UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08748 | |||||||

| ||||||||

Wanger Advisors Trust | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

225 Franklin Street, Boston, Massachusetts |

| 02110 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Scott R. Plummer 5228 Ameriprise Financial Center Minneapolis, MN 55474 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 1-612-671-1947 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | June 30, 2012 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Wanger International

2012 Semiannual Report

Not FDIC insured • No bank guarantee • May lose value

Wanger International

2012 Semiannual Report

Table of Contents

| 2 | Understanding Your Expenses | ||||||

| 3 | Genetic Science | ||||||

| 6 | Performance Review | ||||||

| 8 | Statement of Investments | ||||||

| 19 | Statement of Assets and Liabilities | ||||||

| 19 | Statement of Operations | ||||||

| 20 | Statement of Changes in Net Assets | ||||||

| 21 | Financial Highlights | ||||||

| 22 | Notes to Financial Statements | ||||||

| 26 | Board Approval of the Advisory Agreement | ||||||

Columbia Wanger Asset Management, LLC (CWAM) is one of the leading global small- and mid-cap equity managers in the United States with over 40 years of small- and mid-cap investment experience. As of June 30, 2012, CWAM managed $31.0 billion in assets. CWAM is the investment manager to Wanger USA, Wanger International, Wanger Select and Wanger International Select (together, the Columbia Wanger Funds) and the Columbia Acorn Family of Funds.

Investors should consider the investment objectives, risks, charges and expenses of a mutual fund carefully before investing. For a free prospectus, which contains this and other important information about the Fund, contact your financial adviser or insurance company or contact 1-888-4-WANGER. Read the prospectus carefully before investing.

An important note: Columbia Wanger Funds are available for purchase through variable annuity contracts and variable life insurance policies offered by the separate accounts of participating insurance companies and qualified pension or retirement plans.

The views expressed in "Genetic Science" and in the Performance Review reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund. References to specific company securities should not be construed as a recommendation or investment advice.

1

Wanger International 2012 Semiannual Report

Understanding Your Expenses

As a shareholder, you incur three types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees. There are also ongoing costs, which generally include management fees and other Fund expenses. Lastly, there may be additional fees or charges imposed by the insurance company that sponsors your variable annuity and/or variable life insurance product. The following information is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to help you compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund's expenses

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in the Fund during the period. The actual and hypothetical information in the table below is based on an initial investment of $1,000 at the beginning of the period indicated and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using the Fund's actual operating expenses and total return for the period. You may use the Actual information, together with the amount invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the results by the expenses paid during the period under the Actual column. The amount listed in the "Hypothetical" column assumes a 5% annual rate of return before expenses (which is not the Fund's actual return) and then applies the Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See "Compare with other funds" below for details on how to use the hypothetical data.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing cost of investing in a fund only and do not reflect any transaction costs, such as sales charges, redemption or exchange fees. Therefore, the hypothetical calculations are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If transaction costs were included in these calculations, your costs would be higher.

January 1, 2012 – June 30, 2012

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during period ($) | Fund's annualized expense ratio (%)* | ||||||||||||||||||||||||||||

| Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | ||||||||||||||||||||||||||

| Wanger International | 1,000.00 | 1,000.00 | 1,086.40 | 1,019.59 | 5.50 | 5.32 | 1.06 | ||||||||||||||||||||||||

*Expenses paid during the period are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 366.

Had the investment manager not waived fees or reimbursed a portion of expenses, account value at the end of the period would have been reduced.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Fund. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate account. The hypothetical example provided is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

2

Wanger International 2012 Semiannual Report

Genetic Science

Genetic theory began with Gregor Mendel, a friar who in the middle 19th century meticulously bred different types of peas and tracked traits of offspring. He discovered recessive genes, which are carried by one generation but expressed in the next if both parents have that gene. Human genetic studies began a few decades later. In 1872, Huntington's disease was the first genetic disease identified by scientific research.1

Humans normally have 23 pairs of chromosomes, with half of each pair inherited from each parent. The chromosomes combined consist of over 20,000 genes. These genes ultimately consist of over 3 billion units of four different nitrogenous bases, labeled by their first letters: A, G, C and T.2

DNA, the double helix structure of bases assembled into genes, was discovered by James Watson and Francis Crick in 1953. Various genes were identified over the next several decades. The Human Genome Project, an effort to sequence and identify all genes and bases in human DNA, started in 1990. After $2.7 billion of expenditures over 13 years, a composite genome from three people was specified.3

Gene Sequencing

Kevin Davies' book, The $1,000 Genome, discusses the incredible progress made in gene sequencing technology. First generation sequencing used bacteria to purify and grow DNA fragments utilizing equipment made by Applied Biosystems, which dominated the market for 15 years.4 Hundreds of machines labored for years to complete the Human Genome Project sequencing, at a direct cost of tens of millions of dollars.5

A company called 454 Life Sciences, later acquired by Roche, developed a second generation sequencer. Utilizing a semiconductor chip with thousands of wells, DNA fragments were sequenced in parallel via real-time image processing. First shipped in 2005, the $500,000 machines then sold as fast as they could be built. James Watson's genome was sequenced in 2007 at a cost of $1 million.6

In 2006, Solexa shipped a sequencing machine that also sequenced in parallel, but had throughput and cost advantages. Illumina bought Solexa later that year. By 2007, the equipment could sequence a human's DNA at a cost of $100,000.7 Illumina subsequently created faster and more accurate machines. In early 2010, it pushed the cost of human genome sequencing down to $10,000.8 Service company Knome currently offers full genome sequencing via Illumina equipment, plus interpretation of results, for $4,998.9 Roche recently attempted to acquire Illumina.10

Third generation machines, often utilizing nanotechnology as well as parallel sequencing and faster data processing chips, should cut the cost of sequencing a human genome to well below $1,000, Davies notes.11 Pacific Biosciences of California claimed a potential 30,000-fold speed increase via sequencing in real time as DNA is replicated. Another company, Oxford Nanopore, was working on sequencing via measurement of electric current passing through bases.12 Ion Torrent Systems measures the pH of bases streaming through pores.13

Davies calculated that the cost of DNA sequencing fell 50% a year through 2005, and then by an amazing 90% a year due to a series of disruptive technologies.14 He does not predict when a hand-held "Star Trek Medical Tricorder," capable of reading the DNA of a patient and his disease and then prescribing personalized medicine, will be available, but the world seems headed in that direction.

Personal Genomic Services

It doesn't take a full genome sequence to determine genetic characteristics such as ancestry and possible risks of disease. In November 2007, deCODEme and 23andMe launched competing $1,000 services. Processing cheek swab or saliva DNA on equipment utilizing specialized chips, they sampled up to 600,000 bases, 0.02% of the total, and looked for differences in bases between people, called single nucleotide polymorphisms (SNPs).15 By correlating SNPs with known ancestry and disease databases, the companies provided statistical probabilities to clients based on their DNA samples.

Since 2007, deCODEme has had financial problems; it currently offers the service for $1,100, including updates.16 23andMe currently charges $207 for an initial sampling and a one-year subscription for updates. According to its website, 23andMe provides probabilities for 118 diseases, shows likely responses to 20 drugs, and determines whether clients' children could be at risk for any of 44 inherited diseases.17 Navigenics has also entered the market and provides genetic counseling as well as data.

The personal genomic services companies update disease probabilities as additional data is analyzed. Probabilities can and do change, sometimes drastically, as new correlations and additional SNPs are incorporated into a person's profile. It's somewhat disconcerting that, according to Davies, Navigenics and 23andMe disagree qualitatively on one-third of diseases.18

As more of the population gets increasingly more genes sequenced, more data becomes available and the relationships between genes, health and responses to drugs become better known. Full genome sequencing will likely show an average of three million SNPs per person,19 creating an enormous data management problem as well as new understandings of relationships between genes and diseases.

Limits to Predicting Diseases

Recent research published in Science Translational Medicine titled, "The Predictive Capacity of Personal Genome Sequencing,"20 ingeniously addressed the theoretical potential for genes to predict common diseases. The underlying question was, of course, what are the odds of someone with a specific genome getting

3

Wanger International 2012 Semiannual Report

a specific disease? According to the study, the answer can be determined by studying pairs of people with nearly identical genomes: identical twins. By comparing histories of 24 common diseases among identical twins versus fraternal twins, genetic determination of diseases were inferred.

The study concluded that for 19 of the 24 diseases a negative test score (below average risk) will hardly be reassuring because the odds of getting the disease will still be substantial, at 50% to 80% of the general population's odds. Over half of the ultimate victims of 12 diseases would have tested at below average risk, receiving a false sense of security. However, there was one disease category tested in the study, Alzheimer's disease, in which a negative test result might indicate as little as a 12% relative risk of disease compared to the general population.

