As filed with the Securities and Exchange Commission on September 2, 2016.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09114

The Needham Funds, Inc.

(Exact name of registrant as specified in charter)

445 Park Avenue, New York, NY 10022-2606

(Address of principal executive offices) (Zip code)

Mr. George A. Needham, 445 Park Avenue, New York, NY 10022-2606

(Name and address of agent for service)

1-800-625-7071

Registrant’s telephone number, including area code

Date of fiscal year end: December 31, 2016

Date of reporting period: June 30, 2016

Item 1. Reports to Stockholders.

445 Park Avenue

New York, New York 10022-2606

1-800-625-7071

www.needhamfunds.com

Semi-Annual Report

June 30, 2016

Contents

| 1 |

| Portfolio Characteristics | |

| 7 |

| 8 |

| 9 |

| 10 |

| Schedule of Investments | |

| 11 |

| 14 |

| 17 |

| Schedule of Securities Sold Short | |

| 13 |

| 16 |

| 18 |

| 19 |

| 20 |

| 21 |

| Financial Highlights | |

| 22 |

| 23 |

| 24 |

| 25 |

| 30 |

This report is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus. The prospectus contains more complete information, including investment objectives, risks, expenses and charges and should be read carefully before investing or sending any money. To obtain a prospectus, please call 1-800-625-7071.

Portfolios of The Needham Funds, Inc., like all mutual funds:

The Needham Funds, Inc. are distributed by Needham & Company, LLC.

| 445 Park Avenue

New York, NY 10022

(800) 625-7071

www.needhamfunds.com |

August 2016

Dear Shareholders, Friends of Needham and Prospective Shareholders,

We are pleased to report results for the second quarter and first half of 2016 for the Needham Growth Fund, Needham Aggressive Growth Fund, and Needham Small Cap Growth Fund. Our mission is to create wealth for long-term investors.

Needham Funds’ Second Quarter and Semiannual Review

In the second quarter, the Needham Growth Fund (NEEGX) returned 0.61%, the Needham Aggressive Growth Fund (NEAGX) lost 0.80%, and the Needham Small Cap Growth Fund (NESGX) returned 0.90%. The Russell 2000 Total Return Index returned 3.79%, the S&P 500 Total Return Index returned 2.46%, and the NASDAQ Composite Index declined 0.22%.

For the half-year, the Needham Growth Fund returned 0.88%, the Needham Aggressive Growth Fund returned 1.43%, and the Needham Small Cap Growth Fund outperformed and returned 8.44%. The Russell 2000 Total Return Index returned 2.22%, the S&P 500 Total Return Index returned 3.84%, and the NASDAQ Composite Index declined 2.61%.

First Half 2016: Fears Overcome

Our theme for the first half of 2016 is “Fears Overcome.” 2016 started with an unprecedented sell-off amidst fear of a stock market crash, devaluation in China, and a slowing world economy. Energy companies and their bankers were hurt as West Texas Intermediate oil hit a low of $26.21, down from $37.04 at year end. The oil industry was hurt by a slowing world economy and fears of extra supply coming on-line from Iran.

In late January, Japan announced a surprise interest rate cut, which placed rates at -0.1% for financial firms with deposits at the Bank of Japan. In late January, we learned that 4Q15 GDP growth was just 0.7%. At the low in mid-February, the Russell 2000 was down 16% and the S&P 500 was down 11%. On February 10, Janet Yellen reiterated to Congress the Federal Reserve’s cautious stance in raising interest rates and wouldn’t take negative rates off the table. On February 11, The Guardian called the bottom and wrote, “Global stocks enter bear market after another rout.”(1) This was followed a few days later by Russia, Saudi Arabia, Venezuela and Qatar announcing an oil production cutback, which at the time appeared to have teeth. Oil closed the first quarter at $40 per barrel. The rebound was aided by the weak dollar, which fell 4.5% versus the DXY index, a basket of currencies. All three Needham Funds outperformed during the sell-off and trailed the averages on the rebound.

In the second quarter, the markets continued to overcome fear. In April, we learned that first quarter GDP growth was just 0.5%. The employment report for April showed just 160,000 jobs added. April ended with the markets down seven days in a row, including a big down day to close the month. Apple, Google and Microsoft reported disappointing first quarter earnings, and the Bank of Japan surprised by not easing further. The yen appreciated 5% vs. the dollar on one day. Japan instituted negative interest rates in January. Much more easing is hard to imagine.

Nonetheless, in mid-May, the Federal Reserve minutes read, “It likely would be appropriate to raise rates in June if the economy shows clear signs of a rebound.”(2) The report for May showed a disastrous 32,000 jobs created. Just a few weeks later, Barron’s wrote an article titled, “Watching for a Market Crash.”(3)

| (1) | https://www.theguardian.com/business/live/2016/feb/11/market-turmoil-hong-kong-europe-ftse-banks-yellen-live |

| (2) | http://www.nytimes.com/2016/05/19/business/economy/federal-reserve-interest-rates-meeting-minutes.html?_r=0 |

| (3) | http://www.barrons.com/video/barrons-buzz-watching-for-a-market-crash/781305DB-0706-4D4B-B87C- |

Needless to say, a June interest rate hike seemed off the table.

While the market overcame the previous fears, Brexit was the unanticipated monster. On June 22, the people of the United Kingdom unexpectedly voted to leave the European Union and turmoil filled the markets... for all of two days. The CBOE Market Volatility Index spiked 49%. The S&P 500 fell 5.3%. By July 8, the S&P 500 had regained these losses. The one lasting impact may be that the devalued pound, which fell 10% in those 2 days to $1.315, will be good for companies with more expenses than revenues in the U.K.

To top it off, we had fears of terrorism from attacks in Brussels, Orlando, and Nice, to name a few. Finally, we had the unusual circumstances of two Presidential primary elections more befitting of reality TV shows.

Again, we see no hope for a growth-oriented domestic policy built on an internationally competitive corporate tax regime, lower regulatory and policy barriers to private sector hiring, lower marginal tax rates, and a lower rate of increase of government spending. At best, we believe the economy will muddle along.

These continuing fears make us continue to believe that monetary policy will remain accommodative across the world. The market has climbed a wall of worry that we believe will return with the slightest of market drawdowns.

Even the much-publicized Brexit came to near no impact on the markets. As our investors know, we believe our time is better spent researching companies than worrying about most macro factors, over which we have no control. We continue to see opportunity in our small and mid-cap universe.

Why Small Caps and Why Now?

| 1. | Small caps complement other equity and fixed income positions, which can lead to lower correlation and positive risk-adjusted returns. Professor Harry Markowitz of the University of Chicago posited this thesis and won the 1990 Nobel Prize for his Modern Portfolio Theory.(4) |

| 2. | Over time, small caps can outperform. Eugene S. Fama (University of Chicago, Nobel Prize 2013) and Kenneth R. French (Tuck School of Business, Dartmouth) compared the performance of the average small-cap value stock to the average large-cap growth stock and found that the small caps outperformed by 2.4% per year since 1926. |

| 3. | “You pay a very high price in the stock market for a cheery consensus” was the headline of an article written for Forbes by Warren Buffett in 1974 in the midst of the market crash. It was republished on November 9, 2008.(5) The macro-environment seems chaotic, but then doesn’t it always? |

| 4. | Small caps have lagged the S&P 500 for the last year. The Russell 2000 has underperformed the S&P 500 by about 8% for the year starting May 31, 2015. Mean reversion alone would suggest outperformance relative to the S&P 500. |

| 5. | The Needham Funds and small caps can provide growth at attractive valuations. As shown in Table 1, the Needham Funds have lower average valuations than the indices, with the exception of NEAGX having a slightly higher multiple to sales than the Russell 2000. NEAGX and NEEGX have superior cash flow growth relative to their benchmark indices. They also have superior sales growth compared to the S&P 500. |

Table 1: Superior Growth at Attractive Valuations

(* Forward-looking based on historical data as of 6/30/16. Source: Morningstar.)

| | | | Price/Book* | | Price/Sales* | | Price/Cash Flow* | | Sales Growth | | Cash Flow Growth |

| NEEGX | | | | 2.22 | | | | 1.13 | | | | 4.99 | | | | 5.79 | % | | | 17.19 | % |

| NEAGX | | | | 2.28 | | | | 1.44 | | | | 4.79 | | | | 9.23 | % | | | 19.26 | % |

| S&P 500 | | | | 2.57 | | | | 1.80 | | | | 10.04 | | | | 1.54 | % | | | 1.39 | % |

| Russell 2000 | | | | 1.69 | | | | 1.03 | | | | 6.46 | | | | (0.25 | )% | | | 3.90 | % |

| (4) | A well diversified portfolio is still subject to various risks, including but not limited to investment risk, which could result in a loss of principal. |

| (5) | http://www.forbes.com/2008/11/08/buffett-forbes-article-markets-cx_pm-1107stocks.html |

| 6. | Advice from Warren Buffett, Charlie Munger and Philip Fisher: |

| a. | Pay little attention to the macro. “If you find yourself discussing and debating...STOP.”(6) |

| b. | “Does the company have products or services with sufficient market potential to make possible a sizable increase in sales for at least several years?”(7) |

| c. | “Hold a small piece of an outstanding business with the same tenacity that an owner would exhibit if he owned all of that business.”(8) |

Second Quarter and First Half Contributors Across All Three Needham Funds

For the second quarter, the leading contributor across the Needham Funds was FormFactor, Inc. (FORM), which closed its accretive acquisition of Cascade Microtech, Inc. (formerly CSCD) and returned 24%. Cascade makes wafer probe cards for the radio frequency semiconductor market and will further diversify FormFactor’s business away from the DRAM memory market. The acquisition is estimated to increase FormFactor’s 2017 earnings per share by 25%. The market gave little credit for this acquisition until a month before closing. Since the bottom on May 19, Form Factor’s stock is up 59% as of August 9.

