UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| | | |

| Investment Company Act file number: 811-00834 |

| |

Name of Registrant: Vanguard Windsor Funds | |

| |

Address of Registrant: | |

P.O. Box 2600 | |

Valley Forge, PA 19482 | |

| Name and address of agent for service: | |

| Heidi Stam, Esquire | | |

P.O. Box 876 | | |

Valley Forge, PA 19482 | | |

Registrant’s telephone number, including area code: |

(610) 669-1000 |

| Date of fiscal year end: October 31 | |

Date of reporting period: November 1, 2013 – October 31, 2014 |

| Item 1: Reports to Shareholders | |

Annual Report | October 31, 2014

Vanguard Windsor™ Fund

The mission continues

On May 1, 1975, Vanguard began operations, a fledgling company based on the simple but revolutionary idea that a mutual fund company should be managed solely in the interest of its investors.

Four decades later, that revolutionary spirit continues to animate the enterprise. Vanguard remains on a mission to give investors the best chance of investment success.

As we mark our 40th anniversary, we thank you for entrusting your assets to Vanguard and giving us the opportunity to help you reach your financial goals in the decades to come.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 8 |

| Fund Profile. | 12 |

| Performance Summary. | 14 |

| Financial Statements. | 16 |

| Your Fund’s After-Tax Returns. | 29 |

| About Your Fund’s Expenses. | 30 |

| Glossary. | 32 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Since our founding, Vanguard has drawn inspiration from the enterprise and valor demonstrated by British naval hero Horatio Nelson and his command at the Battle of the Nile in 1798. The photograph displays a replica of a merchant ship from the same era as Nelson’s flagship, the HMS Vanguard.

Your Fund’s Total Returns

| |

| Fiscal Year Ended October 31, 2014 | |

| |

| | Total |

| | Returns |

| Vanguard Windsor Fund | |

| Investor Shares | 14.14% |

| Admiral™ Shares | 14.24 |

| Russell 1000 Value Index | 16.46 |

| Multi-Cap Value Funds Average | 12.18 |

Multi-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company.

Admiral Shares carry lower expenses and are available to investors who meet certain account-balance requirements. |

|

| | | | | |

| Your Fund’s Performance at a Glance | | | | |

| October 31, 2013, Through October 31, 2014 | | | | |

| | | | Distributions Per Share |

| | Starting | Ending | | |

| | Share | Share | Income | Capital |

| | Price | Price | Dividends | Gains |

| Vanguard Windsor Fund | | | | |

| Investor Shares | $19.50 | $21.98 | $0.266 | $0.000 |

| Admiral Shares | 65.81 | 74.17 | 0.970 | 0.000 |

1

Chairman’s Letter

Dear Shareholder,

The U.S. market continued to advance over the 12 months ended October 31, 2014, but large-company growth stocks outperformed their value counterparts, reversing a recent trend. Vanguard Windsor Fund returned more than 14%, a result that was 2 percentage points ahead of the average return of peer funds but fell short of the benchmark Russell 1000 Value Index.

It’s worth noting that the average market capitalization of the stocks in the index is higher than that in Windsor’s portfolio. Large-company stocks easily outperformed small-caps during the period, giving the index a distinct advantage. In other periods, including the previous fiscal year, this divergence has helped the fund outpace the index.

If you own Windsor shares in a taxable account, you may wish to review the fund’s after-tax return presented later in this report.

Their smooth ride turned jagged, but U.S. stocks ended higher

Punctuated by a roller coaster of an October, the broad U.S. stock market returned about 16% for the 12 months ended October 31.

Impressive corporate earnings and various global stimulus measures generally supported stocks against a bleaker backdrop that included tensions in the Middle East and Ukraine as well as international economic concerns. But

over the first two weeks of October, stocks declined sharply as investors reacted to weakness in the global economy, especially the slowdown in China and the threat of deflation in Europe. Reflecting confidence in the U.S. economy, however, the Federal Reserve announced October 29 that it was ending its stimulative bond-buying program as anticipated.

U.S. stocks staged an impressive rebound in the period’s final two weeks, and several major indexes finished at record highs. International stocks didn’t fare as well. Emerging markets posted a modest advance over the 12 months, while stocks from the developed markets of Europe and the Pacific region slipped.

U.S. bonds posted positive returns as already low yields declined

The broad U.S. taxable bond market returned 4.14%. Bond prices, which backtracked at times over the summer, climbed in October as investors sought sanctuary from stock market volatility.

Overall, bond returns have been strong despite many analysts’ expectations that already low yields wouldn’t decline further. Prices rose and yields fell even as the Fed began steadily reducing its bond purchases in January. (Bond prices and yields move in opposite directions.) The yield of the 10-year U.S. Treasury note ended October at 2.31%, down from 2.54% a year earlier.

| | | | |

| Market Barometer | | | |

| |

| | | Average Annual Total Returns |

| | | Periods Ended October 31, 2014 |

| | One | Three | Five |

| | Year | Years | Years |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 16.78% | 19.90% | 16.98% |

| Russell 2000 Index (Small-caps) | 8.06 | 18.18 | 17.39 |

| Russell 3000 Index (Broad U.S. market) | 16.07 | 19.77 | 17.01 |

| FTSE All-World ex US Index (International) | 0.45 | 8.07 | 6.38 |

| |

| Bonds | | | |

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 4.14% | 2.73% | 4.22% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 7.82 | 4.93 | 5.26 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.04 | 0.04 | 0.06 |

| |

| CPI | | | |

| Consumer Price Index | 1.66% | 1.60% | 1.89% |

3

Municipal bonds returned 7.82%, with tax-exempt issues in high demand even at a time of reduced supply.