Those testing positive for Alzheimer's, type 1 diabetes, male coronary heart disease and thyroid autoimmunity could account for over 75% of the patients developing the diseases. The study suggested that the utility of genetic tests will depend on the results of the individual tested, and cautions against complacency and unwise lifestyle choices for those testing negative.

I agree that some subscribers to personal genetics services could obtain valuable results. If, for example, someone learned that his probability of developing glaucoma was much higher than the 4% probability for the average person, the subscriber would more likely get regular glaucoma testing. This is of some value, assuming the stated odds are indeed properly calibrated, which may take years to confirm.

Inherited Diseases

Some inherited diseases, including cystic fibrosis, Tay-Sachs disease and sickle cell anemia, occur only when single defective genes are inherited from each parent. Other single gene diseases, such as Huntington's, are inherited with 50% odds of getting the gene and disease if just one parent is afflicted.

Dozens of rare genetic diseases affect newborns, many of which can be addressed by diet or vitamins.21 Quick diagnosis is often crucial as permanent damage can occur otherwise. As of March 2010, newborns were tested for 29 genetic diseases in most states.22

Sometimes only a tendency to contract a disease is inherited. One version of a specific gene mutation implies a 65% to 85% lifetime probability of a woman developing breast cancer, while another version implies a 45% to 85% probability.23 However, only 5% to 10% of breast cancer patients have those genes.24 Others get the disease with no apparent genetic correlation. Having those genes is a cause for concern, but not having them should not provide a lot of comfort.

Personalized Medicine

In 2003, Allen Roses, vice-president of genetics for GlaxoSmithKline, shocked consumers by stating that more than 90% of drugs work in just 30% to 50% of people.25 Roses was pushing the drug industry to pursue genetic testing rather than trial and error to determine which drugs work for a specific individual. Matt Ridley, in the 2006 version of his book, Genome, stated, "genetic diagnosis followed by conventional cure is probably the genome's greatest boon to medicine."26

Indeed, the lung cancer drug Iressa was approved in 2003 and creates a "miraculous response" in the 10% of patients with a specific genetic mutation of the disease. Herceptin was approved in 2006 to target the 25% of breast cancer patients who are afflicted with a specific genetic version of that disease. Likewise, targeted cancer drugs such as Avastin, Tarceva and Erbitux, are prescribed after genetic testing.27

On January 31, 2012, Kalydeco was approved to treat 1,200 cystic fibrosis patients, 4% of the total, who have a specific gene defect. It is the first drug to treat the defect rather than the symptoms of the disease, and has been termed "transformational" for those who can use it.28 The Cystic Fibrosis Foundation spurred development of the drug by helping to fund the development effort, and aided the process by creating a registry that includes the genetic characteristics of the disease for 90% of American patients.

Some drugs appear to work for most people, but have widely varying optimal dosages. Variations in genes largely determine how quickly people metabolize drugs.29 "Unanticipated drug responses are estimated to result in two million hospitalizations and 100,000 deaths in the United States each year," writes Nicholas Gillham in his book, Genes, Chromosomes, and Disease.30

In the case of blood thinner warfarin (brand name Coumadin), patients exhibit a tenfold range in ability to metabolize the drug.31 Too little of it can result in a stroke, but too much can cause bleeding and hemorrhaging.32 The FDA now provides dosage information on the drug's label based on variants of two genes.33 About 10% of labels for FDA-approved drugs now have pharmacogenomics information.34

Investment Implications

Genetic science is rapidly advancing and will likely revolutionize many aspects of medical care. It is starting to be helpful in predicting susceptibility to common diseases, but will likely be more valuable in identifying risks of inherited diseases and in determining appropriate drug usage and dosage. Given the complexity of the subject, there will likely be increasing demands for genetic counselors.

There exists uncertainty regarding how the FDA and others will regulate genetic tests, as well as the extent to which genetic discoveries will be patentable. On the investment front, we have looked for and invested in opportunities created by genetic science. We've focused on a number of biotechnology and drug companies addressing personalized medicine and niche orphan

4

Wanger International 2012 Semiannual Report

diseases and we will continue to look for additional opportunities.

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, LLC

The information and data provided in this analysis are derived from sources that we deem to be reliable and accurate. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. The views/opinions expressed in this essay are those of the author and not of the Wanger Advisors Trust Board, are subject to change at any time based upon economic, market or other conditions, may differ from views expressed by other Columbia Management associates and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund.

1 Gillham, Nicholas Wright, Genes, Chromosomes, and Disease, (Upper Saddle River, New Jersey, FT Press Science 2011) p. 5.

2 Davies, Kevin, The $1,000 Genome, (New York, New York, Free Press 2010) p. 1, 23.

3 Ibid., p. 9-11.

4 Ibid., p. 79.

5 Ibid., p. 90.

6 Ibid., p. 94.

7 Ibid., p. 111.

8 Gillham, Nicholas Wright, op. cit., p. 244.

9 Davies, Kevin, op. cit., p. 209. www.knome.com.

10 Falconi, Marta, "Roche To Return Tendered Illumina Shares to Shareholders," Dow Jones News Service, April 23, 2012.

11 Davies, Kevin, op. cit., p. 231.

12 Davies, Kevin, op. cit., p. 239.

13 Ibid., p. 245-246.

14 Ibid., p. 133. Disruptive technologies refers to making much more than incremental advances by utilizing a whole new or additional approach. In this context, the parallel sequencing and use of other detection mechanisms such as pH or electric conductivity have caused the cost of sequencing to plunge far faster than a regular learning curve might suggest.

15 Ibid., p. 31-32.

16 Ibid., p. 55,63. www.decodeme.com.

17 www.23andme.com.

18 Davies, Kevin, op. cit., p. 149.

19 Ibid., p. 23.

20 Roberts, Nicholas J., and Vogelstein, Joshua T., et al, "The Predictive Capacity of Personal Genome Sequencing," Science Translational Medicine, Rapid Publication, April 2, 2012, stm.sciencemag.org.

21 Gillham, Nicholas Wright, op. cit., p. 204.

22 Ibid., p. 201.

23 Ibid., p. 184.

24 Ibid., p. 116.

25 Connor, Steve, "Glaxo Chief: Our Drugs Do Not Work On Most Patients," The Independent, December 8, 2003.

26 Ridley, Matt, Genome, (New York, New York, First Harper Perennial, 2006) p. 257.

27 Davies, Kevin, op. cit., p. 255-256.

28 Usdin, Steve, "Product Discovery & Development: Kalydescopic Vision," BioCentury, March 5, 2012, Volume 20, Number 10, p. A2.

29 Davies, Kevin, op. cit., p. 257.

30 Gillham, Nicholas Wright, op. cit., p. 237.

31 Davies, Kevin, op. cit., p. 257.

32 Gillham, Nicholas Wright, op. cit., p. 238.

33 Davies, Kevin, op. cit., p. 257.

34 Hamburg, M.D., Margaret A., and Collins, M.D., Ph.D., Francis S., "The Path to Personalized Medicine," New England Journal of Medicine, July 22, 2010, Volume 363, p. 301-304, www.nejm.org.

5

Wanger International 2012 Semiannual Report

Performance Review Wanger International

|  | ||||||

| Louis J. Mendes III Co-Portfolio Manager | Christopher J. Olson Co-Portfolio Manager | ||||||

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for most recent month-end performance updates.

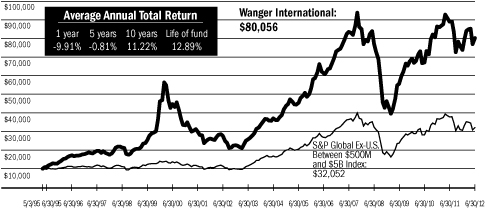

Wanger International returned 8.64% for the six months ended June 30, 2012, 3.82% better than its primary benchmark, the S&P Global Ex-U.S. between $500M and $5B Index.

A reversal of fortune occurred in the markets at the end of the first quarter of 2012 and continued throughout the second quarter. This shift was brought on by high anxiety regarding the financial stability of peripheral eurozone states, and the worsening outlook for Chinese growth. Markets do not like uncertainty, and the lack of a resolution to European budget crises continues to rattle the confidence of long-term investors in the region. As confidence falls, sovereign borrowing costs rise, which further deteriorates the long-term financial outlook. Aside from this unhelpful, self-reinforcing mechanism, signs of a slowing Chinese economy further fuel market volatility. Despite the ebb and flow of sentiment, however, many of the Fund's holdings have continued to post a pleasing growth in earnings.