Amber Road, Inc. (AMBR), which returned 43%, was another leading contributor across all three Needham Funds. Amber Road had a difficult year in 2015, as it struggled to get major customers up and running. The company’s new Quick Start program contributed to improved results in the first quarter and an improved outlook for 2016.

In the first half of 2016, the leading contributors were Newport Corporation (formerly NEWP), which returned 45% on its takeover by MKS Instruments (MKSI), which will diversify MKS’s product line and markets. Newport sells photonics, lasers and optics products and systems to scientific research, microelectronics, security, life and health sciences, and industrial markets. MKS was also a leading contributor, returning 21%, as it sees an opportunity to improve Newport’s margins through manufacturing and other efficiencies. Amber Road returned 52% during the first half and PDF Solutions (PDFS) returned 29%. In January at the Needham Growth Conference, PDF Solutions discussed its new product, Design For Inspection. We believe Design For Inspection has the potential to double the size of PDF’s available market.

Second Quarter and First Half Detractors Across All Three Needham Funds

In the second quarter 2016, the leading detractors were Super Micro Computer, Inc. (SMCI), down 27%, and KVH Industries, down 19%. In mid-April, Super Micro preannounced a revenue shortfall from its large data center customers. KVH supplies communications services, equipment and media content to the maritime industry. Segments of the maritime industry are suffering due to the oil and gas exploration slowdown, slowing international trade, and overcapacity in shipping; KVH has suffered along with these customers. Nonetheless, we believe it is an undervalued stock.

For the first half of 2016, the leading detractors in the Funds were KVH Industries, down 18%, and Photronics (PLAB), down 28%. Photronics makes photomasks, which are used on new designs by semiconductor manufacturers. Photronics saw a pause in spending as its logic and memory customers prepare for their next generation of technology.

Needham Growth Fund

The Needham Growth Fund returned 0.61% in the second quarter ending June 30, 2016 and returned 0.88% in the first six months of 2016.

During the second quarter, FormFactor was the top contributor followed by Amber Road. Express Scripts Holding Corporation (ESRX), the second largest holding of the Fund, returned 10% as it filed a counterclaim to the lawsuit filed against it by Anthem, Inc. (ANTM). Anthem sued Express Scripts in an attempt to extract better commercial terms. Express Scripts purchased Anthem’s pharmacy benefit management business in 2009 and the two entered into a supply agreement. We believe Express Scripts’ counterclaim places the dispute in the proper perspective and the stock market agreed.

A number of NEEGX’s other large-cap, long-term holdings were top second quarter contributors. The Fund’s largest holding at 8.3% of net assets, Thermo Fisher Scientific, Inc. (TMO), returned 4%; other positions contributing included Hess Corporation (HES), up 14%, Medtronic Plc. (MDT), up 16%, and Comcast Corporation Class A (CMCSA), up 7%.

| (6) | Robert Hagstron, Jr., The Warren Buffett Way: Investment Strategies of the World’s Greatest Investor (1995). |

| (7) | Philip Fisher, Common Stocks and Uncommon Profits (2003). |

| (8) | Berkshire Hathaway, Annual Report, 1993. |

In the second quarter, Super Micro Computer and KVH Industries were the largest detractors.

For the first half of 2016, the leading contributors were Newport Corporation, up 45%, and Amber Road, up 52%. ViaSat, Inc. (VSAT) returned 17% and was the third-leading contributor. ViaSat announced additional details about its next-generation ViaSat-3 ultra-high-bandwidth satellites.

The Fund’s leading detractor for the half-year was Express Scripts, down 13%, followed by Gilead Sciences, Inc. (GILD), down 17%. Gilead manufactures and sells market-leading AIDS/HIV and hepatitis C drugs, and the company’s stock price declined over concerns regarding maturity of the hepatitis C drug market.

During the second quarter, Needham Growth Fund added three new positions, all equities already held by the other Needham Funds. Apple, Inc. (AAPL) was purchased on its price drop after the March quarter results. With its loyal customer base, high return on equity, and trading at 8x earnings, after deducting cash, we are believers in Apple. We were recently asked about the fates of Nokia, Motorola, and Blackberry Limited (BB-Canada) as examples of what could happen to Apple. We believe Apple has a culture of innovation, a software and services business, and loyal customers, which will prevent its commoditization.

The Fund also added Vicor Corporation (VICR). Vicor has worked with Alphabet Inc.’s Google (GOOGL) on its Open Compute data centers to distribute DC (direct current) power throughout the data center rather than go through the inefficient conversions to AC (alternating current) and back again to DC.

In the first quarter, the Needham Growth Fund reduced its long-time successful position in Becton Dickinson (BDX) by almost 20% to manage position size. We trimmed other top holdings, including Thermo Fisher Scientific, Express Scripts, Gilead, and ViaSat. In the first quarter, the Fund also reduced its long-time position in Honeywell International, Inc. (HON) due to valuation.

In the second quarter, the Fund exited its long-time positions in Electro Scientific Industries, Inc. (ESIO) and Newport Corporation, through its acquisition by MKS Instruments.

Needham Growth Fund had an Active Share of 103.9% vs. the S&P 500 TR Index, and trailing 12-month turnover of just 9%. Active share is a measure of the differentiation of the holdings of a portfolio from the holdings of its appropriate passive benchmark index. Active Share is calculated by taking the sum of the absolute value of the differences of the weight of each holding in the manager’s portfolio versus the weight of each holding in the benchmark index and dividing by two. It is possible for funds that hold short positions to have an Active Share of over 100%.

On June 30, 2016, the Fund had 54% of net assets in the top 10 positions. 51% of Needham Growth Fund’s net assets were invested in companies with market capitalizations of over $8 billion, 20% between $2 billion and $8 billion, and 29% under $2 billion. During the second quarter, long-time holdings Entegris (ENTG), Electronics for Imaging (EFII), MKS Instruments (MKSI) and WageWorks, Inc. (WAGE) crossed above the $2 billion market cap level. The Fund had a 5% short position and 4% in cash.

Needham Aggressive Growth Fund

The Needham Aggressive Growth Fund lost 0.80% in the second quarter ending June 30, 2016 and returned 1.43% in the first six months of 2016.

In the second quarter, FormFactor, Amber Road and FEI Company (FEIC) were the leading contributors. FEI announced its acquisition by Thermo Fisher Scientific on May 27. FEI’s science and biotech product lines could benefit from the combination, while the quarterly volatility of the semiconductor and other industrial businesses will no longer be significant due to Thermo Fisher’s size.

Another top contributor in the second quarter was WageWorks (WAGE), which returned 18% with a strong quarter and expansion of their business managing the flexible spending accounts for the U.S. Office of Personnel Management, the largest employer in the United States. This partnership will provide nearly 1.8 million eligible employees access to WageWorks’ proprietary platform to manage healthcare and dependent care spending.

In the second quarter, the leading detractors were Super Micro Computer and FormFactor. GSE Systems, Inc. (GVP), down 18%, was the third detractor due to selling pressure on the stock. We added 215,000 shares to the portfolio in the second quarter.

For the half-year, PDF Solutions, Inc. returned 29% and was the top contributor. On May 24, PDF announced its new Design For Inspection solution along with the first two customer orders. These orders were not expected for another two or three quarters. PDF also has growth opportunities to provide its yield ramping software and services to the growing Chinese semiconductor manufacturing market and its Exsensio big-data analytics solution to a range of fabless and fab customers. Amber Road was the second-leading contributor, and WageWorks, which returned 32%, was the third.

The first half 2016 leading detractors were FormFactor and Medallion Financial (MFIN, formerly known as TAXI). Medallion Financial, a short position of NEAGX, originates, acquires and services loans that finance taxicab medallions. The stock was up 35%, from $7 to over $9 per share, and cost the Fund in the first quarter. However, loan delinquencies accelerated, taxicab medallions continued to lose value, and the market ignored the data. As we write this letter in early August, Medallion Financial announced on August 2 a cut to its dividend to $0.05 per share from $0.25 per share; the stock is down over 25% and trading under $6. We believe a number of Medallion’s assets, most obviously its Chicago medallions, are worth far less than reported on the company’s balance sheet.

During the first half of 2016, we added to several positions, including Amber Road, IPG Photonics (IPGP), KVH Industries, PDF Solutions and Vicor Corp. We also reduced positions, including TheStreet, Inc. (TST), Hess Corp., FEI Company, Financial Engines (FNGN), Oil-Dri Corporation of America (ODI), and Photronics (PLAB). In the second quarter, we exited small positions in GSV Capital Corp (GSVC), Newport Corporation, Barracuda Networks (CUDA), Panera Bread Co. (PNRA), and FedEx (FDX).

The Fund had an Active Share of 114.3% versus the Russell 2000 and a trailing 12-month turnover of 12%.

Needham Aggressive Growth Fund exited the quarter with 43% of assets in companies over $2 billion in market cap, up from 31% last quarter. Like the Needham Growth Fund, four of the portfolio’s long-term positions crossed the bar to over $2 billion. The Fund remained concentrated with the top 10 positions at 54% of net assets. The Fund had an 8% short position and was once again fully invested.

