UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08748 |

|

Wanger Advisors Trust |

(Exact name of registrant as specified in charter) |

|

225 Franklin Street, Boston, Massachusetts | | 02110 |

(Address of principal executive offices) | | (Zip code) |

|

Scott R. Plummer

5228 Ameriprise Financial Center

Minneapolis, MN 55474 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-612-671-1947 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2011 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Wanger International

2011 Annual Report

Not FDIC insured • No bank guarantee • May lose value

Wanger International

2011 Annual Report

Table of Contents

| 2 | | | Understanding Your Expenses | |

|

| 3 | | | Vaccines: Medicine's Greatest Lifesaver | |

|

| 6 | | | Performance Review | |

|

| 8 | | | Statement of Investments | |

|

| 19 | | | Statement of Assets and Liabilities | |

|

| 19 | | | Statement of Operations | |

|

| 20 | | | Statement of Changes in Net Assets | |

|

| 21 | | | Financial Highlights | |

|

| 22 | | | Notes to Financial Statements | |

|

| 26 | | | Report of Independent Registered Public Accounting Firm | |

|

| 27 | | | Federal Income Tax Information | |

|

| 28 | | | Board of Trustees and Management of Wanger Advisors Trust | |

|

Columbia Wanger Asset Management, LLC (CWAM) is one of the leading global small- and mid-cap equity managers in the United States with 40 years of small- and mid-cap investment experience. As of December 31, 2011, CWAM managed $29.4 billion in assets. CWAM is the investment adviser to Wanger USA, Wanger International, Wanger Select and Wanger International Select (together, the Columbia Wanger Funds) and the Columbia Acorn Family of Funds.

Investors should consider the investment objectives, risks, charges and expenses of a mutual fund carefully before investing. For a free prospectus, which contains this and other important information about the Fund, contact your financial adviser or insurance company or contact 1-888-4-WANGER. Read the prospectus carefully before investing.

An important note: Columbia Wanger Funds are available for purchase through variable annuity contracts and variable life insurance policies offered by the separate accounts of participating insurance companies and qualified pension or retirement plans.

The views expressed in "Vaccines: Medicine's Greatest Lifesaver" and in the Performance Review reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund. References to specific company securities should not be construed as a recommendation or investment advice.

1

Wanger International 2011 Annual Report

Understanding Your Expenses

As a shareholder, you incur three types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees. There are also ongoing costs, which generally include management fees and other Fund expenses. Lastly, there may be additional fees or charges imposed by the insurance company that sponsors your variable annuity and/or variable life insurance product. The following information is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to help you compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund's expenses

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in the Fund during the period. The actual and hypothetical information in the table below is based on an initial investment of $1,000 at the beginning of the period indicated and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using the Fund's actual operating expenses and total return for the period. You may use the Actual information, together with the amount invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the results by the expenses paid during the period under the Actual column. The amount listed in the "Hypothetical" column assumes a 5% annual rate of return before expenses (which is not the Fund's actual return) and then applies the Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See "Compare with other funds" below for details on how to use the hypothetical data.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing cost of investing in a fund only and do not reflect any transaction costs, such as sales charges, redemption or exchange fees. Therefore, the hypothetical calculations are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If transaction costs were included in these calculations, your costs would be higher.

July 1, 2011 – December 31, 2011

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid during

period ($) | | Fund's annualized

expense ratio (%)* | |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | | |

| Wanger International | | | 1,000.00 | | | | 1,000.00 | | | | 829.20 | | | | 1,020.46 | | | | 4.22 | | | | 4.66 | | | | 0.92 | | |

*Expenses paid during the period are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 365.

Had the investment adviser not waived fees or reimbursed a portion of expenses, account value at the end of the period would have been reduced.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Fund. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate account. The hypothetical example provided is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

2

Wanger International 2011 Annual Report

Vaccines: Medicine's Greatest Lifesaver

I recently read several books on the history of vaccines. As one of the authors put it, "Of all of the benefits of medical science, vaccination is at or near the summit."1

Deadly Diseases

"Bring out your dead!" cries a wretched man pulling a cart of bodies in Monty Python and the Holy Grail. Set in the middle ages, the movie makes fun of the impact of communicable disease at that time. In reality, such diseases were no laughing matter. Once mankind transitioned from isolated bands of nomadic hunter-gatherers to more densely populated groups of farmers, epidemic diseases began to ravage civilization.

Remarkable progress has been made as fatal, communicable disease has now become rare in the developed world. Clearly, improved sanitation and nutrition have helped, but much of the credit goes to the development of vaccines.

The First Vaccine

Dating back to at least the time of the Pharaohs, waves of smallpox epidemics ravaged mankind. In populations previously subject to the disease, mortality rates for those infected could be more than 30% and, for other populations, much more.2 North American Indians had little immunity to the disease. Their population decreased 99% between Columbus's voyage in 1492 and the year 1800, and smallpox was the largest killer.3

People observed that the disease was communicable and one who survived a smallpox infection became immune to the next epidemic of the disease. In ancient China and more recently in Asia and Africa, a crude form of vaccination called variolation developed whereby fluid from a smallpox pustule or parts of smallpox scabs were scraped into the skin of a healthy person. In most cases, immunity would build up before the disease reached a vital organ and the individual would survive.

In 1790, Lady Montague, the wife of the British ambassador to the Ottoman Empire, introduced variolation to Britain. The process was far riskier than vaccines today; most people suffered severe side effects and up to about 3% of those treated died as a result.4 But these were much better odds than for those infected with smallpox.

Edward Jenner, a pharmacist in England, learned that milkmaids were immune to smallpox because they often suffered blisters from cowpox, a related disease. In 1796, Jenner began experimenting with variolating using fluid from a milkmaid's cowpox blisters, rather than smallpox sores. When his subjects were later variolated with smallpox fluid, no reaction occurred, indicating that they were immune from smallpox. Immunization using cowpox fluids rose rapidly and protected millions of people.5

A cowpox-derived vaccine for smallpox continued to be used well into the 20th century, including use by six million New Yorkers who were inoculated during a smallpox scare in 1947. Smallpox was eradicated from nature; the last case occurred in India in 1975.6 Smallpox immunizations ended when health authorities judged the risk of side effects from the vaccine exceeded the risk of the disease returning.

The Golden Age of Vaccines

Beginning in the 1860s, tremendous scientific advances were made. Robert Koch's laboratory in Germany identified bacteria as the source of many diseases and proved that bacteria grown in a lab could cause disease.7 Koch's lab created some vaccines, including those for diphtheria and tetanus.

In France, Louis Pasteur stunned the world by developing the first rabies vaccine in 1885; until then rabies infections resulted in horrible deaths. His mantra was to "isolate, attenuate and vaccinate" the pathogen causing a disease.8 He attenuated a germ by having it reproduce in petri dishes or animal cells where it would evolve in order to optimize in its new environment. Once it evolved to the point it would no longer thrive in and harm humans, it was injected into humans with the hope that the subject would build immunity to full power germs. The Goldilocks trick of course was to make the attenuated germ weak enough so as not to cause harm, but strong enough to create immunity.

While scientific understanding of disease increased rapidly, it was primitive compared to modern times. Diagnostic tools were poor. Bacteria could be seen by optical microscopes, but viruses were unseen until the development of the electron microscope in the 1930s. Viruses were inferred to exist as a result of an 1898 experiment by Danish professor Martinus Beijerinck, who filtered bacteria out through unglazed porcelain containers, but observed remaining, and much smaller, disease-causing elements. Scientists learned how to grow viruses in laboratories only in the late 1940s.9

Early vaccines were dangerous and unreliable by today's standards, though far less dangerous than the underlying diseases they prevented. Vaccines did not stop the great influenza epidemic of 1918-1919. Of a worldwide population of one billion, an estimated 500 million were infected and more than 50 million people died.10 This virus was unusual in that it had high mortality among young, healthy people.

Vaccines continued to progress. During World War II, all 11 million U.S. soldiers were vaccinated for typhoid, tetanus, smallpox, cholera and plague. Vaccines, coupled with antibiotics, drastically improved their health. Disease deaths outnumbered battle deaths by 13:1 in the Spanish American War, matched them in World War I and were outnumbered by 1:85 in World War II.11

Maurice Hilleman's Mission

Maurice Hilleman had a role in creating more vaccines than anyone else in history, some three dozen. As noted by Arthur Allen, author of Vaccine, The Controversial Story of Medicine's Greatest Lifesaver, "...his products undoubtedly

3

Wanger International 2011 Annual Report

saved more lives than those of any other individual in the past half-century."12

Hilleman grew up in Montana, and earned a Ph.D. in microbiology at the University of Chicago where he discovered that chlamydia is a tiny bacteria rather than a virus. He then stunned his mentors by departing academia to work in industry. At Squibb, he developed a vaccine against Japanese B encephalitis to protect American Pacific troops during World War II. In 1948, he joined the Walter Reed Army Medical Center, then a hub of vaccine development.

