UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07239

Name of Registrant: Vanguard Horizon Funds

Address of Registrant: | P.O. Box 2600

Valley Forge, PA 19482 |

Name and address of agent for service: | Heidi Stam, Esquire |

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2005– September 30, 2006

Item 1: Reports to Shareholders |

Vanguard® Strategic Equity Fund |

| |

| |

> Annual Report | |

| |

| |

| |

| |

September 30, 2006 | |

| |

| |

|

|

| |

| |

| |

| |

| |

| |

| |

> | Vanguard Strategic Equity Fund returned 6.5% for the 2006 fiscal year. The fund underperformed both its benchmark index and the average peer fund. |

> | The advisor made some disappointing stock selections in the energy, health care, and financials sectors during the period. Its choices in the consumer discretionary and consumer staples sectors, however, made strong relative contributions to the fund’s return. |

> | The fund’s ten-year record is excellent; for the decade it has solidly outperformed both its benchmark index and peer group. |

Contents | |

| |

Your Fund’s Total Returns | 1 |

Chairman’s Letter | 2 |

Advisor’s Report | 7 |

Fund Profile | 9 |

Performance Summary | 10 |

Financial Statements | 11 |

Your Fund’s After-Tax Returns | 28 |

About Your Fund’s Expenses | 29 |

Glossary | 31 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the cover of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

Your Fund’s Total Returns

Fiscal Year Ended September 30, 2006 | |

| Total |

| Returns |

Vanguard Strategic Equity Fund | 6.5% |

MSCI US Small + Mid Cap 2200 Index | 8.6 |

Average Mid-Cap Core Fund1 | 7.3 |

Dow Jones Wilshire 5000 Index | 10.5 |

Your Fund’s Performance at a Glance |

September 30, 2005–September 30, 2006 |

| | | Distributions Per Share |

| Starting | Ending | Income | Capital |

| Share Price | Share Price | Dividends | Gains |

Vanguard Strategic Equity Fund | $23.28 | $23.07 | $0.21 | $1.44 |

1 | Derived from data provided by Lipper Inc. |

1

Chairman’s Letter

Dear Shareholder,

Vanguard Strategic Equity Fund returned 6.5% for the fiscal year ended September 30, 2006. This result fell short of the return of its benchmark, the Morgan Stanley Capital International (MSCI) US Small + Mid Cap 2200 Index, as well as of the average return of its competitive peers. The fund’s subpar performance resulted from some poorly performing stock choices and missed opportunities in key sectors.

Please note: On November 9, 2006, after the close of the fiscal period, the fund reopened to new accounts. It had been closed since April 20, 2006. The fund’s minimum initial investment was increased to $10,000.

Stocks endured some rough going, then recovered to post strong results

The stock market advanced through the first part of the fund’s fiscal year, then hit a speed bump in May, as investors feared that the economy was growing too rapidly. But a slowdown in the housing market, coupled with a late-summer decline in oil prices, helped to allay inflation concerns. The broad market rebounded to post a solid 10.5% return for the 12-month period. Value-oriented stocks outperformed growth stocks, and large-capitalization stocks edged out small-caps, one of the market’s best-performing segments in recent years.

2

International stocks handily outpaced domestic issues, continuing a multiyear trend. European and emerging market stocks fared particularly well. Stocks in the Pacific region also performed admirably, even though Japanese stocks did not fully participate in the global market’s summer recovery.

In the bond market, prices rallied as the Fed paused

At its August and September meetings, the Federal Reserve Board twice voted to maintain the federal funds rate at 5.25%, marking a pause in the central bank’s two-year inflation-fighting campaign. With investor sentiment buoyed by the

Fed’s near-term inflation outlook, interest rates decreased, driving bond prices higher. The broad taxable bond market finished the period with a 3.7% return, and municipal bonds performed slightly better.

Although rates decreased along the entire maturity spectrum in late summer, the difference between the yields of the shortest- and longest-term issues remained narrow by historical standards. At the end of September, the U.S. Treasury yield curve was actually inverted, meaning that short-term issues such as 3-month and 6-month Treasury notes offered higher yields than those with longer maturities.

Market Barometer | | | |

| Average Annual Total Returns |

| Periods Ended September 30, 2006 |

| One Year | Three Years | Five Years |

Stocks | | | |

Russell 1000 Index (Large-caps) | 10.2% | 12.8% | 7.6% |

Russell 2000 Index (Small-caps) | 9.9 | 15.5 | 13.8 |

Dow Jones Wilshire 5000 Index (Entire market) |

10.5

|

13.3

|

8.6

|

MSCI All Country World Index ex USA (International) | 19.4 | 23.9 | 16.4 |

| | | |

Bonds | | | |

Lehman Aggregate Bond Index (Broad taxable market) |

3.7%

|

3.4%

|

4.8%

|

Lehman Municipal Bond Index | 4.5 | 4.4 | 5.2 |

Citigroup 3-Month Treasury Bill Index | 4.4 | 2.6 | 2.2 |

| | | |

CPI | | | |

Consumer Price Index | 2.1% | 3.1% | 2.6% |

3

Stock-selection challenges led to performance deficit

The period was a challenging one for the Strategic Equity Fund’s computer-driven stock-selection process, which seeks to match the risk profile of the fund’s benchmark while outperforming the index through superior stock selection. The advisor had some miscues and missed opportunities in a few of the fund’s larger sectors—namely energy, health care, and financials—which together accounted for much of the fund’s shortfall versus the benchmark. In short, the advisor’s assessment of the prospects for some of its stock picks proved a bit more positive than the market’s sentiment. Among energy holdings, the fund’s oil and gas drillers turned in much poorer returns than those in the index. In the health care sector, the fund’s equipment makers and biotech holdings proved to be detractors versus those in the index. And among financials—the fund’s (and the benchmark’s) largest sector, at roughly one-fifth of assets, on average—insurance companies and asset managers in the fund’s portfolio failed to keep pace with their index counterparts.

On the positive side, the advisor made a number of good stock choices in consumer-oriented sectors. These sectors were aided by moderating energy prices and the unflinching strength of consumer spending. The fund’s consumer discretionary holdings were boosted by the surprisingly strong performances of apparel retailers and restaurants, particularly Guess? and Darden Restaurants. In consumer staples, tobacco maker Carolina Group and beverage distributor Pepsi Bottling Group were the top contributors to the fund’s relative return.

As the fiscal year’s results attest, the fund’s stock-selection models, which emphasize attractive valuations and earnings quality, are not always in sync with the short-term dynamics of the mid- and small-cap marketplace. The models also incorporate measures of market, or investor, sentiment, which can shift abruptly. As with any active strategy, the same characteristics that differentiate the fund from its benchmark, giving it the chance to outperform, can also lead to occasional periods of weakness. For more details on factors that influenced the fund’s performance over the period, see the Advisor’s Report on page 7.

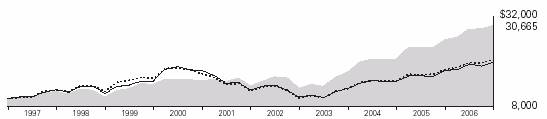

Long-term record is excellent

Despite its challenging recent fiscal period, the fund has proven the merit of its investment process by producing impressive long-term results. Indeed, the fund’s average annual return over the past ten years has surpassed that of its benchmark index by 1.4 percentage points. A hypothetical investment of $10,000 made in the fund ten years ago would have grown to $32,838 by September 30. By comparison, the same investment in the fund’s benchmark index would have

4

been worth $28,950. The second table below compares your fund’s performance with those of its comparative measures.

Your fund’s advisor, Vanguard Quantitative Equity Group, has worked diligently to hone its quantitative models in seeking superior results for the fund. The Strategic Equity Fund’s very low costs are also vital to its long-term success. Low costs help investors maximize their share of the fund’s returns. The first table below compares the fund’s expense ratio with that of its peer group.

Don’t let short-term performance cloud your long-term view

The short-term results of the latest “hot” mutual fund can divert some investors’ attention from the discipline and focus of long-term investing. For those investors, the lure of powerful short-term performance assumes priority over longer-term results.

At Vanguard, we counsel investors to discount short-term performance and, instead, to thoughtfully evaluate a fund’s long-term role within their portfolio. Is it a core holding or does it play a smaller role? Crucial to long-term investing is a well-thought-out, diversified portfolio of stock, bond, and money market funds tailored to meet your personal goals. Once you have completed this “advance” work, we suggest that you stay the course through the market’s ups and downs, resisting the short-term urge to tinker.

Expense Ratios1 | | |

Your fund compared with its peer group | | |

| | Average |

| | Mid-Cap |

| Fund | Core Fund |

Strategic Equity Fund | 0.35% | 1.52% |

Total Returns | | |

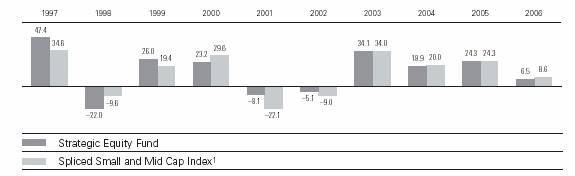

Ten Years Ended September 30, 2006 | | |

| Average | Final Value of a $10,000 |

| Annual Return | Initial Investment |

Strategic Equity Fund | 12.6% | $32,838 |

Spliced Small and Mid Cap Index2 | 11.2 | 28,950 |

Average Mid-Cap Core Fund | 11.5 | 29,632 |

Dow Jones Wilshire 5000 Index | 8.6 | 22,871 |

1 | Fund expense ratio reflects the 12 months ended September 30, 2006. Peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2005. |

2 | The Spliced Small and Mid Cap Index reflects the returns of the Russell 2800 Index through May 31, 2003, and the MSCI US Small + Mid Cap 2200 Index thereafter. |

5

As a part of the stock component of a balanced, diversified investment plan, the Strategic Equity Fund can play an important role in helping you to reach your long-term financial goals. Considering the advisor’s proven skill and the fund’s low operating expenses, we are optimistic about the fund’s prospects for posting competitive long-term results.

Thank you for your continued confidence in Vanguard.

