UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08748 |

|

Wanger Advisors Trust |

(Exact name of registrant as specified in charter) |

|

One Financial Center, Boston, Massachusetts | | 02111 |

(Address of principal executive offices) | | (Zip code) |

|

James R. Bordewick, Jr., Esq. Columbia Management Advisors, LLC One Financial Center Boston, MA 02111 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-617-426-3750 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2009 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Wanger International Select

2009 Annual Report

| NOT FDIC INSURED | | May Lose Value | |

|

| NOT BANK ISSUED | | No Bank Guarantee | |

|

Wanger International Select

2009 Annual Report

Table of Contents

| | 1 | | | Understanding Your Expenses | |

|

| | 2 | | | Skill and Luck | |

|

| | 4 | | | Performance Review | |

|

| | 6 | | | Statement of Investments | |

|

| | 10 | | | Statement of Assets and Liabilities | |

|

| | 10 | | | Statement of Operations | |

|

| | 11 | | | Statement of Changes in Net Assets | |

|

| | 12 | | | Financial Highlights | |

|

| | 13 | | | Notes to Financial Statements | |

|

| | 17 | | | Report of Independent Registered Public Accounting Firm | |

|

| | 18 | | | Federal Income Tax Information | |

|

| | 19 | | | Board of Trustees and Management of Wanger Advisors Trust | |

|

Columbia Wanger Asset Management, L.P. ("CWAM") is one of the leading global small- and mid-cap equity managers in the United States with 40 years of small- and mid-cap investment experience. As of December 31, 2009, CWAM manages $27.3 billion in assets and is the investment advisor to Wanger USA, Wanger International, Wanger Select, Wanger International Select (together, the "Columbia Wanger Funds") and the Columbia Acorn Family of Funds.

Columbia Wanger Asset Management, L.P. is an SEC-registered investment advisor and indirect, wholly owned subsidiary of Bank of America Corporation.

On September 29, 2009, Bank of America Corporation entered into an agreement with Ameriprise Financial, Inc. ("Ameriprise") to sell a portion of the long-term asset management business of Columbia Management Group, LLC, including 100% of CWAM.

The planned acquisition of Columbia Management's long-term asset management business by Ameriprise is subject to federal, state and international regulatory approvals.

Please read and consider the investment objectives, risks, charges and expenses for any fund carefully before investing. For a prospectus, which contains this and other important information about the Fund, contact your financial advisor or insurance company or contact 1-888-4-WANGER.

An important note: Columbia Wanger Funds are sold only to certain life insurance companies in connection with certain variable annuity contracts, variable life insurance policies and eligible qualified retirement plans.

The views expressed in "Skill and Luck" and in the Performance Review reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund. References to specific company securities should not be construed as a recommendation or investment advice.

Wanger International Select 2009 Annual Report

Understanding Your Expenses

As a Fund shareholder, you incur three types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption or exchange fees. There are also ongoing costs, which generally include investment advisory fees and other Fund expenses. Lastly, there may be additional fees or charges imposed by the insurance company that sponsors your variable annuity product. The information on this page is intended to help you understand your ongoing costs of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund's expenses

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in the Fund during the period. The information in the following table is based on an initial, hypothetical investment of $1,000, which is invested at the beginning of the period and held for the entire period. Expense information is calculated two ways and each method provides you with different results. The amount listed in the "Actual" column is calculated using actual operating expenses and total return for the Fund. The amount listed in the "Hypothetical" column assumes that the return each year is 5% before expenses and then applies the Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See "Compare with other funds" for details on using the hypothetical data.

Estimating your actual expenses

To estimate the expenses that you actually paid over the period, first you will need your account balance at the end of the period.

1. Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6.

2. In the section of the table below titled "Expenses paid during the period," you will find a dollar amount in the column labeled "Actual." Multiply this amount by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period.

July 1, 2009 – December 31, 2009

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid during

the period ($) | | Fund's annualized

expense ratio (%)* | |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | |

| Wanger International Select | | | 1,000.00 | | | | 1,000.00 | | | | 1,202.80 | | | | 1,017.90 | | | | 8.05 | | | | 7.37 | | | | 1.45 | | |

*For the six months ended December 31, 2009.

Expenses paid during the period are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 365.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Fund. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate account. The hypothetical example provided is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

Had the investment advisor and/or any of its affiliates not waived fees or reimbursed a portion of expenses, account value at the end of the period would have been reduced.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing cost of investing in a fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees that may be incurred by shareholders of other funds. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate accounts.

1

Wanger International Select 2009 Annual Report

Skill and Luck

Research has proven that it is extremely difficult for institutional investors to consistently outperform the stock market. The performance distribution among mutual funds usually looks like a bell shaped curve, with some funds outperforming, many underperforming, and the average fund underperforming its benchmark roughly by its expense ratio. I'm happy to say that the Columbia Wanger Funds have outperformed their benchmarks during many years. But researchers note that there are thousands of mutual funds, and purely random outcomes will lead some funds to outperform. This raises an interesting debate: Do funds that outperform do so due to skill, or due to luck?

We try hard to apply investment skills in managing our Funds. We follow a time-tested approach and have an experienced and highly specialized team of investment professionals picking the stocks in which we invest. However, in order to cover both bases, I decided to also read up on luck. Dr. Richard Wiseman's The Luck Factor1 discusses his research and provides some common sense approaches that may enable people to become luckier.

Wiseman procured hundreds of volunteers, creating one group of people who considered themselves lucky and another who considered themselves unlucky. He tested conventional notions of luck. As one might expect, the lucky group had no apparent psychic ability; their guesses of upcoming lottery numbers were no better than guesses made by the unlucky group. Superstition was not effective either, as the appearance of a black cat vs. a white cat had no impact on results of a coin toss competition.

Instead, Wiseman concluded that people take specific actions that enable them to be lucky and succeed. He provides four principles that induce luck:

1) Maximize your chance opportunities

2) Listen to your lucky hunches

3) Expect good fortune

4) Turn bad luck into good

Though Wiseman does not explicitly mention investing, each principle can be applied in pursuit of successful money management.

Maximizing chance opportunities entails meeting a large number of people and creating networks to obtain information and investment ideas. Being observant and open to new ideas also helps. Successful investments can be discovered inadvertently: years ago I observed long lines and rising prices at parking garages in downtown Chicago and then profitably invested in a parking lot stock. Rather than pursuing information in hope of confirming existing opinions, pursuing unbiased information could induce the sale of an existing stock and purchase of a superior new one.

Listening to lucky hunches requires the use of intuition. Stocks tend to quickly react to information, and acting early, using imperfect information, is indeed an art form. We once had an analyst who tended to act only after obtaining repeated confirmations that company fundamentals had changed. He performed poorly because stocks often moved before he acted. In contrast, we recently successfully invested in a telecommunications stock that appeared likely to rise as an increasing number of Wall Street analysts began following it. Occasionally, we choose not to pursue possible investment opportunities because they simply don't feel right.

The next luck-inducing principle is to expect good fortune. This is consistent with our investment philosophy. We put money into stocks with the expectation that they will make money over time. We tend to expect continued good fortune from our successful investments and, when it makes sense, let our winners run. This has resulted in lower turnover than the industry average for the Columbia Wanger Funds.

We also attempt to turn bad luck into good and pursue an occasional positive side of bad luck. In the 1980s, several of our analysts complained about aggressive foreign competitors hurting companies we held in our flagship retail small-cap fund, Columbia Acorn Fund. The portfolio manager at that time, Ralph Wanger, coined the phrase, "Don't bitch, switch!" and we've owned some foreign stocks in that fund ever since. We've learned that one company's problem may be another company's opportunity, and that the best choice may be to invest in the latter company.