International bond markets (as measured by the Barclays Global Aggregate Index ex USD) slid in September and October en route to a –2.53% return for the 12 months.

The Fed’s target for short-term interest rates remained at 0%–0.25%, restraining returns for money market funds and savings accounts.

IT winners couldn’t overcome underperformers in other areas

The Windsor Fund looks for stocks that are underappreciated by the market but are expected to ultimately reward long-term investors. Unlike many value funds that focus primarily on traditional value or defensive sectors such as consumer staples, health care, financials, and utilities, Windsor has often charted its own course, seeking underpriced stocks wherever its advisors think they have found ones with potential to eventually outperform the market.

This strategy was evident in the fund’s portfolio composition over the past 12 months. The two advisors, Wellington Management Company and Pzena Investment Management, invested 17% of fund assets on average in the information technology sector, nearly twice the index’s 9% share. IT typically encompasses faster-growing companies favored by growth

| | | |

| Expense Ratios | | | |

| Your Fund Compared With Its Peer Group | | | |

| | Investor | Admiral | Peer Group |

| | Shares | Shares | Average |

| Windsor Fund | 0.37% | 0.27% | 1.24% |

| The fund expense ratios shown are from the prospectus dated February 26, 2014, and represent estimated costs for the current fiscal year. For the fiscal year ended October 31, 2014, the fund’s expense ratios were 0.38% for Investor Shares and 0.28% for Admiral Shares. The peer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end 2013. |

|

|

|

| |

| Peer group: Multi-Cap Value Funds. | | | |

4

funds. The advisors’ overweighting of this sector paid off, as the fund’s IT portfolio returned nearly 37%, 6 percentage points above its counterpart in the index. Semiconductor and hardware stocks posted especially strong results for the fund.

That outperformance was not enough to offset the fund’s subpar returns from nearly every other sector. Energy stocks were among the biggest drags. The advisors overweighted oil and gas exploration companies, which were hurt by falling oil prices. Those lower prices did boost the profit margins of refinery firms, but the fund was underweighted in those, further dampening relative returns. These two decisions resulted in a nearly –4% return for the fund’s energy stocks versus the index sector’s return of more than 4%.

Consumer discretionary was another notable laggard. The fund’s portfolio in this sector returned only about 3%, far below the more than 10% for its benchmark counterpart. Media companies and specialty retail stores particularly crimped relative performance.

Financials, by far the largest sector in both the index and the fund, performed well, but the advisors’ selections trailed those in the index by more than 3 percentage

| | |

| Total Returns | |

| Ten Years Ended October 31, 2014 | |

| | Average |

| | Annual Return |

| Windsor Fund Investor Shares | 7.55% |

| Russell 1000 Value Index | 7.90 |

| Multi-Cap Value Funds Average | 7.01 |

| Multi-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

5

points. Insurance stocks were among the detractors, and the advisors’ overweighting of that industry further hurt.

For more information about the advisors’ approach and the fund’s positioning during the year, please see the Advisors’ Report that follows this letter.

Over the last ten years, the fund has had a solid record of results

Looking at the Windsor Fund’s longer- term record, performance has been solid compared with its peers. The fund’s 7.55% average annual return for Investor Shares over the ten years ended October 31, 2014, was a bit behind that of its index, which, like all indexes, bears no expenses.

The fund’s returns have been positive in nine of its last ten fiscal years, and usually well above the overall market’s long-term averages. The lone negative fiscal year was 2008, when the financial crisis hammered markets worldwide, with Windsor’s focus on out-of-favor companies particularly hurting relative performance. But over the subsequent years, Windsor outperformed its benchmark by more than 2 percentage points in average annual returns.

When market volatility heats up, the best response is to keep cool

After several years of strength, stocks hit a rough patch toward the close of the fiscal year, as I noted earlier. For the first half of October, global stock markets (as measured by the FTSE Global All Cap Index) returned –5.56%. Even though stocks rebounded in the second half of the month, many investors undoubtedly were left feeling unsettled.

What’s my best advice to anxious shareholders? Remain calm and remember that volatility is a normal part of stock market investing. The value of keeping a cool head is highlighted in a Vanguard research paper that looked at how investors behaved during the financial crisis, when global stocks declined about 58% and U.S. stocks about 55%.

The 2010 paper, Resilience in Volatile Markets: 401(k) Participant Behavior, September 2007–December 2009, examined the behavior of participants in Vanguard-administered retirement plans. During that time, about three-quarters of participants made no changes to their accounts, and only 3% gave up on stocks completely.

As stocks recovered, this discipline yielded big benefits. From the end of 2008 to the end of 2013, the average Vanguard 401(k) portfolio nearly doubled in value, largely because of the surge in stock prices.

I’m pleased that, over time, our clients have demonstrated an impressive ability to remain focused on their long-term goals.

6

They stayed the course through the 1987 correction, the dot-com boom of the 1990s, and the more recent financial crisis, and they continue to do so today.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

November 13, 2014

7

Advisors’ Report

For the fiscal year ended October 31, 2014, the Investor Shares of Vanguard Windsor Fund returned 14.14% and the lower-cost Admiral Shares returned 14.24%. Your fund is managed by two independent advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct yet complementary investment approaches. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the percentage and amount of fund assets that each manages, and brief descriptions of their investment strategies are presented in the table below. The advisors have also prepared a discussion of the investment environment that existed during the period and of how their portfolio positioning reflects this assessment. These reports were prepared on November 18, 2014.

