 | | | | 4.6 | | |

| Finance | |

| Banks | | | 567,747 | | | | 1.9 | | |

| | | | 567,747 | | | | 1.9 | | |

| Total Common Stocks | | | 28,658,768 | | | | 96.8 | | |

| Short-Term Obligation | | | 731,000 | | | | 2.5 | | |

| Total Investments | | | 29,389,768 | | | | 99.3 | | |

Cash and Other Assets

Less Liabilities | | | 214,666 | | | | 0.7 | | |

| Net Assets | | $ | 29,604,434 | | | | 100.0 | | |

See accompanying notes to financial statements.

9

Wanger International Select 2008 Annual Report

Statement of Assets and Liabilities

December 31, 2008

| Assets: | |

| Investments, at cost | | $ | 33,805,992 | | |

| Investments, at value | | $ | 29,389,768 | | |

| Cash | | | 787 | | |

| Foreign currency (cost of $21,191) | | | 20,894 | | |

| Receivable for: | |

| Investments sold | | | 50,769 | | |

| Fund shares sold | | | 165,701 | | |

| Dividends | | | 33,520 | | |

| Foreign tax reclaims | | | 20,545 | | |

| Other assets | | | 299 | | |

| Total Assets | | | 29,682,283 | | |

| Liabilities: | |

| Payable for: | |

| Investments purchased | | | 5,107 | | |

| Fund shares repurchased | | | 13,918 | | |

| Investment advisory fee | | | 22,260 | | |

| Administration fee | | | 1,184 | | |

| Transfer agent fee | | | 14 | | |

| Trustees' fees | | | 1 | | |

| Audit fee | | | 15,470 | | |

| Custody fee | | | 4,521 | | |

| Reports to shareholders | | | 7,743 | | |

| Chief compliance officer expenses | | | 89 | | |

| Trustees' deferred compensation plan | | | 6,485 | | |

| Other liabilities | | | 1,057 | | |

| Total Liabilities | | | 77,849 | | |

| Net Assets | | $ | 29,604,434 | | |

| Composition of Net Assets: | |

| Paid-in capital | | $ | 38,965,734 | | |

| Undistributed net investment income | | | 544,737 | | |

| Accumulated net realized loss | | | (5,491,695 | ) | |

| Net unrealized appreciation (depreciation) on: | |

| Investments | | | (4,416,224 | ) | |

| Foreign currency translations | | | 1,882 | | |

| Net Assets | | $ | 29,604,434 | | |

| Fund Shares Outstanding | | | 2,464,477 | | |

Net asset value, offering price and redemption

price per share | | $ | 12.01 | | |

Statement of Operations

For the Year Ended December 31, 2008

| Investment Income: | |

| Dividends (net of foreign taxes withheld of $79,213) | | $ | 1,179,560 | | |

| Interest income | | | 28,405 | | |

| Total Investment Income | | | 1,207,965 | | |

| Expenses: | |

| Investment advisory fee | | | 485,781 | | |

| Administration fee | | | 25,840 | | |

| Transfer agent fee | | | 150 | | |

| Trustees' fees | | | 3,967 | | |

| Custody fee | | | 54,682 | | |

| Chief compliance officer expenses (See Note 4) | | | 1,611 | | |

| Other expenses (See Note 5) | | | 69,863 | | |

| Total Expenses | | | 641,894 | | |

| Custody earnings credit | | | (74 | ) | |

| Net Expenses | | | 641,820 | | |

| Net Investment Income | | | 566,145 | | |

Net Realized and Unrealized Gain (Loss) on

Investments and Foreign Currency: | |

| Net realized loss on: | |

| Investments | | | (5,470,637 | ) | |

| Foreign currency transactions | | | (8,921 | ) | |

| Net realized loss | | | (5,479,558 | ) | |

Net change in unrealized appreciation

(depreciation) on: | | | | | |

| Investments | | | (22,162,132 | ) | |

| Foreign currency translations | | | 598 | | |

Net change in unrealized

appreciation (depreciation) | | | (22,161,534 | ) | |

| Net Loss | | | (27,641,092 | ) | |

| Net Decrease in Net Assets from Operations | | $ | (27,074,947 | ) | |

See accompanying notes to financial statements.