Needham Small Cap Growth Fund

The Needham Small Growth Fund returned 0.90% in the second quarter and 8.44% in the first half of 2016, while the Russell 2000 Total Return Index returned 3.79% in the second quarter and 2.22% in the first half of 2016.

The Fund saw the completion of the acquisition of Newport Corp. (NEWP) to MKS Instruments (MKSI), and we saw a significant cash increase due partly to this deal closing. Ruckus Wireless (RKUS) agreed to sell itself to Brocade Communications (BRCD) for a slight premium and, as a result, we sold the position.

Semiconductor capital equipment was a highlight in the second quarter for the Fund, and we expect to see continued strength from the industry in the second half of 2016 and into 2017. The summer 2015 delays that significantly impacted the Fund’s performance last year are now flowing through many of our investments in the sector. Ultra Clean Holdings (UCTT), NESGX’s second-largest holding, is strongly leveraged to this cycle and ramp of increased capital intensity in the fabrication of semiconductors. Although the long-time Chief Financial Officer, Casey Eichler, decided to leave the company at the end of July, we believe he leaves the company at a time when fundamentals are very strong.

Our investment in Amber Road recovered nicely in the quarter. Amber Road provides cloud-based global trade management solutions. After a substantial correction in 2015 and early in 2016, we added significantly to the position. The cash burn was largely reduced, removing the overhang of a potential equity offering that the market feared. We believe the company is now on firm ground and is able to continue to pursue its long-term financial goals.

We are very pleased with the performance of Needham Small Cap Growth Fund in the first half of the year; many of our long-term holdings performed nicely as their fundamental stories delivered results. Although January and early February was a difficult start to the year, we were able to make valuable investments during this period, which ultimately recovered from their lows. Our investments in the semiconductor capital equipment industry saw greater visibility after a disappointing second half of 2015. We also benefited from an increased trend in consolidation of small cap stocks. Global central banks continued to provide accommodative monetary support to risk assets and this helped the markets to recover. We also saw a recovery in the energy markets that helped to boost the high yield markets off their lows. This recovery provided a tailwind to small cap stocks in the first half, as high yield investment opportunities trade less like equity investments as they trade closer to par. We continued to balance the Fund as our concentrated top ideas achieved price targets and a higher percentage of the Fund.

Closing

The second quarter saw a nice return in the equity markets, as global Central Banks continued to offer accommodative monetary policy, and this continued investor appetite for risk assets. We saw an increase in negative interest rates around the world, which pressured U.S. interest rates lower. The fundamental economic growth story remained slow but the consistency of the growth allowed companies to recover from the significant sell-off in the early months of the year.

The suspense of the Brexit vote in the United Kingdom escalated throughout the quarter and the final decision to leave the EU was a surprise to the markets. The initial negative impact of the Brexit vote on the markets turned out to be short-lived, and during it, we were able to acquire some new additions to our portfolios. While the long-term implications of leaving the EU are not completely known at this time, the markets recovered quite quickly as the actual leave will not occur for at least two years. We expect some companies to expose risk to the Brexit decision but the U.S. markets, in general, are large and strong enough to work through these risks.

We believe the U.S. is still facing sub-par economic growth, but it remains the best place in the world to be investing and working. Asia and Europe are facing difficult economic times. We believe there is opportunity in small and mid-cap stocks in this difficult market. We are particularly excited that this market may give us a chance to add to positions already in the portfolio.

We see opportunity in our strategy of investing in companies that we know well and that we believe are positioned with secular growth drivers. We believe the remainder of 2016 will bring a modest rebound for equities. As it already has this year, we believe the markets will experience more volatility and that our ability to short could dampen the possible volatility.

To reiterate our overall thesis: monetary policy remains accommodative. Most importantly, we see a revolution happening in technology that has created and continues to create investment opportunities.

We welcome our new investors and thank all of our investors for their continued support. If you have any questions, thoughts or concerns, please contact us at (800) 625-7071 or send us an email at cretzler@needhamco.com or jbarr@needhamco.com. For information about the funds, please visit our website at www.needhamfunds.com.

| Sincerely, | |

| | |

|  |

| | |

| Chris Retzler | John O. Barr |

| Portfolio Manager | Portfolio Manager |

| | Semi-Annual Report 2016 |

| | |

| TICKER: NEEGX |

Comparative Performance Statistics as of June 30, 2016 (Unaudited)

| | | | | | | | | | | | | | | | | | | | | | |

| | | 6 Months(7) | | 1 Year | | 3 Years(8) | | 5 Years(8) | | 10 Years(8) | | Since

Inception(8)(12) | | Gross Expense

Ratio(14) |

Needham Growth Fund(1) | | 0.88 | % | | -7.48 | % | | 6.30 | %(9) | | 6.33 | %(10) | | 6.22 | %(11) | | 12.68 | %(13) | | 2.07 | % |

S&P 500 Index(2)(3) | | 3.84 | % | | 3.99 | % | | 11.66 | % | | 12.10 | % | | 7.42 | % | | 8.18 | % | | | |

NASDAQ Composite Index(2)(4) | | -2.61 | % | | -1.58 | % | | 13.95 | % | | 13.29 | % | | 9.57 | % | | 8.64 | % | | | |

S&P 400 MidCap Index(2)(5) | | 7.93 | % | | 1.33 | % | | 10.53 | % | | 10.55 | % | | 8.55 | % | | 11.35 | % | | | |

Russell 2000 Index(2)(6) | | 2.22 | % | | -6.73 | % | | 7.09 | % | | 8.35 | % | | 6.20 | % | | 7.94 | % | | | |

Past performance does not guarantee future results. The performance data quoted represents past performance, and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, please call 1-800-625-7071. The returns shown in the above table and accompanying footnotes are net of expenses. The table above does not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

| 1. | Investment results calculated after reinvestment of dividends. |

| 2. | It is not possible to invest directly in an index. The performance of the index does not include the deduction of expenses associated with a mutual fund, such as investment management fees. |

| 3. | The S&P 500 Index is a broad unmanaged measure of the U.S. stock market. |

| 4. | The NASDAQ Composite Index is a broad-based capitalization-weighted index of all NASDAQ Global Market and Small Cap stocks. |

| 5. | The S&P 400 MidCap Index is a broad unmanaged measure of the U.S. stock market. |

| 6. | The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. |

| 8. | Compound annual growth rate (annualized return). Assumes all dividends were reinvested in shares of the Fund. |

| 9. | Cumulative return for the three year period was 20.11%, assuming all dividends were reinvested in shares of the Fund. |

| 10. | Cumulative return for the five year period was 35.92%, assuming all dividends were reinvested in shares of the Fund. |

| 11. | Cumulative return for the ten year period was 82.79%, assuming all dividends were reinvested in shares of the Fund. |

| 12. | The inception date of the Fund was 1/1/96. |

| 13. | Cumulative return since inception was 1,054.52%, assuming all dividends were reinvested in shares of the Fund. |

| 14. | Gross expense ratio is from the Fund’s prospectus dated May 1, 2016. Additional information pertaining to the Fund’s expense ratios as of June 30, 2016 can be found in the financial highlights. Since January 1, 2009, the investment performance reflects contractually agreed upon fee waivers which expire at the close of business on April 30, 2017. Without these fee waivers, the performance would have been lower. Excluding the indirect costs of investing in acquired funds, total fund operating expenses would be 2.05%. |

Top Ten Holdings*

(as a % of total investments, as of June 30, 2016)

| | | | Security | | | | | % of Total

Investments† | |

| 1 | | Thermo Fisher Scientific, Inc. | | TMO | | 8.69% | | |

| 2 | | Express Scripts Holding Co. | | ESRX | | 8.65% | | |

| 3 | | Gilead Sciences, Inc. | | GILD | | 6.86% | | |

| 4 | | ViaSat, Inc. | | VSAT | | 5.52% | | |

| 5 | | Becton Dickinson and Co. | | BDX | | 5.32% | | |

| 6 | | CarMax, Inc. | | KMX | | 4.86% | | |

| 7 | | FormFactor, Inc. | | FORM | | 4.77% | | |

| 8 | | Super Micro Computer, Inc. | | SMCI | | 4.23% | | |

| 9 | | KVH Industries, Inc. | | KVHI | | 3.58% | | |

| 10 | | Comcast Corp. | | CMCSA | | 3.46% | | |

Top Ten Holdings = 55.94% of Total Investments†

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| † | Percentage of total investments less cash. |

Sector Weightings*

(as a % of total investments, as of June 30, 2016)

| | Sector | | | Long(1) | | (Short)(1) | | Total(1)(2) |

| Consumer Discretionary | | 10.3 | % | | — | | | 10.3 | % |

| Energy | | 3.2 | % | | — | | | 3.2 | % |

| Exchange Traded Funds | | — | | | (0.3 | )% | | (0.3 | )% |

| Financials | | 2.8 | % | | (0.8 | )% | | 2.0 | % |

| Health Care | | 35.5 | % | | — | | | 35.5 | % |

| Industrials | | 3.1 | % | | — | | | 3.1 | % |

| Information Technology | | 46.1 | % | | (3.7 | )% | | 42.4 | % |

| Cash | | 3.8 | % | | — | | | 3.8 | % |

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| (1) | Percentage of total investments includes all stocks, plus cash minus all short positions. |

| (2) | Total represents the difference between the long exposure and the short exposure, which produces the net exposure. |