Most notable about the Fund's results during the six-month period is the relatively strong performance of classic "Wanger-style" companies. By this we refer to companies that are taking advantage of structural changes within the market for their products or services—whether related to regulation, technology, energy efficiency, social change or otherwise. These can be contrasted with companies that primarily depend on macroeconomic factors to drive earnings. Top performers in the period included Nagacorp (+85%), a Cambodian-based casino operator catering to the growing needs of Indochina's emerging middle class for quality entertainment facilities. Two French companies, Eurofins Scientific (+71%) and Gemalto (+47%) performed well despite eurozone concerns. Eurofins Scientific provides laboratory analysis of food, pharmaceuticals and cosmetics products globally and, after a long period of consolidation, looms as a one-stop solution for multinational companies and others increasingly concerned with the safety and purity of traded goods. Gemalto is a leader in developing smart-chip technology for use in credit cards and mobile handsets. These mobile devices are finding increasingly valuable applications in secure payment systems.

Where macroeconomic worries did hurt the Fund was in commodity-related holdings. Fears of slower global growth drove down a number of energy and basic material stocks. Indonesian gold miner Archipelago Resources (-26%), Mongolian coal miner Mongolian Mining (-24%) and South African platinum miner Northam Platinum (-23%) all fell on weakened outlook for demand. Similarly, oil exploration-related companies Celtic Exploration (-41%) and FMC Technologies (-25%) declined on expectations that oil prices would soften.

We expect continued volatility in the second half of the year. The euro debt crisis does not lend itself to a tidy resolution in the short- or even mid-term. The most likely outcome in our view is piecemeal structural reform within uncompetitive states, incented by explicit and tacit German support and the fact that the alternatives entail a lower standard of living for these states on a long-term basis. We believe that this will be a political process fraught with complexity, and made more complicated by the way Europe is organized. This fall, the presidential election in the United States and the transition of leadership in China will also likely become a focus for continued sentiment shifts in the marketplace. As always, we will strive to work through the noise to identify companies where reasonable valuations are supported by good or improving fundamentals.

International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

Fund's Positions in Mentioned Holdings

As a percentage of net assets, as of 6/30/12

| Eurofins Scientific | 1.1 | % | |||||

| Archipelago Resources | 0.9 | ||||||

| Gemalto | 0.9 | ||||||

| Mongolian Mining | 0.6 | ||||||

| Nagacorp | 0.5 | ||||||

| Northam Platinum | 0.4 | ||||||

| FMC Technologies | 0.3 | ||||||

| Celtic Exploration | 0.1 | ||||||

6

Wanger International 2012 Semiannual Report

Growth of a $10,000 Investment in Wanger International

May 3, 1995 (inception date) through June 30, 2012

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment manager and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. For daily and most recent month-end performance updates, please call 1-888-4-WANGER.

This graph compares the results of $10,000 invested in Wanger International on May 3, 1995 (the date the Fund began operations) through June 30, 2012, to the S&P Global Ex-U.S. Between $500M and $5B Index with dividends and capital gains reinvested. Although the index is provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the index.

Top 10 Holdings

As a percentage of net assets, as of 6/30/12

| 1. Far EasTone Telecom (Taiwan) Taiwan's Third Largest Mobile Operator | 1.3 | % | |||||

| 2. Melco Crown Entertainment (Hong Kong) Macau Casino Operator | 1.3 | ||||||

| 3. Hexagon (Sweden) Design, Measurement & Visualization Software & Equipment | 1.2 | ||||||

| 4. Eurofins Scientific (France) Food, Pharmaceuticals & Materials Screening & Testing | 1.1 | ||||||

| 5. Naspers (South Africa) Media in Africa, China, Russia & Other Emerging Markets | 1.0 | ||||||

| 6. Kansai Paint (Japan) Paint Producer in Japan, India, China & Southeast Asia | 1.0 | ||||||

| 7. Partners Group (Switzerland) Private Markets Asset Management | 0.9 | ||||||

| 8. Localiza Rent A Car (Brazil) Car Rental | 0.9 | ||||||

| 9. Taiwan Mobile (Taiwan) Taiwan's Second-largest Mobile Operator | 0.9 | ||||||

| 10. Archipelago Resources (Indonesia) Gold Mining Projects in Indonesia, Vietnam & the Philippines | 0.9 | ||||||

Top 5 Countries

As a percentage of net assets, as of 6/30/12

| Japan | 17.7 | % | |||||

| Taiwan | 7.2 | ||||||

| United Kingdom | 6.8 | ||||||

| South Africa | 4.5 | ||||||

| Netherlands | 4.4 | ||||||

Results as of June 30, 2012

| 2nd quarter | Year to date | 1 year | 5 years | 10 years | |||||||||||||||||||

| Wanger International | -5.68 | % | 8.64 | % | -9.91 | % | -0.81 | % | 11.22 | % | |||||||||||||

| S&P Global Ex-U.S. Between $500M and $5B Index* | -8.03 | 4.82 | -15.17 | -2.48 | 10.95 | ||||||||||||||||||

| MSCI EAFE Index | -7.13 | 2.96 | -13.83 | -6.10 | 5.14 | ||||||||||||||||||

| Lipper Variable Underlying International Growth Funds Index | -6.65 | 5.33 | -11.89 | -4.52 | 5.26 | ||||||||||||||||||

* The Fund's primary benchmark.

NAV as of 6/30/12: $28.17

Performance numbers reflect all Fund expenses but do not include any fees and expenses imposed under your variable annuity or life insurance policy or qualified pension or retirement plan. If performance included the effect of these additional charges, it would be lower.

The Fund's annual operating expense ratio of 1.02% is stated as of the Fund's prospectus dated May 1, 2012, and differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and expense reimbursements as well as different time periods used in calculating the ratios.

All results shown assume reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

The S&P Global Ex-U.S. Between $500M and $5B Index is a subset of the broad market selected by the index sponsor representing the mid- and small-cap developed and emerging markets, excluding the United States. The MSCI Europe, Australasia, Far East (EAFE) Index (Net) is a capitalization-weighted index that tracks the total return of common stocks in 22 developed-market countries within Europe, Australasia and the Far East. The returns of the MSCI EAFE Index (Net) are presented net of the withholding tax rate applicable to foreign non-resident institutional investors in the foreign companies included in the index who do not benefit from double taxation treaties. The performance of the MSCI EAFE Index (Net) is provided to show how the Fund's performance compares to a widely recognized broad-based index of foreign market performance. The Lipper Variable Underlying International Growth Funds Index is an equally weighted representation of the 30 largest variable insurance underlying funds in the Lipper Variable Underlying International Growth Funds Classification, and shows how the Fund's performance compares with returns of an index of funds with similar investment objectives. Indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the Fund. Lipper makes no adjustment for the effect of sales loads.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings.

7

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| Equities – 97.7% | |||||||||||

| Asia – 44.9% | |||||||||||

| Japan – 17.7% | |||||||||||

| 632,589 | Kansai Paint Paint Producer in Japan, India, China & Southeast Asia | $ | 6,778,710 | ||||||||

| 2,292,100 | Seven Bank ATM Processing Services | 5,886,081 | |||||||||

| 2,275 | Wacom Computer Graphic Illustration Devices | 5,095,286 | |||||||||

| 343,300 | Park24 Parking Lot Operator | 5,069,929 | |||||||||

| 180,000 | Hoshizaki Electric Commercial Kitchen Equipment | 4,555,943 | |||||||||

| 339,100 | Kuraray Special Resin, Fine Chemical, Fibers & Textures | 4,394,556 | |||||||||

| 291,631 | Start Today (a) Online Japanese Apparel Retailer | 4,075,395 | |||||||||

| 195,118 | Glory Currency Handling Systems & Related Equipment | 4,070,469 | |||||||||

| 896 | Orix JREIT Diversified REIT | 4,027,534 | |||||||||

| 160,342 | Aeon Delight Facility Maintenance & Management | 3,681,649 | |||||||||

| 98,000 | Sanrio (a) Character Goods & Licensing | 3,572,907 | |||||||||

| 33,599 | Nakanishi Dental Tools & Machinery | 3,414,985 | |||||||||

| 106,641 | Kintetsu World Express Airfreight Logistics | 3,413,179 | |||||||||

| 1,713 | Advance Residence Investment Residential REIT | 3,330,045 | |||||||||

| 78,100 | Miraca Holdings Outsourced Lab Testing, Diagnostic Equipment & Reagents | 3,242,586 | |||||||||

| 185,847 | Daiseki Waste Disposal & Recycling | 3,231,240 | |||||||||

| 289,200 | NGK Insulators Ceramic Products for Auto, Power & Electronics | 3,202,467 | |||||||||

| 54,400 | Disco Semiconductor Dicing & Grinding Equipment | 3,080,829 | |||||||||

| 2,992 | Jupiter Telecommunications Largest Cable Service Provider in Japan | 3,050,579 | |||||||||

| 243,109 | Japan Airport Terminal Airport Terminal Operator at Haneda | 2,965,191 | |||||||||