10

Wanger International Select 2008 Annual Report

Statement of Changes in Net Assets

| | | Year ended December 31, | |

| Increase (Decrease) in Net Assets | | 2008 | | 2007 | |

| Operations: | |

| Net investment income | | $ | 566,145 | | | $ | 256,588 | | |

| Net realized gain (loss) on investments and foreign currency transactions | | | (5,479,558 | ) | | | 14,866,303 | | |

Net change in unrealized appreciation (depreciation) on investments

and foreign currency translations | | | (22,161,534 | ) | | | (1,765,746 | ) | |

| Net Increase (Decrease) in Net Assets from Operations | | | (27,074,947 | ) | | | 13,357,145 | | |

| Distributions to Shareholders: | |

| From net investment income | | | (215,563 | ) | | | (491,093 | ) | |

| From net realized gains | | | (14,461,904 | ) | | | (7,887,030 | ) | |

| Total Distributions to Shareholders | | | (14,677,467 | ) | | | (8,378,123 | ) | |

| Share Transactions: | |

| Subscriptions | | | 4,503,145 | | | | 13,254,652 | | |

| Distributions reinvested | | | 14,677,467 | | | | 8,378,123 | | |

| Redemptions | | | (21,308,289 | ) | | | (15,721,645 | ) | |

| Net Increase (Decrease) from Share Transactions | | | (2,127,677 | ) | | | 5,911,130 | | |

| Total Increase (Decrease) in Net Assets | | | (43,880,091 | ) | | | 10,890,152 | | |

| Net Assets: | |

| Beginning of period | | | 73,484,525 | | | | 62,594,373 | | |

| End of period | | $ | 29,604,434 | | | $ | 73,484,525 | | |

| Undistributed net investment income at end of period | | $ | 544,737 | | | $ | 214,513 | | |

See accompanying notes to financial statements.

11

Wanger International Select 2008 Annual Report

Financial Highlights

| | | Year Ended December 31, | |

| Selected data for a share outstanding throughout each period | | 2008 | | 2007 | | 2006 | | 2005 | | 2004 | |

| Net Asset Value, Beginning of Period | | $ | 28.07 | | | $ | 26.62 | | | $ | 19.63 | | | $ | 17.19 | | | $ | 13.87 | | |

| Income from Investment Operations: | |

| Net investment income (a) | | | 0.21 | | | | 0.10 | | | | 0.11 | | | | 0.13 | | | | 0.04 | | |

Net realized and unrealized gain (loss) on investments

and foreign currency | | | (10.31 | ) | | | 4.92 | | | | 6.94 | | | | 2.66 | | | | 3.33 | | |

| Total from Investment Operations | | | (10.10 | ) | | | 5.02 | | | | 7.05 | | | | 2.79 | | | | 3.37 | | |

| Less Distributions to Shareholders: | |

| From net investment income | | | (0.09 | ) | | | (0.21 | ) | | | (0.06 | ) | | | (0.35 | ) | | | (0.05 | ) | |

| From net realized gains | | | (5.87 | ) | | | (3.36 | ) | | | — | | | | — | | | | — | | |

| Total Distributions to Shareholders | | | (5.96 | ) | | | (3.57 | ) | | | (0.06 | ) | | | (0.35 | ) | | | (0.05 | ) | |

| Net Asset Value, End of Period | | $ | 12.01 | | | $ | 28.07 | | | $ | 26.62 | | | $ | 19.63 | | | $ | 17.19 | | |

| Total Return (b) | | | (44.35 | )% | | | 21.78 | % | | | 36.00 | % | | | 16.43 | %(c) | | | 24.34 | % | |

| Ratios to Average Net Assets/Supplemental Data: | |

| Net expenses (d) | | | 1.24 | % | | | 1.18 | % | | | 1.19 | % | | | 1.32 | % | | | 1.43 | % | |

| Net investment income (d) | | | 1.10 | % | | | 0.37 | % | | | 0.47 | % | | | 0.76 | % | | | 0.29 | % | |

| Waiver | | | — | | | | — | | | | — | | | | 0.00 | %(e) | | | — | | |

| Portfolio turnover rate | | | 68 | % | | | 69 | % | | | 61 | % | | | 48 | % | | | 71 | % | |

| Net assets, end of period (000's) | | $ | 29,604 | | | $ | 73,485 | | | $ | 62,594 | | | $ | 44,026 | | | $ | 35,232 | | |

(a) Net investment income per share was based upon the average shares outstanding during the period.