Sincerely,

John J. Brennan

Chairman and Chief Executive Officer

November 9, 2006

6

Advisor’s Report

For the fiscal year ended September 30, 2006, the Vanguard Strategic Equity Fund returned 6.5%, underperforming its benchmark, the MSCI US Small + Mid Cap 2200 Index, which posted an 8.6% return. During the year, small- and mid-cap value stocks in the benchmark returned 10.3% and 10.0%, respectively, while its small- and mid-cap growth components earned comparatively less—5.4% and 8.1%, respectively. Energy stocks in the benchmark declined –6.5%, while its telecommunication services stocks rose 39.1%.

The investment environment

The benchmark’s solid, but unspectacular, return hid the instability underlying the market during the fiscal year. At the beginning of the period, the price of a barrel of West Texas Intermediate Crude oil was $66.25, the federal funds rate was 3.75%, and the 10-year U.S. Treasury note yielded 4.3%. In May 2006, the fund’s benchmark dropped –4.2% and in June, stock market volatility jumped to levels not seen in three years. During the summer, oil reached $77.03 per barrel, and the 10-year Treasury’s yield reached 5.2%. At the close of the fiscal year, oil stood at $62.92, the federal funds rate was 5.25%, and the 10-year Treasury yielded 4.6%. When we began the fiscal year, markets were extremely concerned about the Federal Reserve Board’s inflation-fighting resolve; as we end the fiscal year, the market’s concern seems to be assuaged.

In our view, it seems unlikely that the Fed’s inflation-fighting commitment has changed dramatically in the last year or that the supply-and-demand dynamics of petroleum have shifted significantly. We still maintain that the markets often overreact to short-term news—that is the basis of our stock-selection strategy.

Our investment approach

Our investment process evaluates each stock in the benchmark for its relative performance potential based on market sentiment, valuation, and earnings quality compared with its peers. We believe that at least one of these three elements captures the market’s overreaction to news. We construct our portfolio from the stocks that have the most attractive expected returns, while remaining neutral to industry and other risk factors. Thus, financials—our largest sector—represents 22% of the portfolio, not because of our view about financial stocks but because the benchmark has a weighting of 22.0% in this sector.

We aggressively buy and sell stocks within sectors in an attempt to provide higher returns than the benchmark. Based on our research to date, we have

7

concluded that attempting to add value by over- or underweighting sectors is not worth the additional risk. Chiefly, this is because we prefer to take many small positions in stocks, rather than a few big ones. With only ten sectors, one wrong over- or underweighting can adversely affect performance much more than one much smaller stock selection gone awry in a well-diversified portfolio. Similarly, we do not tilt toward or away from the benchmark’s smaller-capitalization stocks. The changes in the market environment highlighted earlier in this report demonstrate how difficult it is to add value by leaning toward specific industries or market segments.

The fund’s successes and shortfalls

During the fiscal year, our overall model was modestly successful in assessing future prospects. We add value in two ways: by purchasing stocks that outperform the market and by avoiding stocks that underperform. This year, the stocks that we identified for sale strongly underperformed the benchmark, while our candidates for purchase barely matched the market. Unfortunately, the stocks we held in the portfolio did not match the success of our model. This factor, together with our sentiment indicator’s lackluster results, was the main contributor to the year’s subpar performance.

Our best performance relative to the benchmark was in consumer discretionary stocks, where our overweighted positions in Guess? (+126% for the fiscal year) and Abercrombie & Fitch (+41%) helped the portfolio outperform the benchmark sector. On the other hand, health care was our worst-performing sector relative to the benchmark; our positions in Manor Care (+38%) and Andrx Group (+58%) were unable to overcome the drag from our holdings in Apria Health-care Group (–38%) and United Therapeutics (–25%).

We expect occasional periods of underperformance in our portfolio, since we take significant stock-specific risks in our effort to outperform our universe. While the past year was not a total success, our process has worked well over time. We feel that the fund offers an attractive mix of stocks with high earnings quality, market acceptance, and reasonable valuations. We look forward to the coming fiscal year with confidence in our process.

James D. Troyer,

Principal and Portfolio Manager

Joel M. Dickson, Principal

Vanguard Quantitative Equity Group

October 19, 2006

8

Fund Profile

As of September 30, 2006

Portfolio Characteristics | | |

| | Comparative | Broad |

| Fund | Index1 | Index2 |

Number of Stocks | 777 | 2,174 | 4,974 |

Median Market Cap | $3.5B | $3.8B | $27.5B |

Price/Earnings Ratio | 15.6x | 20.7x | 17.2x |

Price/Book Ratio | 2.4x | 2.5x | 3.7x |

Yield | 1.1% | 1.3% | 1.7% |

Return on Equity | 14.0% | 13.4% | 15.4% |

Earnings Growth Rate | 17.9% | 16.4% | 15.7% |

Foreign Holdings | 0.2% | 0.0% | 1.1% |

Turnover Rate | 80% | — | — |

Expense Ratio | 0.35% | — | — |

Short-Term Reserves | 0% | — | — |

Sector Diversification (% of portfolio) |

| | Comparative | Broad |

| Fund | Index1 | Index2 |

Consumer Discretionary | 16% | 16% | 12% |

Consumer Staples | 3 | 3 | 9 |

Energy | 8 | 8 | 9 |

Financials | 22 | 22 | 23 |

Health Care | 10 | 10 | 12 |

Industrials | 13 | 13 | 11 |

Information Technology | 15 | 15 | 15 |

Materials | 5 | 5 | 3 |

Telecommunication | | | |

Services | 2 | 2 | 3 |

Utilities | 6 | 6 | 3 |

Volatility Measures3 | |

| Fund Versus | Fund Versus |

| Comparative Index1 | Broad Index2 |

R-Squared | 0.98 | 0.84 |

Beta | 1.03 | 1.35 |

Ten Largest Holdings4 (% of total net assets) |

| | |

AmerisourceBergen Corp. | health care | |

| distributors | 1.0% |

Parker Hannifin Corp. | industrial machinery | 1.0 |

Fiserv, Inc. | data processing and | |

| outsourced services | 1.0 |

Safeco Corp. | property and | |

| casualty insurance | 1.0 |

Nordstrom, Inc. | department stores | 1.0 |

Whirlpool Corp. | household appliances | 1.0 |

Freeport-McMoRan | | |

Copper & Gold, Inc. | diversified metals | |

Class B | and mining | 0.9 |

Cummins Inc. | construction and | |

| farm machinery and | |

| heavy trucks | 0.9 |

Darden Restaurants Inc. | restaurants | 0.9 |

Radian Group, Inc. | thrifts and | |

| mortgage finance | 0.9 |

Top Ten | | 9.6% |

Investment Focus

1 | MSCI US Small + Mid Cap 2200 Index. |

2 | Dow Jones Wilshire 5000 Index. |

3 | For an explanation of R-squared, beta, and other terms used here, see the Glossary on page 31. |

4 | “Ten Largest Holdings” excludes any temporary cash investments and equity index products. |

9

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

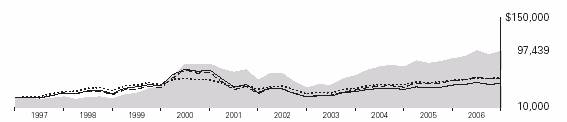

Cumulative Performance: September 30, 1996–September 30, 2006

Initial Investment of $10,000

| | | | |

| Average Annual Total Returns | Final Value |

| Periods Ended September 30, 2006 | of a $10,000 |

| One Year | Five Years | Ten Years | Investment |

Strategic Equity Fund | 6.49% | 14.89% | 12.63% | $32,838 |

Dow Jones Wilshire 5000 Index | 10.48 | 8.64 | 8.62 | 22,871 |

Spliced Small and Mid Cap Index1 | 8.61 | 14.59 | 11.22 | 28,950 |

Average Mid-Cap Core Fund2 | 7.27 | 11.61 | 11.47 | 29,632 |

Fiscal-Year Total Returns (%): September 30, 1996–September 30, 2006

| 1 | The Spliced Small and Mid Cap Index reflects the returns of the Russell 2800 Index through May 31, 2003, and the MSCI US Small + Mid Cap 2200 Index thereafter. |

| 2 | Derived from data provided by Lipper Inc. |

Note: See Financial Highlights table on page 23 for dividend and capital gains information.

10

Financial Statements

Statement of Net Assets

As of September 30, 2006

The fund provides a complete list of its holdings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at www.sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | Market |