| Number of Shares | Value | ||||||||||

| 600 | Mori Hills REIT Investment Tokyo-centric Diversified REIT | $ | 2,592,953 | ||||||||

| 299,000 | Shimadzu Analytical Instrument, Medical & Industrial Equipment | 2,587,246 | |||||||||

| 91,300 | Doshisha Wholesaler | 2,529,208 | |||||||||

| 213,700 | Asahi Diamond Industrial Consumable Diamond Tools | 2,453,878 | |||||||||

| 38,400 | FP Corporation Disposable Food Trays & Containers | 2,381,944 | |||||||||

| 39,111 | Ain Pharmaciez Dispensing Pharmacy/Drugstore Operator | 2,359,305 | |||||||||

| 226,900 | Sintokogio Automated Casting Machines, Surface Treatment System & Consumables | 2,274,676 | |||||||||

| 680 | Kenedix Realty Investment Tokyo Mid-size Office REIT | 2,198,583 | |||||||||

| 99,825 | Aeon Mall Suburban Shopping Mall Developer, Owner & Operator | 2,127,118 | |||||||||

| 85,646 | Icom Two Way Radio Communication Equipment | 2,102,942 | |||||||||

| 88,900 | Misumi Group Industrial Components Distributor | 2,094,956 | |||||||||

| 1,720,700 | Shinsei Bank Commercial Bank | 2,093,406 | |||||||||

| 161,860 | Ushio Industrial Light Sources | 2,006,186 | |||||||||

| 98,703 | Ibiden Electronic Parts & Ceramics | 1,787,934 | |||||||||

| 48,100 | Horiba Measuring Instruments & Analyzers | 1,689,264 | |||||||||

| 227 | Fukuoka REIT Diversified REIT in Fukuoka | 1,563,029 | |||||||||

| 152,566 | Torishima Pump Manufacturing Industrial Pump for Power Generation & Water Supply Systems | 1,533,770 | |||||||||

| 95,200 | Nihon Parkerizing Metal Surface Treatment Agents & Processing | 1,474,536 | |||||||||

| 160 | Japan Real Estate Investment Office REIT in Tokyo | 1,467,001 | |||||||||

| 49,958 | Miura Industrial Boiler | 1,330,186 | |||||||||

| 120,787,681 | |||||||||||

See accompanying notes to financial statements.

8

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| Taiwan – 7.2% | |||||||||||

| 4,148,000 | Far EasTone Telecom Taiwan's Third Largest Mobile Operator | $ | 9,024,641 | ||||||||

| 1,859,000 | Taiwan Mobile Taiwan's Second Largest Mobile Operator | 6,147,660 | |||||||||

| 2,314,000 | CTCI Corp International Engineering Firm | 4,332,508 | |||||||||

| 572,940 | Simplo Technology Battery Packs for Notebook & Tablet PCs | 3,956,943 | |||||||||

| 1,384,830 | Tripod Technologies Printed Circuit Boards (PCB) | 3,936,386 | |||||||||

| 670,000 | Radiant Opto-Electronics (b) LCD Back Light Units & Modules | 3,405,103 | |||||||||

| 287,000 | St. Shine Optical World's Leading Disposable Contact Lens OEM | 3,211,963 | |||||||||

| 1,274,000 | Taiwan Hon Chuan Beverage Packaging (Bottles, Caps, Labels) Manufacturer | 2,869,825 | |||||||||

| 415,000 | MStar Semiconductor Integrated Circuits for TV, Digital Set-top-box & Handset | 2,799,333 | |||||||||

| 1,210,000 | Chroma Ate Automatic Test Systems, Testing & Measurement Instruments | 2,762,200 | |||||||||

| 748,000 | Advantech Industrial PC & Components | 2,487,532 | |||||||||

| 366,000 | President Chain Store Taiwan's Number One Convenience Chain Store Operator | 1,952,827 | |||||||||

| 299,000 | PC Home Taiwanese Internet Retail Company | 1,695,067 | |||||||||

| 280,000 | Lung Yen Funeral Services & Columbaria | 809,505 | |||||||||

| 49,391,493 | |||||||||||

| Hong Kong – 3.9% | |||||||||||

| 740,000 | Melco Crown Entertainment - ADR (b) Macau Casino Operator | 8,524,800 | |||||||||

| 2,484,600 | Lifestyle International Mid to High-end Department Store Operator in Hong Kong & China | 5,474,844 | |||||||||

| 1,777,500 | L'Occitane International Skin Care & Cosmetics Producer | 4,933,088 | |||||||||

| 976,000 | AAC Technologies Miniature Acoustic Components | 2,840,312 | |||||||||

| 3,400,000 | Sasa International Cosmetics Retailer | 2,154,147 | |||||||||

| Number of Shares | Value | ||||||||||

| 1,133,000 | MGM China Holdings Macau Casino Operator | $ | 1,737,291 | ||||||||

| 1,000,000 | Melco International Macau Casino Operator | 809,006 | |||||||||

| 467,200 | Vitasoy International Hong Kong Soy Food Brand | 392,617 | |||||||||

| 26,866,105 | |||||||||||

| Singapore – 3.8% | |||||||||||

| 2,833,000 | Olam International Agriculture Supply Chain Manager | 4,103,164 | |||||||||

| 2,275,000 | Ascendas REIT Industrial Property Landlord | 3,881,034 | |||||||||

| 2,303,000 | CDL Hospitality Trust Hotel Owner/Operator | 3,562,079 | |||||||||

| 4,030,000 | Mapletree Logistics Trust Industrial Property Landlord | 3,133,477 | |||||||||

| 3,981,000 | Mapletree Commercial Trust Retail & Office Property Landlord | 3,091,060 | |||||||||

| 3,173,000 | Mapletree Industrial Trust Industrial Property Landlord | 3,039,542 | |||||||||

| 1,728,000 | Goodpack Limited International Bulk Container Leasing | 2,366,909 | |||||||||

| 409,000 | Singapore Exchange Singapore Equity & Derivatives Market Operator | 2,054,753 | |||||||||

| 360,400 | Petra Foods Cocoa Processor & Chocolate Manufacturer | 711,269 | |||||||||

| 25,943,287 | |||||||||||

| China – 3.2% | |||||||||||

| 3,060,000 | Want Want Chinese Branded Consumer Food Company | 3,784,119 | |||||||||

| 2,040,000 | Digital China IT Distribution & Systems Integration Services | 3,594,952 | |||||||||

| 126,700 | New Oriental Education & Technology - ADR (b) Education Service Provider | 3,104,150 | |||||||||

| 2,213,000 | Zhaojin Mining Industry Gold Mining & Refining in China | 2,909,805 | |||||||||

| 44,300 | NetEase.com - ADR (b) Chinese Online Gaming Services | 2,607,055 | |||||||||

| 30,000,000 | RexLot Holdings Lottery Equipment Supplier in China | 2,149,024 | |||||||||

See accompanying notes to financial statements.

9

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| China – 3.2% (cont) | |||||||||||

| 38,300 | 51job - ADR (b) Integrated Human Resource Services | $ | 1,744,565 | ||||||||

| 3,600,000 | AMVIG Holdings Chinese Tobacco Packaging Material Supplier | 1,594,138 | |||||||||

| 21,487,808 | |||||||||||

| India – 2.5% | |||||||||||

| 38,900 | Asian Paints India's Largest Paint Company | 2,715,494 | |||||||||

| 256,300 | United Breweries India's Largest Brewer | 2,506,725 | |||||||||

| 1,520,000 | Redington India Supply Chain Solutions for IT & Mobile Handsets in Emerging Markets | 2,099,104 | |||||||||

| 941,500 | Adani Ports & Special Economic Zone Indian West Coast Shipping Port | 2,055,718 | |||||||||

| 1,328,300 | Jain Irrigation Systems | 1,993,114 | |||||||||

| 59,405 | Jain Irrigation Systems - DVR (b) Agricultural Micro-irrigation Systems & Food Processing | 42,049 | |||||||||

| 175,600 | Shriram Transport Finance Used Truck Finance | 1,675,073 | |||||||||

| 62,000 | Colgate-Palmolive India Consumer Products in Oral Care | 1,338,048 | |||||||||

| 1,250,800 | S. Kumars Nationwide Textiles, Clothing & Retail | 776,345 | |||||||||

| 4,020,100 | REI Agro Basmati Rice Processing | 673,197 | |||||||||

| 165,000 | Titan Industries Jewlery, Watches & Eyeglasses | 664,397 | |||||||||

| 199,131 | SKIL Ports and Logistics (b) Indian Container Port Project | 352,412 | |||||||||

| 16,891,676 | |||||||||||

| Korea – 1.9% | |||||||||||

| 131,000 | Grand Korea Leisure Largest 'Foreigner Only' Casino Group in Korea | 2,719,468 | |||||||||