(b) Total return at net asset value assuming all distributions reinvested.

(c) Had the investment advisor not waived a portion of expenses, total return would have been reduced.

(d) The benefits derived from custody fees paid indirectly had an impact of less than 0.01%.

(e) Rounds to less than 0.01%.

See accompanying notes to financial statements.

12

Wanger International Select 2008 Annual Report

Notes to Financial Statements

1. Nature of Operations

Wanger International Select (the "Fund"), is a series of Wanger Advisors Trust (the "Trust"), an open-end management investment company organized as a Massachusetts business trust. The investment objective of the Fund is to seek long-term capital appreciation. The Fund is available only for allocation to certain life insurance company separate accounts established for the purpose of funding qualified and non-qualified variable annuity contracts and variable life insurance policies and may also be offered directly to certain types of pension plans and retirement arrangements.

2. Significant Accounting Policies

Security valuation

Securities of the Fund are valued at market value or, if a market quotation for a security is not readily available or is deemed not to be reliable because of events or circumstances that have occurred between the market quotation and the time as of which the security is to be valued, the security is valued at its fair value determined in good faith under consistently applied procedures established by the Board of Trustees. A security traded on a securities exchange or in an over-the-counter market in which transaction prices are reported is valued at the last sales price at the time of valuation. A security traded principally on NASDAQ is valued at the NASDAQ official closing price. A security for which there is no reported sale on the valuation date is valued at the latest bid quotation. Short-term investments maturing in 60 days or less are valued at amortized cost, which approximates market value. A security for which a mark et quotation is not readily available and any other assets are valued at its fair value determined in good faith under consistently applied procedures established by the Board of Trustees. The Trust has retained an independent statistical fair value pricing service to assist in the fair valuation process for securities principally traded in a foreign market in order to adjust for possible changes in value that may occur between the close of the foreign market and the time as of which the securities are to be valued. If a security is valued at fair value, that value may be different from the last quoted market price for the security.

On January 1, 2008, the Fund adopted Statement of Financial Accounting Standards No. 157, Fair Value Measurements ("SFAS 157"). Under SFAS 157, various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

• Level 1—quoted prices in active markets for identical securities

• Level 2—other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk and others)

• Level 3—significant unobservable inputs (including management's own assumptions in determining the value of investments)

The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Examples of the types of securities in which the Fund would typically invest and how they are classified within this SFAS 157 hierarchy are as follows. Typical level 1 securities include exchange traded domestic equities, mutual funds whose NAVs are published each day and exchange traded foreign equities that are not statistically fair valued. Typical level 2 securities include exchange traded foreign equities that are statistically fair valued and short-term investments valued at amortized cost. Typical level 3 securities include any security fair valued by the Fund's Valuation Committee that relies on significant unobservable inputs.

The following table summarizes the inputs used, as of December 31, 2008, in valuing the Fund's assets:

| Valuation Inputs | | Investments in

Securities | | Other Financial

Instruments | |

| Level 1— Quoted Prices | | $ | 3,311,697 | | | $ | — | | |

| Level 2—Other Significant Observable Inputs | | | 26,078,071 | | | | — | | |

| Level 3— Significant Unobservable Inputs | | | — | | | | — | | |

| Total | | $ | 29,389,768 | | | $ | — | | |

Repurchase agreements

The Fund may engage in repurchase agreement transactions. The Fund, through its custodians, receives delivery of underlying securities collateralizing each repurchase agreement. The counterparty is required to maintain collateral that is at all times at least equal to the repurchase price including interest. In the event of default or bankruptcy by the other party to the agreement, realization and/or retention of the collateral may be subject to legal proceedings.