Wellington Management Company, llp

Portfolio Manager:

James N. Mordy, Senior Vice President

and Equity Portfolio Manager

Equity volatility has increased in recent months as the Federal Reserve wound down its monthly bond purchases. Geopolitical tensions and Ebola have also grabbed investors’ attention. The S&P 500 Index provided strong returns over the fiscal year as U.S. economic momentum recovered from a severe and disruptive winter. With other major economies sputtering, global central bank policies

| | | | | |

| Vanguard Windsor Fund Investment Advisors | | |

| |

| | Fund Assets Managed | | |

| Investment Advisor | % | $ Million | | Investment Strategy |

| Wellington Management | 69 | 12,544 | | Seeks to provide long-term total returns above both the |

| Company, LLP | | | | S&P 500 and value-oriented indexes over a complete |

| | | | | market cycle through bottom-up, fundamentally driven |

| | | | | stock selection focused on undervalued securities. |

| Pzena Investment Management, | 29 | 5,289 | | Uses a fundamental, bottom-up, deep-value-oriented |

| LLC | | | | investment strategy. Seeks to buy good businesses at |

| | | | | low prices, focusing exclusively on companies that are |

| | | | | underperforming their historically demonstrated |

| | | | | earnings power. |

| Cash Investments | 2 | 230 | | These short-term reserves are invested by Vanguard in |

| | | | | equity index products to simulate investment in stocks. |

| | | | | Each advisor also may maintain a modest cash |

| | | | | position. |

8

have diverged. Although yields on longer-term U.S. Treasury bonds have remained lower than we anticipated, the dollar has strengthened, pressuring commodity prices, most prominently crude oil.

Once again, information technology was our best sector relative to the S&P 500 Index. Three semiconductor stocks provided exceptional returns: Avago Technologies, NXP Semiconductors, and Skyworks Solutions. In each case, we were early in identifying specific growth-fueling trends that were largely ignored in the stocks’ low valuations. As each generation of smart-phones increases in complexity, Avago and Skyworks have earned greater revenue per phone. NXP is a major beneficiary of several powerful trends such as credit-card security, near-field communication (short-range wireless technology), and emerging automotive connectivity opportunities.

We also benefited from not owning any stocks in telecommunication services, the second-worst-performing sector in the S&P 500 Index.

Energy was the worst performer in the broad market and our worst-performing sector on a relative basis. Crude oil prices have fallen 25% in recent months as fears of geopolitical disruption in the Middle East have given way to the reality of a temporarily oversupplied global market. U.S. natural gas prices have also softened as storage levels were refilled during a mild summer. Our positioning is somewhat aggressive, as we have favored more volatile exploration and production companies over the major integrated companies. Although this has hurt short-term performance, we believe that low-cost producers such as Pioneer Natural Resources, Concho Resources, and Southwestern Energy will be able to continue to grow profitably in a low-price environment, while the higher-cost major companies will be under more pressure. Furthermore, these stocks trade well below their net asset values, using current commodity prices, which bolsters our conviction. Looking to 2015, we see mounting budgetary pressures on the major OPEC countries to coordinate a cut in output, while most energy companies will have to modestly reduce spending in response to lower cash flow.

We also lagged in industrials. American Airlines was a winner (not surprisingly, given healthy industry fundamentals, declining fuel costs, and the company’s first dividend in 34 years), but we had some disappointments. A year ago we were too optimistic about European growth prospects, which had underpinned our investment case for stocks such as Rexel and SKF. In engineering and construction, KBR underperformed its peers in winning new business, and Eaton, one of our top holdings, had an uneven year at best. We have sold KBR and SKF and significantly reduced our stake in Rexel, and we are now slightly underweighted in this sector (a reversal from a year ago).

The consumer discretionary sector has been difficult for investors as online competition, evolving consumer tastes, and oversupply challenge traditional business models.

We avoided some higher-growth companies that lagged the market (Amazon and Starbucks) but were hurt by health-products retailer GNC as its sales fell well short of

9

expectations. If they can limit the magnitude of discounting, U.S. retailers are set up for a better holiday season, with two million more people employed than a year ago, some wage growth, higher consumer net worth, a windfall from lower gas prices, ample inventories, and an extra shopping day between Thanksgiving and Christmas.

The health care sector led the S&P 500 Index. Although high valuations have generally kept us away from many sizzling biotechnology stocks, we see underappreciated value in the pipelines of many traditional pharmaceutical companies. Wellington’s experienced health care team has been a deep resource for us in identifying opportunities in immuno-oncology, and Bristol-Myers Squibb is now our largest portfolio holding.

Our performance in the financial sector was mixed. We have favored the insurance industry, where most of our companies have improved profitability despite continued low interest rates.

We look for continuing modest GDP expansion both in the United States and globally. Although markets have recently concluded that easing inflationary pressures from food and energy prices will keep the Fed on hold for longer before raising short-term interest rates, we think an uptick in wage pressures will be an increasing part of the conversation in the first half of 2015. An easing of monetary policies in Japan and Europe will be helpful. We have reduced exposure to the more cyclical sectors but remained slightly overweighted at the end of the period. Our transactions over the fiscal year favored the consumer discretionary, health care, and financial sectors at the expense of industrials and information technology.

Despite a rising market for more than five years, we continue to find opportunities to buy good companies at a discount, and we will look to prudently manage our risk in what promises to be a more volatile environment.