Ben Sherwood's The Survivors Club2 also mentions a few attributes applicable to investing. Situational awareness is a key part of military survival training and is important in investing too. Although many homebuilding stocks looked cheap during the housing bubble, generally avoiding them benefited our shareholders. Likewise, a well-run company may perform well within a highly competitive industry, but its stock could have substantial downside if its management changes or it grows beyond its niche.

As defined by Sherwood, the "incredulity response" occurs when very unusual events

2

Wanger International Select 2009 Annual Report

occur, such as catastrophes. Market meltdowns also appear to qualify. People tend to not believe such an event is happening and become paralyzed. Instead, survivors need to act positively. During a market meltdown, the market becomes extremely risk averse, and pays investors handsomely to take risk. That was true a year ago and we invested in several companies with substantial debt that our analysis indicated would likely survive and flourish. On average, those stocks performed very well for shareholders.

Both authors believe that people can create their own luck. After reading their perspectives, I have to agree. We at Columbia Wanger Asset Management think that creating luck is a skill and that providing above average returns is no random act.

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, L.P.

The information and data provided in this analysis are derived from sources that we deem to be reliable and accurate. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. The views/opinions expressed in this essay are those of the author and not of the Wanger Advisors Trust Board, are subject to change at any time based upon economic, market or other conditions, may differ from views expressed by other Columbia Management associates or other divisions of Bank of America Corporation and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on b ehalf of any particular Columbia Wanger Fund.

Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility. A fund that maintains a relatively concentrated portfolio may be subject to greater risk than a fund that is more fully diversified.

1 Wiseman, Richard, The Luck Factor, (New York, New York, Miramax Books/Hyperion 2003).

2 Sherwood, Ben, The Survivors Club, (New York, New York, Grand Central Publishing, 2009).

Also referenced in the writing of this essay was a research paper written by Eugene F. Fama and Kenneth R. French titled, "Luck versus Skill in the Cross Section of Mutual Fund Returns." The paper was originally dated October 2007 and updated in November 2009. It can be found on the Social Science Research Network's website at www.ssrn.com.

3

Wanger International Select 2009 Annual Report

Performance Review Wanger International Select

Christopher J. Olson

Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. For daily and most recent month-end performance updates, please call 1-888-4-WANGER.

For the year ended December 31, 2009, Wanger International Select had a 32.92% return while its primary benchmark, the S&P Developed Ex-U.S. Between $2 Billion and $10 Billion Index, was up 38.60%. Having positioned the Fund well for the previous downturn, it lagged over the past year as the markets were boosted by an unprecedented amount of monetary and fiscal stimulus. Our focus for the Fund has been on companies with competitive market positions and business models, longer-term growth prospects and solid balance sheets but these companies were not strong performers during 2009 as investor appetite for risk returned and lower quality stocks rallied. We intend to continue to be manage the Fund following the approach that has resulted in good outperformance relative to its benchmark and peers over the three- and five-year periods.

Naspers was the top contributor to Fund performance for the year, posting a 121% annual gain. Naspers is a media company with assets in South Africa and other emerging markets that has enjoyed strong earnings growth and has benefited from its stake in the rapidly growing Chinese internet company, Tencent. Hexagon, a Swedish manufacturer of measurement equipment, ended the year up 195%. The company's business fundamentals remained robust throughout the recession due to its strong focus on emerging markets where growth has proven to be more stable.

Canada's Pacific Rubiales Energy, an oil production and exploration company with operating assets in Colombia, had the largest return for the year, posting an impressive 697% gain. The stock has benefited from increasing production and new exploration discoveries in Colombia as well as the rebound in oil prices.

Four of the Fund's five worst performing stocks for the period were in Japanese names and included Jupiter Telecommunications, Nintendo, Seven Bank and Daito Trust Construction. Losses in these stocks ranged from 7% to 39%. The Fund sold out of Nintendo midyear and Daito Trust Construction during the first quarter of 2009. The Japanese economy has and continues to suffer from a deflationary environment and declining population. While stocks in Japan are beginning to look interesting from a valuation perspective, the growth outlook remains uncertain, and investors reduced their Japanese holdings over the course of the year to focus on recovery stories in other regions. Cephalon, a U.S. pharmaceutical company, was the other name in the Fund's top five laggards list. Its stock fell 23% in the Fund. Upcoming patent expirations on several of Cephalon's drugs will make way for competition from generics, and potential health care refor m in the United States added to uncertainty about its business. The Fund sold out of its position in Cephalon in the fourth quarter.

International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investing in emerging markets may involve greater risks than investing in more developed countries.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

Fund's Positions in Mentioned Holdings

As a percentage of net assets, as of 12/31/09

| Naspers | | | 6.5 | % | |

| Hexagon | | | 2.5 | | |

| Pacific Rubiales Energy | | | 2.3 | | |

| Jupiter Telecommunications | | | 2.2 | | |

| Seven Bank | | | 1.8 | | |

4

Wanger International Select 2009 Annual Report

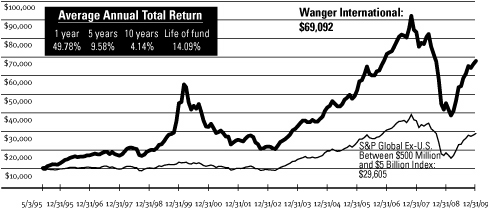

Growth of a $10,000 Investment in Wanger International Select

February 1, 1999 (inception date) through December 31, 2009

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Performance results may reflect any fee waivers or reimbursements of Fund expenses by the investment advisor and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower. For daily and most recent month-end performance updates, please call 1-888-4-WANGER.

This graph compares the results of $10,000 invested in Wanger International Select on February 1, 1999 (the date the Fund began operations) through December 31, 2009, to the S&P Developed Ex-U.S. Between $2 Billion and $10 Billion Index, with dividends and capital gains reinvested. Although the index is provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the index.

Top 10 Holdings

As a percentage of net assets, as of 12/31/09

1. Naspers (South Africa)

Media in Africa & Other Emerging Markets | | | 6.5 | % | |

2. Serco (United Kingdom)

Facilities Management | | | 5.1 | | |

3. Capita Group (United Kingdom)

White Collar, Back Office Outsourcing | | | 3.3 | | |

4. NHN (South Korea)

South Korea's Largest Online Search Engine | | | 3.2 | | |

5. Ascendas REIT (Singapore)

Singapore Industrial Property Landlord | | | 3.1 | | |

6. Olam International (Singapore)

Agriculture Supply Chain Manager | | | 3.0 | | |

7. Eldorado Gold (Canada)

Gold Miner in Turkey, Greece, China & Brazil | | | 2.8 | | |

8. Kansai Paint (Japan)

Paint Producer in Japan, India, China & Southeast Asia | | | 2.7 | | |

9. Red Electrica de Espana (Spain)

Spanish Power Transmission | | | 2.7 | | |

10. Cobham (United Kingdom)

Aerospace Components | | | 2.6 | | |

Top 5 Countries

As a percentage of net assets, as of 12/31/09

| United Kingdom | | | 15.6 | % | |

| Japan | | | 15.6 | | |

| Canada | | | 8.3 | | |

| Singapore | | | 7.0 | | |

| South Korea | | | 7.0 | | |

Results as of December 31, 2009

| | | 4th quarter | | 1 year | |

| Wanger International Select | | | 4.54 | % | | | 32.92 | % | |

S&P Developed Ex-U.S. Between $2 Billion

and $10 Billion Index* | | | 1.14 | | | | 38.60 | | |

| MSCI EAFE Index | | | 2.18 | | | | 31.78 | | |

Lipper Variable Underlying International

Growth Funds Index | | | 4.19 | | | | 35.75 | | |

NAV as of 12/31/09: $15.42

* The Fund's primary benchmark.