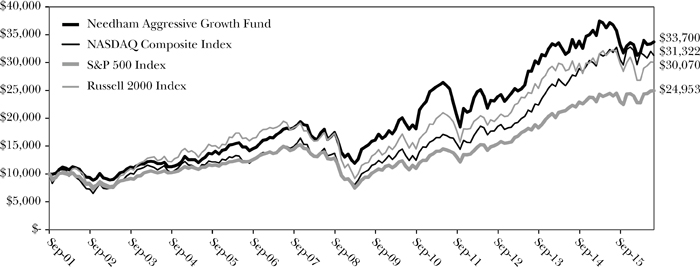

Comparison of Change in Value of a $10,000 Investment

Past performance does not guarantee future results. The performance data quoted represents past performance, and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, please call 1-800-625-7071. The graph above does not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Since inception, the Fund’s adviser has absorbed certain expenses of the Fund, without which returns would have been lower.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

| Needham Funds | |

| | |

NEEDHAM AGGRESSIVE G ROWTH FUND | TICKER: NEAGX |

| Comparative Performance Statistics as of June 30, 2016 (Unaudited) |

| | | 6 Months(6) | | 1 Year | | 3 Years(7) | | 5 Years(7) | | 10 Years(7) | | Since

Inception(7)(11) | | Gross Expense

Ratio(13) |

Needham Aggressive Growth Fund(1) | | 1.43 | % | | -8.29 | % | | 5.81 | %(8) | | 5.96 | %(9) | | 8.56 | %(10) | | 8.54 | %(12) | | 2.43 | % |

S&P 500 Index(2)(3) | | 3.84 | % | | 3.99 | % | | 11.66 | % | | 12.10 | % | | 7.42 | % | | 6.36 | % | | | |

NASDAQ Composite Index(2)(4) | | -2.61 | % | | -1.58 | % | | 13.95 | % | | 13.29 | % | | 9.57 | % | | 8.00 | % | | | |

Russell 2000 Index(2)(5) | | 2.22 | % | | -6.73 | % | | 7.09 | % | | 8.35 | % | | 6.20 | % | | 7.71 | % | | | |

Past performance does not guarantee future results. The performance data quoted represents past performance, and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, please call 1-800-625-7071. The returns shown in the above table and accompanying footnotes are net of expenses. The table above does not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

| 1. | Investment results calculated after reinvestment of dividends. |

| 2. | It is not possible to invest directly in an index. The performance of the index does not include the deduction of expenses associated with a mutual fund, such as investment management fees. |

| 3. | The S&P 500 Index is a broad unmanaged measure of the U.S. stock market. |

| 4. | The NASDAQ Composite Index is a broad-based capitalization-weighted index of all NASDAQ Global Market and Small Cap stocks. |

| 5. | The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. |

| 7. | Compound annual growth rate (annualized return). Assumes all dividends were reinvested in shares of the Fund. |

| 8. | Cumulative return for the three year period was 18.46%, assuming all dividends were reinvested in shares of the Fund. |

| 9. | Cumulative return for the five year period was 33.60%, assuming all dividends were reinvested in shares of the Fund. |

| 10. | Cumulative return for the ten year period was 127.27%, assuming all dividends were reinvested in shares of the Fund. |

| 11. | The inception date of the Fund was 9/4/2001. |

| 12. | Cumulative return since inception was 237.00% assuming all dividends were reinvested in shares of the Fund. |

| 13. | Gross expense ratio is from the Fund’s prospectus dated May 1, 2016. Additional information pertaining to the Fund’s expense ratios as of June 30, 2016 can be found in the financial highlights. Since January 1, 2009, the investment performance reflects contractually agreed upon fee waivers which expire at the close of business on April 30, 2017. Without these fee waivers, the performance would have been lower. Excluding the indirect costs of investing in acquired funds, total fund operating expenses would be 2.41%. |

Top Ten Holdings*

(as a % of total investments, as of June 30, 2016)

| | | | Security | | | | | % of Total

Investments† | |

| 1 | | Akamai Technologies, Inc. | | AKAM | | 7.60% | | |

| 2 | | PDF Solutions, Inc. | | PDFS | | 7.41% | | |

| 3 | | FormFactor, Inc. | | FORM | | 6.20% | | |

| 4 | | Entegris, Inc. | | ENTG | | 5.96% | | |

| 5 | | KVH Industries, Inc. | | KVHI | | 4.96% | | |

| 6 | | Reis, Inc. | | REIS | | 4.94% | | |

| 7 | | Apple, Inc. | | AAPL | | 4.67% | | |

| 8 | | Super Micro Computer, Inc. | | SMCI | | 4.37% | | |

| 9 | | GSE Systems, Inc. | | GVP | | 4.02% | | |

| 10 | | Gilead Sciences, Inc. | | GILD | | 3.95% | | |

Top Ten Holdings = 54.08% of Total Investments†

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| † | Percentage of total investments less cash. |

Sector Weightings*

(as a % of total investments, as of June 30, 2016)

| | Sector | | | Long(1) | | (Short)(1) | | Total(1)(2) |

| Consumer Discretionary | | 4.0 | % | | — | | | 4.0 | % |

| Consumer Staples | | 2.0 | % | | — | | | 2.0 | % |

| Energy | | 0.5 | % | | — | | | 0.5 | % |

| Financials | | 5.1 | % | | (2.7 | )% | | 2.4 | % |

| Health Care | | 10.6 | % | | — | | | 10.6 | % |

| Industrials | | 6.4 | % | | — | | | 6.4 | % |

| Information Technology | | 79.4 | % | | (5.3 | )% | | 74.1 | % |

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| (1) | Percentage of total investments includes all stocks, plus cash minus all short positions. |

| (2) | Total represents the difference between the long exposure and the short exposure, which produces the net exposure. |

Comparison of Change in Value of a $10,000 Investment

Past performance does not guarantee future results. The performance data quoted represents past performance, and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, please call 1-800-625-7071. The graph above does not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Since inception, the Fund’s adviser has absorbed certain expenses of the Fund, without which returns would have been lower.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

| | Semi-Annual Report 2016 |

| | |

NEEDHAM SMALL CAP GROWTH FUND | TICKER: NESGX |

| Comparative Performance Statistics as of June 30, 2016 (Unaudited) |

| | | 6 Months(6) | | 1 Year | | 3 Years(7) | | 5 Years(7) | | 10 Years(7) | | Since

Inception(7)(11) | | Gross Expense

Ratio(13) |

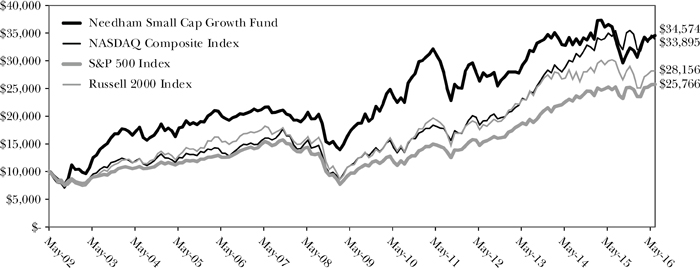

Needham Small Cap Growth Fund(1) | | 8.44 | % | | -4.42 | % | | 4.73 | %(8) | | 2.94 | %(9) | | 5.85 | %(10) | | 9.19 | %(12) | | 2.05 | % |

S&P 500 Index(2)(3) | | 3.84 | % | | 3.99 | % | | 11.66 | % | | 12.10 | % | | 7.42 | % | | 6.94 | % | | | |

NASDAQ Composite Index(2)(4) | | -2.61 | % | | -1.58 | % | | 13.95 | % | | 13.29 | % | | 9.57 | % | | 9.03 | % | | | |

Russell 2000 Index(2)(5) | | 2.22 | % | | -6.73 | % | | 7.09 | % | | 8.35 | % | | 6.20 | % | | 7.61 | % | | | |

Past performance does not guarantee future results. The performance data quoted represents past performance, and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, please call 1-800-625-7071. The returns shown in the above table and accompanying footnotes are net of expenses. The table above does not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

| 1. | Investment results calculated after reinvestment of dividends. |

| 2. | It is not possible to invest directly in an index. The performance of the index does not include the deduction of expenses associated with a mutual fund, such as investment management fees. |

| 3. | The S&P 500 Index is a broad unmanaged measure of the U.S. stock market. |

| 4. | The NASDAQ Composite Index is a broad-based capitalization-weighted index of all NASDAQ Global Market and Small Cap stocks. |

| 5. | The Russell 2000 Index is a broad unmanaged index composed of the smallest 2,000 companies in the Russell 3000 Index. |

| 7. | Compound annual growth rate (annualized return). Assumes all dividends were reinvested in shares of the Fund. |

| 8. | Cumulative return for the three year period was 14.87%, assuming all dividends were reinvested in shares of the Fund. |

| 9. | Cumulative return for the five year period was 15.57%, assuming all dividends were reinvested in shares of the Fund. |

| 10. | Cumulative return for the ten year period was 76.51%, assuming all dividends were reinvested in shares of the Fund. |

| 11. | The inception date of the Fund was 5/22/02. |

| 12. | Cumulative return since inception was 245.74% assuming all dividends were reinvested in shares of the Fund. |

| 13. | Gross expense ratio is from the Fund’s prospectus dated May 1, 2016. Additional information pertaining to the Fund’s expense ratios as of June 30, 2016 can be found in the financial highlights. Since January 1, 2009, the investment performance reflects contractually agreed upon fee waivers which expire at the close of business on April 30, 2017. Without these fee waivers, the performance would have been lower. Excluding the indirect costs of investing in acquired funds, total fund operating expenses would be 2.05%. |