Foreign currency translations

Values of investments denominated in foreign currencies are converted into

U.S. dollars using the spot market rate of exchange at the time of valuation. Purchases and sales of investments and dividend and interest income are translated into U.S. dollars using the spot market rate of exchange prevailing on the respective dates of such transactions. The gain or loss resulting from changes in foreign exchange rates is included with net realized and unrealized gain or loss from investments, as appropriate.

In March 2008, Statement of Financial Accounting Standards No. 161, Disclosures about Derivative Instruments and Hedging Activities—an amendment of FASB Statement No. 133 ("SFAS 161"), was issued. SFAS 161 is effective for fiscal years beginning after November 15, 2008. SFAS 161 requires additional discussion about the reporting entity's derivative instruments and hedging activities, by providing for qualitative disclosures about the objectives and strategies for using derivatives, quantitative data about the fair value of and gains and losses on derivative contracts, and details of credit-risk-related contingent features in their hedged positions. Management is evaluating the impact the application of SFAS 161 will have on the Fund's financial statement disclosures.

Security transactions and investment income

Security transactions are accounted for on the trade date (date the order to buy or sell is executed) and dividend income is recorded on the ex-dividend date, except that certain dividends from foreign securities are recorded as soon as the information is available to the Fund. Interest income is recorded on the accrual basis and includes amortization of discounts on debt obligations when required for federal income tax purposes. Realized gains and losses from security transactions are recorded on an identified cost basis.

Awards, if any, from class action litigation related to securities owned may be recorded as a reduction of cost of those securities. If the applicable securities are no longer owned, the proceeds are recorded as realized gains.

Restricted securities

Restricted securities are securities that may only be resold upon registration under federal securities laws or in transactions exempt from registration. In some cases, the issuer of restricted securities has agreed to register such securities for resale at the issuer's expense either upon demand by the Fund or in connection with another registered offering of the securities. Many restricted securities may be resold in the secondary market in transactions exempt from registration. Such restricted securities may be determined to be liquid under criteria established by the Board of Trustees. The Fund will not incur any registration costs upon such resale.

Use of estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America ("GAAP")

13

Wanger International Select 2008 Annual Report

Notes to Financial Statements

requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results may differ from those estimates.

Fund share valuation

Fund shares are sold and redeemed on a continuing basis at net asset value. Net asset value per share is determined daily as of the close of trading on the New York Stock Exchange ("the Exchange") on each day the Exchange is open for trading by dividing the total value of the Fund's investments and other assets, less liabilities, by the number of Fund shares outstanding.

Custody fees/credits

Custody fees are reduced based on the Fund's cash balances maintained with the custodian. The amount is disclosed as a reduction of total expenses in the Statement of Operations.

Federal income taxes

The Fund has complied with the provisions of the Internal Revenue Code available to regulated investment companies and, in the manner provided therein, distributes all its taxable income, as well as any net realized gain on sales of investments and foreign currency transactions reportable for federal income tax purposes. Accordingly, the Fund paid no federal income taxes and no federal income tax provision was required.

Expenses

General expenses of the Trust are allocated to the Fund and the other series of the Trust based upon relative net assets or other expense allocation methodologies determined by the nature of the expense. Expenses directly attributable to the Fund are charged to the Fund.

Foreign capital gains taxes

Gains in certain countries may be subject to foreign taxes at the fund level, at rates ranging from 10%-15%. The Fund accrues for such foreign taxes on net realized and unrealized gains at the appropriate rate for each jurisdiction.

Distributions to shareholders

Distributions to shareholders are recorded on the ex-date.

Indemnification

In the normal course of business, the Trust on behalf of the Fund enters into contracts that contain a variety of representations and warranties and that provide general indemnities. The Fund's maximum exposure under these arrangements is unknown, as this would involve future claims against the Fund. Also under the Trust's organizational documents, the trustees and officers of the Trust are indemnified against certain liabilities that may arise out of their duties to the Trust. However based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be minimal.