Performance numbers reflect all Fund expenses but do not include any insurance charge imposed by your insurance company's separate accounts. If performance included the effect of these additional charges, it would be lower.

The Fund's annual operating expense ratio is 1.24%. The annual operating expense ratio is as stated in the Fund's prospectus that is current as of the date of this report. Differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and expense reimbursements, if any, as well as different time periods used in calculating the ratios.

All results shown assume reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

The S&P Developed Ex-U.S. Between $2 Billion and $10 Billion Index, the Fund's primary benchmark, is a subset of the broad market selected by the index sponsor representing the mid-cap developed market, excluding the United States. The Morgan Stanley Capital International Europe, Australasia and Far East (MSCI EAFE) Index is a capitalization-weighted index that tracks the total return of common stocks in 21 developed market countries within Europe, Australasia and the Far East. The Lipper Variable Underlying International Growth Funds Index is an equally weighted representation of the 30 largest variable insurance underlying funds in the Lipper Variable Underlying International Growth Funds Classification. Indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the Fund. Lipper makes no adjustment for the effect of sales loads.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings.

5

Wanger International Select 2009 Annual Report

Wanger International Select

Statement of Investments December 31, 2009

Number of

Shares | | | | Value | |

| | | | | Equities – 96.7% | | | | | |

| | | Europe 38.0% | |

| | | United Kingdom – 15.6% | |

| | 190,000 | | | Serco

Facilities Management | | | $1,615,315

| | |

| | 85,000 | | | Capita Group

White Collar, Back Office Outsourcing | | | 1,025,254

| | |

| | 200,000 | | | Cobham

Aerospace Components | | | 806,177

| | |

| | 40,000 | | | Intertek Group

Testing, Inspection & Certification Services | | | 805,401

| | |

| | 25,000 | | | Schroders

United Kingdom Top Tier Asset Manager | | | 533,638

| | |

| | 118,100 | | | Spice Group

United Kingdom Utility Outsourcing | | | 115,291

| | |

| | | | | | | | 4,901,076 | | |

| | | Netherlands – 6.0% | |

| | 13,540 | | | Fugro

Sub-sea Oilfield Services | | | 773,228

| | |

| | 20,000 | | | Imtech

Electromechanical & ICT Installation &

Maintenance | | | 536,713

| | |

| | 3,000 | | | Core Laboratories

Oil & Gas Reservoir Consulting | | | 354,360

| | |

| | 2,700 | | | Smit Internationale

Harbor & Offshore Towage & Marine Services | | | 232,429

| | |

| | | | | | | | 1,896,730 | | |

| | | France – 4.4% | |

| | 7,000 | | | Neopost

Postage Meter Machines | | | 578,347

| | |

| | 14,900 | | | Eutelsat

Fixed Satellite Services | | | 478,046

| | |

| | 8,000 | | | Zodiac Aerospace

Leading Supplier to the Aerospace Industry | | | 333,853

| | |

| | | | | | | | 1,390,246 | | |

| | | Germany – 3.3% | |

| | 50,000 | | | Wirecard

Online Payment Processing & Risk Management | | | 687,424

| | |

| | 14,000 | | | Rhoen-Klinikum

Health Care Services | | | 342,424

| | |

| | | | | | | | 1,029,848 | | |

Number of

Shares | | | | Value | |

| | | Spain – 2.7% | |

| | 15,400 | | | Red Electrica de Espana

Spanish Power Transmission | | $853,498

| |

| | | Sweden – 2.5% | |

| | 53,000 | | | Hexagon

Measurement Equipment | | 778,548

| |

| | | Switzerland – 1.7% | |

| | 2,900 | | | Kuehne & Nagel

Freight Forwarding/Logistics | | 280,532

| |

| | 7,000 | | | Bank Sarasin & Cie (a)

Private Banking | | 264,547

| |

| | | | | | | | 545,079 | | |

| | | Ireland – 0.9% | |

| | 95,000 | | | United Drug

Irish Pharmaceutical Wholesaler & Outsourcer | | 289,864

| |

| | | Denmark – 0.9% | |

| | 2,700 | | | Novozymes

Industrial Enzymes | | 279,962

| |

| | | | | Europe – Total | | | 11,964,851 | | |

| | | Asia – 36.8% | |

| | | Japan – 15.6% | |

| | 104,000 | | | Kansai Paint

Paint Producer in Japan, India, China &

Southeast Asia | | 863,539

| |

| | 700 | | | Jupiter Telecommunications

Largest Cable Service Provider in Japan | | 693,503

| |

| | 14,900 | | | Benesse

Education Service Provider | | 623,092

| |

| | 51,900 | | | Rohto Pharmaceutical

Health & Beauty Products | | 597,367

| |

| | 290 | | | Seven Bank

ATM Processing Services | | 575,976

| |

| | 80 | | | Orix JREIT

Diversified REIT | | 397,595

| |

| | 44,000 | | | Nomura Holdings

Brokerage, Dealing, Underwriting &

Asset Management | | 324,261

| |

| | 13,000 | | | Ain Pharmaciez

Dispensing Pharmacy/Drugstore Operator | | 311,905

| |

See accompanying notes to financial statements.

6

Wanger International Select 2009 Annual Report

Wanger International Select

Statement of Investments December 31, 2009

Number of

Shares | | | | Value | |

| | | Japan – 15.6% (cont) | |

| | 37,000 | | | Kamigumi

Port Cargo Handling & Logistics | | | $268,855

| | |

| | 27,000 | | | Suruga Bank

Regional Bank | | | 234,198

| | |

| | | | | | | | 4,890,291 | | |

| | | Singapore – 7.0% | |

| | 620,000 | | | Ascendas REIT

Singapore Industrial Property Landlord | | | 970,946

| | |

| | 500,000 | | | Olam International

Agriculture Supply Chain Manager | | | 936,389

| | |

| | 50,000 | | | Singapore Exchange

Singapore Equity & Derivatives

Market Operator | | | 294,737

| | |

| | | | | | | | 2,202,072 | | |

| | | South Korea – 7.0% | |

| | 6,000 | | | NHN (a)

South Korea's Largest Online Search Engine | | | 990,757

| | |

| | 3,900 | | | MegaStudy

Online Education Service Provider | | | 799,096

| | |

| | 12,500 | | | Woongjin Coway

South Korean Household Appliance

Rental Service Provider | | | 412,128

| | |

| | | | | | | | 2,201,981 | | |

| | | China – 4.8% | |

| | 284,600 | | | Zhaojin Mining Industry

Gold Mining & Refining in China | | | 561,352

| | |

| | 543,000 | | | Jiangsu Expressway

Chinese Toll Road Operator | | | 483,075

| | |

| | 143,500 | | | Shandong Weigao

Vertically Integrated Hospital Consumable

Manufacturer | | | 476,588

| | |

| | | | | | | | 1,521,015 | | |

| | | Hong Kong – 2.4% | |

| | 35,000 | | | Hong Kong Exchanges and Clearing

Hong Kong Equity & Derivatives

Market Operator | | | 623,084

| | |

| | 40,400 | | | Lifestyle International

Mid to High-end Department Store

Operator in Hong Kong & China | | | 74,934

| | |

Number of

Shares | | | | Value | |

| | 470,714 | | | NagaCorp

Casino/Entertainment Complex in Cambodia | | | $52,002

| | |

| | | | 750,020 | | |

| | | | | Asia – Total | | | 11,565,379 | | |

| | | Other Countries – 21.9% | |

| | | Canada – 8.3% | |

| | 61,050 | | | Eldorado Gold (a)

Gold Miner in Turkey, Greece, China & Brazil | | | 870,934

| | |

| | 50,000 | | | Pacific Rubiales Energy (a)