Top Ten Holdings*

(as a % of total investments, as of June 30, 2016)

| | | | Security | | | | | % of Total

Investments† | |

| 1 | | Amber Road, Inc. | | AMBR | | 11.35% | | |

| 2 | | Ultra Clean Holdings, Inc. | | UCTT | | 11.32% | | |

| 3 | | TTM Technologies, Inc. | | TTMI | | 8.87% | | |

| 4 | | Silicon Graphics International Corp. | | SGI | | 8.13% | | |

| 5 | | PDF Solutions, Inc. | | PDFS | | 7.89% | | |

| 6 | | FormFactor, Inc. | | FORM | | 6.76% | | |

| 7 | | Frequency Electronics, Inc. | | FEIM | | 6.12% | | |

| 8 | | KVH Industries, Inc. | | KVHI | | 5.88% | | |

| 9 | | Super Micro Computer, Inc. | | SMCI | | 5.06% | | |

| 10 | | Reis, Inc. | | REIS | | 3.59% | | |

Top Ten Holdings = 74.97% of Total Investments†

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| † | Percentage of total investments less cash. |

Sector Weightings*

(as a % of total investments, as of June 30, 2016)

| | Sector | | | Long(1) | | (Short)(1) | | Total(1)(2) |

| Closed End Funds | | 0.2 | % | | — | | | 0.2 | % |

| Energy | | 1.3 | % | | — | | | 1.3 | % |

| Exchange Traded Funds | | — | | | (6.3 | )% | | (6.3 | )% |

| Financials | | 2.1 | % | | — | | | 2.1 | % |

| Health Care | | 2.2 | % | | — | | | 2.2 | % |

| Industrials | | 2.9 | % | | — | | | 2.9 | % |

| Information Technology | | 57.2 | % | | (0.8 | )% | | 56.4 | % |

| Cash | | 41.2 | % | | — | | | 41.2 | % |

| * | Current portfolio holdings may not be indicative of future portfolio holdings. |

| (1) | Percentage of total investments includes all stocks, plus cash minus all short positions. |

| (2) | Total represents the difference between the long exposure and the short exposure, which produces the net exposure. |

Comparison of Change in Value of a $10,000 Investment

Past performance does not guarantee future results. The performance data quoted represents past performance, and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, please call 1-800-625-7071. The graph above does not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Since inception, the Fund’s adviser has absorbed certain expenses of the Fund, without which returns would have been lower.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

Disclosure of Fund Expenses (Unaudite

d)

The following expense table is shown so that you can understand the impact of fees on your investment. All mutual funds have operating expenses. As a shareholder of a Portfolio, you incur transactional costs, including redemption fees and ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports, among others. A Portfolio’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in each Portfolio and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period. The expense example table below illustrates your fund’s cost in two ways:

| ● | Actual Expenses. This section helps you to estimate the actual expenses after fee waivers that you paid over the period. The “Ending Account Value” shown is derived from the Portfolio’s actual return, and “Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Portfolio. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your Portfolio under the heading entitled “Expenses Paid During Period”. |

| ● | Hypothetical Expenses on a 5% Return. This section is intended to help you compare your Portfolio’s costs with those of other mutual funds. It assumes that the Portfolio had a return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Portfolio’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your Portfolio’s cost by comparing this hypothetical example with the hypothetical examples that appear in shareholders reports of other funds. |

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

For the Period January 1, 2016 to June 30, 2016

Expense Example Table

| | | | | | | | | |

| | | Beginning

Account Value

1/1/16 | | Ending

Account Value

6/30/16 | | Expenses Paid

During Period*

1/1/16 – 6/30/16 | | Expense Ratio

During Period*

1/1/16 – 6/30/16 |

| Needham Growth Fund | | | | | | | | |

| Actual Expenses | | $1,000.00 | | $1,008.80 | | $11.34 | | 2.27% |

Hypothetical Example for Comparison Purposes

(5% return before expenses) | | $1,000.00 | | $1,013.58 | | $11.36 | | 2.27% |

| | | | | | | | | |

| Needham Aggressive Growth Fund | | | | | | | | |

| Actual Expenses | | $1,000.00 | | $1,014.30 | | $14.77 | | 2.95% |

Hypothetical Example for Comparison Purposes

(5% return before expenses) | | $1,000.00 | | $1,010.19 | | $14.74 | | 2.95% |

| | | | | | | | | |

| Needham Small Cap Growth Fund | | | | | | | | |

| Actual Expenses | | $1,000.00 | | $1,084.40 | | $10.52 | | 2.03% |

Hypothetical Example for Comparison Purposes

(5% return before expenses) | | $1,000.00 | | $1,014.77 | | $10.17 | | 2.03% |

| * | Expenses are equal to the average account value times the Portfolio’s annualized expense ratio multiplied 182/366 (to reflect the one-half-year period). |

| | | | | | |

| Schedule of Investments | | | | | | |

| June 30, 2016 (Unaudited) | | | | | | |

| | | Shares | | | Market Value | |

| Common Stocks (96.4%) | | | | | | |

| | | | | | | |

| Aerospace & Defense (0.4%) | | | | | | |

| Honeywell International, Inc. | | | 4,500 | | | $ | 523,440 | |

| | | | | | | | | |

| Airlines (0.2%) | | | | | | | | |

| United Continental Holdings, Inc.* | | | 5,000 | | | | 205,200 | |

| | | | | | | | | |

| Auto Components (0.2%) | | | | | | | | |

| Sypris Solutions, Inc.* | | | 213,573 | | | | 181,537 | |

| | | | | | | | | |

| Biotechnology (6.6%) | | | | | | | | |

| Gilead Sciences, Inc.† | | | 93,000 | | | | 7,758,060 | |

| | | | | | | | | |

| Capital Markets (2.3%) | | | | | | | | |

| Financial Engines, Inc.† | | | 60,000 | | | | 1,552,200 | |

| GSV Capital Corp. | | | 47,500 | | | | 238,450 | |

| Oaktree Capital Group LLC | | | 20,000 | | | | 895,200 | |

| | | | | | | | 2,685,850 | |

| | | | | | | | | |

| Communications Equipment (8.8%) | | | | | | | | |

| KVH Industries, Inc.* | | | 526,300 | | | | 4,052,510 | |

| ViaSat, Inc.*† | | | 87,500 | | | | 6,247,500 | |

| | | | | | | | 10,300,010 | |

| | | | | | | | | |

| Electrical Equipment (0.1%) | | | | | | | | |

| Vicor Corp.* | | | 15,000 | | | | 151,050 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (5.5%) | | | | | | | | |

| Corning, Inc. | | | 35,000 | | | | 716,800 | |

| FLIR Systems, Inc. | | | 15,000 | | | | 464,250 | |

| Frequency Electronics, Inc.* | | | 33,247 | | | | 309,197 | |

| IPG Photonics Corp.* | | | 6,000 | | | | 480,000 | |

| Jabil Circuit, Inc.† | | | 150,000 | | | | 2,770,500 | |

| National Instruments Corp. | | | 23,300 | | | | 638,420 | |

| TTM Technologies, Inc.* | | | 36,500 | | | | 274,845 | |

| Vishay Intertechnology, Inc. | | | 62,500 | | | | 774,375 | |

| | | | | | | | 6,428,387 | |

| | | | | | | | | |

| Energy Equipment & Services (0.8%) | | | | | | | | |

| Schlumberger Ltd. | | | 12,500 | | | | 988,500 | |

| | | | | | | | | |

| Health Care Equipment & Supplies (10.0%) | | | | | | | | |

| Analogic Corp. | | | 6,250 | | | | 496,500 | |

| Becton Dickinson and Co. | | | 35,500 | | | | 6,020,445 | |

| CONMED Corp. | | | 30,000 | | | | 1,431,900 | |

| Medtronic PLC | | | 26,290 | | | | 2,281,183 | |

| Varian Medical Systems, Inc.* | | | 19,000 | | | | 1,562,370 | |

| | | | | | | | 11,792,398 | |

| | | | | | | | | |

| Health Care Providers & Services (8.3%) | | | | | | | | |

| Express Scripts Holding Co.*† | | | 129,000 | | | | 9,778,200 | |

| Health Care Technology (0.1%) | | | | | | |

| Castlight Health, Inc.* | | | 20,000 | | | | 79,200 | |

| | | | | | | | | |

| Internet Software & Services (6.5%) | | | | | | | | |

| Akamai Technologies, Inc.*† | | | 56,000 | | | | 3,132,080 | |

| Amber Road, Inc.* | | | 404,800 | | | | 3,121,008 | |

| Q2 Holdings, Inc.* | | | 20,000 | | | | 560,400 | |

| Reis, Inc. | | | 34,500 | | | | 859,050 | |

| | | | | | | | 7,672,538 | |

| | | | | | | | | |

| Life Sciences Tools & Services (8.6%) | | | | | | | | |

| Bruker Corp. | | | 10,000 | | | | 227,400 | |

| Thermo Fisher Scientific, Inc.† | | | 66,500 | | | | 9,826,040 | |

| | | | | | | | 10,053,440 | |

| | | | | | | | | |

| Media (3.8%) | | | | | | | | |

| Comcast Corp. | | | 60,000 | | | | 3,911,400 | |

| Twenty-First Century Fox, Inc. | | | 10,000 | | | | 270,500 | |

| World Wrestling Entertainment, Inc. | | | 12,500 | | | | 230,125 | |

| | | | | | | | 4,412,025 | |

| | | | | | | | | |

| Oil, Gas & Consumable Fuels (2.2%) | | | | | | | | |

| Hess Corp.† | | | 43,000 | | | | 2,584,300 | |

| | | | | | | | | |

| Pharmaceuticals (0.2%) | | | | | | | | |

| Corium International, Inc.* | | | 80,000 | | | | 277,600 | |

| | | | | | | | | |

| Professional Services (1.2%) | | | | | | | | |

| WageWorks, Inc.* | | | 23,500 | | | | 1,405,535 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (15.2%) | | | | | | | | |