| | | Value• |

| | Shares | ($000) |

Common Stocks (100.0%)1 | | |

Consumer Discretionary (15.7%) | |

| Nordstrom, Inc. | 1,536,900 | 65,011 |

| Whirlpool Corp. | 770,800 | 64,832 |

| Darden Restaurants Inc. | 1,411,300 | 59,938 |

| VF Corp. | 749,294 | 54,661 |

| Royal Caribbean | | |

| Cruises, Ltd. | 1,229,019 | 47,698 |

| Abercrombie & Fitch Co. | 496,300 | 34,483 |

| Polo Ralph Lauren Corp. | 523,380 | 33,857 |

* | Guess ?, Inc. | 687,900 | 33,384 |

* | AutoNation, Inc. | 1,493,347 | 31,211 |

| Phillips-Van Heusen Corp. | 719,100 | 30,037 |

* | Liberty Media Capital A | 303,947 | 25,401 |

| Brinker International, Inc. | 612,800 | 24,567 |

| Men’s Wearhouse, Inc. | 603,350 | 22,451 |

| Newell Rubbermaid, Inc. | 675,146 | 19,120 |

| Cablevision Systems | | |

| NY Group Class A | 805,600 | 18,295 |

| Dillard’s Inc. | 555,200 | 18,172 |

| Jackson Hewitt Tax | | |

| Service Inc. | 580,000 | 17,406 |

| Catalina Marketing Corp. | 610,570 | 16,791 |

| Ruby Tuesday, Inc. | 581,800 | 16,401 |

* | The Goodyear Tire & | | |

| Rubber Co. | 1,037,799 | 15,048 |

| New York Times Co. | | |

| Class A | 643,386 | 14,785 |

| Barnes & Noble, Inc. | 370,045 | 14,040 |

| ^Regal Entertainment Group | |

| Class A | 681,147 | 13,500 |

* | CSK Auto Corp. | 879,600 | 12,402 |

* | Skechers U.S.A., Inc. | 501,200 | 11,783 |

| Sherwin-Williams Co. | 208,357 | 11,622 |

| Jones Apparel Group, Inc. | 352,800 | 11,445 |

* | Payless ShoeSource, Inc. | 459,400 | 11,439 |

* | Charming Shoppes, Inc. | 777,258 | 11,099 |

| Meredith Corp. | 193,320 | 9,536 |

* | The Pantry, Inc. | 166,400 | 9,380 |

| Washington Post Co. Class B | 12,378 | 9,123 |

* | NVR, Inc. | 17,000 | 9,095 |

* | Jack in the Box Inc. | 173,100 | 9,032 |

* | MGM Mirage, Inc. | 228,422 | 9,020 |

| Bob Evans Farms, Inc. | 284,017 | 8,600 |

| Claire’s Stores, Inc. | 268,300 | 7,824 |

* | RCN Corp. | 273,012 | 7,726 |

| K-Swiss, Inc. | 252,351 | 7,586 |

| Belo Corp. Class A | 448,900 | 7,097 |

* | Genesco, Inc. | 200,200 | 6,901 |

| Mattel, Inc. | 343,400 | 6,765 |

| Cato Corp. Class A | 271,350 | 5,945 |

* | DreamWorks | | |

| Animation SKG, Inc. | 234,133 | 5,832 |

| Domino’s Pizza, Inc. | 218,100 | 5,594 |

* | Mohawk Industries, Inc. | 73,925 | 5,504 |

* | Gemstar-TV Guide | | |

| International, Inc. | 1,603,422 | 5,323 |

* | ProQuest Co. | 408,440 | 5,318 |

* | JAKKS Pacific, Inc. | 285,500 | 5,090 |

| Entercom | | |

| Communications Corp. | 199,999 | 5,040 |

| John Wiley & Sons Class A | 133,800 | 4,818 |

| ServiceMaster Co. | 427,200 | 4,789 |

| Brown Shoe Co., Inc. | 122,900 | 4,405 |

| Modine Manufacturing Co. | 174,700 | 4,250 |

| ^Bandag, Inc. | 103,500 | 4,248 |

* | Laureate Education Inc. | 88,224 | 4,222 |

| Group 1 Automotive, Inc. | 83,500 | 4,167 |

| ^Furniture Brands | | |

| International Inc. | 217,000 | 4,132 |

| Sonic Automotive, Inc. | 175,000 | 4,041 |

* | Wyndham Worldwide Corp. | 142,900 | 3,997 |

* | Career Education Corp. | 163,900 | 3,688 |

| United Auto Group, Inc. | 156,000 | 3,650 |

| World Wrestling | | |

| Entertainment, Inc. | 209,087 | 3,435 |

* | Cox Radio, Inc. | 222,131 | 3,410 |

| Harte-Hanks, Inc. | 128,200 | 3,378 |

* | The Dress Barn, Inc. | 154,780 | 3,377 |

| Warner Music Group Corp. | 122,163 | 3,170 |

11

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Visteon Corp. | 382,900 | 3,121 |

* | TRW Automotive | | |

| Holdings Corp. | 129,546 | 3,118 |

| Steven Madden, Ltd. | 74,131 | 2,909 |

| Beazer Homes USA, Inc. | 69,800 | 2,725 |

| Building Materials | | |

| Holding Corp. | 103,900 | 2,703 |

| ArvinMeritor, Inc. | 189,300 | 2,696 |

* | Select Comfort Corp. | 112,900 | 2,470 |

* | Corinthian Colleges, Inc. | 223,600 | 2,417 |

* | Meritage Corp. | 57,700 | 2,401 |

| American Greetings Corp. | | |

| Class A | 100,700 | 2,328 |

| IHOP Corp. | 47,300 | 2,192 |

* | Papa John’s International, Inc. | 60,621 | 2,189 |

| Sotheby’s | 66,278 | 2,137 |

* | Blockbuster Inc. Class A | 544,000 | 2,089 |

* | Steak n Shake Co. | 121,208 | 2,047 |

| Ethan Allen Interiors, Inc. | 59,000 | 2,045 |

| Advance Auto Parts, Inc. | 55,786 | 1,838 |

| Journal Communications, Inc. | 160,900 | 1,813 |

| Ross Stores, Inc. | 70,643 | 1,795 |

| Dow Jones & Co., Inc. | 53,000 | 1,778 |

| Aaron Rents, Inc. Class B | 68,800 | 1,581 |

| Asbury Automotive Group, Inc. | 76,300 | 1,572 |

| Movado Group, Inc. | 61,100 | 1,553 |

| Kimball International, Inc. | | |

| Class B | 78,786 | 1,521 |

| International Speedway Corp. | 29,684 | 1,479 |

* | Dollar Tree Stores, Inc. | 46,704 | 1,446 |

| Stage Stores, Inc. | 48,000 | 1,408 |

| UniFirst Corp. | 44,200 | 1,381 |

* | Spanish Broadcasting | | |

| System, Inc. | 313,574 | 1,370 |

| Service Corp. International | 139,900 | 1,307 |

| The Buckle, Inc. | 34,100 | 1,294 |

| Dover Downs Gaming & | | |

| Entertainment, Inc. | 104,450 | 1,269 |

| Winnebago Industries, Inc. | 39,600 | 1,243 |

* | FTD Group, Inc. | 79,900 | 1,234 |

* | ^Tempur-Pedic International Inc. | 66,000 | 1,133 |

| ^Brookfield Homes Corp. | 31,800 | 896 |

* | ^Netflix.com, Inc. | 38,025 | 866 |

| Kellwood Co. | 27,400 | 790 |

* | O’Charley’s Inc. | 40,900 | 776 |

| Haverty Furniture Cos., Inc. | 48,200 | 769 |

| Landry’s Restaurants, Inc. | 24,600 | 742 |

* | Tenneco Automotive, Inc. | 27,800 | 650 |

| Lithia Motors, Inc. | 20,900 | 517 |

* | Interactive Data Corp. | 25,000 | 499 |

| Liz Claiborne, Inc. | 12,300 | 486 |

* | Vertrue Inc. | 11,600 | 456 |

* | Harris Interactive Inc. | 73,070 | 446 |

| Technical Olympic USA, Inc. | 43,000 | 423 |

| CSS Industries, Inc. | 12,700 | 377 |

| Xerium Technologies Inc. | 31,600 | 350 |

* | Penn National Gaming, Inc. | 8,566 | 313 |

| Stewart Enterprises, Inc. | | |

| Class A | 45,958 | 269 |

* | ITT Educational Services, Inc. | 3,800 | 252 |

| American Eagle Outfitters, Inc. | 5,600 | 245 |

* | Denny’s Corp. | 56,917 | 194 |

| Journal Register Co. | 31,300 | 177 |

| Salem Communications Corp. | 7,207 | 82 |

| | | 1,057,564 |

Consumer Staples (3.2%) | | |

| Carolina Group | 867,600 | 48,056 |

| The Pepsi Bottling | | |

| Group, Inc. | 951,500 | 33,778 |

| The Kroger Co. | 622,000 | 14,393 |

* | Central Garden and Pet Co. | 264,440 | 12,762 |

| Del Monte Foods Co. | 1,139,527 | 11,908 |

| Brown-Forman Corp. | | |

| Class B | 155,107 | 11,889 |

| Longs Drug Stores, Inc. | 244,410 | 11,245 |

* | Herbalife Ltd. | 274,700 | 10,406 |

* | Energizer Holdings, Inc. | 142,800 | 10,280 |

* | Hansen Natural Corp. | 266,324 | 8,650 |

| The Great Atlantic & | | |

| Pacific Tea Co., Inc. | 300,199 | 7,229 |

| Estee Lauder Cos. Class A | 139,300 | 5,618 |

* | NBTY, Inc. | 169,783 | 4,970 |

| Lancaster Colony Corp. | 90,100 | 4,033 |

| Ruddick Corp. | 120,700 | 3,142 |

| Corn Products | | |

| International, Inc. | 93,500 | 3,043 |

| Seaboard Corp. | 2,290 | 2,759 |

* | Dean Foods Co. | 65,602 | 2,757 |

* | Prestige Brands Holdings Inc. | 197,000 | 2,195 |

| Molson Coors Brewing Co. | | |

| Class B | 28,200 | 1,943 |

* | Performance Food Group Co. | 57,991 | 1,629 |

| Ingles Markets, Inc. | 44,400 | 1,171 |

| ^Mannatech, Inc. | 62,984 | 1,116 |

| Weis Markets, Inc. | 18,300 | 728 |

| Premium Standard Farms Inc. | 34,770 | 662 |

* | Wild Oats Markets Inc. | 36,667 | 593 |

* | BJ’s Wholesale Club, Inc. | 20,200 | 589 |

* | Alliance One | | |

| International, Inc. | 120,000 | 492 |

| Vector Group Ltd. | 26,590 | 431 |

| Chiquita Brands | | |

| International, Inc. | 10,748 | 144 |

| | | 218,611 |

Energy (8.1%) | | |

| Patterson-UTI Energy, Inc. | 2,112,927 | 50,203 |

| Helmerich & Payne, Inc. | 2,142,242 | 49,336 |

| Sunoco, Inc. | 584,900 | 36,375 |

| Chesapeake Energy Corp. | 1,240,729 | 35,956 |

| Hess Corp. | 813,627 | 33,700 |

| Tesoro Petroleum Corp. | 483,500 | 28,033 |

* | Swift Energy Co. | 609,600 | 25,493 |

12

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Nabors Industries, Inc. | 778,762 | 23,168 |