Pzena Investment Management, LLC

Portfolio Managers:

Richard Pzena, Managing Principal

and Co-Chief Investment Officer

John P. Goetz, Managing Principal

and Co-Chief Investment Officer

Our portion of the fund benefited from strong performance by our technology holdings, while our consumer discretionary and energy holdings lagged. We have frequently discussed the compellingly cheap valuations applied to “old tech” companies (in contrast to the heady valuations in “new tech”). Recently, companies in the IT hardware, enterprise software, and semiconductor industries have performed well after delivering consensus-beating results, including Hewlett-Packard, Microsoft, and Intel (among the top contributors to performance over the period), and we have pared our exposures. Hewlett-Packard’s share price has risen sharply from its December 2012 low on the back of solid execution and strong cash-flow generation, which are evidence that management is addressing problems. Although we have taken some profits, the shares remain attractively valued.

10

In consumer discretionary, office supply company Staples was a large detractor from portfolio results because of weaker-than-expected revenues and earnings in the retail segment. Staples is the world’s largest business-to-business internet company, and we believe the delivery side is its real asset. While we expect industry revenues to remain weak, we see further cost-cutting opportunities through reduced retail square footage. General Motors shares were also weak after safety-related recalls. Although the recalls are a setback, the market reaction has become another reason to own the stock, as GM shares have fallen in excess of the company’s recall liabilities.

Our energy holdings were driven lower in September and October after Brent Crude prices declined as Saudi Arabia chose not to defend $100-per-barrel oil in the face of strong supply and slightly weakening demand from China.

Financials produced mixed results. Our exposure includes insurance companies, wealth managers, and banks. Our holdings in money-center and investment banks were strong, but their returns were more than offset by lagging performance from our regional banks and insurance holdings.

As a cautious tone persists among many investors, we find value to be in the “high beta” (high volatility) and economically sensitive sectors. As a result, our largest allocations are to financials, technology, and integrated oil companies. Financials constitute the largest part of our portfolio. Much of this exposure is to big money-center banks, reflecting still-depressed valuations driven by the market’s persistent skepticism about a full recovery for these generally strong franchises. But profitability has partly rebounded, and adjustment to the immense changes in the regulatory landscape is progressing. Although the stock prices of the big money-center banks (such as Citigroup, Bank of America, and JPMorgan Chase) almost doubled in the last two years, we believe those achievements have not been fully recognized in banks’ share prices, and we expect the stocks to do well as drags on earnings dissipate over the next few years.

We continue to focus on technology companies that have the potential to benefit from higher future corporate spending on equipment and services. Despite recent declines in oil prices, we have always viewed the current price to be closer to normal for the long term, and we still consider integrated oil companies to be very cheap as investors continue to overpenalize their lack of reserve growth and heightened global political risk. High-dividend-paying companies with less cyclical earnings profiles—such as utilities, real estate investment trusts (REITs), and pharmaceuticals—trade at premium valuations and thus have little representation in our “deep value” portfolio. We expect our portfolio to benefit as this valuation gap normalizes.

11

Windsor Fund

Fund Profile

As of October 31, 2014

| | | |

| Share-Class Characteristics | |

| | Investor | Admiral |

| | Shares | Shares |

| Ticker Symbol | VWNDX | VWNEX |

| Expense Ratio1 | 0.37% | 0.27% |

| 30-Day SEC Yield | 1.40% | 1.50% |

| | | | |

| Portfolio Characteristics | | |

| | | | DJ |

| | | | U.S |

| | | Russell | Total |

| | | 1000 | Market |

| | | Value | FA |

| | Fund | Index | Index |

| Number of Stocks | 139 | 695 | 3,756 |

| Median Market Cap | $29.8B | $58.1B | $47.3B |

| Price/Earnings Ratio | 16.7x | 17.5x | 20.4x |

| Price/Book Ratio | 1.9x | 1.8x | 2.7x |

| Return on Equity | 15.4% | 13.8% | 17.8% |

| Earnings Growth | | | |

| Rate | 15.5% | 13.0% | 15.7% |

| Dividend Yield | 1.8% | 2.3% | 1.9% |

| Foreign Holdings | 13.7% | 0.0% | 0.0% |

| Turnover Rate | 38% | — | — |

| Short-Term Reserves | 1.9% | — | — |

| | | |

| Volatility Measures | | |

| | Russell | DJ |

| | 1000 | U.S. Total |

| | Value | Market |

| | Index | FA Index |

| R-Squared | 0.92 | 0.94 |

| Beta | 1.07 | 1.08 |

| These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months. |

|

| | | |

| Ten Largest Holdings (% of total net assets) |

| American International | | |

| Group Inc. | Multi-line Insurance | 2.1% |

| MetLife Inc. | Life & Health | |

| | Insurance | 2.1 |

| Citigroup Inc. | Diversified Banks | 2.1 |

| Bristol-Myers Squibb Co. | Pharmaceuticals | 2.1 |

| Wells Fargo & Co. | Diversified Banks | 1.8 |

| Aetna Inc. | Managed Health | |

| | Care | 1.6 |

| Ameriprise Financial Inc. | Asset Management | |

| | & Custody Banks | 1.6 |

| NXP Semiconductor NV | Semiconductors | 1.6 |

| Eaton Corp. plc | Electrical | |

| | Components & | |

| | Equipment | 1.6 |

| Bank of America Corp. | Diversified Banks | 1.5 |

| Top Ten | | 18.1% |

| The holdings listed exclude any temporary cash investments and equity index products. |

|

Investment Focus

1 The expense ratios shown are from the prospectus dated February 26, 2014, and represent estimated costs for the current fiscal year. For the fiscal year ended October 31, 2014, the expense ratios were 0.38% for Investor Shares and 0.28% for Admiral Shares.