Oil Production & Exploration in Colombia | | | 738,634

| | |

| | 6,000 | | | Potash Corp. of Saskatchewan

World's Largest Producer of Potash | | | 651,000

| | |

| | 12,900 | | | CCL Industries

Leading Global Label Manufacturer | | | 348,448

| | |

| | | | | | | | 2,609,016 | | |

| | | South Africa – 6.5% | |

| | 50,000 | | | Naspers

Media in Africa & Other Emerging Markets | | | 2,029,055

| | |

| | | United States – 4.6% | |

| | 4,700 | | | Diamond Offshore

Offshore Drilling Contractor | | | 462,574

| | |

| | 7,000 | | | Oceaneering International (a)

Provider of Sub-sea Services &

Manufactured Products | | | 409,640

| | |

| | 7,000 | | | Alexion Pharmaceuticals (a)

Biotech Focused on Orphan Diseases | | | 341,740

| | |

| | 6,500 | | | Atwood Oceanics (a)

Offshore Drilling Contractor | | | 233,025

| | |

| | | | | | | | 1,446,979 | | |

| | | Australia – 1.5% | |

| | 38,000 | | | United Group

Engineering & Facilities Management | | | 483,867

| | |

| | | Israel – 1.0% | |

| | 25,000 | | | Israel Chemicals

Producer of Potash, Phosphates, Bromine &

Specialty Chemicals | | | 326,414

| | |

| | | | | Other Countries – Total | | | 6,895,331 | | |

| Total Equities (Cost: $23,833,338) – 96.7% | | | 30,425,561 | | |

See accompanying notes to financial statements.

7

Wanger International Select 2009 Annual Report

Wanger International Select

Statement of Investments December 31, 2009

Number of Shares

or Principal Amount | | | | Value | |

| | | Exchange Traded Fund 1.0% | |

| | 25,000 | | | iShares MSCI Taiwan Index Fund | | $ | 324,250 | | |

| | | Taiwan Exchange Traded Fund | | | |

| | | Total Exchange Traded Fund (Cost: $249,340) | | | 324,250 | | |

| Short-Term Obligation – 2.5% | |

| | | Repurchase Agreement – 2.5% | |

| $ | 771,000 | | | Repurchase Agreement with Fixed

Income Clearing Corp., dated 12/31/09,

due 1/04/10 at 0.00%, collateralized by

a U.S. Treasury obligation, maturing

3/18/10, market value $789,921

(repurchase proceeds $771,000) | | | 771,000 | | |

| | | Total Short-Term Obligation (Cost: $771,000) | | | 771,000 | | |

| Total Investments (Cost: $24,853,678) – 100.2% (b)(c) | | | 31,520,811 | | |

| Cash and Other Assets Less Liabilities – (0.2)% | | | (66,689 | ) | |

| Total Net Assets – 100.0% | | $ | 31,454,122 | | |

Notes to Statement of Investments:

(a) Non-income producing security.

(b) On December 31, 2009, the Fund's total investments were denominated in currencies as follows:

| Currency | | Value | | Percentage

of Net Assets | |

| Euro | | $ | 5,105,825 | | | | 16.2 | | |

| British Pound | | | 4,901,076 | | | | 15.6 | | |

| Japanese Yen | | | 4,890,291 | | | | 15.6 | | |

| U.S. Dollar | | | 3,547,589 | | | | 11.3 | | |

| Hong Kong Dollar | | | 2,271,035 | | | | 7.2 | | |

| Singapore Dollar | | | 2,202,072 | | | | 7.0 | | |

| South Korean Won | | | 2,201,981 | | | | 7.0 | | |

| South African Rand | | | 2,029,055 | | | | 6.5 | | |

| Canadian Dollar | | | 1,958,016 | | | | 6.2 | | |

Other currencies less than

5% of total net assets | | | 2,413,871 | | | | 7.6 | | |

Cash and other assets

less liabilities | | | (66,689 | ) | | | (0.2 | ) | |

| | | $ | 31,454,122 | | | | 100.0 | | |

(c) At December 31, 2009, for federal income tax purposes, the cost of investments was $25,309,623, and net unrealized appreciation was $6,211,188, consisting of gross unrealized appreciation of $7,064,206 and gross unrealized depreciation of $853,018.

The following table summarizes the inputs used, as of December 31, 2009, in valuing the Fund's assets:

| Investment Type | | Quoted Prices

(Level 1) | | Other

Significant

Observable

Inputs

(Level 2) | | Significant

Unobservable

Inputs

(Level 3) | | Total | |

| Equities | |

| Europe | | $ | 354,360 | | | $ | 11,610,491 | | | $ | — | | | $ | 11,964,851 | | |

| Asia | | | — | | | | 11,565,379 | | | | — | | | | 11,565,379 | | |

| Other Countries | | | 4,055,995 | | | | 2,839,336 | | | | — | | | | 6,895,331 | | |

| Total Equities | | $ | 4,410,355 | | | $ | 26,015,206 | | | $ | — | | | $ | 30,425,561 | | |

Total Exchange Traded

Fund | | | 324,250 | | | | — | | | | — | | | | 324,250 | | |

Total Short-Term

Obligation | | | — | | | | 771,000 | | | | — | | | | 771,000 | | |

| Total Investments | | $ | 4,734,605 | | | $ | 26,786,206 | | | $ | — | | | $ | 31,520,811 | | |

The Fund's assets assigned to the Level 2 input category include certain foreign securities for which a third party statistical pricing service may be employed for purposes of fair market valuation.

For more information on valuation inputs, and their aggregation into the levels used in the table above, please refer to the Security Valuation section in the accompanying Notes to Financial Statements.

See accompanying notes to financial statements.

8

Wanger International Select 2009 Annual Report

Wanger International Select

Portfolio Diversification December 31, 2009

At December 31, 2009, the Fund's portfolio investments as a percentage of net assets was diversified as follows:

| | | Value | | Percentage of

Net Assets | |

| Industrial Goods & Services | |

| Outsourcing Services | | $ | 3,692,249 | | | | 11.7 | | |

| Other Industrial Services | | | 2,440,366 | | | | 7.8 | | |

| Industrial Materials & Specialty Chemicals | | | 1,469,915 | | | | 4.7 | | |

| Electrical Components | | | 806,177 | | | | 2.6 | | |

| Machinery | | | 578,347 | | | | 1.8 | | |

| | | | 8,987,054 | | | | 28.6 | | |

| Information | |

| TV Broadcasting | | | 2,029,055 | | | | 6.5 | | |

| Financial Processors | | | 1,605,245 | | | | 5.1 | | |

| Internet Related | | | 990,757 | | | | 3.1 | | |

| Instrumentation | | | 778,548 | | | | 2.5 | | |

| CATV | | | 693,503 | | | | 2.2 | | |

| Satellite Broadcasting & Services | | | 478,046 | | | | 1.5 | | |

| | | | 6,575,154 | | | | 20.9 | | |

| Energy & Minerals | |

| Mining | | | 2,437,646 | | | | 7.8 | | |

| Oil Services | | | 1,878,467 | | | | 6.0 | | |

| Oil & Gas Producers | | | 738,634 | | | | 2.3 | | |

| | | | 5,054,747 | | | | 16.1 | | |

| Consumer Goods & Services | |

| Other Consumer Services | | | 1,909,250 | | | | 6.0 | | |

| Nondurables | | | 945,815 | | | | 3.0 | | |

| Retail | | | 311,905 | | | | 1.0 | | |

| Casinos & Gaming | | | 52,002 | | | | 0.2 | | |

| | | | 3,218,972 | | | | 10.2 | | |

| | | Value | | Percentage of

Net Assets | |

| Other Industries | |

| Real Estate | | $ | 1,368,541 | | | | 4.4 | | |

| Transportation | | | 984,359 | | | | 3.1 | | |

| Regulated Utilities | | | 853,498 | | | | 2.7 | | |

| | | | 3,206,398 | | | | 10.2 | | |

| Finance | |

| Brokerage & Money Management | | | 1,122,446 | | | | 3.5 | | |

| Banks | | | 810,174 | | | | 2.6 | | |

| | | | 1,932,620 | | | | 6.1 | | |

| Health Care | |

| Medical Equipment & Devices | | | 818,328 | | | | 2.6 | | |

| Health Care Services | | | 342,424 | | | | 1.1 | | |

| Pharmaceuticals | | | 289,864 | | | | 0.9 | | |

| | | | 1,450,616 | | | | 4.6 | | |

| Total Equities | | | 30,425,561 | | | | 96.7 | | |

| Exchange Traded Fund | | | 324,250 | | | | 1.0 | | |

| Short-Term Obligation | | | 771,000 | | | | 2.5 | | |

| Total Investments | | | 31,520,811 | | | | 100.2 | | |

Cash and Other Assets

Less Liabilities | | | (66,689 | ) | | | (0.2 | ) | |

| Net Assets | | $ | 31,454,122 | | | | 100.0 | | |

See accompanying notes to financial statements.