| Frontier Oil Corp. | 853,200 | 22,678 |

* | Todco Class A | 633,825 | 21,930 |

| Holly Corp. | 502,958 | 21,793 |

* | Helix Energy | | |

| Solutions Group, Inc. | 622,682 | 20,798 |

* | Unit Corp. | 405,012 | 18,618 |

| ENSCO International, Inc. | 409,709 | 17,958 |

| Rowan Cos., Inc. | 516,506 | 16,337 |

* | Veritas DGC Inc. | 243,433 | 16,023 |

* | Grey Wolf, Inc. | 2,017,419 | 13,476 |

* | Atwood Oceanics, Inc. | 294,100 | 13,226 |

| Diamond Offshore | | |

| Drilling, Inc. | 179,750 | 13,009 |

* | Pioneer Drilling Co. | 957,400 | 12,293 |

* | Denbury Resources, Inc. | 424,097 | 12,256 |

| El Paso Corp. | 746,900 | 10,188 |

| Tidewater Inc. | 164,000 | 7,247 |

* | Maverick Tube Corp. | 73,800 | 4,784 |

* | Pride International, Inc. | 155,500 | 4,264 |

* | SEACOR Holdings Inc. | 43,300 | 3,572 |

* | Parker Drilling Co. | 363,500 | 2,574 |

* | NS Group Inc. | 37,700 | 2,434 |

| W&T Offshore, Inc. | 79,800 | 2,331 |

* | Lone Star Technologies, Inc. | 46,792 | 2,264 |

| Foundation Coal Holdings, Inc. | 66,000 | 2,136 |

* | Giant Industries, Inc. | 24,675 | 2,004 |

* | Stone Energy Corp. | 41,800 | 1,692 |

* | Energy Partners, Ltd. | 61,300 | 1,511 |

* | Hercules Offshore, Inc. | 5,000 | 155 |

| | | 549,815 |

Financials (22.1%) | | |

| Capital Markets (2.1%) | | |

| Ameriprise Financial, Inc. | 1,213,121 | 56,895 |

* | E*TRADE Financial Corp. | 1,557,744 | 37,261 |

| Raymond James | | |

| Financial, Inc. | 411,150 | 12,022 |

* | Investment Technology | | |

| Group, Inc. | 215,280 | 9,634 |

| A.G. Edwards & Sons, Inc. | 165,700 | 8,829 |

* | Knight Capital Group, Inc. | | |

| Class A | 472,753 | 8,604 |

| MCG Capital Corp. | 296,008 | 4,834 |

* | Piper Jaffray Cos., Inc. | 58,200 | 3,528 |

| Gamco Investors Inc. Class A | 59,929 | 2,281 |

| T. Rowe Price Group Inc. | 22,383 | 1,071 |

| Capital Southwest Corp. | 1,000 | 119 |

| | | |

| Commercial Banks (3.1%) | | |

| Synovus Financial Corp. | 1,211,657 | 35,586 |

| Huntington Bancshares Inc. | 1,060,551 | 25,379 |

| TCF Financial Corp. | 841,500 | 22,123 |

| Colonial BancGroup, Inc. | 887,200 | 21,736 |

| Bank of Hawaii Corp. | 412,986 | 19,889 |

| First Republic Bank | 199,331 | 8,484 |

| Sterling Bancshares, Inc. | 251,700 | 5,097 |

| Hancock Holding Co. | 92,195 | 4,937 |

| BancorpSouth, Inc. | 170,933 | 4,745 |

| United Bankshares, Inc. | 118,080 | 4,395 |

| City Holding Co. | 106,855 | 4,260 |

| Whitney Holdings Corp. | 104,700 | 3,745 |

| Greater Bay Bancorp | 130,701 | 3,687 |

| Independent Bank Corp. (MI) | 149,035 | 3,619 |

| Compass Bancshares Inc. | 53,700 | 3,060 |

| Columbia Banking | | |

| System, Inc. | 81,828 | 2,619 |

| F.N.B. Corp. | 154,100 | 2,567 |

| Trustmark Corp. | 79,500 | 2,499 |

| BOK Financial Corp. | 44,886 | 2,361 |

| Republic Bancorp, Inc. | 141,800 | 1,890 |

| Citizens Banking Corp. | 64,900 | 1,704 |

| Susquehanna Bancshares, Inc. | 58,600 | 1,432 |

| Pacific Capital Bancorp | 50,000 | 1,349 |

| NBT Bancorp, Inc. | 56,252 | 1,308 |

| Old National Bancorp | 64,200 | 1,226 |

| BancFirst Corp. | 25,322 | 1,183 |

| Chittenden Corp. | 37,300 | 1,070 |

| Sterling Financial Corp. | 31,300 | 1,015 |

| IBERIABANK Corp. | 14,700 | 897 |

| Sterling Financial Corp. (PA) | 38,588 | 849 |

| Community Trust Bancorp Inc. | 21,356 | 804 |

| First Indiana Corp. | 27,587 | 718 |

| Nara Bancorp, Inc. | 38,605 | 706 |

| Integra Bank Corp. | 26,401 | 667 |

| Hanmi Financial Corp. | 32,800 | 643 |

| Sky Financial Group, Inc. | 25,736 | 641 |

| Union Bankshares Corp. | 14,000 | 620 |

| United Community Banks, Inc. | 19,603 | 589 |

| Peoples Bancorp, Inc. | 19,800 | 579 |

| R & G Financial Corp. Class B | 74,100 | 552 |

| West Coast Bancorp | 17,842 | 545 |

| Banner Corp. | 13,037 | 535 |

| First Community | | |

| Bancshares, Inc. | 16,018 | 535 |

| TriCo Bancshares | 21,042 | 521 |

| Capitol Bancorp Ltd. | 11,300 | 503 |

| Center Financial Corp. | 19,300 | 459 |

| U.S.B. Holding Co., Inc. | 19,124 | 422 |

| Great Southern Bancorp, Inc. | 14,280 | 401 |

| CVB Financial Corp. | 22,467 | 332 |

| First Citizens BancShares | | |

| Class A | 1,700 | 325 |

| Provident Bankshares Corp. | 7,903 | 293 |

| Independent Bank Corp. (MA) | 7,411 | 241 |

| First Merchants Corp. | 7,586 | 179 |

First Source Corp. | 5,845 | 173 |

Simmons First National Corp. | 5,942 | 172 |

FirstMerit Corp. | 6,101 | 141 |

Suffolk Bancorp | 4,423 | 141 |

Harleysville National Corp. | 6,019 | 121 |

First Financial Bankshares, Inc. | 2,900 | 111 |

First Financial Corp. (IN) | 3,122 | 100 |

| | |

| | |

13

| | | Market |

| | | Value• |

| | Shares | ($000) |

| Heartland Financial USA, Inc. | 3,169 | 81 |

| First Bancorp (NC) | 3,946 | 80 |

| Washington Trust Bancorp, Inc. | 2,200 | 58 |

| | | |

| Consumer Finance (0.9%) | | |

* | AmeriCredit Corp. | 1,057,545 | 26,428 |

| ^The First Marblehead Corp. | 179,000 | 12,398 |

| Advanta Corp. Class B | 235,197 | 8,679 |

* | World Acceptance Corp. | 136,100 | 5,986 |

| Cash America | | |

| International Inc. | 114,624 | 4,480 |

| Advance America, Cash | | |

| Advance Centers, Inc. | 14,723 | 212 |

| | | |

| Diversified Financial Services (0.4%) | |

| Leucadia National Corp. | 864,290 | 22,618 |

| Resource America, Inc. | 65,020 | 1,352 |

* | Primus Guaranty, Ltd. | 75,722 | 917 |

* | Asset Acceptance | | |

| Capital Corp. | 52,933 | 860 |

| | | |

| Insurance (4.0%) | | |

| Safeco Corp. | 1,109,502 | 65,383 |

| First American Corp. | 763,821 | 32,340 |

| W.R. Berkley Corp. | 680,735 | 24,091 |

| Nationwide Financial | | |

| Services, Inc. | 450,400 | 21,664 |

| Assurant, Inc. | 344,500 | 18,400 |

| LandAmerica Financial | | |

| Group, Inc. | 249,300 | 16,401 |

| UnumProvident Corp. | 841,900 | 16,324 |

| Zenith National | | |

| Insurance Corp. | 375,909 | 14,995 |

| Ohio Casualty Corp. | 499,483 | 12,922 |

| American Financial | | |

| Group, Inc. | 188,200 | 8,832 |

| Hanover Insurance | | |

| Group Inc. | 191,400 | 8,542 |

| Stewart Information | | |

| Services Corp. | 209,900 | 7,298 |

* | Philadelphia Consolidated | | |

| Holding Corp. | 100,300 | 3,990 |

| Safety Insurance Group, Inc. | 81,220 | 3,952 |

| Fidelity National Financial, Inc. | 64,200 | 2,674 |

| ^Fidelity National Title | | |

| Group, Inc. Class A | 113,200 | 2,373 |

| Cincinnati Financial Corp. | 49,118 | 2,361 |

| ^Odyssey Re Holdings Corp. | 48,100 | 1,625 |

| Scottish Re Group Ltd. | 134,200 | 1,459 |

* | Argonaut Group, Inc. | 33,599 | 1,043 |

| Infinity Property & | | |

| Casualty Corp. | 22,589 | 929 |

| Commerce Group, Inc. | 27,010 | 812 |

| IPC Holdings Ltd. | 22,000 | 669 |

| Horace Mann Educators Corp. | 34,200 | 658 |

| National Western Life | | |

| Insurance Co. Class A | 2,720 | 625 |

| Bristol West Holdings, Inc. | 31,000 | 451 |

| Presidential Life Corp. | 19,000 | 425 |

| Harleysville Group, Inc. | 11,100 | 388 |

| Axis Capital Holdings Ltd. | 11,000 | 382 |

| Torchmark Corp. | 6,000 | 379 |

* | CNA Surety Corp. | 15,800 | 319 |

| Crawford & Co. Class B | 3,200 | 22 |

| | | |

| Real Estate Investment Trusts (7.6%) | |

| Archstone-Smith Trust REIT | 725,200 | 39,480 |

| Host Marriott Corp. REIT | 1,384,400 | 31,744 |

| ProLogis REIT | 444,824 | 25,382 |

| Avalonbay Communities, Inc. | | |

| REIT | 202,300 | 24,357 |

| Boston Properties, Inc. REIT | 220,100 | 22,745 |

| Essex Property Trust, Inc. | | |

| REIT | 152,700 | 18,538 |

| General Growth | | |

| Properties Inc. REIT | 366,400 | 17,459 |

| Plum Creek | | |

| Timber Co. Inc. REIT | 495,600 | 16,870 |

| Pan Pacific Retail | | |

| Properties, Inc. REIT | 186,300 | 12,933 |

| Camden Property Trust REIT | 168,100 | 12,777 |

| Developers Diversified | | |

| Realty Corp. REIT | 228,900 | 12,763 |

| Apartment Investment & | | |

| Management Co. Class A | | |

| REIT | 211,200 | 11,491 |