12

Windsor Fund

| | | | |

| Sector Diversification (% of equity exposure) |

| | | Russell | DJ |

| | | 1000 | U.S. Total |

| | | Value | Market |

| | Fund | Index | FA Index |

| Consumer | | | |

| Discretionary | 11.6% | 6.2% | 12.5% |

| Consumer Staples | 5.0 | 7.1 | 8.3 |

| Energy | 11.6 | 12.2 | 8.5 |

| Financials | 27.7 | 29.5 | 17.7 |

| Health Care | 16.0 | 13.7 | 13.9 |

| Industrials | 8.0 | 10.3 | 11.3 |

| Information | | | |

| Technology | 16.1 | 9.2 | 18.8 |

| Materials | 2.7 | 3.2 | 3.6 |

| Telecommunication | | | |

| Services | 0.0 | 2.2 | 2.2 |

| Utilities | 1.3 | 6.4 | 3.2 |

13

Windsor Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

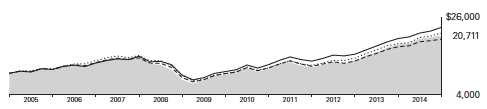

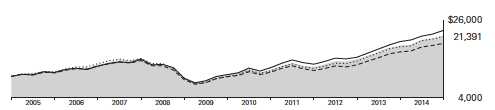

Cumulative Performance: October 31, 2004, Through October 31, 2014

Initial Investment of $10,000

| | | | | |

| | | Average Annual Total Returns | |

| | | Periods Ended October 31, 2014 | |

| | | | | | Final Value |

| | | One | Five | Ten | of a $10,000 |

| | | Year | Years | Years | Investment |

| Windsor Fund*Investor Shares | 14.14% | 16.65% | 7.55% | $20,711 |

| •••••••• | Russell 1000 Value Index | 16.46 | 16.49 | 7.90 | 21,393 |

| – – – – | Multi-Cap Value Funds Average | 12.18 | 14.73 | 7.01 | 19,684 |

| | Dow Jones U.S. Total Stock Market | | | | |

| | Float Adjusted Index | 16.00 | 17.09 | 8.71 | 23,060 |

| Multi-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. |

| | | | |

| | | | | Final Value |

| | One | Five | Ten | of a $50,000 |

| | Year | Years | Years | Investment |

| Windsor Fund Admiral Shares | 14.24% | 16.77% | 7.67% | $104,651 |

| Russell 1000 Value Index | 16.46 | 16.49 | 7.90 | 106,966 |

| Dow Jones U.S. Total Stock Market Float | | | | |

| Adjusted Index | 16.00 | 17.09 | 8.71 | 115,300 |

See Financial Highlights for dividend and capital gains information.

14

Windsor Fund

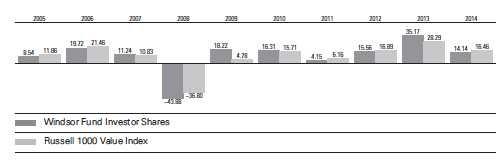

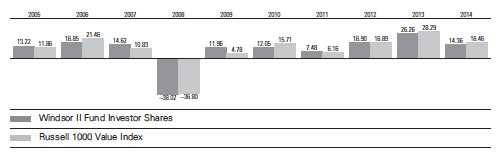

Fiscal-Year Total Returns (%): October 31, 2004, Through October 31, 2014

Average Annual Total Returns: Periods Ended September 30, 2014

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| | | | |

| | Inception | One | Five | Ten |

| | Date | Year | Years | Years |

| Investor Shares | 10/23/1958 | 17.30% | 15.46% | 7.59% |

| Admiral Shares | 11/12/2001 | 17.39 | 15.56 | 7.71 |

15

Windsor Fund

Financial Statements

Statement of Net Assets

As of October 31, 2014

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Common Stocks (97.5%)1 | | |

| Consumer Discretionary (11.3%) | |

| | Lennar Corp. Class A | 5,181,690 | 223,227 |

| | Newell Rubbermaid Inc. | 6,381,300 | 212,689 |

| | Lowe’s Cos. Inc. | 3,588,500 | 205,262 |

| | Delphi Automotive plc | 2,493,400 | 171,995 |

| | Ralph Lauren Corp. | | |

| | Class A | 951,900 | 156,911 |

| | TJX Cos. Inc. | 2,119,000 | 134,175 |

| * | Toll Brothers Inc. | 3,857,000 | 123,231 |

| | Omnicom Group Inc. | 1,462,125 | 105,068 |

| * | TRW Automotive | | |

| | Holdings Corp. | 1,020,000 | 103,377 |

| | Staples Inc. | 7,100,921 | 90,040 |

| | Nordstrom Inc. | 1,195,700 | 86,820 |

| | General Motors Co. | 2,546,225 | 79,952 |

| | Ford Motor Co. | 5,290,400 | 74,542 |

| | Kohl’s Corp. | 1,303,475 | 70,674 |

| * | News Corp. Class A | 4,426,075 | 68,516 |

| | Comcast Corp. | 1,155,700 | 63,725 |

| | Interpublic Group of | | |

| | Cos. Inc. | 2,732,025 | 52,974 |

| * | News Corp. Class B | 1,469,052 | 22,109 |

| | | | 2,045,287 |

| Consumer Staples (4.8%) | | |

| | BRF SA ADR | 6,760,200 | 176,103 |

| | Ingredion Inc. | 2,248,117 | 173,667 |

| | CVS Health Corp. | 1,882,000 | 161,495 |

| | Japan Tobacco Inc. | 2,937,300 | 101,768 |

| | Wal-Mart Stores Inc. | 1,321,900 | 100,821 |

| | Diageo plc | 2,759,687 | 81,226 |

| | Kellogg Co. | 1,198,425 | 76,651 |

| | | | 871,731 |

| Energy (11.3%) | | |

| | BP plc ADR | 4,856,800 | 211,077 |

| | Royal Dutch Shell plc | | |

| | ADR | 2,891,606 | 207,588 |

| | Baker Hughes Inc. | 3,509,650 | 185,871 |

| | Pioneer Natural | | |

| | Resources Co. | 877,200 | 165,843 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Exxon Mobil Corp. | 1,552,175 | 150,111 |