In 1957, Hilleman moved to Merck, where he continued to develop vaccines well past his official retirement in 1984. He had a tremendous work ethic, often working seven days a week and expecting the same from his staff. He and his team were on a mission to rid the world of disease. They developed eight of 14 now common vaccines for measles, mumps, hepatitis A and B, chickenpox, meningitis, pneumonia and Hib (hemophilus influenza, which harms infants and young children).13 One of his accomplishments was the combination MMR (measles, mumps and rubella) vaccine.

Hilleman discovered that the influenza virus is particularly difficult to deal with due to frequent minor drifts in its surface, which each year makes the last year's vaccine obsolete. Periodically, the virus shifts its surface characteristics substantially, becoming much more virulent. Hilleman inferred that a shift occurred in Hong Kong in 1957 and, by having Merck produce 40 million doses of vaccine, saved thousands of lives in America. Potential future shifts keep virologists up at night.

Hilleman helped develop the first two anti-cancer vaccines. One vaccine prevents hepatitis B, the third most common known cause of cancer in the world (after sunlight and smoking).14 It was the first vaccine utilizing recombinant technology and the first made by a single protein. His innovations helped create a vaccine to prevent HPV (human papillomavirus), the cause of cervical cancer. Hilleman had high integrity, as he refused to risk changes in manufacturing processes in order to enhance yields and profits.15 He died in 2005 at age 85.

Vaccine Scares

Two notable scares set back progress on vaccine usage.

In 1982, a TV station in Washington D.C. aired "Vaccine Roulette," a story highlighting risks of the DTP (diphtheria, tetanus, pertussis) vaccine. It showed reactions well known to physicians, including cases of seizures, high fevers and fainting. In a case of ambush journalism, it edited doctors' comments out of context and failed to mention that none of the victims portrayed suffered permanent damage. Other media quoted the story further out of context, claiming permanent damage. The media also failed to mention the consequences of contracting the underlying diseases.16

In 1998, the British medical journal The Lancet published a paper alleging a link between the MMR vaccine and autism.17 It claimed that, in some cases, the vaccine caused the measles virus to lodge in the intestines and create leakage, allowing opioid peptides to escape and penetrate the brain, causing autism. The paper was under fire by scientists immediately. The opioid causation theory had already been widely discredited, the findings of measles in intestines could not be duplicated by other scientists and there was no comparison between autism rates of children who got the vaccine and those who did not. A review by 37 experts found that the theories were "biologically implausible," and the conclusions essentially worthless.18

Fourteen separate groups of investigators did statistical studies that also refuted the link.19 One notable study covered 530,000 children in Denmark from 1991-1998, comparing vaccinated and unvaccinated children. It showed "strong evidence against the hypothesis that MMR vaccination causes autism."20 By 2004, 10 of the original 12 authors of The Lancet article

withdrew their support of the paper.21 The Lancet formally retracted the paper in 2010 and, that same year, the primary author of the paper had his U. K. medical license revoked.

Once the MMR-autism link was largely discredited, vaccine opponents claimed a link between mercury in vaccines and autism. Minute amounts of ethyl mercury were utilized in vaccines, usually less than the more toxic methyl mercury infants get exposed to from the environment. Combined, in some cases, the dosage did exceed government guidelines, so the mercury was removed. Studies showed that reported rates of autism continued to climb once mercury was removed from vaccines.22 "In spite of all the concern...there has not been a single case of proven mercury toxicity from vaccines...," writes Kurt Link, author of The Vaccine Controversy: The History, Use, and Safety of Vaccinations.23

Unfortunately, many people appear to rely on one-sided scares and opinions expressed in talk shows and by celebrity activists, rather than on scientific evidence. Immunization rates around the world have fluctuated with publicity, funding for inoculations, public policy and legal requirements. Where immunizations have dropped, outbreaks have occurred. A diphtheria epidemic hit the former Soviet Union in 1993, causing 4,000 deaths.24 In Japan, where pertussis immunizations fell from 80% in 1974 to 10% in 1976, a 1979 epidemic of that disease resulted in 13,000 infections and 41 deaths.25 In the United States, where pockets of low immunization rates exist, outbreaks occur. Some of the Chicago suburbs are currently experiencing a whooping cough outbreak.26

Perspectives on Risks

There have been mistakes in vaccine development, production and use that have resulted in injuries and deaths. However, those numbers pale in comparison to the injuries and deaths caused by the underlying diseases that are being conquered by vaccines. While rare

4

Wanger International 2011 Annual Report

vaccine side effects continue to exist, drugs and vaccines come with disclosures of the known side effects and risks, however unlikely. Diseases don't.

Many people believe some vaccine-preventable diseases to be fairly benign and some are, in most cases. Yet measles is one of the most contagious viruses and has killed more children than any other disease in history.27 It hospitalized 48,000 Americans yearly in the 1960s and killed 400 during a 1964 epidemic.28

Chickenpox is perceived to be a mild disease and it usually is. Acquiring chickenpox creates lifetime immunity to the disease (though susceptibility to shingles) so some question the usefulness of the vaccine. However, Paul Offit, author of Vaccinated, One Man's Quest to Defeat the World's Deadliest Diseases, points out that chickenpox creates risk of encephalitis, hepatitis, pneumonia and Group A streptococci, the "flesh-eating bacteria." He notes that, before the vaccine, some 10,000 people a year were hospitalized and 100 died annually in the United States due to the disease or related illnesses.29

German measles (rubella) was considered a benign illness featuring a rash and a low fever until Australian ophthalmologist Sir Norman McAllister Gregg discovered a link to birth defects. When striking a mother in her first trimester, rubella causes fetal anomalies in 90% of pregnancies. In 1964-65, prior to the rubella vaccine, the last major epidemic in the United States caused thousands of birth defects.30 Hilleman's MMR vaccine was approved in 1971 and the number dropped to seven U.S. cases in 1983.31

Whooping cough (pertussis) is a horrible disease for babies and small children. Babies have died because of outbreaks when vaccination rates declined as a result of scares. The underlying vaccine has changed since the "Vaccine Roulette" television program, to an acellular version with fewer side effects.32 That is why the combination vaccine is now called DTaP rather than DTP.

While no vaccine is 100% effective, the fact remains that if the vast majority of people are vaccinated, a disease cannot infect enough victims to spread. Link writes, "In the prevaccine era, every family lost a child or knew of one so lost due to vaccine-preventable diseases. Today in the USA, the death of a child is an unexpected tragedy; in the past it was an expected sorrow."33 American life expectancies increased 30 years during the 20th century, largely due to vaccines.34

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, LLC

The information and data provided in this analysis are derived from sources that we deem to be reliable and accurate. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. The views/opinions expressed in this essay are those of the author and not of the Columbia Wanger Funds Board, are subject to change at any time based upon economic, market or other conditions, may differ from views expressed by other Columbia Management associates and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund.

The information included on Pages 3-5 of this report is unaudited.

1 Link, M.D., Kurt, The Vaccine Controversy, The History, Use, And Safety of Vaccinations, (Westport, Connecticut, Praeger Publishers 2005) p. 38.

2 Mnookin, Seth, The Panic Virus, A True Story of Medicine, Science, and Fear, (New York, New York, Simon & Schuster 2011) p. 30.

3 Offit, M.D., Paul A., Vaccinated, One Man's Quest to Defeat the World's Deadliest Diseases, (New York, New York, HarperCollins Publishers 2007) pg. 32.

4 Link, M.D., Kurt, op. cit., p. 12.

5 Allen, Arthur, Vaccine, The Controversial Story of Medicines Greatest Lifesaver, (New York, New York, W. W. Norton & Company 2007) p. 49-50.