| SL Green Realty Corp. REIT | 94,600 | 10,567 |

| Regency Centers Corp. REIT | 151,700 | 10,431 |

| iStar Financial Inc. REIT | 236,800 | 9,875 |

| United Dominion Realty Trust | | |

| REIT | 312,400 | 9,434 |

| Federal Realty | | |

| Investment Trust REIT | 121,900 | 9,057 |

| Taubman Co. REIT | 200,800 | 8,920 |

| Maguire Properties, Inc. REIT | 217,100 | 8,845 |

| New Plan Excel Realty Trust | | |

| REIT | 312,700 | 8,459 |

| Reckson Associates | | |

| Realty Corp. REIT | 194,726 | 8,334 |

| AMB Property Corp. REIT | 149,100 | 8,217 |

| Kimco Realty Corp. REIT | 187,600 | 8,042 |

| Tanger Factory Outlet | | |

| Centers, Inc. REIT | 223,300 | 7,954 |

| BRE Properties Inc. Class A | | |

| REIT | 128,000 | 7,645 |

| The Macerich Co. REIT | 96,300 | 7,353 |

| FelCor Lodging Trust, Inc. | | |

| REIT | 364,700 | 7,312 |

| Kilroy Realty Corp. REIT | 92,500 | 6,969 |

| Post Properties, Inc. REIT | 129,600 | 6,159 |

14

| | Market |

| | Value• |

| Shares | ($000) |

Home Properties, Inc. REIT | 104,700 | 5,985 |

Colonial Properties Trust REIT | 120,800 | 5,775 |

Thornburg Mortgage, Inc. | | |

REIT | 214,300 | 5,458 |

^New Century Financial Corp. | | |

REIT | 137,692 | 5,413 |

Rayonier Inc. REIT | 142,050 | 5,370 |

HRPT Properties Trust REIT | 443,500 | 5,300 |

Heritage Property | | |

Investment Trust REIT | 139,200 | 5,075 |

Global Signal, Inc. REIT | 90,000 | 4,552 |

CapitalSource Inc. REIT | 171,400 | 4,426 |

^Novastar Financial, Inc. REIT | 149,600 | 4,367 |

American Home Mortgage | | |

Investment Corp. REIT | 125,000 | 4,359 |

Annaly Mortgage | | |

Management Inc. REIT | 316,600 | 4,160 |

Equity Inns, Inc. REIT | 257,300 | 4,096 |

Glimcher Realty Trust REIT | 159,700 | 3,957 |

Innkeepers USA Trust REIT | 236,100 | 3,846 |

Sunstone Hotel | | |

Investors, Inc. REIT | 121,800 | 3,620 |

KKR Financial Corp. REIT | 145,100 | 3,561 |

Saul Centers, Inc. REIT | 75,700 | 3,407 |

^Redwood Trust, Inc. REIT | 62,900 | 3,168 |

Weingarten Realty Investors | | |

REIT | 68,300 | 2,938 |

Friedman, Billings, | | |

Ramsey Group, Inc. REIT | 359,900 | 2,890 |

Impac Mortgage | | |

Holdings, Inc. REIT | 281,600 | 2,639 |

Senior Housing | | |

Properties Trust REIT | 122,400 | 2,612 |

LaSalle Hotel Properties REIT | 59,600 | 2,583 |

Potlatch Corp. REIT | 65,400 | 2,426 |

BioMed Realty Trust, Inc. | | |

REIT | 79,500 | 2,412 |

Pennsylvania REIT | 48,100 | 2,048 |

American Financial | | |

Realty Trust REIT | 179,800 | 2,007 |

Strategic Hotels and | | |

Resorts, Inc. REIT | 99,900 | 1,986 |

Saxon Inc. REIT | 130,000 | 1,825 |

GMH Communities Trust | | |

REIT | 115,000 | 1,451 |

Mills Corp. REIT | 71,700 | 1,198 |

Inland Real Estate Corp. REIT | 30,700 | 538 |

MFA Mortgage | | |

Investments, Inc. REIT | 71,500 | 533 |

Franklin Street | | |

Properties Corp. REIT | 26,300 | 522 |

Highland Hospitality Corp. | | |

| REIT | 36,400 | 522 |

| Digital Realty Trust, Inc. REIT | 16,600 | 520 |

| Spirit Finance Corp. REIT | 44,600 | 518 |

| National Health Investors REIT | 18,200 | 516 |

| Acadia Realty Trust REIT | 20,100 | 513 |

| RAIT Investment Trust REIT | 17,700 | 511 |

| Trustreet Properties, Inc. REIT | 40,800 | 510 |

| Hospitality Properties Trust | | |

| REIT | 10,700 | 505 |

| Lexington Corporate | | |

| Properties Trust REIT | 23,800 | 504 |

| Omega Healthcare | | |

| Investors, Inc. REIT | 33,500 | 503 |

| Ashford Hospitality Trust REIT | 41,900 | 500 |

| Newcastle Investment Corp. | | |

| REIT | 18,200 | 499 |

| Anthracite Capital Inc. REIT | 38,700 | 498 |

| Deerfield Triarc Capital Corp. | | |

| REIT | 37,900 | 497 |

| DiamondRock Hospitality Co. | | |

| REIT | 29,700 | 493 |

| First Potomac REIT | 16,000 | 484 |

| Longview Fibre Co. REIT | 23,300 | 473 |

| Sun Communities, Inc. REIT | 5,700 | 182 |

| | | |

| Real Estate Management & Development (0.7%) |

| ^The St. Joe Co. | 260,100 | 14,272 |

* | CB Richard Ellis Group, Inc. | 418,200 | 10,288 |

| Jones Lang LaSalle Inc. | 118,800 | 10,155 |

| Forest City Enterprise | | |

| Class A | 154,400 | 8,384 |

* | Trammell Crow Co. | 58,300 | 2,129 |

* | Move, Inc. | 108,900 | 535 |

| | | |

| Thrifts & Mortgage Finance (3.3%) | |

| Radian Group, Inc. | 965,541 | 57,932 |

| IndyMac Bancorp, Inc. | 1,286,505 | 52,953 |

| ^Corus Bankshares Inc. | 1,251,628 | 27,986 |

| MGIC Investment Corp. | 448,164 | 26,876 |

| Downey Financial Corp. | 240,600 | 16,010 |

| The PMI Group Inc. | 228,800 | 10,024 |

* | ^First Federal Financial Corp. | 169,900 | 9,637 |

| PFF Bancorp, Inc. | 117,600 | 4,356 |

| WSFS Financial Corp. | 45,550 | 2,833 |

* | Triad Guaranty, Inc. | 48,300 | 2,472 |

| First Financial Holdings, Inc. | 63,953 | 2,188 |

| Anchor Bancorp | | |

| Wisconsin Inc. | 76,545 | 2,186 |

| BankUnited Financial Corp. | 54,000 | 1,408 |

| TierOne Corp. | 41,201 | 1,398 |

| City Bank Lynnwood (WA) | 14,873 | 699 |

* | Accredited Home Lenders | | |

| Holding Co. | 13,000 | 467 |

* | Ocwen Financial Corp. | 31,000 | 462 |

| ITLA Capital Corp. | 4,130 | 222 |

| United Community | | |

| Financial Corp. | 14,500 | 179 |

| | | 1,490,849 |

15

| | | Market |

| | | Value• |

| | Shares | ($000) |

Health Care (10.3%) | | |

| AmerisourceBergen Corp. | 1,540,157 | 69,615 |

* | Barr Pharmaceuticals Inc. | 1,109,200 | 57,612 |

* | Sierra Health Services, Inc. | 1,122,900 | 42,491 |

* | Community Health | | |

| Systems, Inc. | 991,399 | 37,029 |

* | Laboratory Corp. of | | |

| America Holdings | 467,764 | 30,671 |

* | Triad Hospitals, Inc. | 692,475 | 30,490 |

* | Haemonetics Corp. | 604,499 | 28,291 |

* | ICOS Corp. | 1,084,483 | 27,177 |

* | Pediatrix Medical | | |

| Group, Inc. | 521,300 | 23,771 |

* | Sciele Pharma, Inc. | 1,235,890 | 23,284 |

| Valeant Pharmaceuticals | | |

| International | 1,077,600 | 21,315 |

| Mylan Laboratories, Inc. | 1,054,214 | 21,221 |

| Manor Care, Inc. | 403,800 | 21,111 |

* | Alkermes, Inc. | 1,132,975 | 17,958 |

* | King Pharmaceuticals, Inc. | 821,900 | 13,997 |

* | ImClone Systems, Inc. | 451,400 | 12,784 |

* | IDEXX Laboratories Corp. | 125,348 | 11,424 |

* | Myriad Genetics, Inc. | 459,107 | 11,317 |

* | Kinetic Concepts, Inc. | 326,200 | 10,262 |

* | Apria Healthcare Group Inc. | 514,600 | 10,158 |

* | The TriZetto Group, Inc. | 638,688 | 9,670 |

* | Advanced Medical | | |

| Optics, Inc. | 242,694 | 9,599 |

* | Applera Corp.–Celera | | |

| Genomics Group | 679,500 | 9,459 |

* | Illumina, Inc. | 286,100 | 9,453 |

* | Adams Respiratory | | |

| Therapeutics, Inc. | 251,358 | 9,197 |

* | Viasys Healthcare Inc. | 305,200 | 8,314 |

* | LifePoint Hospitals, Inc. | 210,900 | 7,449 |

| Medicis | | |

| Pharmaceutical Corp. | 216,700 | 7,010 |

* | ^Enzon Pharmaceuticals, Inc. | 842,300 | 6,949 |

* | Magellan Health | | |

| Services, Inc. | 131,903 | 5,619 |

* | Lincare Holdings, Inc. | 162,096 | 5,615 |

| Dade Behring Holdings Inc. | 137,726 | 5,531 |

* | Techne Corp. | 108,521 | 5,519 |

* | Zoll Medical Corp. | 147,267 | 5,285 |

| Universal Health Services | | |

| Class B | 84,900 | 5,088 |

| Chemed Corp. | 147,800 | 4,768 |

* | ^New River | | |

| Pharmaceuticals Inc. | 172,838 | 4,447 |

* | ^Palomar Medical | | |

| Technologies, Inc. | 99,057 | 4,180 |

* | Sunrise Senior Living, Inc. | 138,300 | 4,131 |

* | SonoSite, Inc. | 124,018 | 3,522 |

| Perrigo Co. | 190,400 | 3,231 |

| IMS Health, Inc. | 120,900 | 3,221 |

* | Kindred Healthcare, Inc. | 101,290 | 3,011 |

* | Molecular Devices Corp. | 157,669 | 2,915 |

* | K-V Pharmaceutical Co. | | |

| Class A | 118,700 | 2,813 |

| Hillenbrand Industries, Inc. | 48,000 | 2,735 |

* | PAREXEL International Corp. | 75,650 | 2,503 |

| Owens & Minor, Inc. | | |

| Holding Co. | 73,400 | 2,414 |

* | Bio-Rad Laboratories, Inc. | | |

| Class A | 27,500 | 1,945 |

* | ICU Medical, Inc. | 38,800 | 1,765 |