| | Cameco Corp. | 8,344,000 | 145,019 |

| * | Southwestern Energy Co. | 4,454,000 | 144,800 |

| | Canadian Natural | | |

| | Resources Ltd. | 3,718,900 | 129,715 |

| * | Cobalt International | | |

| | Energy Inc. | 10,822,642 | 126,733 |

| | National Oilwell Varco Inc. | 1,472,700 | 106,977 |

| | Anadarko Petroleum Corp. | 1,018,400 | 93,469 |

| | Valero Energy Corp. | 1,710,400 | 85,674 |

| | Halliburton Co. | 1,513,300 | 83,443 |

| | Chevron Corp. | 616,400 | 73,937 |

| * | Concho Resources Inc. | 457,800 | 49,914 |

| | Murphy Oil Corp. | 826,350 | 44,119 |

| | Apache Corp. | 528,575 | 40,806 |

| | | | 2,045,096 |

| Financials (27.0%) | | |

| | American International | | |

| | Group Inc. | 7,212,800 | 386,390 |

| | MetLife Inc. | 7,116,725 | 386,011 |

| | Citigroup Inc. | 7,146,075 | 382,529 |

| | Wells Fargo & Co. | 6,197,050 | 329,001 |

| | Ameriprise Financial Inc. | 2,320,300 | 292,752 |

| | Bank of America Corp. | 15,416,100 | 264,540 |

| | Principal Financial | | |

| | Group Inc. | 4,549,100 | 238,236 |

| | XL Group plc Class A | 6,564,125 | 222,393 |

| | Weyerhaeuser Co. | 5,771,500 | 195,423 |

| | PNC Financial Services | | |

| | Group Inc. | 2,070,250 | 178,849 |

| | Unum Group | 4,937,100 | 165,195 |

| | SL Green Realty Corp. | 1,312,400 | 151,845 |

| | Public Storage | 781,200 | 144,007 |

| | JPMorgan Chase & Co. | 2,330,400 | 140,943 |

| | Zions Bancorporation | 4,609,244 | 133,530 |

| | Goldman Sachs Group Inc. | 638,050 | 121,223 |

| | State Street Corp. | 1,527,775 | 115,286 |

| | Voya Financial Inc. | 2,725,700 | 106,984 |

| | UBS AG | 6,067,175 | 105,448 |

| | Julius Baer Group Ltd. | 2,395,631 | 104,961 |

16

Windsor Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Morgan Stanley | 2,982,366 | 104,234 |