6 Ibid., p. 115, 303.

7 Offit, M.D., Paul A., op. cit., p. 144.

8 Allen, Arthur, op. cit., p. 65, 121.

9 Offit, M.D., Paul A., op. cit., p. 37, 41-42.

10 Ibid., p. 2-3.

11 Allen, Arthur, op. cit., p. 119, 159.

12 Ibid., p. 221.

13 Link, M.D., Kurt, op. cit., p. 101.

14 Offit, M.D., Paul A., op. cit., p. 115.

15 Ibid., p. 130, 156.

16 Allen, Arthur, op. cit., p. 251-256.

17 Wakefield, Andrew J., et al., "Ileal-lymphoid-nodular Hyperplasia, Non-Specific Colitis, and Pervasive Developmental Disorders in Children," The Lancet 351, Issue 9103 (1998), p. 637-41.

18 Mnookin, Seth, op. cit., p. 106-107, 114.

19 Offit, M.D., Paul A., op. cit., p. 167.

20 Mnookin, Seth, op. cit., p. 163.

21 Murch, Simon H., et al., "Retraction of an Interpretation," The Lancet 363, Issue 9411 (2004), p. 750.

22 Mnookin, Seth, op. cit., p. 167.

23 Link, M.D., Kurt, op. cit., p. 21.

24 Ibid., p. 57.

25 Mnookin, Seth, op. cit., p. 277.

26 Synett, Lawerence, "Whooping Cough Strikes Collar Counties," Chicago Tribune, December 6, 2011.

27 Mnookin, Seth, op. cit., p. 19.

28 Allen, Arthur, op. cit., p. 217.

29 Offit, M.D., Paul A., op. cit., p. 102.

30 Link, M.D., Kurt, op. cit., p. 82-84.

31 Allen, Arthur, op. cit., p. 240.

32 Ibid., p. 352, 286.

33 Link, M.D., Kurt, op. cit., p. 163.

34 Offit, M.D., Paul A., op. cit., p. xiv.

5

Wanger International 2011 Annual Report

Performance Review Wanger International

| |  | |

|

Louis J. Mendes III

Co-Portfolio Manager | | Christopher J. Olson

Co-Portfolio Manager | |

|

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for performance updates for the most recent month-end.

Wanger International ended 2011 down 14.62%, outperforming the 16.94% decline of its primary benchmark, the S&P Global Ex-U.S. Between $500M and $5B Index. International small-cap stocks underperformed larger-cap stocks in a year marked by extreme volatility and high correlation among most risk assets. For comparison, the large-cap developed international market, as tracked by the MSCI EAFE Index, declined 12.14% during the year.

In 2010, the economic schism between stagnant, deflating developed economies and the high-growth inflationary emerging economies bore out in the strong performance of emerging market stocks. In 2011, fears of a renewed global recession dragged down all markets tied to economic growth, especially those of Europe and the emerging markets. Although early concerns over inflation in China, India and Brazil abated as the year progressed, they were replaced by the far greater concerns of potential sovereign debt defaults in Europe. European banks are important lenders in Asia and Latin America. Investors worried that the banks could serve as a transmission mechanism of European credit contraction.

Notwithstanding the horrific news related to the Japanese tsunami and associated nuclear catastrophe in the spring, Japanese equities proved to be among the best performers globally in 2011. The Fund's Japanese holdings, which represented on average 17% of the portfolio, fell less than 1% in U.S. dollar terms, buoyed in part by an appreciating yen. Internet-related companies Gree (a social networking game developer) and Start Today (an online apparel retailer) posted 181% and 86% gains, respectively, for the year for Wanger International. Investors became enthusiastic about their innovative business models, prospective near-term earnings growth in excess of 50% and high valuations assigned in transactions involving internet-related companies elsewhere in the world. We like these businesses and remain invested, but took some money off the table in both cases to fund more attractively valued new ideas.

As mentioned above, the European debt crisis became the overriding political and economic development affecting global risk premiums in the year and did take a toll on the Fund's equity holdings. Continental European holdings were off over 18%. Danish enzyme manufacturer Novozymes was an exception and up almost 11% for the year. On the downside, German auto supplier and defense contractor Rheinmetall was off 44% for the year despite solid improvements and respectable growth in its exhaust-system business, where fuel efficiency and tightening emission standards are creating opportunity. In the age of European austerity, however, the outlook for defense spending has soured, which explains the disappointing share price movement as earnings multiples of European defense stocks contracted.

Emerging market small-cap stocks, strong performers in 2010, were the worst performing equity class in 2011. The Fund's Brazilian holdings declined more than 30%, Chinese holdings more than 35% and Indian holdings more than 53%. At the end of the year, emerging market stocks represented about 24% of the Fund's assets, which compares with a benchmark weight of 25%. Our full weight here reflects our conviction in the long-term underlying opportunities offered by emerging market small-cap stocks as these emerging societies continue to negotiate the transition from informal to formal economies and raise the purchasing power and living standards of millions of people.

2012 has several major catalysts that we believe will affect global risk and the opportunity for continued growth in international small-cap equities. In the beginning of the year, all eyes will continue to look toward Europe for a resolution on the euro debt crisis. This is expected to be resolved before the high rhetoric associated with major elections of new governments in both China and the United States in the fall. As always, we will continue to work hard to find and invest in dynamic growth companies for you, our shareholders.

International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

Fund's Positions in Mentioned Holdings

As a percentage of net assets, as of 12/31/11

| Novozymes | | | 0.9 | % | |

| Gree | | | 0.7 | % | |

| Rheinmetall | | | 0.5 | % | |

| Start Today | | | 0.2 | % | |

6

Wanger International 2011 Annual Report

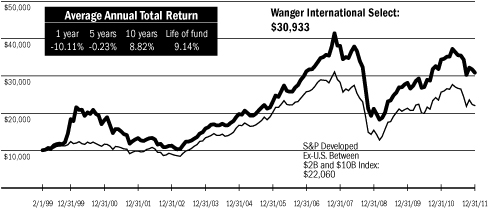

Growth of a $10,000 Investment in Wanger International

May 3, 1995 (inception date) through December 31, 2011

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. For daily and most recent month-end performance updates, please call 1-888-4-WANGER.

This graph compares the results of $10,000 invested in Wanger International on May 3, 1995 (the date the Fund began operations) through December 31, 2011, to the S&P Global Ex-U.S. Between $500M and $5B Index with dividends and capital gains reinvested. Although the index is provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the index.

Top 10 Holdings

As a percentage of net assets, as of 12/31/11

1. Far Eastone Telecom (Taiwan)

Taiwan's Third Largest Mobile Operator | | | 1.2

| % | |

2. Melco Crown Entertainment - ADR (Hong Kong)

Macau Casino Operator | | | 1.2

| % | |

3. Archipelago Resources (Indonesia)

Gold Mining Projects in Indonesia, Vietnam & the Philippines | | | 1.2

| % | |

4. Kansai Paint (Japan)

Paint Producer in Japan, India, China & Southeast Asia | | | 1.1

| % | |

5. Hexagon (Sweden)

Design, Measurement & Visualization Software & Equipment | | | 1.1

| % | |

6. Gemalto (France)

Digital Security Solutions | | | 1.1

| % | |

7. Zhaojin Mining Industry (China)

Gold Mining & Refining in China | | | 1.0

| % | |

8. Localiza Rent A Car (Brazil)

Car Rental | | | 1.0

| % | |

9. Olam International (Singapore)

Agriculture Supply Chain Manager | | | 1.0

| % | |

10. Naspers (South Africa)

Media in Africa, China, Russia & Other Emerging Markets | | | 0.9

| % | |

Top 5 Countries

As a percentage of net assets, as of 12/31/11

| Japan | | | 18.1 | % | |

| United Kingdom | | | 6.7 | | |

| Taiwan | | | 6.0 | | |

| Netherlands | | | 4.9 | | |

| United States | | | 4.7 | | |

Results as of December 31, 2011

| | | 4th quarter | | 1 year | | 5 years | | 10 years | |

| Wanger International | | | 1.63 | % | | | -14.62 | % | | | 0.21 | % | | | 10.91 | % | |

S&P Global Ex-U.S.

Between $500M and

$5B Index* | | | 0.75 | | | | -16.94 | | | | -0.58 | | | | 11.10 | | |

| MSCI EAFE Index | | | 3.33 | | | | -12.14 | | | | -4.72 | | | | 4.67 | | |

Lipper International

Growth Funds Variable

Underlying Index | | | 5.28 | | | | -13.10 | | | | -3.45 | | | | 4.18 | | |

* The Fund's primary benchmark.

NAV as of 12/31/11: $28.79

Performance numbers reflect all Fund expenses but do not include any fees and expenses imposed under your variable annuity or life insurance policy or qualified pension or retirement plan. If performance included the effect of these additional charges, it would be lower.