3. Federal Tax Information

The timing and character of income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP. Reclassifications are made to the Fund's capital accounts for permanent tax differences to reflect income and gains available for distribution (or available capital loss carryforwards) under income tax regulations.

For the year ended December 31, 2008, permanent book and tax basis differences resulting primarily from differing treatments for foreign currency transactions and distribution reclassifications were identified and reclassified among the components of the Fund's net assets as follows:

Undistributed

Net Investment

Income | | Accumulated

Net Realized

Loss | | Paid-In Capital | |

| $ | (20,358 | ) | | $ | 20,358 | | | $ | — | | |

Net investment income and net realized gains/(losses), as disclosed on the Statement of Operations, and net assets were not affected by this reclassification.

The tax character of distributions paid during the years ended December 31, 2008 and December 31, 2007 were as follows:

| | | December 31, 2008 | | December 31, 2007 | |

Distributions paid from:

Ordinary Income* | | $ | 3,006,152 | | | $ | 1,250,481 | | |

| Long-Term Capital Gains | | | 11,671,315 | | | | 7,127,642 | | |

* For tax purposes short-term capital gain distributions, if any, are considered ordinary income distributions.

As of December 31, 2008, the components of distributable earnings on a tax basis were as follows:

Undistributed

Ordinary

Income | | Undistributed

Long-Term

Capital Gains | | Net Unrealized

Depreciation* | |

| $ | 544,737 | | | $ | — | | | $ | (4,801,738 | ) | |

* The differences between book-basis and tax-basis net unrealized appreciation/(depreciation) are primarily due to deferral of losses from wash sales.

The following capital loss carryforwards, determined as of December 31, 2008, may be available to reduce taxable income arising from future net realized gains on investments, if any, to the extent permitted by the Internal Revenue Code:

Year of

Expiration | | Capital Loss

Carryforward | |

| | 2016 | | | $ | 2,630,085 | | |

Under current tax rules, certain currency and capital losses realized after October 31 may be deferred and treated as occurring on the first day of the following fiscal year. As of December 31, 2008, post-October capital losses of $2,476,096 attributed to security transactions were deferred to January 1, 2009.

Under Financial Accounting Standards Board ("FASB") Interpretation No. 48, Accounting for Uncertainty in Income Taxes—an Interpretation of FASB Statement No. 109 ("FIN 48") management determines whether a tax position of the Fund is more likely than not to be sustained upon examination by the applicable taxing authority, including resolution of any related appeals or litigation processes, based on the technical merits of the position. The tax benefit to be recognized is measured as the largest amount of benefit that is greater than fifty percent likely of being realized upon ultimate settlement. Management has evaluated the known implications of FIN 48 on its computation of net assets for the Fund. As a result of this evaluation, management believes that FIN 48 does not have any effect on the Fund's financial statements. However, management's conclusions regarding FIN 48 may be subject to review and adjustment at a later date based on factors including, but not limited to, further implementation guidance from the FASB, new tax laws, regulations, and

14

Wanger International Select 2008 Annual Report

Notes to Financial Statements

administrative interpretations (including relevant court decisions). The Fund's federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service. The Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

4. Transactions With Affiliates

Columbia Wanger Asset Management, L.P. ("CWAM") is a wholly owned subsidiary of Columbia Management Group, LLC, ("Columbia Management") which in turn is an indirect wholly owned subsidiary of Bank of America Corporation ("BOA"). CWAM furnishes continuing investment supervision to the Fund and is responsible for the overall management of the Fund's business affairs.

Under the Fund's investment advisory agreement, management fees are accrued daily based on the Fund's average daily net assets and paid monthly to CWAM at the annual rates shown in the table below:

| Average Daily Net Assets | | Annual Fee Rate | |

| Up to $500 million | | | 0.94 | % | |

| $500 million and over | | | 0.89 | % | |

For the year ended December 31, 2008, the Fund's effective investment advisory fee rate was 0.94% of average daily net assets.

Through April 30, 2009, CWAM will reimburse the Fund to the extent that ordinary operating expenses (exclusive of brokerage commissions, interest, taxes and extraordinary expenses, but inclusive of custodial charges relating to overdrafts, if any), after giving effect to any balance credits from the Fund's custodian, exceed an annual percentage of 1.45% of average daily net assets. There was no reimbursement for the year ended December 31, 2008.