* | Progenics | | |

| Pharmaceuticals, Inc. | 74,063 | 1,738 |

* | ^Telik, Inc. | 88,200 | 1,569 |

* | Radiation Therapy | | |

| Services, Inc. | 51,900 | 1,517 |

| Alpharma, Inc. Class A | 64,100 | 1,499 |

* | PSS World Medical, Inc. | 64,400 | 1,287 |

| Datascope Corp. | 38,271 | 1,281 |

* | Symmetry Medical Inc. | 81,900 | 1,236 |

* | Bruker BioSciences Corp. | 168,026 | 1,178 |

* | Tanox, Inc. | 94,526 | 1,117 |

* | VCA Antech, Inc. | 26,300 | 948 |

| Vital Signs, Inc. | 15,855 | 898 |

* | Greatbatch, Inc. | 29,478 | 667 |

* | Odyssey Healthcare, Inc. | 42,022 | 596 |

* | AMN Healthcare Services, Inc. | 13,900 | 330 |

* | Lexicon Genetics Inc. | 46,670 | 176 |

* | IntraLase Corp. | 8,073 | 159 |

* | AmSurg Corp. | 7,020 | 156 |

| Young Innovations, Inc. | 3,400 | 122 |

* | Alliance Imaging, Inc. | 5,200 | 41 |

* | SurModics, Inc. | 474 | 17 |

| | | 695,868 |

Industrials (12.9%) | | |

| Parker Hannifin Corp. | 883,494 | 68,674 |

| Cummins Inc. | 520,900 | 62,107 |

| Manpower Inc. | 899,275 | 55,099 |

| CSX Corp. | 1,583,914 | 52,000 |

* | ^USG Corp. | 912,400 | 42,919 |

| Precision Castparts Corp. | 618,691 | 39,077 |

| The Timken Co. | 1,060,800 | 31,591 |

* | AMR Corp. | 1,253,151 | 28,998 |

| JLG Industries, Inc. | 1,383,400 | 27,405 |

| Trinity Industries, Inc. | 814,640 | 26,207 |

| A.O. Smith Corp. | 574,600 | 22,656 |

| Ryder System, Inc. | 435,300 | 22,496 |

* | EMCOR Group, Inc. | 367,700 | 20,165 |

| John H. Harland Co. | 501,300 | 18,272 |

| R.R. Donnelley & Sons Co. | 519,520 | 17,123 |

* | Monster Worldwide Inc. | 466,458 | 16,881 |

| Steelcase Inc. | 1,074,100 | 16,853 |

| Con-way, Inc. | 364,600 | 16,341 |

* | Navistar International Corp. | 580,374 | 14,985 |

| Adesa, Inc. | 621,300 | 14,358 |

* | PHH Corp. | 453,400 | 12,423 |

16

| | | Market |

| | | Value• |

| | Shares | ($000) |

| Applied Industrial | | |

| Technology, Inc. | 474,975 | 11,589 |

| Universal Forest | | |

| Products, Inc. | 221,249 | 10,852 |

* | Allied Waste Industries, Inc. | 836,688 | 9,429 |

* | NCI Building Systems, Inc. | 161,000 | 9,365 |

* | McDermott International, Inc. | 223,250 | 9,332 |

| Lincoln Electric Holdings, Inc. | 152,011 | 8,277 |

* | Alaska Air Group, Inc. | 206,900 | 7,870 |

| Lennox International Inc. | 313,200 | 7,172 |

* | Dollar Thrifty Automotive | | |

| Group, Inc. | 150,900 | 6,726 |

| Freightcar America Inc. | 126,087 | 6,683 |

| Kennametal, Inc. | 117,600 | 6,662 |

* | United Rentals, Inc. | 276,400 | 6,426 |

* | Labor Ready, Inc. | 403,000 | 6,420 |

| Watsco, Inc. | 131,500 | 6,050 |

* | EnPro Industries, Inc. | 185,300 | 5,570 |

* | Foster Wheeler Ltd. | 137,900 | 5,322 |

| Aramark Corp. Class B | 161,400 | 5,304 |

| Belden CDT Inc. | 125,500 | 4,798 |

| Harsco Corp. | 60,000 | 4,659 |

* | Consolidated Graphics, Inc. | 77,400 | 4,657 |

| Watson Wyatt & | | |

| Co. Holdings | 111,700 | 4,571 |

| Apogee Enterprises, Inc. | 297,558 | 4,526 |

| ElkCorp | 165,289 | 4,488 |

* | General Cable Corp. | 112,500 | 4,299 |

* | US Airways Group Inc. | 94,800 | 4,203 |

| Acuity Brands, Inc. | 91,300 | 4,145 |

| IKON Office Solutions, Inc. | 307,400 | 4,131 |

| Republic Services, Inc. | | |

| Class A | 100,869 | 4,056 |

* | ^Encore Wire Corp. | 112,000 | 3,952 |

| Herman Miller, Inc. | 114,500 | 3,917 |

* | Amerco, Inc. | 47,500 | 3,522 |

* | Corrections Corp. of America | 79,950 | 3,458 |

* | Mobile Mini, Inc. | 110,956 | 3,152 |

* | Builders FirstSource, Inc. | 198,048 | 3,016 |

| McGrath RentCorp | 115,213 | 2,949 |

* | Volt Information Sciences Inc. | 77,400 | 2,752 |

| Arkansas Best Corp. | 58,640 | 2,523 |

| Crane Co. | 60,200 | 2,516 |

| The Manitowoc Co., Inc. | 55,090 | 2,467 |

* | Spherion Corp. | 342,600 | 2,450 |

| The Toro Co. | 52,600 | 2,218 |

* | Genlyte Group, Inc. | 28,216 | 2,009 |

| Barnes Group, Inc. | 106,000 | 1,861 |

* | American Commercial | | |

| Lines Inc. | 28,200 | 1,677 |

| Kelly Services, Inc. Class A | 60,846 | 1,668 |

| Cintas Corp. | 40,000 | 1,633 |

| Regal-Beloit Corp. | 36,700 | 1,596 |

| Triumph Group, Inc. | 37,600 | 1,592 |

* | Cenveo Inc. | 79,900 | 1,504 |

* | West Corp. | 29,257 | 1,413 |

| Mueller Industries Inc. | 38,600 | 1,358 |

* | ABX Air, Inc. | 190,210 | 1,069 |

* | Continental Airlines, Inc. | | |

| Class B | 37,000 | 1,047 |

| Viad Corp. | 28,350 | 1,004 |

| Joy Global Inc. | 26,601 | 1,000 |

| NACCO Industries, Inc. | | |

| Class A | 7,100 | 965 |

* | Kforce Inc. | 70,679 | 843 |

| Carlisle Co., Inc. | 9,102 | 765 |

| Ennis, Inc. | 34,500 | 747 |

* | CBIZ Inc. | 100,600 | 734 |

| Bluelinx Holdings Inc. | 76,300 | 726 |

* | Accuride Corp. | 65,900 | 726 |

* | Terex Corp. | 15,500 | 701 |

| Kaydon Corp. | 18,400 | 681 |

| ^Simpson Manufacturing Co. | 20,900 | 565 |

| Albany International Corp. | 17,700 | 563 |

* | Swift Transportation Co., Inc. | 20,000 | 474 |

* | Thomas & Betts Corp. | 5,400 | 258 |

* | K&F Industries Holdings | 13,700 | 257 |

| Tennant Co. | 8,200 | 200 |

| Kaman Corp. Class A | 9,157 | 165 |

| | | 872,905 |

Information Technology (14.8%) | |

* | Fiserv, Inc. | 1,451,583 | 68,355 |

* | Computer Sciences Corp. | 1,103,200 | 54,189 |

* | RealNetworks, Inc. | 3,841,698 | 40,760 |

| National | | |

| Semiconductor Corp. | 1,457,700 | 34,300 |

* | LAM Research Corp. | 677,498 | 30,711 |

| Anixter International Inc. | 496,000 | 28,009 |

* | Arris Group Inc. | 2,388,551 | 27,373 |

* | Alliance Data Systems Corp. | 483,900 | 26,706 |

| Harris Corp. | 563,000 | 25,048 |

* | CSG Systems | | |

| International, Inc. | 932,678 | 24,651 |

* | Silicon Image, Inc. | 1,861,047 | 23,673 |

* | Micron Technology, Inc. | 1,359,842 | 23,661 |

* | Lexmark International, Inc. | 404,500 | 23,323 |

* | Palm, Inc. | 1,491,514 | 21,716 |

| Seagate Technology | 900,800 | 20,799 |

* | Transaction Systems | | |

| Architects, Inc. | 553,191 | 18,986 |

* | Ceridian Corp. | 828,239 | 18,519 |

* | CommScope, Inc. | 506,000 | 16,627 |

* | Global Imaging Systems, Inc. | 720,354 | 15,898 |

* | j2 Global | | |

| Communications, Inc. | 566,567 | 15,394 |

* | ^Genesis Microchip Inc. | 1,264,948 | 14,888 |

* | Coherent, Inc. | 380,398 | 13,185 |

* | Zoran Corp. | 794,750 | 12,780 |

* | Freescale | | |

| Semiconductor, Inc. | | |

| Class A | 314,800 | 11,978 |

17

| | | Market |

| | | Value• |

| | Shares | ($000) |

* | Arrow Electronics, Inc. | 432,900 | 11,874 |

* | Western Digital Corp. | 613,800 | 11,110 |

* | Informatica Corp. | 813,856 | 11,060 |

* | EarthLink, Inc. | 1,505,369 | 10,944 |

* | Interdigital | | |

| Communications Corp. | 306,943 | 10,467 |

* | ^Finisar Corp. | 2,882,941 | 10,465 |

* | MicroStrategy Inc. | 96,819 | 9,859 |

* | MEMC Electronic | | |

| Materials, Inc. | 262,800 | 9,626 |

* | Cadence Design | | |

| Systems, Inc. | 547,400 | 9,284 |

* | ^Komag, Inc. | 282,700 | 9,035 |

* | Brocade Communications | | |

| Systems, Inc. | 1,278,943 | 9,029 |

* | Benchmark Electronics, Inc. | 335,175 | 9,010 |

* | Sybase, Inc. | 361,785 | 8,770 |

| MTS Systems Corp. | 260,926 | 8,438 |

* | ON Semiconductor Corp. | 1,411,400 | 8,299 |

* | Nuance | | |

| Communications, Inc. | 1,008,299 | 8,238 |

* | Fairchild Semiconductor | | |

| International, Inc. | 437,400 | 8,179 |

* | UTStarcom, Inc. | 910,889 | 8,080 |

* | DST Systems, Inc. | 130,400 | 8,042 |

* | MPS Group, Inc. | 520,104 | 7,859 |

| Imation Corp. | 173,500 | 6,966 |

| Molex, Inc. | 175,062 | 6,822 |

* | ^Atheros Communications | 347,735 | 6,304 |

* | Vishay Intertechnology, Inc. | 420,900 | 5,909 |

* | Advanced Energy | | |

| Industries, Inc. | 326,357 | 5,561 |

* | MKS Instruments, Inc. | 273,450 | 5,554 |

* | Novellus Systems, Inc. | 193,700 | 5,358 |

* | Freescale | | |

| Semiconductor, Inc. | | |

| Class B | 137,600 | 5,230 |

| Park Electrochemical Corp. | 160,000 | 5,069 |