| 11,800 | NHN Korean Online Search Services | 2,588,142 | |||||||||

| 71,700 | Woongjin Coway Korean Household Appliance Rental Service Provider | 2,238,788 | |||||||||

| Number of Shares | Value | ||||||||||

| 55,400 | Handsome Korea's Leading High-end Apparel Company | $ | 1,247,488 | ||||||||

| 66,800 | iMarketKorea Procurement, Distribution of MRO (Maintenance, Repair, Operations) Goods | 1,238,245 | |||||||||

| 28,360 | Kepco Plant Service & Engineering Power Plant & Grid Maintenance | 1,196,203 | |||||||||

| 20,600 | Hana Tour Service Korea's Largest Wholesale Tour Provider | 808,816 | |||||||||

| 6,500 | Hyundai Home Shopping TV Home Shopping Company | 636,110 | |||||||||

| 12,673,260 | |||||||||||

| Indonesia – 1.8% | |||||||||||

| 7,592,066 | Archipelago Resources (b) Gold Mining Projects in Indonesia, Vietnam & the Philippines | 6,064,064 | |||||||||

| 6,123,900 | Tower Bersama Infrastructure (b) Communications Towers | 2,145,356 | |||||||||

| 1,471,000 | Mitra Adiperkasa Operator of Department Store & Specialty Retail Stores | 1,129,354 | |||||||||

| 1,800,000 | Ace Indonesia Home Improvement Retailer | 975,294 | |||||||||

| 4,681,000 | MNC Skyvision (b) Largest Satellite Pay TV Operator in Indonesia | 783,802 | |||||||||

| 256,000 | Mayora Indah Consumer Branded Food Manufacturer | 694,767 | |||||||||

| 847,500 | Southern Arc Minerals (b) Gold & Copper Exploration in Indonesia | 233,081 | |||||||||

| 12,025,718 | |||||||||||

| Mongolia – 0.9% | |||||||||||

| 6,913,000 | Mongolian Mining (b) Coking Coal Mining in Mongolia | 3,922,826 | |||||||||

| 118,952 | Ivanhoe Mines (a) (b) | 1,173,046 | |||||||||

| 108,951 | Ivanhoe Mines (a) (b) (c) Copper Mine Project in Mongolia | 1,054,646 | |||||||||

| 6,150,518 | |||||||||||

See accompanying notes to financial statements.

10

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| Philippines – 0.8% | |||||||||||

| 8,297,525 | SM Prime Holdings Shopping Mall Operator | $ | 2,571,911 | ||||||||

| 942,890 | Int'l Container Terminal Container Handling Terminals & Port Management | 1,655,119 | |||||||||

| 2,064,100 | Manila Water Company Water Utility Company in the Philippines | 1,202,168 | |||||||||

| 5,429,198 | |||||||||||

| Thailand – 0.7% | |||||||||||

| 12,465,500 | Home Product Center Home Improvement Retailer | 4,978,291 | |||||||||

| Cambodia – 0.5% | |||||||||||

| 7,000,000 | Nagacorp Casino/Entertainment Complex in Cambodia | 3,130,246 | |||||||||

| Total Asia | 305,755,281 | ||||||||||

| Europe – 31.3% | |||||||||||

| United Kingdom – 6.8% | |||||||||||

| 2,250,000 | Charles Taylor (d) Insurance Services | 5,620,525 | |||||||||

| 115,500 | Intertek Group Testing, Inspection, Certification Services | 4,838,974 | |||||||||

| 1,021,000 | BBA Aviation Aviation Support Services | 3,268,641 | |||||||||

| 388,449 | Serco Facilities Management | 3,262,210 | |||||||||

| 296,872 | JLT Group International Business Insurance Broker | 3,261,906 | |||||||||

| 352,000 | Domino's Pizza UK & Ireland Pizza Delivery in the UK, Ireland & Germany | 2,838,295 | |||||||||

| 90,000 | Rightmove Internet Real Estate Listings | 2,248,892 | |||||||||

| 67,600 | Aggreko Temporary Power & Temperature Control Services | 2,198,399 | |||||||||

| 327,000 | Abcam Online Sales of Antibodies | 2,135,334 | |||||||||

| 264,837 | Greggs Bakery | 2,092,143 | |||||||||

| 199,590 | Smith and Nephew Medical Equipment & Supplies | 1,996,392 | |||||||||

| 58,588 | Rotork Valve Actuators for Oil & Water Pipelines | 1,812,033 | |||||||||

| Number of Shares | Value | ||||||||||

| 200,900 | Shaftesbury London Prime Retail REIT | $ | 1,621,847 | ||||||||

| 31,200 | Next Clothes & Home Retailer in the UK | 1,566,620 | |||||||||

| 180,000 | WH Smith British Retailer | 1,536,760 | |||||||||

| 229,742 | Premier Oil (b) Oil & Gas Producer in Europe, Pakistan & Asia | 1,220,625 | |||||||||

| 267,000 | Chemring Defense Manufacturer of Countermeasures & Energetics | 1,149,540 | |||||||||

| 494,998 | PureCircle (a) (b) Natural Sweeteners | 1,112,711 | |||||||||

| 45,604 | Tullow Oil Oil & Gas Producer | 1,054,026 | |||||||||

| 29,141 | Spirax Sarco Steam Systems for Manufacturing & Process Industries | 908,186 | |||||||||

| 331,900 | Sterling Resources (b) Oil & Gas Exploration - Europe | 332,519 | |||||||||

| 46,076,578 | |||||||||||

| Netherlands – 4.4% | |||||||||||

| 183,314 | UNIT4 Business Software Development | 4,672,049 | |||||||||

| 293,428 | Aalberts Industries Flow Control & Heat Treatment | 4,568,917 | |||||||||

| 190,423 | Imtech Electromechanical & Information & Communications Technology Installation & Maintenance | 4,546,961 | |||||||||

| 142,136 | Koninklijke TenCate Advanced Textiles & Industrial Fabrics | 3,794,338 | |||||||||

| 52,129 | Fugro Subsea Oilfield Services | 3,162,087 | |||||||||

| 144,166 | Arcadis Engineering Consultants | 3,153,041 | |||||||||

| 37,116 | Vopak World's Largest Operator of Petroleum & Chemical Storage Terminals | 2,380,683 | |||||||||

| 101,682 | TKH Group Dutch Industrial Conglomerate | 2,184,226 | |||||||||

| 16,249 | Core Laboratories Oil & Gas Reservoir Consulting | 1,883,259 | |||||||||

| 30,345,561 | |||||||||||

See accompanying notes to financial statements.

11

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| Switzerland – 3.8% | |||||||||||

| 35,650 | Partners Group Private Markets Asset Management | $ | 6,340,441 | ||||||||

| 28,886 | Geberit Plumbing Supplies | 5,698,574 | |||||||||

| 37,396 | Dufry Group (b) Operates Airport Duty Free & Duty Paid Shops | 4,532,720 | |||||||||

| 1,758 | Sika Chemicals for Construction & Industrial Applications | 3,394,734 | |||||||||

| 19,216 | Kuehne & Nagel Freight Forwarding/Logistics | 2,035,804 | |||||||||

| 32,747 | Zehnder Radiators & Ventilation Systems | 1,957,401 | |||||||||

| 67,830 | Bank Sarasin & Cie (b) Private Banking | 1,911,125 | |||||||||

| 25,870,799 | |||||||||||

| France – 3.6% | |||||||||||

| 62,700 | Eurofins Scientific Food, Pharmaceuticals & Materials Screening & Testing | 7,786,223 | |||||||||

| 84,000 | Gemalto Digital Security Solutions | 6,033,164 | |||||||||

| 77,724 | Neopost Postage Meter Machines | 4,147,878 | |||||||||

| 113,700 | Saft Niche Battery Manufacturer | 2,727,890 | |||||||||

| 27,200 | Norbert Dentressangle Leading European Logistics & Transport Group | 1,725,682 | |||||||||

| 15,550 | Compagnie Française de l'Afrique Occidentale African Wholesaler & Distributor | 736,097 | |||||||||

| 220,933 | Hi-Media (b) Online Advertiser in Europe | 563,140 | |||||||||

| 20,321 | Mersen Advanced Industrial Materials | 509,155 | |||||||||

| 24,229,229 | |||||||||||

| Germany – 3.3% | |||||||||||

| 287,894 | Wirecard Online Payment Processing & Risk Management | 5,582,380 | |||||||||

| 17,109 | Rational Commercial Ovens | 4,078,062 | |||||||||

| Number of Shares | Value | ||||||||||

| 56,872 | Dürr Automotive Plant Engineering & Associated Capital Equipment | $ | 3,509,109 | ||||||||