| | Axis Capital Holdings Ltd. | 1,602,221 | 77,131 |

| | Progressive Corp. | 2,074,375 | 54,784 |

| | Hartford Financial | | |

| | Services Group Inc. | 1,382,425 | 54,716 |

| | Comerica Inc. | 1,132,600 | 54,070 |

| | Willis Group Holdings plc | 1,261,950 | 51,147 |

| | Citizens Financial | | |

| | Group Inc. | 2,062,250 | 48,710 |

| | Regions Financial Corp. | 4,739,400 | 47,062 |

| | KeyCorp | 3,482,075 | 45,963 |

| | Fifth Third Bancorp | 2,283,800 | 45,653 |

| * | Genworth Financial Inc. | | |

| | Class A | 2,832,750 | 39,630 |

| | Intercontinental | | |

| | Exchange Inc. | 160,800 | 33,493 |

| | Invesco Ltd. | 695,225 | 28,136 |

| | Franklin Resources Inc. | 453,750 | 25,233 |

| | | | 4,875,508 |

| Health Care (15.6%) | | |

| | Bristol-Myers Squibb Co. | 6,408,400 | 372,905 |

| | Aetna Inc. | 3,590,256 | 296,232 |

| | AstraZeneca plc ADR | 2,830,600 | 206,464 |

| | Medtronic Inc. | 2,634,500 | 179,568 |

| | Roche Holding AG | 530,325 | 156,635 |

| | UnitedHealth Group Inc. | 1,547,100 | 146,990 |

| | Amgen Inc. | 839,400 | 136,134 |

| | Sanofi | 1,331,110 | 123,299 |

| | Eli Lilly & Co. | 1,801,500 | 119,493 |

| | Covidien plc | 1,249,000 | 115,458 |

| | Cigna Corp. | 1,133,675 | 112,880 |

| | Abbott Laboratories | 2,532,575 | 110,395 |

| | Johnson & Johnson | 1,018,700 | 109,795 |

| | Merck & Co. Inc. | 1,622,100 | 93,984 |

| * | Express Scripts | | |

| | Holding Co. | 1,209,700 | 92,929 |

| | Teva Pharmaceutical | | |

| | Industries Ltd. ADR | 1,485,500 | 83,886 |

| | Becton Dickinson and Co. | 613,425 | 78,948 |

| * | Mylan Inc. | 1,446,000 | 77,433 |

| | McKesson Corp. | 364,500 | 74,143 |

| | Baxter International Inc. | 740,613 | 51,947 |

| | Pfizer Inc. | 1,487,900 | 44,563 |

| * | Laboratory Corp. of | | |

| | America Holdings | 251,775 | 27,516 |

| | Quest Diagnostics Inc. | 84,561 | 5,366 |

| | | | 2,816,963 |

| Industrials (7.8%) | | |

| | Eaton Corp. plc | 4,162,200 | 284,653 |

| | Raytheon Co. | 1,836,100 | 190,734 |

| * | Sensata Technologies | | |

| | Holding NV | 3,349,200 | 163,475 |

| | Dover Corp. | 1,663,900 | 132,180 |

| | Norfolk Southern Corp. | 1,191,700 | 131,850 |

| | Parker-Hannifin Corp. | 927,025 | 117,760 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Honeywell | | |

| | International Inc. | 1,077,800 | 103,598 |

| | American Airlines | | |

| | Group Inc. | 2,041,700 | 84,424 |

| | Masco Corp. | 3,732,548 | 82,377 |

| | Rexel SA | 2,995,662 | 50,393 |

| | General Dynamics Corp. | 216,500 | 30,258 |

| | L-3 Communications | | |

| | Holdings Inc. | 211,050 | 25,634 |

| | | | 1,397,336 |

| Information Technology (15.6%) | |

| * | NXP Semiconductor NV | 4,202,300 | 288,530 |

| * | Arrow Electronics Inc. | 4,190,050 | 238,246 |

| | Cisco Systems Inc. | 9,049,025 | 221,430 |

| | Lam Research Corp. | 2,774,000 | 215,984 |

| | Avago Technologies Ltd. | | |

| | Class A | 2,247,200 | 193,821 |

| | Hewlett-Packard Co. | 5,372,675 | 192,771 |

| | SanDisk Corp. | 1,989,800 | 187,320 |

| * | Check Point Software | | |

| | Technologies Ltd. | 2,258,300 | 167,679 |

| * | Teradata Corp. | 3,564,440 | 150,847 |

| | Apple Inc. | 1,304,800 | 140,918 |

| | Oracle Corp. | 3,368,700 | 131,548 |

| | Microsoft Corp. | 2,556,500 | 120,028 |

| | Intel Corp. | 3,012,125 | 102,442 |

| | Accenture plc Class A | 1,237,300 | 100,370 |

| | Corning Inc. | 4,130,925 | 84,395 |

| * | Cognizant Technology | | |

| | Solutions Corp. Class A | 1,655,100 | 80,852 |

| | Analog Devices Inc. | 1,204,000 | 59,742 |

| | Maxim Integrated | | |

| | Products Inc. | 1,955,200 | 57,365 |

| | TE Connectivity Ltd. | 865,010 | 52,878 |

| | Skyworks Solutions Inc. | 541,300 | 31,525 |

| | | | 2,818,691 |

| Materials (2.6%) | | |

| | Celanese Corp. Class A | 2,445,100 | 143,601 |

| | Methanex Corp. | 2,142,500 | 127,136 |

| | Reliance Steel & | | |

| | Aluminum Co. | 1,589,700 | 107,273 |

| | LyondellBasell Industries | | |

| | NV Class A | 590,300 | 54,089 |

| * | Owens-Illinois Inc. | 1,570,500 | 40,472 |

| | | | 472,571 |

| Other (0.3%) | | |

| 2 | Vanguard Value ETF | 703,525 | 58,153 |

| |

| Utilities (1.2%) | | |

| | Entergy Corp. | 1,307,873 | 109,887 |

| | PG&E Corp. | 1,899,400 | 95,578 |

| | FirstEnergy Corp. | 189,186 | 7,064 |

| | | | 212,529 |

| Total Common Stocks | | |

| (Cost $13,373,266) | | 17,613,865 |

17

Windsor Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Temporary Cash Investments (2.9%)1 | |

| Money Market Fund (1.6%) | | |

| 3 | Vanguard Market Liquidity | | |

| | Fund, 0.114% | 289,984,223 | 289,984 |

| |

| | | Face | |

| | | Amount | |

| | | ($000) | |

| Repurchase Agreement (1.2%) | | |

| | Bank of America Securities, LLC | |

| | 0.090%, 11/3/14 (Dated | | |

| | 10/31/14, Repurchase Value | |

| | $217,802,000, collateralized | | |

| | by Federal Home Loan Mortgage | |

| | Corp. 2.138%–5.968%, | | |

| | 5/1/34–11/1/44, and Federal | | |

| | National Mortgage Assn. | | |

| | 1.953%–4.069%, | | |

| | 11/1/20–10/1/44, with a | | |

| | value of $222,156,000) | 217,800 | 217,800 |

| |

| U.S. Government and Agency Obligations (0.1%) |

| 4,6 | Fannie Mae Discount Notes, | | |

| | 0.080%, 11/5/14 | 3,000 | 3,000 |

| 5,6 | Federal Home Loan Bank | | |

| | Discount Notes, 0.060%, | | |

| | 12/31/14 | 3,500 | 3,500 |

| 5 | Federal Home Loan Bank | | |

| | Discount Notes, 0.080%, | | |

| | 2/20/15 | 2,300 | 2,300 |

| 4,6 | Freddie Mac Discount Notes, | | |

| | 0.050%, 1/14/15 | 4,000 | 3,999 |

| | | | 12,799 |

| Total Temporary Cash Investments | |

| (Cost $520,583) | | 520,583 |

| Total Investments (100.4%) | | |

| (Cost $13,893,849) | | 18,134,448 |

| | |

| | Market |

| | Value• |

| | ($000) |

| Other Assets and Liabilities (-0.4%) | |

| Other Assets | 194,613 |

| Liabilities | (265,995) |

| | (71,382) |

| Net Assets (100%) | 18,063,066 |

| |

| |

| At October 31, 2014, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 12,982,237 |