* | Progress Software Corp. | 193,524 | 5,032 |

* | Plexus Corp. | 248,700 | 4,775 |

* | Cirrus Logic, Inc. | 654,946 | 4,775 |

* | LTX Corp. | 928,444 | 4,652 |

* | ManTech International Corp. | 134,000 | 4,423 |

* | Avnet, Inc. | 223,400 | 4,383 |

* | Paxar Corp. | 218,700 | 4,370 |

* | Perot Systems Corp. | 306,700 | 4,229 |

| Fidelity National Information | | |

| Services, Inc. | 113,100 | 4,185 |

| Reynolds & Reynolds Class A | 105,657 | 4,175 |

* | Rofin-Sinar Technologies Inc. | 67,202 | 4,084 |

* | Tellabs, Inc. | 367,842 | 4,032 |

* | Hyperion Solutions Corp. | 116,100 | 4,003 |

* | Photronics Inc. | 282,463 | 3,991 |

| MoneyGram | | |

| International, Inc. | 135,200 | 3,929 |

* | Sykes Enterprises, Inc. | 188,400 | 3,834 |

* | Cymer, Inc. | 83,702 | 3,675 |

* | Conexant Systems, Inc. | 1,783,466 | 3,567 |

* | Dolby Laboratories Inc. | 175,400 | 3,482 |

| AVX Corp. | 191,800 | 3,393 |

* | Teradyne, Inc. | 250,300 | 3,294 |

* | Euronet Worldwide, Inc. | 132,291 | 3,248 |

| Technitrol, Inc. | 98,400 | 2,937 |

* | OmniVision Technologies, Inc. | 197,300 | 2,815 |

| Bel Fuse, Inc. Class B | 87,218 | 2,799 |

* | BMC Software, Inc. | 94,836 | 2,581 |

| Fair Isaac, Inc. | 66,500 | 2,432 |

* | Amkor Technology, Inc. | 467,000 | 2,410 |

* | SPSS, Inc. | 95,243 | 2,374 |

* | Trident Microsystems, Inc. | 99,490 | 2,314 |

| United Online, Inc. | 188,768 | 2,299 |

| CTS Corp. | 165,300 | 2,278 |

* | Macrovision Corp. | 95,400 | 2,260 |

* | Veeco Instruments, Inc. | 111,908 | 2,255 |

* | LSI Logic Corp. | 271,100 | 2,228 |

* | Agere Systems Inc. | 149,000 | 2,225 |

* | Avocent Corp. | 69,300 | 2,087 |

* | Interwoven Inc. | 183,314 | 2,022 |

* | Aeroflex, Inc. | 194,300 | 1,997 |

| Jack Henry & Associates Inc. | 80,400 | 1,750 |

* | BearingPoint, Inc. | 207,200 | 1,629 |

* | Cabot Microelectronics Corp. | 53,299 | 1,536 |

* | eFunds Corp. | 59,800 | 1,446 |

* | Silicon Storage | | |

| Technology, Inc. | 328,653 | 1,354 |

* | Ciber, Inc. | 200,700 | 1,331 |

* | TTM Technologies, Inc. | 109,600 | 1,282 |

| Black Box Corp. | 29,682 | 1,155 |

* | Mattson Technology, Inc. | 129,324 | 1,073 |

* | MRO Software Inc. | 37,600 | 965 |

* | Insight Enterprises, Inc. | 45,000 | 927 |

* | DTS Inc. | 38,452 | 814 |

* | Asyst Technologies, Inc. | 107,016 | 723 |

| Methode Electronics, Inc. | | |

| Class A | 64,000 | 609 |

* | Rogers Corp. | 9,400 | 580 |

* | SYNNEX Corp. | 20,100 | 463 |

* | MICROS Systems, Inc. | 9,000 | 440 |

* | DealerTrack Holdings Inc. | 19,304 | 427 |

* | eSPEED, Inc. Class A | 38,816 | 357 |

* | Vignette Corp. | 25,600 | 347 |

| Agilysys, Inc. | 21,700 | 305 |

* | Tyler Technologies, Inc. | 19,300 | 250 |

* | IXYS Corp. | 25,841 | 217 |

* | Kopin Corp. | 49,116 | 165 |

* | Keane, Inc. | 10,100 | 146 |

* | Digital Insight Corp. | 4,210 | 123 |

| infoUSA Inc. | 1,500 | 12 |

| | | 1,002,240 |

18

| | | Market |

| | | Value• |

| | Shares | ($000) |

Materials (4.8%) | | |

| Freeport-McMoRan | | |

| Copper & Gold, Inc. | | |

| Class B | 1,202,500 | 64,045 |

| Eagle Materials, Inc. | 1,420,175 | 47,832 |

| Reliance Steel & | | |

| Aluminum Co. | 1,282,000 | 41,203 |

| Nucor Corp. | 672,900 | 33,302 |

| Phelps Dodge Corp. | 231,308 | 19,592 |

| Martin Marietta | | |

| Materials, Inc. | 228,900 | 19,370 |

| Temple-Inland Inc. | 471,362 | 18,902 |

| Greif Inc. Class A | 212,500 | 17,023 |

| Louisiana-Pacific Corp. | 705,300 | 13,239 |

| United States Steel Corp. | 228,300 | 13,168 |

| Commercial Metals Co. | 392,600 | 7,982 |

| Celanese Corp. Series A | 343,200 | 6,143 |

| Lubrizol Corp. | 107,700 | 4,925 |

| Quanex Corp. | 144,400 | 4,383 |

| ^Cleveland-Cliffs Inc. | 93,200 | 3,552 |

| Steel Dynamics, Inc. | 55,532 | 2,802 |

| Sonoco Products Co. | 73,000 | 2,456 |

| Metal Management, Inc. | 62,700 | 1,746 |

| Silgan Holdings, Inc. | 37,205 | 1,397 |

| Gibraltar Industries Inc. | 62,289 | 1,382 |

* | Pactiv Corp. | 29,700 | 844 |

| H.B. Fuller Co. | 27,800 | 652 |

| | | 325,940 |

Telecommunication Services (2.4%) | |

* | Qwest Communications | | |

| International Inc. | 6,444,100 | 56,193 |

| Citizens | | |

| Communications Co. | 1,639,602 | 23,020 |

| Embarq Corp. | 441,500 | 21,355 |

* | Leap Wireless | | |

| International, Inc. | 310,474 | 15,055 |

* | Cincinnati Bell Inc. | 2,623,900 | 12,647 |

| Telephone & | | |

| Data Systems, Inc. | 273,045 | 11,495 |

| CenturyTel, Inc. | 108,600 | 4,308 |

* | Premiere Global | | |

| Services, Inc. | 308,958 | 2,682 |

| Windstream Corp. | 198,766 | 2,622 |

| North Pittsburgh | | |

| Systems, Inc. | 70,142 | 1,765 |

* | U.S. Cellular Corp. | 26,800 | 1,600 |

| Commonwealth Telephone | | |

| Enterprises, Inc. | 35,832 | 1,477 |

* | Syniverse Holdings Inc. | 96,800 | 1,452 |

* | General Communication, Inc. | 58,900 | 730 |

* | Broadwing Corp. | 36,500 | 461 |

| Centennial | | |

| Communications Corp. | | |

| Class A | 55,100 | 294 |

* | Covad Communications | | |

| Group, Inc. | 183,900 | 274 |

* | American Tower Corp. | | |

| Class A | 6,900 | 252 |

| Surewest Communications | 9,600 | 187 |

| Consolidated Communications | | |

| Holdings, Inc. | 9,353 | 175 |

| Iowa Telecommunications | | |

| Services Inc. | 4,100 | 81 |

* | Cbeyond Inc. | 2,500 | 69 |

| | | 158,194 |

Utilities (5.7%) | | |

| CenterPoint Energy Inc. | 2,259,449 | 32,355 |

| Xcel Energy, Inc. | 1,455,745 | 30,061 |

| Energen Corp. | 705,172 | 29,526 |

* | Allegheny Energy, Inc. | 701,000 | 28,159 |

| DTE Energy Co. | 604,015 | 25,073 |

| Pepco Holdings, Inc. | 948,405 | 22,923 |

| ONEOK, Inc. | 540,039 | 20,408 |

| Cleco Corp. | 597,075 | 15,070 |

| Pinnacle West Capital Corp. | 331,568 | 14,937 |

| Westar Energy, Inc. | 606,200 | 14,252 |

| Wisconsin Energy Corp. | 311,861 | 13,454 |

| Edison International | 321,000 | 13,366 |

| FirstEnergy Corp. | 234,300 | 13,088 |

| Avista Corp. | 384,100 | 9,096 |

| Southwest Gas Corp. | 268,800 | 8,956 |

* | NRG Energy, Inc. | 191,900 | 8,693 |

| Puget Energy, Inc. | 366,300 | 8,326 |

| OGE Energy Corp. | 202,300 | 7,305 |

| NSTAR | 200,100 | 6,675 |

* | CMS Energy Corp. | 429,700 | 6,205 |

| Energy East Corp. | 247,700 | 5,875 |

| MDU Resources Group, Inc. | 260,050 | 5,810 |

| PNM Resources Inc. | 153,700 | 4,238 |

| Hawaiian Electric | | |

| Industries Inc. | 140,200 | 3,794 |

| Nicor Inc. | 85,400 | 3,652 |

| TECO Energy, Inc. | 224,725 | 3,517 |

| Vectren Corp. | 127,900 | 3,434 |

| IDACORP, Inc. | 84,096 | 3,180 |

| WGL Holdings Inc. | 90,800 | 2,846 |

* | AES Corp. | 126,100 | 2,571 |

| Black Hills Corp. | 76,200 | 2,561 |

| ALLETE, Inc. | 54,835 | 2,383 |

| Northwest Natural Gas Co. | 58,600 | 2,302 |

| Otter Tail Corp. | 75,675 | 2,213 |

| Great Plains Energy, Inc. | 60,130 | 1,865 |

| Empire District Electric Co. | 74,208 | 1,661 |

* | El Paso Electric Co. | 70,900 | 1,584 |

| American Electric | | |

| Power Co., Inc. | 33,380 | 1,214 |

| UGI Corp. Holding Co. | 35,500 | 868 |

| MGE Energy, Inc. | 4,800 | 155 |

| | | 383,651 |

Total Common Stocks | | |

(Cost $6,018,498) | | 6,755,637 |

19

| | Market |

| | Value• |

| Shares | ($000) |

Temporary Cash Investments (1.6%)1 | |

Money Market Fund (1.6%) | | |

2 Vanguard Market Liquidity | |

Fund, 5.306%—Note E | 103,910,400 | 103,910 |

| | |

| Face | |

| Amount | |

| ($000) | |

U.S. Agency Obligation (0.0%) | |

3 Federal Home Loan | | |

Mortgage Corp. | | |

4 5.150%, 12/26/06 | 2,000 | 1,976 |

Total Temporary Cash Investments | |

(Cost $105,886) | | 105,886 |

Total Investments (101.6%) | | |

(Cost $6,124,384) | | 6,861,523 |

Other Assets and Liabilities (–1.6%) | |

Other Assets—Note B | | 65,461 |

Liabilities—Note E | | (171,939) |

| | (106,478) |

Net Assets (100%) | | |

Applicable to 292,827,049 outstanding $.001 |

par value shares of beneficial interest | |