The Fund's annual operating expense ratio is 1.04%. The annual operating expense ratio is as stated in the Fund's prospectus that is current as of the date of this report. Differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and reimbursements as well as different time periods used in calculating the ratios. Please see Note 4 to the Financial Statements on Page 24 for more information about the Fund's fees and expenses.

All results shown assume reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

The S&P Global Ex-U.S. Between $500M and $5B Index is a subset of the broad market selected by the index sponsor representing the mid- and small-cap developed and emerging markets, excluding the United States. The Morgan Stanley Capital International Europe, Australasia, Far East (MSCI EAFE) Index (Net) is a capitalization-weighted index that tracks the total return of common stocks in 22 developed-market countries within Europe, Australasia and the Far East. The returns of the MSCI EAFE Index (Net) are presented net of the withholding tax rate applicable to foreign non-resident institutional investors in the foreign companies included in the index who do not benefit from double taxation treaties. The Lipper International Growth Funds Variable Underlying Index is an equally weighted representation of the 30 largest variable insurance underlying funds in the Lipper International Growth Funds Variable Underlying Classification. Indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the Fund. Lipper makes no adjustment for the effect of sales loads.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings.

7

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| | | Equities – 97.1% | |

| | | Asia – 43.3% | |

| | | Japan – 18.1% | |

| | 864,789 | | | Kansai Paint

Paint Producer in Japan, India, China & Southeast Asia | | $ | 7,702,340

| | |

| | 2,843,000 | | | Seven Bank

ATM Processing Services | | | 5,563,534

| | |

| | 369,100 | | | Kuraray

Special Resin, Fine Chemical, Fibers & Textures | | | 5,238,144

| | |

| | 212,600 | | | Hoshizaki Electric

Commercial Kitchen Equipment | | | 4,987,662

| | |

| | 247,042 | | | Aeon Delight

Facility Maintenance & Management | | | 4,980,148

| | |

| | 143,400 | | | Gree

Mobile Social Networking Game Developer/Platform | | | 4,929,558

| | |

| | 2,963 | | | Wacom

Computer Graphic Illustration Devices | | | 4,493,748

| | |

| | 84,111 | | | Ain Pharmaciez

Dispensing Pharmacy/Drugstore Operator | | | 4,047,540

| | |

| | 963 | | | Orix JREIT

Diversified REIT | | | 3,960,430

| | |

| | 1,920 | | | Advance Residence Investment

Residential REIT | | | 3,704,080

| | |

| | 264,609 | | | Japan Airport Terminal

Airport Terminal Operator at Haneda | | | 3,443,458

| | |

| | 36,599 | | | Nakanishi

Dental Tools & Machinery | | | 3,377,585

| | |

| | 255,000 | | | Park24

Parking Lot Operator | | | 3,372,771

| | |

| | 116,041 | | | Kintetsu World Express

Airfreight Logistics | | | 3,370,469

| | |

| | 283,000 | | | NGK Insulators

Ceramic Products for Auto, Power & Electronics | | | 3,350,583

| | |

| | 3,190,700 | | | Shinsei Bank

Commercial Bank | | | 3,299,068

| | |

| | 3,250 | | | Jupiter Telecommunications

Largest Cable Service Provider in Japan | | | 3,289,673

| | |

| | 110,416 | | | Tsumura

Traditional Chinese/Japanese Herbal Rx Drugs (Kampo) | | | 3,255,094

| | |

| | 243,200 | | | Asahi Diamond Industrial

Consumable Diamond Tools | | | 2,926,435

| | |

| | 147,503 | | | Ibiden

Electronic Parts & Ceramics | | | 2,904,048

| | |

Number of

Shares | | | | Value | |

| | 335,000 | | | Shimadzu

Analytical Instrument, Medical & Industrial Equipment | | $ | 2,825,067

| | |

| | 130,518 | | | Glory

Currency Handling Systems & Related Equipment | | | 2,807,484

| | |

| | 181,360 | | | Ushio

Industrial Light Sources | | | 2,606,638

| | |

| | 158,847 | | | Daiseki

Waste Disposal and Recycling | | | 2,580,999

| | |

| | 110,825 | | | Aeon Mall

Suburban Shopping Mall Developer, Owner & Operator | | | 2,351,123

| | |

| | 57,500 | | | Pigeon

Baby Care Products | | | 2,343,602

| | |

| | 355 | | | Fukuoka REIT

Diversified REIT in Fukuoka | | | 2,332,444

| | |

| | 90,146 | | | Icom

Two Way Radio Communication Equipment | | | 2,305,316

| | |

| | 700 | | | Mori Hills REIT Investment

Tokyo Centric Diversified REIT | | | 2,286,029

| | |

| | 780 | | | Kenedix Realty Investment

Tokyo Mid Size Office REIT | | | 2,261,533

| | |

| | 96,700 | | | Misumi Group

Industrial Components Distributor | | | 2,213,009

| | |

| | 78,358 | | | Miura

Industrial Boiler Manufacturer | | | 2,207,014

| | |

| | 60,986 | | | Hamamatsu Photonics

Optical Sensors for Medical & Industrial Applications | | | 2,126,287

| | |

| | 238,900 | | | Sintokogio

Automated Casting Machines, Surface Treatment

System & Consumables | | | 2,094,926

| | |

| | 162,666 | | | Torishima Pump Manufacturing

Industrial Pump for Power Generation &

Water Supply Systems | | | 2,081,820

| | |

| | 32,000 | | | FP Corporation

Disposable Food Trays & Containers | | | 2,073,246

| | |

| | 39,000 | | | Disco

Semiconductor Dicing & Grinding Equipment | | | 2,030,733

| | |

| | 57,179 | | | Start Today

Online Japanese Apparel Retailer | | | 1,341,423

| | |

| | 2,900 | | | Doshisha

Wholesaler | | | 83,633

| | |

| | | | | | | | 123,148,694 | | |

See accompanying notes to financial statements.

8

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| | | Taiwan – 6.0% | |

| | 4,533,000 | | | Far Eastone Telecom

Taiwan's 3rd Largest Mobile Operator | | $ | 8,515,240

| | |

| | 833,400 | | | President Chain Store

Taiwan's Number One Convenience Chain Store Operator | | | 4,538,606

| | |

| | 705,440 | | | Simplo Technology

Battery Packs for Notebook & Tablet PCs | | | 4,105,449

| | |

| | 308,700 | | | St. Shine Optical

World's Leading Disposable Contact Lens OEM | | | 3,255,949

| | |

| | 1,261,830 | | | Tripod Technologies

Printed Circuit Boards | | | 3,039,306

| | |

| | 842,000 | | | Taiwan Mobile

Taiwan's 2nd Largest Mobile Operator | | | 2,623,302

| | |

| | 1,281,900 | | | Chroma Ate

Automatic Test Systems, Testing & Measurement Instruments | | | 2,512,092

| | |

| | 1,747,000 | | | CTCI Corp

International Engineering Firm | | | 2,380,676

| | |

| | 1,292,300 | | | Taiwan Hon Chuan

Beverage Packaging (bottles, caps, labels) Manufacturer | | | 2,379,639

| | |

| | 830,000 | | | Advantech

Industrial PC & Components | | | 2,295,011

| | |

| | 743,000 | | | Radiant Opto-Electronics

Back Light Modules for LCDs | | | 2,119,702

| | |

| | 287,300 | | | PC Home

Taiwanese Internet Retail Company | | | 1,764,591

| | |

| | 310,200 | | | Lung Yen

Funeral Services & Columbaria | | | 906,704

| | |

| | 59,350 | | | Formosa International Hotels

Hotel, Food & Beverage Operation &

Hospitality Management Services | | | 767,927

| | |

| | | | | | | | 41,204,194 | | |

| | | China – 4.1% | |

| | 4,352,000 | | | Zhaojin Mining Industry

Gold Mining & Refining in China | | | 6,902,875

| | |

| | 81,000 | | | NetEase.com - ADR (a)

Chinese Online Gaming Services | | | 3,632,850

| | |

| | 140,000 | | | New Oriental Education &

Technology - ADR (a)

China's Largest Private Education Service Provider | | | 3,367,000

| | |

| | 2,440,800 | | | Want Want

Chinese Branded Consumer Food Company | | | 2,431,235

| | |

Number of

Shares | | | | Value | |

| | 1,509,500 | | | Digital China

IT Distribution & Systems Integration Services | | $ | 2,332,882

| | |

| | 644,000 | | | ENN Energy

China's Largest Private Gas Operator | | | 2,061,793

| | |

| | 1,509,000 | | | China Yurun Food (b)