9

Wanger International Select 2009 Annual Report

Statement of Assets and Liabilities

December 31, 2009

| Assets: | |

| Investments, at cost | | $ | 24,853,678 | | |

| Investments, at value | | $ | 31,520,811 | | |

| Cash | | | 116 | | |

| Receivable for: | |

| Investments sold | | | 662 | | |

| Fund shares sold | | | 30,282 | | |

| Dividends receivable | | | 30,519 | | |

| Foreign tax reclaims | | | 1,512 | | |

| Other assets | | | 202 | | |

| Total Assets | | | 31,584,104 | | |

| Liabilities: | |

| Expense reimbursement due to investment advisor | | | 10,092 | | |

| Payable for: | |

| Investments purchased | | | 14,473 | | |

| Fund shares repurchased | | | 35,657 | | |

| Investment advisory fee | | | 25,043 | | |

| Administration fee | | | 1,332 | | |

| Transfer agent fee | | | 15 | | |

| Trustees' fees | | | 2 | | |

| Audit fee | | | 15,370 | | |

| Custody fee | | | 6,100 | | |

| Reports to shareholders | | | 10,425 | | |

| Chief compliance officer expenses | | | 79 | | |

| Trustees' deferred compensation plan | | | 10,136 | | |

| Other liabilities | | | 1,258 | | |

| Total Liabilities | | | 129,982 | | |

| Net Assets | | $ | 31,454,122 | | |

| Composition of Net Assets: | |

| Paid-in capital | | $ | 33,835,883 | | |

| Overdistributed net investment income | | | (77,609 | ) | |

| Accumulated net realized loss | | | (8,970,563 | ) | |

| Net unrealized appreciation (depreciation) on: | |

| Investments | | | 6,667,133 | | |

| Foreign currency translations | | | (722 | ) | |

| Net Assets | | $ | 31,454,122 | | |

| Fund Shares Outstanding | | | 2,039,608 | | |

Net asset value, offering price and redemption

price per share | | $ | 15.42 | | |

Statement of Operations

For the Year Ended December 31, 2009

| Investment Income: | |

| Dividends (net foreign taxes withheld of $51,156) | | $ | 621,815 | | |

| Interest income | | | 479 | | |

| Securities lending income | | | 21 | | |

| Total Investment Income | | | 622,315 | | |

| Expenses: | |

| Investment advisory fee | | | 266,056 | | |

| Administration fee | | | 14,152 | | |

| Transfer agent fee | | | 169 | | |

| Trustees' fees | | | 5,688 | | |

| Custody fee | | | 63,568 | | |

| Reports to shareholders | | | 26,758 | | |

| Audit fee | | | 24,101 | | |

| Chief compliance officer expenses (See Note 4) | | | 1,320 | | |

| Other expenses (See Note 5) | | | 18,451 | | |

| Total Expenses | | | 420,263 | | |

Fees waived or expenses reimbursed

by investment advisor | | | (9,931 | ) | |

| Custody earnings credit | | | — | * | |

| Net Expenses | | | 410,332 | | |

| Net Investment Income | | | 211,983 | | |

Net Realized and Unrealized Gain (Loss) on

Investments and Foreign Currency: | |

| Net realized gain (loss) on: | |

| Investments | | | (3,478,003 | ) | |

| Foreign currency transactions | | | 32,252 | | |

| Net realized loss | | | (3,445,751 | ) | |

Net change in unrealized appreciation

(depreciation) on: | |

| Investments | | | 11,083,357 | | |

| Foreign currency translations | | | (2,604 | ) | |

Net change in unrealized

appreciation (depreciation) | | | 11,080,753 | | |

| Net Gain | | | 7,635,002 | | |

| Net Increase in Net Assets from Operations | | $ | 7,846,985 | | |

* Rounds to less than $1.

See accompanying notes to financial statements.

10

Wanger International Select 2009 Annual Report

Statement of Changes in Net Assets

| | | Year Ended December 31, | |

| Increase (Decrease) in Net Assets | | 2009 | | 2008 | |

| Operations: | |

| Net investment income | | $ | 211,983 | | | $ | 566,145 | | |

| Net realized loss on investments and foreign currency transactions | | | (3,445,751 | ) | | | (5,479,558 | ) | |

Net change in unrealized appreciation (depreciation)

on investments and foreign currency translations | | | 11,080,753 | | | | (22,161,534 | ) | |

| Net Increase (Decrease) in Net Assets from Operations | | | 7,846,985 | | | | (27,074,947 | ) | |

| Distributions to Shareholders: | |

| From net investment income | | | (867,446 | ) | | | (215,563 | ) | |

| From net realized gains | | | — | | | | (14,461,904 | ) | |

| Total Distributions to Shareholders | | | (867,446 | ) | | | (14,677,467 | ) | |

| Share Transactions: | |

| Subscriptions | | | 1,881,562 | | | | 4,503,145 | | |

| Distributions reinvested | | | 867,446 | | | | 14,677,467 | | |

| Redemptions | | | (7,878,859 | ) | | | (21,308,289 | ) | |

| Net Decrease from Share Transactions | | | (5,129,851 | ) | | | (2,127,677 | ) | |

| Total Increase (Decrease) in Net Assets | | | 1,849,688 | | | | (43,880,091 | ) | |

| Net Assets: | |

| Beginning of period | | | 29,604,434 | | | | 73,484,525 | | |

| End of period | | $ | 31,454,122 | | | $ | 29,604,434 | | |

| Undistributed/(overdistributed) net investment income at end of period | | $ | (77,609 | ) | | $ | 544,737 | | |

See accompanying notes to financial statements.