| 47,100 | Rheinmetall Defense & Automotive | 2,315,301 | |||||||||

| 70,772 | CTS Eventim Event Ticket Sales | 2,129,666 | |||||||||

| 79,400 | NORMA Group Clamps for Automotive & Industrial Applications | 1,744,636 | |||||||||

| 19,339 | Bertrandt Outsourced Engineering | 1,448,656 | |||||||||

| 39,500 | Elringklinger Automobile Components | 942,542 | |||||||||

| 39,590 | Deutsche Beteiligungs Private Equity Investment Management | 781,707 | |||||||||

| 22,532,059 | |||||||||||

| Sweden – 2.2% | |||||||||||

| 459,649 | Hexagon Design, Measurement & Visualization Software & Equipment | 7,889,836 | |||||||||

| 477,910 | Sweco Engineering Consultants | 5,036,099 | |||||||||

| 75,800 | Unibet European Online Gaming Operator | 1,921,763 | |||||||||

| 51,601 | East Capital Explorer Sweden-based Russia & Central Eastern Europe Investment Fund | 355,439 | |||||||||

| 15,203,137 | |||||||||||

| Denmark – 1.4% | |||||||||||

| 189,879 | Novozymes Industrial Enzymes | 4,923,828 | |||||||||

| 19,041 | SimCorp Software for Investment Managers | 3,282,524 | |||||||||

| 20,718 | Solar Technical Wholesaler of Electrical, Plumbing & HVAC Equipment | 1,123,391 | |||||||||

| 9,329,743 | |||||||||||

| Italy – 1.2% | |||||||||||

| 301,517 | Pirelli (a) Global Tire Supplier | 3,180,048 | |||||||||

See accompanying notes to financial statements.

12

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| Italy – 1.2% (cont) | |||||||||||

| 18,800 | Tod's (a) Leather Shoes & Bags | $ | 1,885,792 | ||||||||

| 850,000 | Geox (a) Apparel & Shoe Maker | 1,880,500 | |||||||||

| 1,118,273 | CIR (a) Italian Holding Company | 1,102,887 | |||||||||

| 8,049,227 | |||||||||||

| Russia – 0.8% | |||||||||||

| 118,500 | Yandex (b) Search Engine for Russian & Turkish Languages | 2,257,425 | |||||||||

| 246,800 | Petropavlovsk Gold & Iron Ore Mining in Russia | 1,768,128 | |||||||||

| 43,100 | Mail.ru - GDR (b) (e) Internet Social Networking & Games for Russian Speakers | 1,467,813 | |||||||||

| 5,493,366 | |||||||||||

| Iceland – 0.7% | |||||||||||

| 4,344,101 | Marel Largest Manufacturer of Poultry & Fish Processing Equipment | 4,579,364 | |||||||||

| Ireland – 0.5% | |||||||||||

| 29,800 | Paddy Power Irish Betting Services | 1,945,354 | |||||||||

| 488,000 | United Drug Irish Pharmaceutical Wholesaler & Outsourcer | 1,280,497 | |||||||||

| 3,225,851 | |||||||||||

| Spain – 0.4% | |||||||||||

| 70,063 | Red Eléctrica de España Spanish Power Transmission | 3,057,934 | |||||||||

| Portugal – 0.4% | |||||||||||

| 1,009,900 | Redes Energéticas Nacionais Portuguese Power Transmission & Gas Transportation | 2,673,318 | |||||||||

| Czech Republic – 0.4% | |||||||||||

| 15,049 | Komercni Banka Leading Czech Universal Bank | 2,625,317 | |||||||||

| Number of Shares | Value | ||||||||||

| Finland – 0.4% | |||||||||||

| 121,541 | Stockmann (a) Department Store & Fashion Retailer in Scandinavia & Russia | $ | 2,457,274 | ||||||||

| Belgium – 0.3% | |||||||||||

| 51,323 | EVS Broadcast Equipment Digital Live Mobile Production Software & Systems | 2,421,183 | |||||||||

| Norway – 0.3% | |||||||||||

| 272,396 | Atea Leading Nordic IT Hardware/Software Reseller & Installation Company | 2,398,545 | |||||||||

| Kazakhstan – 0.3% | |||||||||||

| 388,200 | Halyk Savings Bank of Kazakhstan - GDR (b) Largest Retail Bank & Insurer in Kazakhstan | 1,936,227 | |||||||||

| Greece – 0.1% | |||||||||||

| 529,085 | Intralot Lottery & Gaming Systems & Services | 597,281 | |||||||||

| Total Europe | 213,101,993 | ||||||||||

| Other Countries – 16.8% | |||||||||||

| South Africa – 4.5% | |||||||||||

| 132,600 | Naspers Media in Africa, China, Russia & Other Emerging Markets | 7,082,487 | |||||||||

| 359,785 | Mr. Price South African Retailer of Apparel, Household & Sporting Goods | 4,932,695 | |||||||||

| 2,199,200 | Rand Merchant Insurance Directly Sold Property & Casualty Insurance; Holdings in Other Insurers | 4,683,921 | |||||||||

| 1,333,156 | Coronation Fund Managers South African Fund Manager | 4,513,823 | |||||||||

| 567,800 | Adcock Ingram Holdings Manufacturer of Pharmaceuticals & Medical Supplies | 4,173,682 | |||||||||

| 999,500 | Northam Platinum Platinum Mining in South Africa | 2,858,858 | |||||||||

| 116,223 | Massmart Holdings General Merchandise, Food & Home Improvement Stores; Wal-Mart Subsidiary | 2,406,440 | |||||||||

| 30,651,906 | |||||||||||

See accompanying notes to financial statements.

13

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| Canada – 3.9% | |||||||||||

| 159,649 | CCL Industries Leading Global Label Manufacturer | $ | 5,856,881 | ||||||||

| 139,615 | ShawCor Oil & Gas Pipeline Products | 5,053,347 | |||||||||

| 74,000 | Onex Capital Private Equity | 2,873,215 | |||||||||

| 68,142 | AG Growth (a) Leading Manufacturer of Augers & Grain Handling Equipment | 2,455,682 | |||||||||

| 88,830 | Black Diamond Group Provides Accommodations/Equipment for Oil Sands Development | 1,990,190 | |||||||||

| 117,000 | Alliance Grain Traders Global Leader in Pulse Processing & Distribution | 1,569,806 | |||||||||

| 244,077 | Horizon North Logistics Provides Diversified Oil Service Offering in Northern Canada | 1,392,876 | |||||||||

| 30,351 | Baytex (a) Oil & Gas Producer in Canada | 1,278,612 | |||||||||

| 378,516 | DeeThree Exploration (b) (f) | 1,202,358 | |||||||||

| 86,526 | DeeThree Exploration (b) Canadian Oil & Gas Producer | 280,459 | |||||||||

| 57,000 | Celtic Exploration (b) Canadian Oil & Gas Producer | 770,936 | |||||||||

| 195,271 | Pan Orient (b) Asian Oil & Gas Explorer | 719,248 | |||||||||

| 53,000 | Athabasca Oil Sands (b) Oil Sands & Unconventional Oil Development | 583,047 | |||||||||

| 201,000 | Americas Petrogas (b) Oil & Gas Exploration in Argentina, Potash in Peru | 373,136 | |||||||||

| 42,800 | Crew Energy (b) Canadian Oil & Gas Producer | 241,725 | |||||||||

| 26,641,518 | |||||||||||

| Australia – 3.7% | |||||||||||

| 5,609,785 | Commonwealth Property Office Fund Australia Prime Office REIT | 5,847,620 | |||||||||

| 450,200 | UGL (a) Engineering & Facilities Management | 5,764,631 | |||||||||

| 1,379,700 | Challenger Financial Largest Annuity Provider | 4,633,953 | |||||||||

| Number of Shares | Value | ||||||||||

| 57,385 | Cochlear Cochlear Implants | $ | 3,897,182 | ||||||||

| 865,650 | IAG General Insurance Provider | 3,104,757 | |||||||||

| 181,300 | Domino's Pizza Enterprises Domino's Pizza Operator in Australia/New Zealand & France/Benelux | 1,874,094 | |||||||||

| 25,122,237 | |||||||||||

| United States – 3.5% | |||||||||||

| 139,366 | BioMarin Pharmaceutical (b) Biotech Focused on Orphan Diseases | 5,516,106 | |||||||||

| 120,500 | Atwood Oceanics (b) Offshore Drilling Contractor | 4,559,720 | |||||||||

| 111,165 | Textainer Group Holdings (a) Top International Container Leasor | 4,101,989 | |||||||||

| 88,370 | World Fuel Services Global Fuel Broker | 3,360,711 | |||||||||

| 62,949 | Hornbeck Offshore (b) Supply Vessel Operator in U.S. Gulf of Mexico | 2,441,162 | |||||||||

| 65,200 | Rowan (b) Contract Offshore Driller | 2,107,916 | |||||||||

| 46,146 | FMC Technologies (b) Oil & Gas Well Head Manufacturer | 1,810,308 | |||||||||

| 23,897,912 | |||||||||||

| Israel – 1.0% | |||||||||||

| 542,004 | Israel Chemicals Producer of Potash, Phosphates, Bromine & Specialty Chemicals | 5,996,923 | |||||||||

| 67,000 | Caesarstone (b) Quartz Countertops | 811,370 | |||||||||

| 6,808,293 | |||||||||||

| Senegal – 0.2% | |||||||||||

| 6,012 | Sonatel Leading Telecoms Operator in Western Africa | 1,322,241 | |||||||||

| Total Other Countries | 114,444,107 | ||||||||||

| Latin America – 4.7% | |||||||||||

| Brazil – 2.8% | |||||||||||

| 420,900 | Localiza Rent A Car Car Rental | 6,330,789 | |||||||||

See accompanying notes to financial statements.