Meat Processor in China | | | 1,972,381

| | |

| | 3,567,100 | | | AMVIG Holdings

Chinese Tobacco Packaging Material Supplier | | | 1,890,177

| | |

| | 28,000,000 | | | RexLot Holdings

Lottery Equipment Supplier in China | | | 1,832,813

| | |

| | 32,500 | | | 51job - ADR (a) (b)

Integrated Human Resource Service | | | 1,363,050

| | |

| | 61,602 | | | Noah Holdings - ADR (a) (b)

Wealth Management Product Distributor in China | | | 378,853

| | |

| | | | | | | | 28,165,909 | | |

| | | Singapore – 4.1% | |

| | 4,134,000 | | | Olam International

Agriculture Supply Chain Manager | | | 6,776,327

| | |

| | 4,900,000 | | | Mapletree Industrial Trust

Singapore Industrial Property Landlord | | | 4,060,070

| | |

| | 6,190,000 | | | Mapletree Logistics Trust

Industrial Property Landlord | | | 4,028,952

| | |

| | 2,730,000 | | | Ascendas REIT

Singapore Industrial Property Landlord | | | 3,854,818

| | |

| | 2,300,000 | | | CDL Hospitality Trust

Hotel Owner/Operator | | | 2,740,526

| | |

| | 4,000,000 | | | Mapletree Commercial Trust

Retail & Office Property Landlord | | | 2,621,790

| | |

| | 430,000 | | | Singapore Exchange

Singapore Equity & Derivatives Market Operator | | | 2,032,477

| | |

| | 1,840,000 | | | Goodpack Limited

International Bulk Container Leasing | | | 1,964,329

| | |

| | | | | | | | 28,079,289 | | |

| | | Hong Kong – 3.6% | |

| | 874,400 | | | Melco Crown Entertainment - ADR (a) (b)

Macau Casino Operator | | | 8,411,728

| | |

| | 2,150,000 | | | Lifestyle International

Mid- to High-end Department Store Operator in

Hong Kong & China | | | 4,732,372

| | |

| | 1,970,000 | | | L'Occitane International

Skin Care & Cosmetics Producer | | | 3,950,592

| | |

See accompanying notes to financial statements.

9

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| | | Hong Kong – 3.6% (cont) | |

| | 4,642,000 | | | Sasa International

Cosmetics Retailer | | $ | 2,558,564

| | |

| | 1,068,000 | | | AAC Technologies

Miniature Acoustic Components | | | 2,389,465

| | |

| | 1,548,400 | | | MGM China Holdings (a)

Macau Casino Operator | | | 2,014,330

| | |

| | 935,000 | | | Melco International (a)

Macau Casino Operator | | | 689,999

| | |

| | | | | | | | 24,747,050 | | |

| | | India – 2.1% | |

| | 1,398,200 | | | Jain Irrigation Systems | | | 2,274,130 | | |

| | 59,405 | | | Jain Irrigation Systems - DVR (a)

Agricultural Micro-irrigation Systems & Food Processing | | | 39,432

| | |

| | 991,200 | | | Mundra Port & Special Economic Zone

Indian West Coast Shipping Port | | | 2,237,191

| | |

| | 44,100 | | | Asian Paints

India's Largest Paint Company | | | 2,152,612

| | |

| | 2,145,900 | | | Manappuram Finance

Short-term Lending Collateralized by Household Gold | | | 1,858,222

| | |

| | 188,000 | | | Shriram Transport Finance

Truck Financing in India | | | 1,487,210

| | |

| | 178,000 | | | United Breweries

India's Largest Brewer | | | 1,286,145

| | |

| | 4,020,100 | | | REI Agro

Basmati Rice Processing | | | 1,247,610

| | |

| | 1,250,800 | | | S. Kumars Nationwide

Textiles, Clothing & Retail | | | 555,903

| | |

| | 199,131 | | | SKIL Ports and Logistics (a)

Indian Container Port Project | | | 491,708

| | |

| | 99,500 | | | Titan Industries

Jewelry, Watches & Eyeglasses | | | 319,941

| | |

| | | | | | | | 13,950,104 | | |

| | | Indonesia – 1.4% | |

| | 7,592,066 | | | Archipelago Resources (a)

Gold Mining Projects in Indonesia, Vietnam & the Philippines | | | 8,150,168

| | |

| | 1,194,900 | | | Ace Indonesia

Home Improvement Retailer | | | 539,871

| | |

Number of

Shares | | | | Value | |

| | 1,757,800 | | | Tower Bersama Infrastructure

Communications Towers | | $ | 460,146

| | |

| | 874,600 | | | Jasa Marga

Largest Toll Road Operator in Indonesia | | | 404,636

| | |

| | | | | | | | 9,554,821 | | |

| | | Mongolia – 1.1% | |

| | 4,447,500 | | | Mongolian Mining (a)

Coking Coal Mining in Mongolia | | | 3,334,401

| | |

| | 129,245 | | | Ivanhoe Mines (a) | | | 2,295,010 | | |

| | 117,980 | | | Ivanhoe Mines (a) (c)

Copper Mine Project in Mongolia | | | 2,090,606

| | |

| | | | | | | | 7,720,017 | | |

| | | Korea – 1.1% | |

| | 155,600 | | | Woongjin Coway (a)

South Korean Household Appliance Rental Service Provider | | | 4,954,829

| | |

| | 13,000 | | | NHN (a)

Korean Online Search Services | | | 2,382,579

| | |

| | 7,600 | | | Handsome (a)

Korea's Leading High-end Apparel Company | | | 196,142

| | |

| | | | | | | | 7,533,550 | | |

| | | Thailand – 0.8% | |

| | 14,859,100 | | | Home Product Center

Home Improvement Retailer | | | 5,174,350

| | |

| | | Philippines – 0.7% | |

| | 9,023,600 | | | SM Prime Holdings

Shopping Mall Operator | | | 2,738,052

| | |

| | 1,023,030 | | | Int'l Container Terminal

Container Handling Terminals & Port Management | | | 1,238,127

| | |

| | 2,064,100 | | | Manila Water Company

Water Utility Company in the Philippines | | | 913,997

| | |

| | | | | | | | 4,890,176 | | |

| | | Cambodia – 0.2% | |

| | 5,252,200 | | | Nagacorp

Casino/Entertainment Complex in Cambodia | | | 1,322,186

| | |

| | | | | Total Asia | | | 295,490,340 | | |

See accompanying notes to financial statements.

10

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| | | Europe – 33.2% | |

| | | United Kingdom – 6.7% | |

| | 185,000 | | | Intertek Group

Testing, Inspection & Certification Services | | $ | 5,846,657

| | |

| | 2,250,000 | | | Charles Taylor (d)

Insurance Services | | | 4,442,065

| | |

| | 680,000 | | | Chemring

Defense Manufacturer of Countermeasures & Energetics | | | 4,223,104

| | |

| | 378,000 | | | JLT Group

International Business Insurance Broker | | | 4,047,600

| | |

| | 980,000 | | | Workspace Group

United Kingdom Real Estate | | | 3,435,780

| | |

| | 413,901 | | | Serco

Facilities Management | | | 3,046,816

| | |

| | 87,000 | | | Rotork

Valve Actuators for Oil & Water Pipelines | | | 2,607,642

| | |

| | 56,000 | | | Next

Clothes & Home Retailer in the United Kingdom | | | 2,380,314

| | |

| | 500,000 | | | GlobeOp Financial Services

Hedge Fund Administrator | | | 2,213,025

| | |

| | 223,973 | | | Smith and Nephew

Medical Equipment & Supplies | | | 2,175,677

| | |

| | 349,000 | | | Abcam

Online Sales of Antibodies | | | 1,978,289

| | |

| | 90,604 | | | Tullow Oil

Oil & Gas Producer | | | 1,972,726

| | |

| | 307,400 | | | Domino's Pizza United Kingdom & Ireland

Pizza Delivery in United Kingdom, Ireland & Germany | | | 1,921,504

| | |

| | 318,303 | | | Premier Oil (a)

Oil & Gas Producer in Europe, Pakistan & Asia | | | 1,794,398

| | |

| | 223,300 | | | Shaftesbury

London Prime Retail REIT | | | 1,620,179

| | |

| | 556,698 | | | PureCircle (a)