11

Wanger International Select 2009 Annual Report

Financial Highlights

| | | Year Ended December 31, | |

| Selected data for a share outstanding throughout each period | | 2009 | | 2008 | | 2007 | | 2006 | | 2005 | |

| Net Asset Value, Beginning of Period | | $ | 12.01 | | | $ | 28.07 | | | $ | 26.62 | | | $ | 19.63 | | | $ | 17.19 | | |

| Income from Investment Operations: | |

| Net investment income (a) | | | 0.10 | | | | 0.21 | | | | 0.10 | | | | 0.11 | | | | 0.13 | | |

| Net realized and unrealized gain (loss) on investments and foreign currency | | | 3.71 | | | | (10.31 | ) | | | 4.92 | | | | 6.94 | | | | 2.66 | | |

| Total from Investment Operations | | | 3.81 | | | | (10.10 | ) | | | 5.02 | | | | 7.05 | | | | 2.79 | | |

| Less Distributions to Shareholders: | |

| From net investment income | | | (0.40 | ) | | | (0.09 | ) | | | (0.21 | ) | | | (0.06 | ) | | | (0.35 | ) | |

| From net realized gains | | | — | | | | (5.87 | ) | | | (3.36 | ) | | | — | | | | — | | |

| Total Distributions to Shareholders | | | (0.40 | ) | | | (5.96 | ) | | | (3.57 | ) | | | (0.06 | ) | | | (0.35 | ) | |

| Net Asset Value, End of Period | | $ | 15.42 | | | $ | 12.01 | | | $ | 28.07 | | | $ | 26.62 | | | $ | 19.63 | | |

| Total Return (b) | | | 32.92 | %(c) | | | (44.35 | )% | | | 21.78 | % | | | 36.00 | % | | | 16.43 | %(c) | |

| Ratios to Average Net Assets/Supplemental Data: | |

| Net expenses (d) | | | 1.45 | % | | | 1.24 | % | | | 1.18 | % | | | 1.19 | % | | | 1.32 | % | |

| Net investment income (d) | | | 0.75 | % | | | 1.10 | % | | | 0.37 | % | | | 0.47 | % | | | 0.76 | % | |

| Waiver/Reimbursement | | | 0.04 | % | | | — | | | | — | | | | — | | | | 0.00 | %(e) | |

| Portfolio turnover rate | | | 62 | % | | | 68 | % | | | 69 | % | | | 61 | % | | | 48 | % | |

| Net assets, end of period (000s) | | $ | 31,454 | | | $ | 29,604 | | | $ | 73,485 | | | $ | 62,594 | | | $ | 44,026 | | |

(a) Net investment income per share was based upon the average shares outstanding during the period.

(b) Total return at net asset value assuming all distributions reinvested.

(c) Had the investment advisor not waived a portion of expenses, total return would have been reduced.

(d) The benefits derived from custody fees paid indirectly had an impact of less than 0.01%.

(e) Rounds to less than 0.01%.

See accompanying notes to financial statements.

12

Wanger International Select 2009 Annual Report

Notes to Financial Statements

1. Nature of Operations

Wanger International Select (the "Fund"), is a series of Wanger Advisors Trust (the "Trust"), an open-end management investment company organized as a Massachusetts business trust. The investment objective of the Fund is to seek long-term capital appreciation. The Fund is available only for allocation to certain life insurance company separate accounts established for the purpose of funding qualified and non-qualified variable annuity contracts and variable life insurance policies and may also be offered directly to certain types of pension plans and retirement arrangements.

On September 29, 2009, Bank of America Corporation, the indirect parent company of Columbia Wanger Asset Management, L.P. ("CWAM"), entered into an agreement to sell a portion of the asset management business of Columbia Management Group, LLC ("Columbia Management") to Ameriprise Financial, Inc. The transaction ("Transaction") includes a sale of CWAM. The Transaction is subject to certain approvals and other conditions to closing, and is currently expected to close in the spring of 2010.

2. Significant Accounting Policies

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America ("GAAP") requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

Management has evaluated the events and transactions that have occurred through February 18, 2010, the date the financial statements were issued, and noted no items requiring adjustment of the financial statements or additional disclosures. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements.

Security valuation

Securities of the Fund are valued at market value or, if a market quotation for a security is not readily available or is deemed not to be reliable because of events or circumstances that have occurred between the market quotation and the time as of which the security is to be valued, the security is valued at its fair value determined in good faith under consistently applied procedures established by the Board of Trustees. A security traded on a securities exchange or in an over-the-counter market in which transaction prices are reported is valued at the last sales price at the time of valuation. A security traded principally on NASDAQ is valued at the NASDAQ official closing price. Mutual Funds and Exchange Traded Funds are valued at their closing net asset value as reported to NASDAQ. A security for which there is no reported sale on the valuation date is valued at the latest bid quotation. Short-term investments maturing in 60 days or less are valued at amortized cost, which approximates market value. A security for which a market quotation is not readily available and any other assets are valued at its fair value determined in good faith under consistently applied procedures established by the Board of Trustees. The Trust has retained an independent statistical fair value pricing service that employs a systematic methodology to assist in the fair valuation process for securities principally traded in a foreign market in order to adjust for possible changes in value that may occur between the close of the foreign market and the time as of which the securities are to be valued. If a security is valued at a "fair value", that value may be different from the last quoted market price for the security.

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

• Level 1—quoted prices in active markets for identical securities

• Level 2—other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk and others)

• Level 3—significant unobservable inputs (including management's own assumptions in determining the value of investments)

The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Examples of the types of securities in which the Fund would typically invest and how they are classified within this hierarchy are as follows. Typical level 1 securities include exchange traded domestic equities, mutual funds whose NAVs are published each day and exchange traded foreign equities that are not statistically fair valued. Typical level 2 securities include exchange traded foreign equities that are statistically fair valued and short-term investments valued at amortized cost. Additionally, securities fair valued by the Fund's valuation committee that rely on significant observable inputs are also included in level 2. Typical level 3 securities include any security fair valued by the Fund's Valuation Committee that relies on significant unobservable inputs.

Repurchase agreements

The Fund may engage in repurchase agreement transactions. The Fund, through its custodian, receives delivery of underlying securities collateralizing each repurchase agreement. The counterparty is required to maintain collateral that is at all times at least equal to the repurchase price including interest. In the event of default or bankruptcy by the other party to the agreement, realization and/or retention of the collateral may be subject to legal proceedings.

Foreign currency translations

Values of investments denominated in foreign currencies are converted into U.S. dollars using the New York spot market rate of exchange at the time of valuation. Purchases and sales of investments and dividend and interest income are translated into U.S. dollars using the spot market rate of exchange prevailing on the respective dates of such transactions. The gain or loss resulting from changes in foreign exchange rates is included with net realized and unrealized gain or loss from investments, as appropriate.

Security transactions and investment income

Security transactions are accounted for on the trade date (date the order to buy or sell is executed) and dividend income is recorded on the ex-dividend date, except that certain dividends from foreign securities are recorded as soon as the information is available to the Fund. Interest income is recorded on the accrual basis and includes amortization of discounts on debt obligations when required for federal income tax purposes. Realized gains and losses from security transactions are recorded on an identified cost basis.

Awards, if any, from class action litigation related to securities owned may be recorded as a reduction of cost of those securities. If the applicable securities are no longer owned, the proceeds are recorded as realized gains.

Restricted securities

Restricted securities are securities that may only be resold upon registration under federal securities laws or in transactions exempt from registration. In some cases, the issuer of restricted securities has agreed to register such securities for resale at the issuer's expense either upon demand by the Fund or in connection with another registered offering of the securities. Many restricted securities may be resold in the secondary market in transactions exempt from registration. Such restricted securities may be determined to be liquid under criteria established by the Board of Trustees.

13

Wanger International Select 2009 Annual Report

Notes to Financial Statements, continued

Securities lending

The Fund may lend securities up to one-third of the value of its total assets to certain approved brokers, dealers and other financial institutions to earn additional income. The Fund retains the benefits of owning the securities, including receipt of dividends or interest generated by the security. The Fund also receives a fee for the loan. The Fund has the ability to recall the loans at any time and could do so in order to vote proxies or to sell the loaned securities. Each loan is collateralized by cash that exceeds the value of the securities on loan. The market value of the loaned securities is determined daily at the close of business of the Fund and any additional required collateral is delivered to each Fund on the next business day. The Fund has elected to invest the cash collateral in the Dreyfus Government Cash Management Fund and the income earned is paid to the Fund, net of any fees remitted to Goldman Sachs Agency Lending as the lending agent and borrower rebates. The Fund's advisor, CWAM, does not retain any fees earned by the lending program. Generally, in the event of borrower default, the Fund has the right to use the collateral to offset any losses incurred. In the event the Fund is delayed or prevented from exercising its right to dispose of the collateral, there may be a potential loss to the Fund. Some of these losses may be indemnified by the lending agent. The Fund bears the risk of loss with respect to the investment of collateral.