| Applied Materials, Inc. | | | 8,000 | | | | 191,760 | |

| Brooks Automation, Inc. | | | 85,000 | | | | 953,700 | |

| Entegris, Inc.* | | | 200,000 | | | | 2,894,000 | |

| FormFactor, Inc.* | | | 600,000 | | | | 5,394,000 | |

| Lam Research Corp. | | | 2,500 | | | | 210,150 | |

| MKS Instruments, Inc. | | | 59,000 | | | | 2,540,540 | |

| Nova Measuring Instruments Ltd.* | | | 130,000 | | | | 1,422,200 | |

| PDF Solutions, Inc.* | | | 212,500 | | | | 2,972,875 | |

| Photronics, Inc.* | | | 130,000 | | | | 1,158,300 | |

| Ultra Clean Holdings, Inc.* | | | 7,700 | | | | 43,813 | |

| | | | | | | | 17,781,338 | |

| | | | | | | | | |

| Software (0.2%) | | | | | | | | |

| Barracuda Networks, Inc.* | | | 13,650 | | | | 206,661 | |

| | | | | | | | | |

| Specialty Retail (5.7%) | | | | | | | | |

| CarMax, Inc.*† | | | 112,000 | | | | 5,491,360 | |

| Dick’s Sporting Goods, Inc. | | | 24,000 | | | | 1,081,440 | |

| Tiffany & Co. | | | 2,500 | | | | 151,600 | |

| | | | | | | | 6,724,400 | |

See accompanying notes to financial statements.

| Needham Growth Fund | | | | | | |

| Schedule of Investments (Continued) | | | | | | |

| June 30, 2016 (Unaudited) | | | | | | |

| | | Shares | | | Market Value | |

| Common Stocks – Continued | | | | | | |

| | | | | | | |

| Technology Hardware, Storage & Peripherals (7.9%) | | | | | | |

| Apple, Inc. | | | 7,500 | | | $ | 717,000 | |

| Electronics For Imaging, Inc.* | | | 64,000 | | | | 2,754,560 | |

| Hutchinson Technology, Inc.* | | | 287,500 | | | | 974,625 | |

| Silicon Graphics International Corp.* | | | 6,325 | | | | 31,815 | |

| Super Micro Computer, Inc.* | | | 192,500 | | | | 4,783,625 | |

| | | | | | | | 9,261,625 | |

| | | | | | | | | |

| Textiles, Apparel & Luxury Goods (0.2%) | | | | | | | | |

| Under Armour, Inc.* | | | 5,018 | | | | 191,971 | |

| | | | | | | | | |

| Thrifts & Mortgage Finance (0.4%) | | | | | | | | |

| Ladder Capital Corp. | | | 36,007 | | | | 439,286 | |

| | | | | | | | | |

| Trading Companies & Distributors (1.0%) | | | | | | | | |

| Air Lease Corp. | | | 45,000 | | | | 1,205,100 | |

| | | | | | | | | |

| Total Common Stocks | | | | | | | | |

| (Cost $55,077,092) | | | | | | $ | 113,087,651 | |

| Short-Term Investments (3.7%) | | | | | | |

| | | | | | | |

| Money Market Fund (3.7%) | | | | | | |

| | | | | | | |

| Dreyfus Treasury Securities Cash Management – Institutional Class 0.16%(a) (Cost $4,314,655) | | | 4,314,655 | | | | 4,314,655 | |

| | | | | | | | | |

| Total Investments (100.1%) | | | | | | | | |

| (Cost $59,391,747) | | | | | | | 117,402,306 | |

| Total Securities Sold Short (-4.5%) (Proceeds $4,585,547) | | | | | | | (5,336,457 | ) |

| Other Assets in Excess of Liabilities (4.4%) | | | | | | | 5,227,741 | |

| Net Assets (100.0%) | | | | | | $ | 117,293,590 | |

| * | Non-income producing security. |

| (a) | Rate shown is the seven day yield as of June 30, 2016. |

| † | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $3,498,100. |

| | The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (‘‘S&P’’). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC. |

See accompanying notes to financial statements.

| | | | | | |

| Schedule of Securities Sold Short | | | | | | |

| June 30, 2016 (Unaudited) | | | | | | |

| | | | | | | |

| | | Shares | | | Market Value | |

| Securities Sold Short (-4.2%) | | | | | | |

| | | | | | | |

| Capital Markets (-0.7%) | | | | | | |

| Medallion Financial Corp. | | | 115,000 | | | $ | 848,700 | |

| | | | | | | | | |

| Communications Equipment (-2.3%) | | | | | | | | |

| Ubiquiti Networks, Inc.* | | | 69,250 | | | | 2,677,205 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (-0.3%) | | | | | | | | |

| Acacia Communications, Inc.* | | | 2,500 | | | | 99,850 | |

| Advanced Energy Industries, Inc.* | | | 3,750 | | | | 142,350 | |

| Applied Micro Circuits Corp.* | | | 15,000 | | | | 96,300 | |

| | | | | | | | 338,500 | |

| | | | | | | | | |

| Software (-0.9%) | | | | | | | | |

| ANSYS, Inc.* | | | 12,500 | | | | 1,134,375 | |

| | | | | | | | | |

| Total Securities Sold Short (-4.2%) | | | | | | | | |

| (Proceeds $4,260,729) | | | | | | | | |

| | | | | | | | 4,998,780 | |

| Exchange Traded Funds Sold Short (-0.3%) | | | | | | | | |

| iShares Russell 2000 ETF | | | 2,000 | | | | 229,940 | |

| VanEck Vectors Semiconductor ETF | | | 1,875 | | | | 107,737 | |

| | | | | | | | | |

| Total Exchange Traded Funds Sold Short | | | | | | | | |

| (Proceeds $324,818) | | | | | | | 337,677 | |

| | | | | | | | | |

| Total Securities & Exchange Traded Funds Sold Short (-4.5%) | | | | | | | | |

| (Proceeds $4,585,547) | | | | | | $ | 5,336,457 | |

| * | Non-income producing security. |

See accompanying notes to financial statements.

Ne

edham Aggressive Growth Fund

Schedule of Investments

June 30, 2016 (Unaudited)

| | | Shares | | | Market Value | |

| Common Stocks (99.6%) | | | | | | |

| | | | | | | |

| Biotechnology (3.9%) | | | | | | |

| Gilead Sciences, Inc.† | | | 23,000 | | | $ | 1,918,660 | |

| | | | | | | | | |

| Capital Markets (1.3%) | | | | | | | | |

| Financial Engines, Inc. | | | 25,000 | | | | 646,750 | |

| | | | | | | | | |

| Commercial Services & Supplies (0.3%) | | | | | | | | |

| Clean Harbors, Inc.* | | | 2,400 | | | | 125,064 | |

| | | | | | | | | |

| Communications Equipment (8.7%) | | | | | | | | |

| KVH Industries, Inc.* | | | 313,100 | | | | 2,410,870 | |

| Norsat International, Inc.* | | | 67,500 | | | | 454,275 | |

| ViaSat, Inc.*† | | | 19,500 | | | | 1,392,300 | |

| | | | | | | | 4,257,445 | |

| | | | | | | | | |

| Diversified Financial Services (0.1%) | | | | | | | | |

| TheStreet, Inc. | | | 45,000 | | | | 50,850 | |

| | | | | | | | | |

| Electrical Equipment (1.5%) | | | | | | | | |

| Vicor Corp.* | | | 72,500 | | | | 730,075 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (4.7%) | | | | | | | | |