Natural Sweeteners | | | 821,324

| | |

| | 58,825 | | | Greggs

Bakery | | | 462,258

| | |

| | 238,400 | | | Sterling Resources (a) | | | 390,801 | | |

| | 161,600 | | | Sterling Resources (a) (e) (f)

Oil & Gas Exploration - Europe | | | 259,607

| | |

| | 306,096 | | | Kesa Electricals

Europe's Leading Electricals Retailers | | | 319,922

| | |

| | | | | | | | 45,959,688 | | |

Number of

Shares | | | | Value | |

| | | Netherlands – 4.9% | |

| | 242,087 | | | Imtech (b)

Electromechanical & ICT Installation & Maintenance | | $ | 6,271,124

| | |

| | 306,949 | | | Aalberts Industries

Flow Control & Heat Treatment | | | 5,156,550

| | |

| | 85,184 | | | Fugro

Sub-sea Oilfield Services | | | 4,949,648

| | |

| | 169,844 | | | Koninklijke TenCate

Advanced Textiles & Industrial Fabrics | | | 4,673,388

| | |

| | 189,614 | | | UNIT4

Business Software Development | | | 4,490,966

| | |

| | 28,860 | | | Core Laboratories (b)

Oil & Gas Reservoir Consulting | | | 3,288,597

| | |

| | 161,566 | | | Arcadis

Engineering Consultants | | | 2,530,193

| | |

| | 39,474 | | | Vopak

World's Largest Operator of Petroleum &

Chemical Storage Terminals | | | 2,085,718

| | |

| | | | | | | | 33,446,184 | | |

| | | Germany – 4.0% | |

| | 317,594 | | | Wirecard

Online Payment Processing & Risk Management | | | 5,105,193

| | |

| | 18,409 | | | Rational

Commercial Ovens | | | 4,007,509

| | |

| | 198,108 | | | Rhoen-Klinikum

Health Care Services | | | 3,774,228

| | |

| | 84,100 | | | Rheinmetall

Defense & Automotive | | | 3,726,358

| | |

| | 79,100 | | | Dürr

Automotive Plant Engineering &

Associated Capital Equipment | | | 3,480,757

| | |

| | 105,772 | | | CTS Eventim

Event Ticket Sales | | | 3,175,975

| | |

| | 68,400 | | | Elringklinger

Automobile Components | | | 1,697,943

| | |

| | 20,900 | | | Bertrandt

Outsourced Engineering | | | 1,371,697

| | |

| | 45,390 | | | Deutsche Beteiligungs

Private Equity Investment Management | | | 915,263

| | |

| | | | | | | | 27,254,923 | | |

See accompanying notes to financial statements.

11

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| | | France – 4.0% | |

| | 149,400 | | | Gemalto

Digital Security Solutions | | $ | 7,266,507

| | |

| | 67,352 | | | Eurofins Scientific

Food, Pharmaceuticals & Materials Screening & Testing | | | 4,910,306

| | |

| | 69,867 | | | Neopost

Postage Meter Machines | | | 4,707,546

| | |

| | 125,400 | | | Saft Batteries

Niche Battery Manufacturer | | | 3,546,234

| | |

| | 44,544 | | | Rubis

Tank Storage & Liquefied Petroleum Gas Distribution | | | 2,329,104

| | |

| | 28,900 | | | Norbert Dentressangle

Leading European Logistics & Transport Group | | | 2,019,807

| | |

| | 57,400 | | | Mersen

Advanced Industrial Materials | | | 1,734,671

| | |

| | 220,933 | | | Hi-Media (a)

Online Advertiser in Europe | | | 631,933

| | |

| | | | | | | | 27,146,108 | | |

| | | Switzerland – 3.7% | |

| | 32,820 | | | Partners Group

Private Markets Asset Management | | | 5,726,816

| | |

| | 27,986 | | | Geberit (a)

Plumbing Supplies | | | 5,392,809

| | |

| | 37,516 | | | Kuehne & Nagel

Freight Forwarding/Logistics | | | 4,213,710

| | |

| | 41,000 | | | Dufry Group (a)

Operates Airport Duty Free & Duty Paid Shops | | | 3,773,502

| | |

| | 1,958 | | | Sika

Chemicals for Construction & Industrial Applications | | | 3,689,620

| | |

| | 86,652 | | | Bank Sarasin & Cie

Private Banking | | | 2,532,308

| | |

| | | | | | | | 25,328,765 | | |

| | | Sweden – 2.2% | |

| | 508,007 | | | Hexagon

Design, Measurement & Visualization Software & Equipment | | | 7,595,690

| | |

| | 513,810 | | | Sweco

Engineering Consultants | | | 4,292,918

| | |

| | 84,900 | | | Unibet

European Online Gaming Operator | | | 1,955,326

| | |

Number of

Shares | | | | Value | |

| | 111,426 | | | East Capital Explorer

Sweden-based Russia/Central Eastern Europe

Investment Fund | | $ | 870,256

| | |

| | | | | | | | 14,714,190 | | |

| | | Italy – 1.7% | |

| | 338,100 | | | Ansaldo STS

Railway Systems Integrator | | | 3,206,569

| | |

| | 1,692,600 | | | CIR

Italian Holding Company | | | 2,699,242

| | |

| | 689,000 | | | Geox (b)

Apparel & Shoe Maker | | | 1,926,094

| | |

| | 221,000 | | | Pirelli

Global Tire Supplier | | | 1,852,599

| | |

| | 21,000 | | | Tod's (b)

Leather Shoes & Bags | | | 1,705,895

| | |

| | | | | | | | 11,390,399 | | |

| | | Denmark – 1.4% | |

| | 206,515 | | | Novozymes

Industrial Enzymes | | | 6,375,274

| | |

| | 21,676 | | | SimCorp

Software for Investment Managers | | | 3,309,918

| | |

| | | | | | | | 9,685,192 | | |

| | | Ireland – 0.7% | |

| | 1,112,900 | | | United Drug

Irish Pharmaceutical Wholesaler & Outsourcer | | | 2,952,761

| | |

| | 36,400 | | | Paddy Power

Irish Betting Services | | | 2,097,134

| | |

| | | | | | | | 5,049,895 | | |

| | | Russia – 0.7% | |

| | 264,200 | | | Petropavlovsk

Gold & Iron Ore Mining in Russia | | | 2,523,361

| | |

| | 77,500 | | | Mail.ru - GDR (a) (f)

Internet Social Networking & Games for Russian Speakers | | | 2,015,000

| | |

| | | | | | | | 4,538,361 | | |

| | | Iceland – 0.6% | |

| | 4,344,101 | | | Marel (a)

Largest Manufacturer of Poultry &

Fish Processing Equipment | | | 4,443,233

| | |

See accompanying notes to financial statements.

12

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| | | Norway – 0.4% | |

| | 302,648 | | | Atea

Leading Nordic IT Hardware/Software Re-seller &

Installation Company | | $ | 3,036,170

| | |

| | | Czech Republic – 0.4% | |

| | 16,891 | | | Komercni Banka

Leading Czech Republic Universal Bank | | | 2,846,999

| | |

| | | Belgium – 0.4% | |

| | 53,991 | | | EVS Broadcast Equipment

Digital Live Mobile Production Software & Systems | | | 2,759,477

| | |

| | | Portugal – 0.4% | |

| | 1,002,300 | | | Redes Energéticas Nacionais

Portuguese Power Transmission & Gas Transportation | | | 2,737,149

| | |

| | | Spain – 0.4% | |

| | 61,803 | | | Red Eléctrica de España

Spanish Power Transmission | | | 2,644,822

| | |

| | | Finland – 0.3% | |

| | 127,941 | | | Stockmann

Department Store & Fashion Retailer in

Scandinavia & Russia | | | 1,983,741

| | |

| | | Kazakhstan – 0.2% | |

| | 217,900 | | | Halyk Savings Bank of

Kazakhstan - GDR (a)

Largest Retail Bank & Insurer in Kazakhstan | | | 1,058,994

| | |

| | | Greece – 0.1% | |

| | 839,300 | | | Intralot

Lottery & Gaming Systems & Services | | | 731,056

| | |

| | | | | Total Europe | | | 226,755,346 | | |

| | | Other Countries – 15.7% | |

| | | United States – 4.7% | |

| | 78,368 | | | Alexion Pharmaceuticals (a)

Biotech Focused on Orphan Diseases | | | 5,603,312

| | |

| | 122,233 | | | World Fuel Services

Global Fuel Broker | | | 5,131,341

| | |

| | 120,500 | | | Atwood Oceanics (a)