14

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

| Number of Shares | Value | ||||||||||

| Brazil – 2.8% (cont.) | |||||||||||

| 136,000 | Multiplus Loyalty Program Operator in Brazil | $ | 3,243,415 | ||||||||

| 219,900 | Mills Estruturas e Servicos de Engenharia Civil Engineering & Construction | 2,956,087 | |||||||||

| 518,200 | Odontoprev Dental Insurance | 2,613,575 | |||||||||

| 150,000 | Arcos Dorados (a) McDonald's Master Franchise for Latin America | 2,217,000 | |||||||||

| 418,000 | MRV Engenharia Brazilan Property Developer | 1,925,068 | |||||||||

| 19,285,934 | |||||||||||

| Mexico – 0.8% | |||||||||||

| 67,990 | Grupo Aeroportuario del Sureste - ADR Mexican Airport Operator | 5,307,979 | |||||||||

| Guatemala – 0.3% | |||||||||||

| 164,360 | Tahoe Resources (b) Silver Project in Guatemala | 2,271,432 | |||||||||

| Uruguay – 0.4% | |||||||||||

| 230,870 | Union Agriculture Group (b) (f) (g) Farmland Operator in Uruguay | 2,260,217 | |||||||||

| Chile – 0.2% | |||||||||||

| 677,000 | Viña Concha y Toro Global Branded Wine Manufacturer | 1,324,933 | |||||||||

| Colombia – 0.1% | |||||||||||

| 932,244 | Canacol (b) Oil Producer in South America | 416,630 | |||||||||

| 3,074,000 | Gulf United (b) Prospecting for Oil Alongside Large Producers in Colombia | 184,440 | |||||||||

| 601,070 | |||||||||||

| Argentina – 0.1% | |||||||||||

| 604,000 | Madalena Ventures (b) (f) | 199,336 | |||||||||

| 302,000 | Madalena Ventures (b) Oil & Gas Exploration in Argentina | 103,821 | |||||||||

| 303,157 | |||||||||||

| Total Latin America | 31,354,722 | ||||||||||

| Total Equities (Cost: $513,770,478) – 97.7% | 664,656,103 | ||||||||||

| Number of Shares | Value | ||||||||||

| Securities Lending Collateral – 2.8% | |||||||||||

| 19,057,146 | Dreyfus Government Cash Management Fund (7 day yield of 0.01%) (h) | $ | 19,057,146 | ||||||||

| Total Securities Lending Collateral (Cost: $19,057,146) | 19,057,146 | ||||||||||

| Total Investments (Cost: $532,827,624) – 100.5% (i) (j) | 683,713,249 | ||||||||||

| Obligation to Return Collateral for Securities Loaned – (2.8)% | (19,057,146 | ) | |||||||||

| Cash and Other Assets Less Liabilities – 2.3% | 15,972,888 | ||||||||||

| Total Net Assets – 100.0% | $ | 680,628,991 | |||||||||

ADR = American Depositary Receipts

DVR = Differential Voting Right Equity Shares

GDR = Global Depositary Receipts

REIT = Real Estate Investment Trust

Notes to Statement of Investments (dollar values in thousands)

(a) All or a portion of this security was on loan at June 30, 2012. The total market value of securities on loan at June 30, 2012 was $18,795,678.

(b) Non-income producing security.

(c) Security is traded on a U.S. exchange.

(d) An affiliated person of the Fund may include any company in which the Fund owns five percent or more of its outstanding voting shares. Holdings and transactions in these affiliated companies during the six months ended June 30, 2012, are as follows:

Security | Balance of Shares Held 12/31/11 | Purchases/ Additions | Sales/ Reductions | Balance of Shares Held 6/30/12 | Value | Dividend | |||||||||||||||||||||

| Charles Taylor | 2,250,000 | — | — | 2,250,000 | $ | 5,620,525 | $ | 237,836 | |||||||||||||||||||

The aggregate cost and value of this company at June 30, 2012, was $9,152,033 and $5,620,525, respectively. Investments in the affiliated company represented 0.83% of the Fund's total net assets at June 30, 2012.

(e) Security exempt from registration under Section 4(2) of the Securities Act of 1933. This security may only be resold in exempt transactions to qualified buyers. Private resales of this security to qualified institutional buyers are also exempt from registration pursuant to Rule 144A under the Securities Act of 1933. At June 30, 2012, this security had an aggregate value of $1,467,813, which represented 0.22% of total net assets.

See accompanying notes to financial statements.

15

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

(f) Denotes a restricted security, which is subject to restrictions on resale under federal securities laws. These securities are valued at fair value determined in good faith under consistently applied procedures established by the Board of Trustees. At June 30, 2012, the market value of these securities amounted to $3,661,911, which represented 0.54% of total net assets.

Additional information on these securities is as follows:

Security | Acquisition Dates | Shares | Cost | Value | |||||||||||||||

| Union Agriculture Group | 12/8/10- 6/27/12 | 230,870 | $ | 2,649,999 | $ | 2,260,217 | |||||||||||||

| DeeThree Exploration | 9/7/10- 3/8/11 | 378,516 | 1,283,408 | 1,202,358 | |||||||||||||||

| Madalena Ventures | 10/21/10 | 604,000 | 382,726 | 199,336 | |||||||||||||||

| $4,316,133 | $3,661,911 | ||||||||||||||||||

(g) Illiquid security.

(h) Investment made with cash collateral received from securities lending activity.

(i) On June 30, 2012, the Fund's total investments were denominated in currencies as follows:

| Currency | Value | Percentage of Net Assets | |||||||||

| Japanese Yen | $ | 120,787,681 | 17.7 | ||||||||

| Euro | 97,705,658 | 14.4 | |||||||||

| United States Dollar | 59,258,859 | 8.7 | |||||||||

| British Pound | 53,928,663 | 7.9 | |||||||||

| Taiwan Dollar | 49,391,493 | 7.3 | |||||||||

| Hong Kong Dollar | 39,426,416 | 5.8 | |||||||||

| Other currencies less than 5% of total net assets | 244,157,333 | 35.9 | |||||||||

| $ | 664,656,103 | 97.7 | |||||||||

(j) At June 30, 2012, for federal income tax purposes, the cost of investments was $532,827,624 and net unrealized appreciation (depreciation) was $150,885,625 consisting of gross unrealized appreciation of $193,535,551 and gross unrealized depreciation of $42,649,926.

Fair Value Measurements

Various inputs are used in determining the value of the Fund's investments, following the input prioritization hierarchy established by GAAP. These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical securities

• Level 2 – prices determined using other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk and others)

• Level 3 – prices determined using significant unobservable inputs where quoted prices or observable inputs are unavailable or less reliable (including management's own assumptions about the factors market participants would use in pricing an investment)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Examples of the types of securities in which the Fund would typically invest and how they are classified within this hierarchy are as follows. Typical Level 1 securities include exchange traded domestic equities, mutual funds whose NAVs are published each day and exchange traded foreign equities that are not statistically fair valued. Typical Level 2 securities include exchange traded foreign equities that are statistically fair valued, forward foreign currency exchange contracts and short-term investments valued at amortized cost. Additionally, securities fair valued by the Valuation Committee (the Committee) of the Fund's Board of Trustees (the Board) that rely on significant observable inputs are also included in Level 2. Typical Level 3 securities include any security fair valued by the Committee that relies on significant unobservable inputs.

Under the direction of the Board, the Committee is responsible for carrying out the valuation procedures approved by the Board.