CWAM provides administrative services and receives an administration fee from the Fund. Effective August 1, 2008, CWAM provides administrative services and receives an administration fee from the Fund at the following annual rates:

Wanger Advisors Trust Aggregate

Average Daily Net Assets of the Trust: | | Annual Fee Rate | |

| Up to $4 billion | | | 0.05 | % | |

| $4 billion to $6 billion | | | 0.04 | % | |

| $6 billion to $8 billion | | | 0.03 | % | |

| $8 billion and over | | | 0.02 | % | |

Prior to August 1, 2008, administration fees were accrued daily and paid monthly to CWAM at the annual rate of 0.05%.

For the year ended December 31, 2008, the Fund's effective administration fee rate was 0.05% of average daily net assets. CWAM has delegated to Columbia Management Advisors, LLC ("Columbia"), an indirect, wholly owned subsidiary of BOA, the responsibility for certain administrative services.

Certain officers and trustees of the Trust are also officers of CWAM. The Trust makes no direct payments to its officers and trustees who are affiliated with CWAM.

The Board of Trustees appointed a Chief Compliance Officer to the Trust in accordance with federal securities regulations. The Fund, along with other affiliated funds, pays its pro-rata share of the expenses associated with the Office of the Chief Compliance Officer. These expenses are disclosed separately as "Chief compliance officer expenses" in the Statement of Operations.

The Trust offers a deferred compensation plan for its independent trustees. Under that plan, a trustee may elect to defer all or a portion of his or her compensation. Amounts deferred are retained by the Trust and represent an unfunded obligation of the Trust. The value of amounts deferred is determined by reference to the change in value of Class Z shares of one or more series of Columbia Acorn Trust or a money market fund as specified by the trustee. Benefits under the deferred compensation plan are payable when the trustee ceases to be a member of the Board of Trustees.

Columbia Management Distributors, Inc. (the "Distributor"), an affiliate of Columbia and an indirect, wholly owned subsidiary of BOA, serves as the principal underwriter of the Trust and receives no compensation from the Fund for its services.

Columbia Management Services, Inc. (the "Transfer Agent"), an affiliate of Columbia and an indirect, wholly owned subsidiary of BOA, provides shareholder services to the Fund and has subcontracted with Boston Financial Data Services ("BFDS") to serve as subtransfer agent. For such services, the Transfer Agent receives a fee, paid monthly, at the annual rate of $21.00 per open account. . The Transfer Agent also receives reimbursement for certain out-of-pocket expenses.

During the year ended December 31, 2008, the Fund engaged in purchase and sales transactions with funds that have a common investment advisor (or affiliated investment advisors), common directors/trustees, and/or common officers. Those purchase and sale transactions complied with provisions of Rule 17a-7 under the Investment Company Act of 1940 and were $- and $656,591, respectively.

5. Borrowing Arrangements

The Trust participates in a $150 million credit facility, which was entered into to facilitate portfolio liquidity. Interest is charged to each participating fund based on its borrowings at a rate per annum equal to the Federal Funds rate plus 0.50%. In addition, a commitment fee of 0.08% per annum of the unutilized line of credit is accrued and apportioned among the participating funds based on their relative net assets. The commitment fee is included in "Other expenses" in the Statement of Operations. No amounts were borrowed by the Fund under this facility during the year ended December 31, 2008. The Trust enters into this line of credit for one year durations. The Trust has already secured the line of credit for the entire year of 2009.

6. Fund Share Transactions

Proceeds and payments on Fund shares as shown in the Statement of Changes in Net Assets are in respect of the following numbers of shares:

| | | Year Ended

December 31, 2008 | | Year Ended

December 31, 2007 | |

| Shares sold | | | 246,505 | | | | 497,815 | | |

Shares issued in reinvestment

of dividend distributions | | | 740,912 | | | | 363,318 | | |

| Less shares redeemed | | | (1,140,778 | ) | | | (595,024 | ) | |

| Net increase (decrease) in shares outstanding | | | (153,361 | ) | | | 266,109 | | |

7. Investment Transactions

The aggregate cost of purchases and proceeds from sales other than short-term obligations for the year ended December 31, 2008 were $34,205,762 and $46,633,759, respectively.