(unlimited authorization) | | 6,755,045 |

Net Asset Value Per Share | | $23.07 |

At September 30, 2006, net assets consisted of:5 |

| Amount | Per |

| ($000) | Share |

Paid-in Capital | 5,706,514 | $19.49 |

Undistributed Net | | |

Investment Income | 45,366 | .15 |

Accumulated Net | | |

Realized Gains | 266,009 | .91 |

Unrealized Appreciation | | |

Investment Securities | 737,139 | 2.52 |

Futures Contracts | 17 | — |

Net Assets | 6,755,045 | $23.07 |

| • | See Note A in Notes to Financial Statements. |

| * | Non-income-producing security. |

| ^ | Part of security position is on loan to broker-dealers. See Note E in Notes to Financial Statements. |

| 1 | The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 100.0% and 1.6%, respectively, of net assets. See Note C in Notes to Financial Statements. |

| 2 | Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield. |

| 3 | The issuer operates under a congressional charter; its securities are neither issued nor guaranteed by the U.S. government. If needed, access to additional funding from the U.S. Treasury (beyond the issuer’s line of credit) would require congressional action. |

| 4 | Securities with a value of $1,976,000 have been segregated as initial margin for open futures contracts. |

| 5 | See Note C in Notes to Financial Statements for the tax-basis components of net assets. |

20

Statement of Operations

| Year Ended |

| September 30, 2006 |

| ($000) |

Investment Income | |

Income | |

Dividends | 94,066 |

Interest1 | 824 |

Security Lending | 2,262 |

Total Income | 97,152 |

Expenses | |

The Vanguard Group—Note B | |

Investment Advisory Services | 1,244 |

Management and Administrative | 19,159 |

Marketing and Distribution | 1,559 |

Custodian Fees | 177 |

Auditing Fees | 21 |

Shareholders’ Reports | 167 |

Trustees’ Fees and Expenses | 7 |

Total Expenses | 22,334 |

Net Investment Income | 74,818 |

Realized Net Gain (Loss) | |

Investment Securities Sold | 332,108 |

Futures Contracts | (382) |

Realized Net Gain (Loss) | 331,726 |

Change in Unrealized Appreciation (Depreciation) | |

Investment Securities | (51,964) |

Futures Contracts | 23 |

Change in Unrealized Appreciation (Depreciation) | (51,941) |

Net Increase (Decrease) in Net Assets Resulting from Operations | 354,603 |

1 | Interest income from an affiliated company of the fund was $727,000. |

21

Statement of Changes in Net Assets

| Year Ended September 30, |

| 2006 | 2005 |

| ($000) | ($000) |

Increase (Decrease) in Net Assets | | |

Operations | | |

Net Investment Income | 74,818 | 40,401 |

Realized Net Gain (Loss) | 331,726 | 356,210 |

Change in Unrealized Appreciation (Depreciation) | (51,941) | 442,538 |

Net Increase (Decrease) in Net Assets Resulting from Operations | 354,603 | 839,149 |

Distributions | | |

Net Investment Income | (49,617) | (22,893) |

Realized Capital Gain1 | (340,229) | (156,981) |

Total Distributions | (389,846) | (179,874) |

Capital Share Transactions—Note F | | |

Issued | 2,273,341 | 1,959,945 |

Issued in Lieu of Cash Distributions | 365,856 | 168,947 |

Redeemed | (1,031,900) | (558,509) |

Net Increase (Decrease) from Capital Share Transactions | 1,607,297 | 1,570,383 |

Total Increase (Decrease) | 1,572,054 | 2,229,658 |

Net Assets | | |

Beginning of Period | 5,182,991 | 2,953,333 |

End of Period2 | 6,755,045 | 5,182,991 |

| 1 | Includes fiscal 2006 and 2005 short-term gain distributions totaling $92,145,000 and $37,610,000, respectively. Short-term gain distributions are treated as ordinary income dividends for tax purposes. |

| 2 | Net Assets—End of Period includes undistributed net investment income of $45,366,000 and $27,314,000. |

22

Financial Highlights

| | | Nov. 1, | | | |

| Year Ended | 2003, to | |

For a Share Outstanding | September 30, | Sept. 30, | Year Ended October 31, |

Throughout Each Period | 2006 | 2005 | 20041 | 2003 | 2002 | 2001 |

Net Asset Value, | | | | | | |

Beginning of Period | $23.28 | $19.70 | $17.85 | $13.01 | $13.68 | $18.07 |

Investment Operations | | | | | | |

Net Investment Income | .27 | .19 | .13 | .13 | .14 | .16 |

Net Realized and Unrealized | | | | | | |

Gain (Loss) on Investments | 1.17 | 4.49 | 1.85 | 4.84 | (.67) | (1.31) |

Total from | | | | | | |

Investment Operations | 1.44 | 4.68 | 1.98 | 4.97 | (.53) | (1.15) |

Distributions | | | | | | |

Dividends from | | | | | | |

Net Investment Income | (.21) | (.14) | (.13) | (.13) | (.14) | (.21) |

Distributions from | | | | | | |

Realized Capital Gains | (1.44) | (.96) | — | — | — | (3.03) |

Total Distributions | (1.65) | (1.10) | (.13) | (.13) | (.14) | (3.24) |

Net Asset Value, | | | | | | |

End of Period | $23.07 | $23.28 | $19.70 | $17.85 | $13.01 | $13.68 |

| | | | | | |

Total Return2 | 6.49% | 24.32% | 11.14% | 38.55% | –4.02% | –6.48% |

| | | | | | |

Ratios/Supplemental Data | | | | | | |

Net Assets, | | | | | | |

End of Period (Millions) | $6,755 | $5,183 | $2,953 | $1,714 | $876 | $767 |

Ratio of Total Expenses to | | | | | | |

Average Net Assets | 0.35% | 0.40% | 0.45%* | 0.50% | 0.50% | 0.54% |

Ratio of Net Investment | | | | | | |

Income to Average Net Assets | 1.18% | 0.99% | 0.83%* | 1.04% | 0.94% | 1.06% |

Portfolio Turnover Rate | 80% | 75% | 66% | 100% | 73% | 82% |

1 | The fund’s fiscal year-end changed from October 31 to September 30, effective September 30, 2004. |

2 | Total returns do not reflect the 1% fee assessed through April 6, 2001, on redemptions of shares held in the fund for less than five years. |

See accompanying Notes, which are an integral part of the Financial Statements.

23

Notes to Financial Statements

Vanguard Strategic Equity Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund files reports with the SEC under the company name Vanguard Horizon Funds.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4:00 p.m. Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Accordingly, no provision for federal income taxes is required in the financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents the income earned on investing cash collateral, less expenses associated with the loan.

6. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions

received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

24

B. The Vanguard Group furnishes at cost investment advisory, corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At September 30, 2006, the fund had contributed capital of $709,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.71% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

C. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

The fund used a tax accounting practice to treat a portion of the price of capital shares redeemed during the year as distributions from net investment income and realized capital gains. Accordingly, the fund has reclassified $7,149,000 from undistributed net investment income, and $30,701,000 from accumulated net realized gains, to paid-in capital.

For tax purposes, at September 30, 2006, the fund had $67,363,000 of ordinary income and $250,390,000 of long-term capital gains available for distribution.

At September 30, 2006, the cost of investment securities for tax purposes was $6,124,531,000. Net unrealized appreciation of investment securities for tax purposes was $736,992,000, consisting of unrealized gains of $972,659,000 on securities that had risen in value since their purchase and $235,667,000 in unrealized losses on securities that had fallen in value since their purchase.

At September 30, 2006, the aggregate settlement value of open futures contracts expiring in December 2006 and the related unrealized appreciation (depreciation) were:

| | ($000) |

| | Aggregate | Unrealized |

| Number of | Settlement | Appreciation |

Futures Contracts | Long Contracts | Value | (Depreciation) |

S&P 500 Index | 2 | 673 | 17 |