The Committee meets as necessary, and no less frequently than quarterly, to determine fair values for securities for which market quotations are not readily available or for which the investment manager believes that available market quotations are unreliable, and to review the continuing appropriateness of the current value of any security subject to the Trust's Portfolio Pricing Policy and the pricing procedures of the investment manager (the Policies). The Policies address, among other things: circumstances under which market quotations will be deemed readily available; selection of third party pricing vendors; appropriate pricing methodologies; events that require fair valuation and fair value techniques; and circumstances under which securities will be deemed to pose a potential for stale pricing, including when securities are illiquid, restricted, or in default. The Committee may also meet to discuss additional valuation matters, which may include review of back-testing results, review of time-sensitive information or approval of other valuation related actions, and to review the appropriateness of the Policies.

For investments categorized as Level 3, the significant unobservable inputs used in the fair value measurement of the Funds' securities may include: (i) data specific to the issuer or comparable issuers, (ii) general market or specific sector news and (iii) quoted prices and specific or similar security transactions. The Committee considers this data and any changes from prior periods in order to assess the reasonableness of observable and unobservable inputs, any assumptions or internal models used to value those securities and changes in fair value. Significant changes in any of these factors could result in lower or higher fair value measurements. Various factors impact the frequency of monitoring (which may occur as often as daily), however the Committee may determine that changes to inputs, assumptions and models are not required with the same frequency.

The following table summarizes the inputs used, as of June 30, 2012, in valuing the Fund's assets:

Investment Type | Quoted Prices (Level 1) | Other Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | |||||||||||||||

| Equities | |||||||||||||||||||

| Asia | $ | 18,441,343 | $ | 287,313,938 | $ | — | $ | 305,755,281 | |||||||||||

| Europe | 4,473,203 | 208,628,790 | — | 213,101,993 | |||||||||||||||

| Other Countries | 50,148,442 | 64,295,665 | — | 114,444,107 | |||||||||||||||

| Latin America | 28,895,170 | 199,335 | 2,260,217 | 31,354,722 | |||||||||||||||

| Total Equities | 101,958,158 | 560,437,728 | 2,260,217 | 664,656,103 | |||||||||||||||

| Total Securities Lending Collateral | 19,057,146 | — | — | 19,057,146 | |||||||||||||||

| Total Investments | $ | 121,015,304 | $ | 560,437,728 | $ | 2,260,217 | $ | 683,713,249 | |||||||||||

See accompanying notes to financial statements.

16

Wanger International 2012 Semiannual Report

Wanger International

Statement of Investments (Unaudited) June 30, 2012

The Fund's assets assigned to the Level 2 input category are generally valued using a market approach, in which a security's value is determined through its correlation to prices and information from observable market transactions for similar or identical assets. Foreign equities are generally valued at the last sale price on the foreign exchange or market on which they trade. The Fund may use a statistical fair valuation model, in accordance with the policy adopted by the Board, provided by an independent third party to value securities principally traded in foreign markets in order to adjust for possible stale pricing that may occur between the close of the foreign exchanges and the time for valuation. These models take into account available market data including intraday index, ADR, and ETF movements. Securities acquired via private placement that have a holding period or an extended settlement period are valued at a discount to the same shares that are trading freely on the market. These discounts are determined by the investment manager's experience with similar securities or situations. Factors may include, but are not limited to, trade volume, shares outstanding and stock price.

The following table shows transfers between Level 1 and Level 2 of the fair value hierarchy:

| Transfers In | Transfers Out | ||||||||||||||

| Level 1 | Level 2 | Level 1 | Level 2 | ||||||||||||

| $ | 1,451,902 | $ | — | $ | — | $ | 1,451,902 | ||||||||

Financial assets were transferred from Level 2 to Level 1 as resale restrictions no longer apply.

The following table reconciles asset balances for the period ending June 30, 2012, in which significant observable and/or unobservable inputs (Level 3) were used in determining value:

| Investments in Securities | Balance as of December 31, 2011 | Realized Gain/(Loss) | Change in Unrealized Appreciation (Depreciation) | Purchases | Sales | Transfers into Level 3 | Transfers out of Level 3 | Balance as of June 30, 2012 | |||||||||||||||||||||||||||

| Equities | |||||||||||||||||||||||||||||||||||

| Latin America | $ | 2,201,705 | $ | — | $ | 58,512 | $ | — | $ | — | $ | — | $ | — | $ | 2,260,217 | |||||||||||||||||||

| $ | 2,201,705 | $ | — | $ | 58,512 | $ | — | $ | — | $ | — | $ | — | $ | 2,260,217 | ||||||||||||||||||||

The information in the above reconciliation table represents fiscal year to date activity for any securities identified as using Level 3 inputs at either the beginning or the end of the current fiscal period.

The change in unrealized appreciation attributed to securities owned at June 30, 2012, which were valued using significant unobservable inputs (Level 3), amounted to $58,512.

The Fund does not hold any significant investments categorized as Level 3.

Certain common stock classified as Level 3 are valued at fair value, using a market approach, as determined in good faith under consistently applied procedures established by and under the general supervision of the Board. To determine fair value for these securities, for which no market exists, the Committee utilizes the valuation technique it deems most appropriate in the circumstances, using some unobservable inputs, which may include but are not limited to trades of similar securities, estimated earnings of the company, market multiples derived from a set of comparable companies, and the position of the security within the company's capital structure. Significant increases or decreases to any of these inputs could result in a significantly lower or higher fair value measurement. Generally, a change in estimated earnings of a company may result in a change to the comparable companies and market multiples utilized.

See accompanying notes to financial statements.

17

Wanger International 2012 Semiannual Report

Wanger International

Portfolio Diversification (Unaudited) June 30, 2012

At June 30, 2012 the funds investments as a percentage of net assets were diversified as follows:

| Value | Percentage of Net Assets | ||||||||||

| Industrial Goods & Services | |||||||||||

| Other Industrial Services | $ | 58,188,453 | 8.6 | ||||||||

| Machinery | 53,220,623 | 7.8 | |||||||||

| Industrial Materials & Specialty Chemicals | 32,102,105 | 4.7 | |||||||||

| Construction | 14,870,631 | 2.2 | |||||||||

| Industrial Distribution | 10,489,430 | 1.6 | |||||||||

| Electrical Components | 10,479,104 | 1.5 | |||||||||

| Conglomerates | 9,438,610 | 1.4 | |||||||||

| Outsourcing Services | 9,183,765 | 1.3 | |||||||||

| 197,972,721 | 29.1 | ||||||||||

| Consumer Goods & Services | |||||||||||

| Retail | 49,574,428 | 7.3 | |||||||||

| Food & Beverage | 38,806,616 | 5.7 | |||||||||

| Casinos & Gaming | 30,714,557 | 4.5 | |||||||||

| Other Consumer Services | 14,160,757 | 2.1 | |||||||||

| Apparel | 13,099,210 | 1.9 | |||||||||

| Travel | 5,672,200 | 0.8 | |||||||||

| Other Durable Goods | 4,700,868 | 0.7 | |||||||||

| Other Entertainment | 4,532,720 | 0.7 | |||||||||

| Educational Services | 3,681,650 | 0.5 | |||||||||

| Nondurables | 3,450,387 | 0.5 | |||||||||

| Restaurants | 3,282,333 | 0.5 | |||||||||

| Consumer Goods Distribution | 2,306,290 | 0.3 | |||||||||

| Furniture & Textiles | 1,883,259 | 0.3 | |||||||||

| 175,865,275 | 25.8 | ||||||||||

| Information | |||||||||||

| Computer Hardware & Related Equipment | 20,132,101 | 3.0 | |||||||||

| Internet Related | 16,490,773 | 2.4 | |||||||||

| Business Software | 7,399,638 | 1.1 | |||||||||

| Mobile Communications | 7,288,468 | 1.1 | |||||||||

| Instrumentation | 7,038,530 | 1.0 | |||||||||

| Electronics Distribution | 6,340,441 | 0.9 | |||||||||

| Telephone & Data Services | 5,996,923 | 0.9 | |||||||||

| Financial Processors | 5,612,062 | 0.8 | |||||||||

| Satellite Brodcasting & Services | 4,101,989 | 0.6 | |||||||||

| Semiconductors & Related Equipment | 3,957,874 | 0.6 | |||||||||

| Advertising | 2,315,301 | 0.3 | |||||||||

| Computer Services | 1,448,657 | 0.2 | |||||||||

| CATV | 1,220,625 | 0.2 | |||||||||

| 89,343,382 | 13.1 | ||||||||||

| Energy & Minerals | |||||||||||

| Oil & Gas Producers | 35,565,373 | 5.2 | |||||||||

| Mining | 23,500,027 | 3.5 | |||||||||

| Oil Services | 14,383,747 | 2.1 | |||||||||

| Agricultural Commodities | 6,450,051 | 1.0 | |||||||||

| Oil Refining, Marketing & Distribution | 809,505 | 0.1 | |||||||||

| 80,708,703 | 11.9 | ||||||||||

| Value | Percentage of Net Assets | ||||||||||