Offshore Drilling Contractor | | | 4,794,695

| | |

Number of

Shares | | | | Value | |

| | 131,000 | | | BioMarin Pharmaceutical (a)

Biotech Focused on Orphan Diseases | | $ | 4,503,780

| | |

| | 75,660 | | | FMC Technologies (a)

Oil & Gas Wellhead Manufacturer | | | 3,951,722

| | |

| | 121,361 | | | Textainer Group Holdings (b)

Top International Container Leasor | | | 3,534,032

| | |

| | 33,000 | | | Oil States International (a)

Diversified North American Oil Service Provider | | | 2,520,210

| | |

| | 70,000 | | | Hornbeck Offshore (a)

Supply Vessel Operator in U.S. Gulf of Mexico | | | 2,171,400

| | |

| | | | | | | | 32,210,492 | | |

| | | Canada – 4.7% | |

| | 173,849 | | | CCL Industries

Leading Global Label Manufacturer | | | 5,343,030

| | |

| | 77,920 | | | Baytex (b)

Oil & Gas Producer in Canada | | | 4,357,401

| | |

| | 152,815 | | | ShawCor

Oil & Gas Pipeline Products | | | 4,332,071

| | |

| | 82,600 | | | Onex Capital

Private Equity | | | 2,690,226

| | |

| | 71,742 | | | AG Growth

Leading Manufacturer of Augers &

Grain Handling Equipment | | | 2,639,401

| | |

| | 131,430 | | | Black Diamond Group

Provides Accommodations/Equipment for

Oil Sands Development | | | 2,381,544

| | |

| | 107,600 | | | Alliance Grain Traders

Global Leader in Pulse Processing & Distribution | | | 2,193,720

| | |

| | 90,000 | | | Celtic Exploration (a)

Canadian Oil & Gas Producer | | | 2,020,417

| | |

| | 135,000 | | | Crew Energy (a)

Canadian Oil & Gas Producer | | | 1,490,798

| | |

| | 318,277 | | | Horizon North Logistics

Provides Diversified Oil Service Offering in Northern Canada | | | 1,455,873

| | |

| | 92,000 | | | Athabasca Oil Sands (a)

Oil Sands SAGD & Alberta Deep Basin Development | | | 1,127,931

| | |

| | 378,516 | | | DeeThree Exploration (a) (e) | | | 746,443 | | |

| | 133,000 | | | DeeThree Exploration (a)

Canadian Oil & Gas Producer | | | 267,632

| | |

| | 847,500 | | | Southern Arc Minerals (a) (e)

Gold and Copper Exploration in Indonesia | | | 543,066

| | |

See accompanying notes to financial statements.

13

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| | | Canada – 4.7% (cont) | |

| | 228,671 | | | Pan Orient (a)

Growth Oriented, Return-focused Asian Explorer | | $ | 437,702

| | |

| | | | | | | | 32,027,255 | | |

| | | South Africa – 4.3% | |

| | 146,600 | | | Naspers

Media in Africa, China, Russia & Other Emerging Markets | | | 6,414,040

| | |

| | 628,700 | | | Adcock Ingram Holdings

Manufacturer of Pharmaceuticals & Medical Supplies | | | 4,809,165

| | |

| | 466,185 | | | Mr. Price

South African Retailer of Apparel, Household &

Sporting Goods | | | 4,608,403

| | |

| | 2,364,500 | | | Rand Merchant Insurance

Directly Sold Property & Casualty Insurance;

Holdings in Other Insurers | | | 3,924,943

| | |

| | 1,225,533 | | | Coronation Fund Managers

South African Fund Manager | | | 3,446,197

| | |

| | 859,800 | | | Northam Platinum

Platinum Mining in South Africa | | | 3,195,273

| | |

| | 131,123 | | | Massmart Holdings

General Merchandise, Food & Home Improvement Stores;

Wal-Mart Subsidiary | | | 2,745,241

| | |

| | | | | | | | 29,143,262 | | |

| | | Australia – 1.2% | |

| | 328,525 | | | UGL

Engineering & Facilities Management | | | 3,992,365

| | |

| | 61,985 | | | Cochlear

Cochlear Implants | | | 3,936,737

| | |

| | | | | | | | 7,929,102 | | |

| | | Israel – 0.6% | |

| | 382,004 | | | Israel Chemicals

Producer of Potash, Phosphates, Bromine &

Specialty Chemicals | | | 3,959,370

| | |

| | | Senegal – 0.2% | |

| | 6,312 | | | Sonatel

Leading Telecoms Operator in Western Africa | | | 1,494,483

| | |

| | | | | Total Other Countries | | | 106,763,964 | | |

Number of

Shares | | | | Value | |

| | | Latin America – 4.9% | |

| | | Brazil – 3.0% | |

| | 500,000 | | | Localiza Rent A Car

Car Rental | | | 6,862,351

| | |

| | 818,300 | | | Suzano

Brazilian Pulp & Paper Producer | | | 2,956,892

| | |

| | 152,100 | | | Multiplus

Loyalty Program Operator in Brazil | | | 2,629,795

| | |

| | 180,000 | | | Odontoprev

Dental Insurance | | | 2,566,948

| | |

| | 447,400 | | | MRV Engenharia

Brazilan Low-income Property Developer | | | 2,566,508

| | |

| | 269,400 | | | Mills Estruturas e Servicos de Engenharia

Civil Engineering & Construction | | | 2,556,429

| | |

| | | | | | | | 20,138,923 | | |

| | | Mexico – 0.6% | |

| | 77,276 | | | Grupo Aeroportuario del Sureste - ADR

Mexican Airport Operator | | | 4,322,819

| | |

| | | Argentina – 0.4% | |

| | 220,833 | | | Union Agriculture Group (a) (e) (g)

Farmland Operator in Uruguay | | | 2,201,705

| | |

| | 845,000 | | | Madalena Ventures (a) (e)

Oil & Gas Exploration in Argentina | | | 739,702

| | |

| | | | | | | | 2,941,407 | | |

| | | Chile – 0.4% | |

| | 46,828 | | | Sociedad Quimica y Minera de

Chile - ADR (b)

Producer of Specialty Fertilizers, Lithium & Iodine | | | 2,521,688

| | |

| | | Guatemala – 0.3% | |

| | 116,400 | | | Tahoe Resources (a)

Silver Project in Guatemala | | | 2,020,076

| | |

| | | Colombia – 0.2% | |

| | 1,152,300 | | | Canacol (a)

Oil Producer in South America | | | 870,941

| | |

| | 3,074,000 | | | Gulf United (a) (e)

Prospecting for Oil Alongside Large Producers in Colombia | | | 649,229

| | |

| | | | 1,520,170 | | |

| | | | | Total Latin America | | | 33,465,083 | | |

Total Equities

(Cost: $530,074,453) – 97.1% | | | 662,474,733 | | |

See accompanying notes to financial statements.

14

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

Number of

Shares | | | | Value | |

| Securities Lending Collateral – 2.7% | |

| | 18,597,914 | | | Dreyfus Government Cash

Management Fund

(7 day yield of 0.00%) (h) | | $ | 18,597,914 | | |

Total Securities Lending Collateral

(Cost: $18,597,914) | | | 18,597,914 | | |

Total Investments

(Cost: $548,672,367) (i) (j) – 99.8% | | | 681,072,647 | | |

Obligation to Return Collateral for

Securities Loaned – (2.7)% | | | (18,597,914 | ) | |

| Cash and Other Assets Less Liabilities – 2.9% | | | 19,742,517 | | |

| Total Net Assets – 100.0% | | $ | 682,217,250 | | |

ADR = American Depositary Receipts

DVR = Differential Voting Right Equity Shares

GDR = Global Depositary Receipts

AUD = Australian Dollar

CAD = Canadian Dollar

EUR = Euro

USD = US Dollar

Notes to Statement of Investments:

(a) Non-income producing security.

(b) All or a portion of this security was on loan at December 31, 2011. The total market value of securities on loan at December 31, 2011 was $18,143,573.

(c) Security is traded on a U.S. exchange.

(d) An affiliated person of the Fund may include any company in which the Fund owns five percent or more of its outstanding voting shares. Holdings and transactions in this affiliated company during the year ended December 31, 2011, are as follows:

Affiliates | | Balance

of Shares

Held

12/31/10 | | Purchases/

Additions | | Sales/

Reductions | | Balance of

Shares

Held

12/31/11 | | Value | | Dividend | |

Charles

Taylor | | | 2,250,000 | | | | — | | | | — | | | | 2,250,000 | | | $ | 4,442,065 | | | $ | 277,570 | | |

The aggregate cost and value of this company at December 31, 2011, was $9,152,033 and $4,442,065, respectively. Investments in the affiliated company represented 0.65% of the Fund's total net assets at December 31, 2011.