8. Legal Proceedings

CWAM, Columbia Acorn Trust (another mutual fund family advised by CWAM), and the trustees of Colombia Acorn Trust (collectively, the "Columbia defendants") are named as defendants in class and derivative complaints that have been consolidated in a Multi-District Action (the "MDL Action") in the federal district court of Maryland. These lawsuits contend that defendants permitted certain investors to market time their trades in certain Columbia Acorn Funds. The MDL Action is ongoing. However, all claims against the Trust and the independent trustees of Columbia Acorn Trust have been dismissed.

Columbia Acorn Trust and CWAM are also defendants in a class action lawsuit that alleges, in summary, that Columbia Acorn Trust and CWAM

15

Wanger International Select 2008 Annual Report

Notes to Financial Statements

exposed shareholders of Columbia Acorn International Fund to trading by market timers by allegedly: (a) failing to properly evaluate daily whether a significant event affecting the value of the fund's securities had occurred after foreign markets had closed but before the calculation of the funds' net asset value ("NAV"); (b) failing to implement the fund's portfolio valuation and share pricing policies and procedures; and (c) failing to know and implement applicable rules and regulations concerning the calculation of NAV (the "Fair Valuation Lawsuit"). The Seventh Circuit ruled that the plaintiffs' state law claims were preempted under federal law resulting in the dismissal of plaintiffs' complaint. Plaintiffs appealed the Seventh Circuit's ruling to the United States Supreme Court. The Supreme Court reversed the Seventh Circuit's ruling on jurisdictional grounds and the case was ultimately remanded to the state court.

On March 21, 2005, a class action complaint was filed against the Trust and CWAM seeking to rescind the CDSC assessed upon redemption of Class B shares of the Columbia Acorn Funds due to the alleged market timing of the Columbia Acorn Funds (the "CDSC Lawsuit"). In addition to the rescission of sales charges, plaintiffs seek recovery of actual damages, attorneys' fees and costs. The case has been transferred to the MDL Action in the federal district court of Maryland.

On September 14, 2007, the plaintiffs and the Columbia defendants named in the MDL Action, including the Columbia Funds, entered into a stipulation of settlement with respect to all Columbia-related claims in the MDL Action described above, including the CDSC and Fair Valuation Lawsuits. The settlement is subject to court approval.

Columbia Acorn Trust and CWAM intend to defend these suits vigorously. CWAM believes that the lawsuits are not likely to materially affect its ability to provide investment management services to the Fund.

16

Wanger International Select 2008 Annual Report

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of Wanger International Select,

In our opinion, the accompanying statement of assets and liabilities, including the statement of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Wanger International Select (a series of the Wanger Advisors Trust, hereinafter referred to as the "Fund") at December 31, 2008, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as "financial statements") are the responsibility of the Fund's management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2008 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Chicago, Illinois

February 16, 2009

17

Wanger International Select 2008 Annual Report

Federal Income Tax Information (Unaudited)

Foreign taxes paid during the fiscal year ended December 31, 2008 of $79,180 ($0.03 per share) are expected to be passed through to shareholders. This entire amount will be eligible for shareholders to claim as a foreign tax credit.

Gross income derived from sources within foreign countries was $1,174,187 ($0.48 per share) for the fiscal year ended December 31, 2008.

Gross income derived from sources within foreign countries was $981,481 ($0.37 per share) for the fiscal year ended December 31, 2007.

1.16% of the ordinary income distributed by the Fund, for the year ended December 31, 2008 qualified for the corporate dividends received deduction.

18

Wanger International Select 2008 Annual Report

Excerpt from:

Wanger Advisors Trust

Management Fee Evaluation of the Senior Officer

Prepared Pursuant to the New York Attorney General's

Assurance of Discontinuance

May 2008

19

Wanger International Select 2008 Annual Report

Introduction