The net lending income earned in 2009 by the Fund is included in the Statement of Operations. There were no loans outstanding on December 31, 2009.

Fund share valuation

Fund shares are sold and redeemed on a continuing basis at net asset value. Net asset value per share is determined daily as of the close of trading on the New York Stock Exchange ("the Exchange") on each day the Exchange is open for trading by dividing the total value of the Fund's investments and other assets, less liabilities, by the number of Fund shares outstanding.

Custody fees/Credits

Custody fees are reduced based on the Fund's cash balances maintained with the custodian. The amount is disclosed as a reduction of total expenses in the Statement of Operations.

Federal income taxes

The Fund has complied with the provisions of the Internal Revenue Code available to regulated investment companies and, in the manner provided therein, distributes all its taxable income, as well as any net realized gain on sales of investments and foreign currency transactions reportable for federal income tax purposes. Accordingly, the Fund paid no federal income taxes and no federal income tax provision was required.

Expenses

General expenses of the Trust are allocated to the Fund and the other series of the Trust based upon relative net assets or other expense allocation methodologies determined by the nature of the expense. Expenses directly attributable to the Fund are charged to the Fund.

Foreign capital gains taxes

Gains in certain countries may be subject to foreign taxes at the fund level, at rates ranging from 10%-15%. The Fund accrues for such foreign taxes on net realized and unrealized gains at the appropriate rate for each jurisdiction.

Distributions to shareholders

Distributions to shareholders are recorded on the ex-dividend date.

Indemnification

In the normal course of business, the Trust on behalf of the Fund enters into contracts that contain a variety of representations and warranties and that provide general indemnities. The Fund's maximum exposure under these arrangements is unknown, as this would involve future claims against the Fund. Also under the Trust's organizational documents, the trustees and officers of the Trust are indemnified against certain liabilities that may arise out of their duties to the Trust. However based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be minimal.

3. Federal Tax Information

The timing and character of income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP. Reclassifications are made to the Fund's capital accounts for permanent tax differences to reflect income and gains available for distribution (or available capital loss carryforwards) under income tax regulations.

For the year ended December 31, 2009, permanent book and tax basis differences resulting primarily from differing treatments for foreign currency transactions and passive foreign investment companies ("PFIC") adjustments were identified and reclassified among the components of the Fund's net assets as follows:

Overdistributed

Net Investment Income | | Accumulated

Net Realized Loss | | Paid-In Capital | |

| $ | 33,117 | | | $ | (33,117 | ) | | $ | — | | |

Net investment income and net realized gains (losses), as disclosed on the Statement of Operations, and net assets were not affected by this reclassification.

The tax character of distributions paid during the years ended December 31, 2009 and December 31, 2008 were as follows:

| | | December 31, 2009 | | December 31, 2008 | |

| Distributions paid from: | |

| Ordinary Income* | | $ | 867,446 | | | $ | 3,006,152 | | |

| Long-Term Capital Gains | | | — | | | | 11,671,315 | | |

* For tax purposes short-term capital gains distributions, if any, are considered ordinary income distributions.

As of December 31, 2009, the components of distributable earnings on a tax basis were as follows:

Undistributed

Ordinary

Income | | Undistributed

Long-Term

Capital Gains | |

Net Unrealized

Appreciation* | |

| $ | 230,735 | | | $ | — | | | $ | 6,211,188 | | |

* The differences between book-basis and tax-basis net unrealized appreciation are primarily due to deferral of losses from wash sales and PFIC adjustments.

The following capital loss carryforwards, determined as of December 31, 2009, may be available to reduce taxable income arising from future net realized gains on investments, if any, to the extent permitted by the Internal Revenue Code:

Year of

Expiration | | Capital Loss

Carryforward | |

| | 2016 | | | $ | 2,630,085 | | |

| | 2017 | | | | 5,996,635 | | |

| Total | | | 8,626,720 | | |

14

Wanger International Select 2009 Annual Report

Notes to Financial Statements, continued

Under current tax rules, certain currency (and capital) losses realized after October 31 may be deferred and treated as occurring on the first day of the following fiscal year. As of December 31, 2009, post-October capital losses of $196,242 attributed to security transactions were deferred to January 1, 2010.

Management is required to determine whether a tax position of the Fund is more likely than not to be sustained upon examination by the applicable taxing authority, including resolution of any related appeals or litigation processes, based on the technical merits of the position. The tax benefit to be recognized by the Fund is measured as the largest amount of benefit that is greater than fifty percent likely of being realized upon ultimate settlement. Management is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. However, management's conclusions may be subject to review and adjustment at a later date based on factors including, but not limited to, new tax laws, regulations, and administrative interpretations (including relevant court decisions). The Fund's federal tax returns for the prior three fiscal year s remain subject to examination by the Internal Revenue Service.

4. Transactions With Affiliates

CWAM is a wholly owned subsidiary of Columbia Management which in turn is an indirect wholly owned subsidiary of Bank of America Corporation ("BOA"). CWAM furnishes continuing investment supervision to the Fund and is responsible for the overall management of the Fund's business affairs.

Under the Fund's investment advisory agreement, management fees are accrued daily based on the Fund's average daily net assets and paid monthly to CWAM at the annual rates shown in the table below:

| Average Daily Net Assets | | Annual Fee Rate | |

| | Up to $500 million | | | | 0.94 | % | |

| | $500 million and over | | | | 0.89 | % | |

For the year ended December 31, 2009, the Fund's effective investment advisory fee rate was 0.94% of average daily net assets.

Through April 30, 2010, CWAM will reimburse the Fund to the extent that ordinary operating expenses (exclusive of brokerage commissions, interest, taxes and extraordinary expenses, but inclusive of custodian charges relating to overdrafts, if any), after giving effect to any balance credits from the Fund's custodian, exceed an annual percentage of 1.45% of average daily net assets on an annualized basis. For the year ended December 31, 2009, the Fund was reimbursed $9,931.

CWAM provides administrative services and receives an administration fee from the Fund at the following annual rates.

Wanger Advisors Trust Aggregate

Average Daily Net Assets of the Trust | | Annual Fee Rate | |

| Up to $4 billion | | | 0.05 | % | |

| $4 billion to $6 billion | | | 0.04 | % | |

| $6 billion to $8 billion | | | 0.03 | % | |

| $8 billion and over | | | 0.02 | % | |

For the year ended December 31, 2009, the Fund's effective administration fee rate was 0.05% of average daily net assets. CWAM has delegated to Columbia Management Advisors, LLC ("Columbia"), an indirect, wholly owned subsidiary of BOA, the responsibility for certain administrative services.

Certain officers and trustees of the Trust are also officers of CWAM. The Trust makes no direct payments to its officers and trustees who are affiliated with CWAM.

The Board of Trustees has appointed a Chief Compliance Officer to the Trust in accordance with federal securities regulations. The Fund, along with other affiliated funds, pays its pro-rata share of the expenses associated with the Office of the Chief Compliance Officer. These expenses are disclosed separately as "Chief compliance officer expenses" in the Statement of Operations.

The Trust offers a deferred compensation plan for its independent trustees. Under that plan, a trustee may elect to defer all or a portion of his or her compensation. Amounts deferred are retained by the Trust and may represent an unfunded obligation of the Trust. The value of amounts deferred is determined by reference to the change in value of Class Z shares of one or more series of Columbia Acorn Trust or a money market fund as specified by the trustee. Benefits under the deferred compensation plan are payable when the trustee ceases to be a member of the Board of Trustees.