(e) Denotes a restricted security, which is subject to restrictions on resale under federal securities laws. These securities are valued at a fair value determined in good faith under consistently applied procedures established by the Board of Trustees. At December 31, 2011, the market value of these securities amounted to $5,139,751, which represented 0.75% of total net assets.

Additional information on these securities is as follows:

Security | | Acquisition

Dates | | Shares | | Cost | | Value | |

| Union Agriculture Group | | 12/08/10-

12/16/11 | | | 220,833 | | | $ | 2,649,999 | | | $ | 2,201,705 | | |

| DeeThree Exploration | | 09/07/10-

03/08/11 | | | 378,516 | | | | 1,283,408 | | | | 746,443 | | |

| Madalena Ventures | | 10/21/10 | | | 845,000 | | | | 535,436 | | | | 739,702 | | |

| Gulf United | | 02/11/11 | | | 3,074,000 | | | | 922,200 | | | | 649,229 | | |

| Southern Arc Minerals | | 02/16/11 | | | 847,500 | | | | 1,374,835 | | | | 543,066 | | |

| Sterling Resources | | 12/02/10 | | | 161,600 | | | | 482,244 | | | | 259,607 | | |

| | | | | $7,248,122 | | $5,139,752 | |

(f) Security exempt from registration under Section 4(2) of the Securities Act of 1933. This security may only be resold in exempt transactions to qualified buyers. Private resales of this security to qualified institutional buyers are also exempt from registration pursuant to Rule 144A under the Securities Act of 1933. At December 31, 2011, this security had an aggregate value of $2,274,607, which represented 0.33% of total net assets.

(g) Illiquid security.

(h) Investment made with cash collateral received from securities lending activity.

(i) On December 31, 2011, the Fund's total investments were denominated in currencies as follows:

| Currency | | Value | | Percentage of

Net Assets | |

| Japanese Yen | | $ | 123,148,694 | | | | 18.0 | | |

| Euro | | | 111,855,156 | | | | 16.4 | | |

| US Dollar | | | 67,512,611 | | | | 9.9 | | |

| Pound Sterling | | | 56,474,518 | | | | 8.3 | | |

| Taiwan Dollar | | | 41,204,194 | | | | 6.0 | | |

| Hong Kong Dollar | | | 40,416,065 | | | | 5.9 | | |

| Canadian Dollar | | | 38,603,391 | | | | 5.7 | | |

Other currencies less than

5% of total net assets | | | 183,260,104 | | | | 26.9 | | |

Cash and other assets

less liabilities | | | 19,742,517 | | | | 2.9 | | |

| | | $ | 682,217,250 | | | | 100.0 | | |

(j) At December 31, 2011, for federal income tax purposes, cost of investments was $570,434,330 and net unrealized appreciation was $110,638,317 consisting of gross unrealized appreciation of $160,305,306 and gross unrealized depreciation of $(49,666,989).

See accompanying notes to financial statements.

15

Wanger International 2011 Annual Report

Wanger International

Statement of Investments, December 31, 2011

At December 31, 2011, the Fund had entered into the following forward foreign currency exchange contracts:

Forward

Foreign

Currency

Exchange

Contracts

to Buy | | Forward

Foreign

Currency

Exchange

Contracts

to Sell | | Principal

Amount in

Foreign

Currency | | Principal

Amount in

U.S. Dollar | | Settlement

Date | | Unrealized

Appreciation | |

| AUD | | | | USD | | | | | 3,719,980 | | | $ | 3,750,000 | | | 01/13/12 | | $ | 50,532 | | |

| CAD | | | | USD | | | | | 2,861,880 | | | | 2,800,000 | | | 01/13/12 | | | 8,620 | | |

| USD | | | | EUR | | | | | 4,684,874 | | | | 6,452,243 | | | 01/13/12 | | | 388,478 | | |

| | | | | | | | | $ | 13,002,243 | | | | | | | $ | 447,630 | | |

The counterparty for all forward foreign currency exchange contracts is State Street Bank and Trust Company.

Fair Value Measurements

Various inputs are used in determining the value of the Fund's investments, following the input prioritization hierarchy established by GAAP. These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical securities

• Level 2 – prices determined using other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk and others)

• Level 3 – prices determined using significant unobservable inputs where quoted prices or observable inputs are unavailable or less reliable (including management's own assumptions about the factors market participants would use in pricing an investment)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Examples of the types of securities in which the Fund would typically invest and how they are classified within this hierarchy are as follows. Typical Level 1 securities include exchange traded domestic equities, mutual funds whose NAVs are published each day and exchange traded foreign equities that are not statistically fair valued. Typical Level 2 securities include exchange traded foreign equities that are statistically fair valued, forward foreign currency exchange contracts and short-term investments valued at amortized cost. Additionally, securities fair valued by the Valuation Committee of the Fund's Board of Trustees that rely on significant observable inputs are also included in Level 2. Typical Level 3 securities include any security fair valued by the Fund's Valuation Committee that relies on significant unobservable inputs.

The following table summarizes the inputs used, as of December 31, 2011, in valuing the Fund's assets:

| Investment Type | | Other

Quoted Prices

(Level 1) | | Significant

Observable

Inputs

(Level 2) | | Significant

Unobservable

Inputs

(Level 3) | | Total | |

| Equities | |

| Asia | | $ | 21,539,097 | | | $ | 273,951,243 | | | $ | — | | | $ | 295,490,340 | | |

| Europe | | | 3,679,398 | | | | 223,075,948 | | | | — | | | | 226,755,346 | | |

| Other Countries | | | 62,948,238 | | | | 43,815,726 | | | | — | | | | 106,763,964 | | |

| Latin America | | | 29,874,447 | | | | 1,388,931 | | | | 2,201,705 | | | | 33,465,083 | | |

| Total Equities | | | 118,041,180 | | | | 542,231,848 | | | | 2,201,705 | | | | 662,474,733 | | |

Total Securities

Lending Collateral | | | 18,597,914 | | | | — | | | | — | | | | 18,597,914 | | |

| Total Investments | | | 136,639,094 | | | | 542,231,848 | | | | 2,201,705 | | | | 681,072,647 | | |

Unrealized Appreciation

on Forward Foreign

Currency Exchange

Contracts | | | — | | | | 447,630 | | | | — | | | | 447,630 | | |

| Total | | $ | 136,639,094 | | | $ | 542,679,478 | | | $ | 2,201,705 | | | $ | 681,520,277 | | |

The Fund's assets assigned to the Level 2 input category are generally valued using a market approach, in which a security's value is determined through its correlation to prices and information from observable market transactions for similar or identical assets. Foreign equities are generally valued at the last sales price on the foreign exchange or market on which they trade. The Fund may use a systematic fair valuation model, in accordance with the policy adopted by the Board of Trustees, provided by an independent third party to value securities principally traded in foreign markets in order to adjust for possible stale pricing that may occur between the close of the foreign exchanges and the time for valuation. These models take into account available market data including intraday index, ADR, and ETF movements. Forward foreign currency exchange contracts are valued at the prevailing forward exchange rate of the underlying currencies. Securities acquired via private placement that have a holding period or an extended settlement period are valued at a discount to the same shares that are trading freely on the market. These discounts are determined by the adviser's experience with similar securities or situations. Factors may include, but are not limited to, trade volume, shares outstanding and stock price.

The Fund's assets assigned to the Level 3 input category are valued at fair value as determined in good faith under consistently applied procedures established by and under the general supervision of the Board of Trustees. To determine fair value, management will utilize the valuation technique that they deem the most appropriate in the circumstances. Securities for which no market exists are valued based upon the market approach using some unobservable inputs which may include, but are not limited to, projected earnings, available cash, line of business, multiples, and consideration of the prioritization of the equity in a company's capital structure.

The following table shows transfers between Level 1 and Level 2 of the fair value hierarchy:

| Transfers In | | Transfers Out | |

| Level 1 | | Level 2 | | Level 1 | | Level 2 | |

| $ | 33,231,276 | | | $ | 4,258,800 | | | $ | 4,258,800 | | | $ | 33,231,276 | | |

Financial assets were transferred from Level 2 to Level 1 as they resumed trading during the period and as resale restrictions expired.