| FEI Co.† | | | 6,000 | | | | 641,280 | |

| FLIR Systems, Inc. | | | 8,500 | | | | 263,075 | |

| Frequency Electronics, Inc.* | | | 43,619 | | | | 405,657 | |

| IPG Photonics Corp.* | | | 7,500 | | | | 600,000 | |

| National Instruments Corp. | | | 9,700 | | | | 265,780 | |

| Vishay Precision Group, Inc.* | | | 10,000 | | | | 134,200 | |

| | | | | | | | 2,309,992 | |

| | | | | | | | | |

| Energy Equipment & Services (0.4%) | | | | | | | | |

| Aspen Aerogels, Inc.* | | | 35,200 | | | | 174,944 | |

| | | | | | | | | |

| Health Care Equipment & Supplies (3.3%) | | | | | | | | |

| Analogic Corp. | | | 5,750 | | | | 456,780 | |

| Becton Dickinson and Co. | | | 4,500 | | | | 763,155 | |

| LeMaitre Vascular, Inc. | | | 28,000 | | | | 399,560 | |

| | | | | | | | 1,619,495 | |

| | | | | | | | | |

| Health Care Providers & Services (1.3%) | | | | | | | | |

| Civitas Solutions, Inc.* | | | 7,500 | | | | 156,225 | |

| Express Scripts Holding Co.* | | | 6,000 | | | | 454,800 | |

| | | | | | | | 611,025 | |

| | | | | | | | | |

| Health Care Technology (0.9%) | | | | | | | | |

| Omnicell, Inc.* | | | 13,000 | | | | 444,990 | |

| | | | | | | | | |

| Household Durables (0.3%) | | | | | | | | |

| iRobot Corp.* | | | 4,000 | | | | 140,320 | |

| Household Products (1.9%) | | | | | | |

| Oil-Dri Corp. of America | | | 26,268 | | | | 907,034 | |

| | | | | | | | | |

| Internet Software & Services (16.6%) | | | | | | | | |

| Akamai Technologies, Inc.*† | | | 66,000 | | | | 3,691,380 | |

| Amber Road, Inc.* | | | 172,800 | | | | 1,332,288 | |

| ARI Network Services, Inc.* | | | 15,000 | | | | 63,000 | |

| ChannelAdvisor Corp.* | | | 14,117 | | | | 204,555 | |

| comScore, Inc.* | | | 3,000 | | | | 71,640 | |

| Q2 Holdings, Inc.* | | | 12,500 | | | | 350,250 | |

| Reis, Inc.† | | | 96,500 | | | | 2,402,850 | |

| | | | | | | | 8,115,963 | |

| | | | | | | | | |

| Media (0.2%) | | | | | | | | |

| World Wrestling Entertainment, Inc. | | | 6,000 | | | | 110,460 | |

| | | | | | | | | |

| Oil, Gas & Consumable Fuels (0.1%) | | | | | | | | |

| Hess Corp. | | | 500 | | | | 30,050 | |

| | | | | | | | | |

| Pharmaceuticals (0.3%) | | | | | | | | |

| Corium International, Inc.* | | | 46,050 | | | | 159,794 | |

| | | | | | | | | |

| Professional Services (4.1%) | | | | | | | | |

| CRA International, Inc.* | | | 13,500 | | | | 340,470 | |

| WageWorks, Inc.*† | | | 28,000 | | | | 1,674,680 | |

| | | | | | | | 2,015,150 | |

| | | | | | | | | |

| Real Estate Investment Trusts (REITs) (2.9%) | | | | | | | | |

| Equinix, Inc. | | | 3,593 | | | | 1,393,114 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (26.3%) | | | | | | | | |

| Entegris, Inc.* | | | 200,000 | | | | 2,894,000 | |

| FormFactor, Inc.* | | | 335,000 | | | | 3,011,650 | |

| MKS Instruments, Inc. | | | 27,000 | | | | 1,162,620 | |

| Nova Measuring Instruments Ltd.* | | | 94,900 | | | | 1,038,206 | |

| PDF Solutions, Inc.*† | | | 257,500 | | | | 3,602,425 | |

| Photronics, Inc.* | | | 97,500 | | | | 868,725 | |

| Ultra Clean Holdings, Inc.* | | | 31,425 | | | | 178,808 | |

| Xcerra Corp.* | | | 10,000 | | | | 57,500 | |

| | | | | | | | 12,813,934 | |

| | | | | | | | | |

| Software (5.1%) | | | | | | | | |

| Bottomline Technologies, Inc.* | | | 22,000 | | | | 473,660 | |

| Exa Corp.* | | | 5,000 | | | | 72,250 | |

| GSE Systems, Inc.* | | | 875,000 | | | | 1,951,250 | |

| | | | | | | | 2,497,160 | |

| | | | | | | | | |

| Specialty Retail (3.2%) | | | | | | | | |

| CarMax, Inc.*† | | | 22,500 | | | | 1,103,175 | |

| Dick’s Sporting Goods, Inc. | | | 10,000 | | | | 450,600 | |

| | | | | | | | 1,553,775 | |

See accompanying notes to financial statements.

Needham Aggressive Growth Fund

Schedule of Investments (Continued)

June 30, 2016 (Unaudited)

| | | Shares | | | Market Value | |

| Common Stocks - Continued | | | | | | |

| | | | | | | |

| Technology Hardware, Storage & Peripherals (11.8%) | | | | | | |

| Apple, Inc.† | | | 23,750 | | | $ | 2,270,500 | |

| Electronics For Imaging, Inc.* | | | 16,000 | | | | 688,640 | |

| Hutchinson Technology, Inc.* | | | 162,500 | | | | 550,875 | |

| Silicon Graphics International Corp.* | | | 25,075 | | | | 126,127 | |

| Super Micro Computer, Inc.*† | | | 85,500 | | | | 2,124,675 | |

| | | | | | | | 5,760,817 | |

| | | | | | | | | |

| Thrifts & Mortgage Finance (0.4%) | | | | | | | | |

| Ladder Capital Corp. | | | 16,783 | | | | 204,753 | |

| | | | | | | | | |

Total Common Stocks

(Cost $26,784,990) | | | | | | $ | 48,591,614 | |

| Short-Term Investments (0.0%) | | | | | | |

| | | | | | | |

| Money Market Fund (0.0%) | | | | | | |

| Dreyfus Treasury Securities Cash Management – Institutional Class 0.16%(a) (Cost $1,687) | | | 1,687 | | | | 1,687 | |

| | | | | | | | | |

Total Investments (99.6%)

(Cost $26,786,677) | | | | | | | 48,593,301 | |

Total Securities Sold Short (-7.3%)

(Proceeds $3,046,647) | | | | | | | (3,578,915 | ) |

| Other Assets in Excess of Liabilities (7.7%) | | | | | | | 3,789,645 | |

| Net Assets (100.0%) | | | | | | $ | 48,804,031 | |

| * | Non-income producing security. |

| (a) | Rate shown is the seven day yield as of June 30, 2016. |

| † | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $3,772,700. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (‘‘S&P’’). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

See accompanying notes to financial statements.

N

eedham Aggressive Growth Fund

Schedule of Securities Sold Short

June 30, 2016 (Unaudited)

| | | Shares | | | Market Value | |

| Securities Sold Short (-7.3%) | | | | | | |

| | | | | | | |

| Capital Markets (-1.8%) | | | | | | |

| Medallion Financial Corp. | | | 123,000 | | | $ | 907,740 | |

| | | | | | | | | |

| Communications Equipment (-3.7%) | | | | | | | | |

| Ubiquiti Networks, Inc.* | | | 46,250 | | | | 1,788,025 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (-0.4%) | | | | | | | | |

| Acacia Communications, Inc.* | | | 2,500 | | | | 99,850 | |

| Applied Micro Circuits Corp.* | | | 15,000 | | | | 96,300 | |

| | | | | | | | 196,150 | |

| | | | | | | | | |

| Software (-0.8%) | | | | | | | | |

| ANSYS, Inc.* | | | 4,500 | | | | 408,375 | |

| | | | | | | | | |

| Thrifts & Mortgage Finance (-0.6%) | | | | | | | | |

| Federal Home Loan Mortgage Corp.* | | | 142,500 | | | | 263,625 | |

| Federal National Mortgage Association* | | | 7,500 | | | | 15,000 | |

| | | | | | | | 278,625 | |

| | | | | | | | | |

Total Securities Sold Short (-7.3%)

(Proceeds $3,046,647) | | | | | | $ | 3,578,915 | |

| * | Non-income producing security. |

See accompanying notes to financial statements.

Ne

edham Small Cap Growth Fund

Schedule of Investments

June 30, 2016 (Unaudited)

| | | Shares | | | Market Value | |

| Common Stocks (62.8%) | | | | | | |

| | | | | | | |

| Capital Markets (0.5%) | | | | | | |

| Financial Engines, Inc. | | | 5,000 | | | $ | 129,350 | |

| | | | | | | | | |

| Communications Equipment (3.7%) | | | | | | | | |

| KVH Industries, Inc.* | | | 121,950 | | | | 939,015 | |

| | | | | | | | | |

| Diversified Financial Services (1.3%) | | | | | | | | |

| TheStreet, Inc. | | | 300,000 | | | | 339,000 | |

| | | | | | | | | |

| Electrical Equipment (0.7%) | | | | | | | | |

| Generac Holdings, Inc.* | | | 5,000 | | | | 174,800 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components (10.5%) | | | | | | | | |

| Frequency Electronics, Inc.* | | | 105,000 | | | | 976,500 | |

| Jabil Circuit, Inc. | | | 7,500 | | | | 138,525 | |

| National Instruments Corp. | | | 4,700 | | | | 128,780 | |

| TTM Technologies, Inc.* | | | 188,000 | | | | 1,415,640 | |

| | | | | | | | 2,659,445 | |

| | | | | | | | | |

| Energy Equipment & Services (0.1%) | | | | | | | | |

| Aspen Aerogels, Inc.* | | | 5,000 | | | | 24,850 | |

| | | | | | | | | |

| Health Care Providers & Services (0.9%) | | | | | | | | |

| Express Scripts Holding Co.* | | | 2,900 | | | | 219,820 | |

| | | | | | | | | |

| Health Care Technology (1.2%) | | | | | | | | |

| Castlight Health, Inc.* | | | 25,000 | | | | 99,000 | |

| Omnicell, Inc.* | | | 6,000 | | | | 205,380 | |

| | | | | | | | 304,380 | |

| | | | | | | | | |

| Internet Software & Services (10.0%) | | | | | | | | |

| Akamai Technologies, Inc.* | | | 1,000 | | | | 55,930 | |

| Amber Road, Inc.* | | | 235,000 | | | | 1,811,850 | |

| Hortonworks, Inc.* | | | 2,500 | | | | 26,725 | |

| Reis, Inc.† | | | 23,000 | | | | 572,700 | |

| YUME, Inc.* | | | 20,000 | | | | 73,600 | |

| | | | | | | | 2,540,805 | |

| | | | | | | | | |

| Oil, Gas & Consumable Fuels (1.1%) | | | | | | | | |

| Hess Corp. | | | 4,750 | | | | 285,475 | |

| | | | | | | | | |

| Pharmaceuticals (0.1%) | | | | | | | | |

| Corium International, Inc.* | | | 5,000 | | | | 17,350 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (19.8%) | | | | | | | | |