Columbia Management Distributors, Inc. (the "Distributor"), an affiliate of Columbia and an indirect, wholly owned subsidiary of BOA, serves as the principal underwriter of the Trust and receives no compensation from the Fund for its services.

Columbia Management Services, Inc. (the "Transfer Agent"), an affiliate of Columbia and an indirect, wholly owned subsidiary of BOA, provides shareholder services to the Fund and has subcontracted with Boston Financial Data Services ("BFDS") to serve as subtransfer agent. For such services, the Transfer Agent receives a fee, paid monthly, at the annual rate of $21.00 per account. . The Transfer Agent also receives reimbursement for certain out-of-pocket expenses.

During the year ended December 31, 2009, the Fund did not engage in purchase and sales transactions with funds that have a common investment advisor (or affiliated investment advisors), common directors/trustees, and/or common officers.

5. Borrowing Arrangements

The Trust participates in a $150 million credit facility, along with another Trust managed by CWAM, which was entered into to facilitate portfolio liquidity. Under the facility, interest is charged to each participating fund based on its borrowings at a rate per annum equal to the higher of Federal Funds Rate or Overnight LIBOR plus 0.750%. In addition, a commitment fee of 0.12% per annum of the unutilized line of credit is accrued and apportioned among the participating funds based on their relative net assets. The commitment fee is included in "Other expenses" in the Statement of Operations. No amounts were borrowed by the Fund under this facility during the year ended December 31, 2009. The Trust enters into this line of credit for one year durations. The Trust has secured the line of credit for the entire year of 2010.

6. Fund Share Transactions

Proceeds and payments on Fund shares as shown in the Statement of Changes in Net Assets are in respect of the following numbers of shares:

| | | Year Ended

December 31, 2009 | | Year Ended

December 31, 2008 | |

| Shares sold | | | 143,216 | | | | 246,505 | | |

Shares issued in reinvestment

of dividend distributions | | | 77,552 | | | | 740,912 | | |

| Less shares redeemed | | | (645,637 | ) | | | (1,140,778 | ) | |

| Net decrease in shares outstanding | | | (424,869 | ) | | | (153,361 | ) | |

7. Investment Transactions

The aggregate cost of purchases and proceeds from sales other than short-term obligations for the year ended December 31, 2009 were $17,026,842 and $22,561,564, respectively.

8. Legal Proceedings

CWAM, Columbia Acorn Trust, (another mutual fund family advised by CWAM), and the trustees of Columbia Acorn Trust (collectively, the "Columbia defendants") are named as defendants in class and derivative complaints that have been consolidated in a Multi-District Action (the "MDL Action") in the

15

Wanger International Select 2009 Annual Report

Notes to Financial Statements, continued

federal district court of Maryland. These lawsuits contend that defendants permitted certain investors to market time their trades in certain Columbia Acorn Funds. The MDL Action is ongoing. However, all claims against the Trust and the independent trustees of Columbia Acorn Trust have been dismissed.

Columbia Acorn Trust and CWAM are also defendants in a class action lawsuit that alleges, in summary, that Columbia Acorn Trust and CWAM exposed shareholders of Columbia Acorn International Fund to trading by market timers by allegedly: (a) failing to properly evaluate daily whether a significant event affecting the value of that fund's securities had occurred after foreign markets had closed but before the calculation of the funds' net asset value (NAV"); (b) failing to implement the fund's portfolio valuation and share pricing policies and procedures; and (c) failing to know and implement applicable rules and regulations concerning the calculation of NAV (the "Fair Valuation Lawsuit"). The Seventh Circuit ruled that the plaintiffs' state law claims were preempted under federal law resulting in the dismissal of plaintiffs' complaint. Plaintiffs appealed the Seventh Circuit's ruling to the United States Supreme Court. The Suprem e Court reversed the Seventh Circuit's ruling on jurisdictional grounds and the case was ultimately remanded to the state court.

On March 21, 2005, a class action complaint was filed against the Trust and CWAM seeking to rescind the CDSC assessed upon redemption of Class B shares of the Columbia Acorn Funds due to the alleged market timing of the Columbia Acorn Funds (the "CDSC Lawsuit"). In addition to the rescission of sales charges, plaintiffs seek recovery of actual damages, attorneys' fees and costs. The case has been transferred to the MDL Action in the federal district court of Maryland.

On September 14, 2007, the plaintiffs and the Columbia defendants named in the MDL Action, including the Columbia Funds, entered into a stipulation of settlement with respect to all Columbia-related claims in the MDL Action described above, including the CDSC and Fair Valuation Lawsuits. The settlement is subject to court approval.

Columbia Acorn Funds and CWAM intend to defend these suits vigorously. CWAM believes that the lawsuits are not likely to materially affect its ability to provide investment management services to the Fund.

16

Wanger International Select 2009 Annual Report

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of Wanger International Select:

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Wanger International Select (a series of the Wanger Advisors Trust, hereinafter referred to as the "Fund") at December 31, 2009, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as "financial statements") are the responsibility of the Fund's management; our responsibility is to express an opinion on these financial statements b ased on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2009 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Chicago, Illinois

February 18, 2010

17

Wanger International Select 2009 Annual Report

Federal Income Tax Information (Unaudited)

Foreign taxes paid during the fiscal year ended December 31, 2009 of $51,156 are expected to be passed through to shareholders. This represents $0.03 per share. Eligible shareholders may claim this amount as a foreign tax credit.

Gross income derived from sources within foreign countries was $621,168 ($0.30 per share) for the fiscal year ended December 31, 2009.

12.12% of the ordinary income distributed by the Fund for the fiscal year ended December 31, 2009, qualified for the corporate dividends received deduction.

18

Wanger International Select 2009 Annual Report

Board of Trustees and Management of Wanger Advisors Trust

The Board of Trustees of the Trust has overall management responsibility for the Trust and the Funds. Each trustee may serve a term of unlimited duration. The Trust's bylaws generally require that trustees retire at the end of the calendar year in which they attain 75 years. The trustees appoint their own successors, provided that at least two-thirds of the trustees, after such appointment, have been elected by shareholders. Shareholders may remove a trustee, with or without cause, upon the vote of two-thirds of the Trust's outstanding shares at any meeting called for that purpose. A trustee may be removed, with or without cause, upon the vote of a majority of the trustees.

The names of the trustees and officers of the Trust, the date each was first elected or appointed to office, their principal business occupations during at least the last five years, and other directorships they hold are shown below. Each trustee serves in such capacity for each of the four series of the Trust and each of the six series of Columbia Acorn Trust.

The business address of each trustee and officer of the Trust is Columbia Wanger Asset Management, L.P., 227 West Monroe, Suite 3000, Chicago, Illinois 60606. The Fund's Statement of Additional Information includes additional information about the Fund's trustees and officers. You may obtain a free copy of the Statement of Additional Information by writing or calling toll-free:

Columbia Wanger Asset Management, L.P.

Shareholder Services Group

227 W. Monroe, Suite 3000

Chicago, IL 60606

888-4-WANGER (888-492-6437)

Name, Position(s) with

Wanger Advisors

Trust and Age at

December 31, 2009 | | Year First

Elected or

Appointed

to Office | | Principal Occupation(s) during

Past Five Years | | Number of

Portfolios in

Fund Complex

Overseen

by Trustee/Officer | | Other

Directorships

in addition

to Wanger

Advisors Trust | |

| Trustees who are not interested persons of Wanger Advisors Trust: | | | | | | | |

|

Laura M. Born, 44,

Trustee | | | 2007 | | | Adjunct Assistant Professor of Finance, University of Chicago Booth School of Business; formerly, Managing Director–Investment Banking, J.P. Morgan Chase & Co. (broker/ dealer) 2002-2007. | | | 10 | | | Columbia Acorn Trust. | |

|

Michelle L. Collins, 49,