| Cohu, Inc. | | | 5,000 | | | | 54,250 | |

| Entegris, Inc.*† | | | 11,000 | | | | 159,170 | |

| FormFactor, Inc.* | | | 120,000 | | | | 1,078,800 | |

| MKS Instruments, Inc.† | | | 12,500 | | | | 538,250 | |

| PDF Solutions, Inc.*† | | | 90,000 | | | | 1,259,100 | |

| Photronics, Inc.* | | | 15,000 | | | | 133,650 | |

| Ultra Clean Holdings, Inc.* | | | 317,575 | | | | 1,807,002 | |

| | | | | | | | 5,030,222 | |

| | | | | | | | | |

| Software (0.6%) | | | | | | | | |

| Barracuda Networks, Inc.* | | | 10,000 | | | | 151,400 | |

| | | | | | | | | |

| Technology Hardware, Storage & Peripherals (10.1%) | | | | | | | | |

| Hutchinson Technology, Inc.* | | | 137,500 | | | | 466,125 | |

| Silicon Graphics International Corp.* | | | 258,119 | | | | 1,298,338 | |

| Super Micro Computer, Inc.*† | | | 32,500 | | | | 807,625 | |

| | | | | | | | 2,572,088 | |

| | | | | | | | | |

| Thrifts & Mortgage Finance (0.2%) | | | | | | | | |

| LendingTree, Inc.* | | | 500 | | | | 44,165 | |

| | | | | | | | | |

| Trading Companies & Distributors (2.1%) | | | | | | | | |

| Air Lease Corp.† | | | 20,000 | | | | 535,600 | |

| | | | | | | | | |

Total Common Stocks

(Cost $15,410,122) | | | | | | $ | 15,967,765 | |

| | | | | | | | | |

| Closed-End Funds (0.2%) | | | | | | | | |

| Tekla Healthcare Investors | | | 1,000 | | | | 23,420 | |

| Tekla Life Sciences Investors | | | 1,500 | | | | 25,785 | |

| | | | | | | | 49,205 | |

| | | | | | | | |

Total Closed-End Funds

(Cost $48,852) | | | | | | $ | 49,205 | |

| | | | | | | | | |

| Short-Term Investments (39.3%) | | | | | | | | |

| | | | | | | | | |

| Money Market Fund (39.3%) | | | | | | | | |

| Dreyfus Treasury Securities Cash Management – Institutional Class 0.16%(a) (Cost $10,004,695) | | | 10,004,695 | | | | 10,004,695 | |

| | | | | | | | | |

| | | | | | | | |

Total Investments (102.3%)

(Cost $25,463,669) | | | | | | | 26,021,665 | |

Total Securities Sold Short (-6.8%)

(Proceeds $1,615,444) | | | | | | | (1,720,465 | ) |

| Other Assets in Excess of Liabilities (4.5%) | | | | | | | 1,143,513 | |

| Net Assets (100.0%) | | | | | | $ | 25,444,713 | |

| * | Non-income producing security. |

| (a) | Rate shown is the seven day yield as of June 30, 2016. |

| † | Security position is either entirely or partially held in a segregated account as collateral for securities sold short, aggregating a total market value of $1,082,175. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (‘‘S&P’’). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

See accompanying notes to financial statements.

Needham Small Cap Growth Fund

Sc

hedule of Securities Sold Short

June 30, 2016 (Unaudited)

| | | Shares | | | Market Value | |

| Securities Sold Short (-0.8%) | | | | | | |

| | | | | | | |

| Communications Equipment (-0.2%) | | | | | | |

| Ubiquiti Networks, Inc.* | | | 1,500 | | | $ | 57,990 | |

| | | | | | | | | |

| Semiconductors & Semiconductor Equipment (-0.6%) | | | | | | | | |

| Advanced Energy Industries, Inc.* | | | 3,750 | | | | 142,350 | |

| | | | | | | | | |

Total Securities Sold Short (-0.8%)

(Proceeds $167,386) | | | | | | | 200,340 | |

| | | | | | | | | |

| Exchange Traded Funds Sold Short (-6.0%) | | | | | | | | |

| iShares Russell 2000 ETF | | | 3,000 | | | | 344,910 | |

| iShares Russell 2000 Growth ETF | | | 3,000 | | | | 411,540 | |

| iShares Russell 2000 Value ETF | | | 2,000 | | | | 194,600 | |

| iShares Micro-Cap ETF | | | 5,000 | | | | 353,600 | |

| VanEck Vectors Semiconductor ETF | | | 3,750 | | | | 215,475 | |

| | | | | | | | | |

Total Exchange Traded Funds Sold Short (-6.0%)

(Proceeds $1,448,058) | | | | | | | 1,520,125 | |

| | | | | | | | | |

Total Securities and Exchange Traded Funds Sold Short (-6.8%)

(Proceeds $1,615,444) | | | | | | $ | 1,720,465 | |

| * | Non-income producing security. |

See accompanying notes to financial statements.

Statements of Assets and Liabilities

June 30, 2016 (Unaudited)

| | | | | | | | | | | |

| | | Needham

Growth Fund | | Needham

Aggressive

Growth Fund | | Needham

Small Cap

Growth Fund | |

| Assets | | | | | | | | | | |

Investments, at Value

(Cost $59,391,747, $26,786,677, $25,463,669) | | $ | 117,402,306 | | $ | 48,593,301 | | $ | 26,021,665 | |

| Cash | | | — | | | — | | | 490 | |

| Receivables: | | | | | | | | | | |

| Deposit with Broker for Securities Sold Short | | | 5,310,756 | | | 3,498,426 | | | 1,441,412 | |

| Dividends and Interest | | | 40,337 | | | 6,414 | | | 3,561 | |

| Fund Shares Sold | | | 354 | | | 10,979 | | | 6,037 | |

| Investment Securities Sold | | | 205,213 | | | 504,928 | | | 391,224 | |

| Prepaid Expenses | | | 20,053 | | | 11,718 | | | 19,145 | |

| Total Assets | | | 122,979,019 | | | 52,625,766 | | | 27,883,534 | |

| | | | | | | | | | | |

| Liabilities | | | | | | | | | | |

Securities Sold Short, at Value

(Proceeds $4,585,547, $3,046,647, $1,615,444) | | | 5,336,457 | | | 3,578,915 | | | 1,720,465 | |

| Payables: | | | | | | | | | | |

| Investment Securities Purchased | | | 1,099 | | | 71,551 | | | 571,375 | |

| Fund Shares Redeemed | | | 91,665 | | | 46,727 | | | 79,992 | |

| Due to Adviser | | | 120,233 | | | 49,353 | | | 20,121 | |

| Distribution Fees | | | 24,490 | | | 10,202 | | | 5,374 | |

| Administration and Accounting Fees | | | 36,699 | | | 16,412 | | | 8,940 | |

| Transfer Agent Fees | | | 14,621 | | | 10,606 | | | 10,094 | |

| Directors’ Fees | | | 2,557 | | | 2,447 | | | 560 | |

| Accrued Expenses and Other Liabilities | | | 57,608 | | | 35,522 | | | 21,900 | |

| Total Liabilities | | | 5,685,429 | | | 3,821,735 | | | 2,438,821 | |

| | | | | | | | | | | |

| Net Assets | | $ | 117,293,590 | | $ | 48,804,031 | | $ | 25,444,713 | |

Shares Issued and Outstanding $0.001 Par Value

(Authorized 800,000,000,100,000,000 and 100,000,000 respectively) | | | 2,838,761 | | | 2,460,418 | | | 1,886,721 | |

Net Asset Value, Offering and Redemption Price Per Share(a) | | $ | 41.32 | | $ | 19.84 | | $ | 13.49 | |

| | | | | | | | | | | |

| Components of Net Assets | | | | | | | | | | |

| Paid-in Capital | | | 53,090,618 | | | 25,546,715 | | | 24,158,256 | |

| Accumulated Net Investment Loss | | | (807,878 | ) | | (497,651 | ) | | (211,199 | ) |

| Accumulated Net Realized Gain from Investments, Securities Sold Short, Foreign Currency Transactions and Currency | | | 7,751,201 | | | 2,480,611 | | | 1,044,681 | |

| Net Unrealized Appreciation on Investment Securities and Securities Sold Short | | | 57,259,649 | | | 21,274,356 | | | 452,975 | |

| Total Net Assets | | $ | 117,293,590 | | $ | 48,804,031 | | $ | 25,444,713 | |

| (a) | Subject to certain exceptions, a 2% redemption fee is imposed upon shares redeemed within 60 days of their purchase. See Note 2 of the notes to financial statements. |

See accompanying notes to financial statements.

For the six months ended June 30, 2016 (Unaudited)

| | | | | | | | | | | |

| | | Needham

Growth Fund | | Needham

Aggressive

Growth Fund | | Needham

Small Cap

Growth Fund | |

| Investment Income | | | | | | | | | | |

| Dividends | | $ | 511,243 | | $ | 210,836 | | $ | 27,409 | |

| Interest | | | 2,989 | | | 224 | | | 4,686 | |

| Total Investment Income | | | 514,232 | | | 211,060 | | | 32,095 | |

| | | | | | | | | | | |

| Expenses | | | | | | | | | | |

| Investment Advisory Fees | | | 733,381 | | | 299,885 | | | 149,869 | |