| Undistributed Net Investment Income | 52,131 |

| Accumulated Net Realized Gains | 783,014 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 4,240,599 |

| Futures Contracts | 5,285 |

| Foreign Currencies | (200) |

| Net Assets | 18,063,066 |

| |

| Investor Shares—Net Assets | |

| Applicable to 326,596,069 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 7,178,923 |

| Net Asset Value Per Share— | |

| Investor Shares | $21.98 |

| |

| Admiral Shares—Net Assets | |

| Applicable to 146,743,011 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 10,884,143 |

| Net Asset Value Per Share— | |

| Admiral Shares | $74.17 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 98.5% and 1.9%, respectively, of net assets.

2 Considered an affiliated company of the fund as the issuer is another member of The Vanguard Group.

3 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

4 The issuer was placed under federal conservatorship in September 2008; since that time, its daily operations have been managed by the Federal Housing Finance Agency and it receives capital from the U.S. Treasury, as needed to maintain a positive net worth, in exchange for senior preferred stock.

5 The issuer operates under a congressional charter; its securities are generally neither guaranteed by the U.S. Treasury nor backed by the full faith and credit of the U.S. government.

6 Securities with a value of $9,799,000 have been segregated as initial margin for open futures contracts.

ADR—American Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

18

Windsor Fund

Statement of Operations

| |

| | Year Ended |

| | October 31, 2014 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1,2 | 296,076 |

| Interest2 | 466 |

| Securities Lending | 1,569 |

| Total Income | 298,111 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 22,266 |

| Performance Adjustment | 4,612 |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 15,317 |

| Management and Administrative—Admiral Shares | 11,699 |

| Marketing and Distribution—Investor Shares | 1,112 |

| Marketing and Distribution—Admiral Shares | 1,391 |

| Custodian Fees | 190 |

| Auditing Fees | 35 |

| Shareholders’ Reports—Investor Shares | 43 |

| Shareholders’ Reports—Admiral Shares | 28 |

| Trustees’ Fees and Expenses | 30 |

| Total Expenses | 56,723 |

| Expenses Paid Indirectly | (231) |

| Net Expenses | 56,492 |

| Net Investment Income | 241,619 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold2 | 1,558,125 |

| Futures Contracts | 38,988 |

| Foreign Currencies | (376) |

| Realized Net Gain (Loss) | 1,596,737 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 454,551 |

| Futures Contracts | (4,373) |

| Foreign Currencies | (284) |

| Change in Unrealized Appreciation (Depreciation) | 449,894 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 2,288,250 |

1 Dividends are net of foreign withholding taxes of $4,324,000.

2 Dividend income, interest income, and realized net gain (loss) from affiliated companies of the fund were $1,303,000, $362,000, and $17,300,000, respectively.

See accompanying Notes, which are an integral part of the Financial Statements.

19

Windsor Fund

Statement of Changes in Net Assets

| | |

| | Year Ended October 31, |

| | 2014 | 2013 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 241,619 | 221,195 |

| Realized Net Gain (Loss) | 1,596,737 | 1,394,140 |

| Change in Unrealized Appreciation (Depreciation) | 449,894 | 2,680,607 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 2,288,250 | 4,295,942 |

| Distributions | | |

| Net Investment Income | | |

| Investor Shares | (91,690) | (110,032) |

| Admiral Shares | (139,380) | (110,078) |

| Realized Capital Gain | | |

| Investor Shares | — | — |

| Admiral Shares | — | — |

| Total Distributions | (231,070) | (220,110) |

| Capital Share Transactions | | |

| Investor Shares | (810,259) | (1,629,460) |

| Admiral Shares | 545,483 | 1,318,490 |

| Net Increase (Decrease) from Capital Share Transactions | (264,776) | (310,970) |

| Total Increase (Decrease) | 1,792,404 | 3,764,862 |

| Net Assets | | |

| Beginning of Period | 16,270,662 | 12,505,800 |

| End of Period1 | 18,063,066 | 16,270,662 |

| 1 Net Assets—End of Period includes undistributed net investment income of $52,131,000 and $41,958,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

20

Windsor Fund

Financial Highlights

| | | | | |

| Investor Shares | | | | | |

| |

| For a Share Outstanding | | | Year Ended October 31, |

| Throughout Each Period | 2014 | 2013 | 2012 | 2011 | 2010 |

| Net Asset Value, Beginning of Period | $19.50 | $14.66 | $12.92 | $12.56 | $10.97 |

| Investment Operations | | | | | |

| Net Investment Income | . 279 | .255 | .252 | .184 | .1901 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | 2.467 | 4.839 | 1.729 | . 346 | 1.586 |

| Total from Investment Operations | 2.746 | 5.094 | 1.981 | .530 | 1.776 |

| Distributions | | | | | |

| Dividends from Net Investment Income | (. 266) | (. 254) | (. 241) | (.170) | (.186) |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Total Distributions | (. 266) | (. 254) | (. 241) | (.170) | (.186) |

| Net Asset Value, End of Period | $21.98 | $19.50 | $14.66 | $12.92 | $12.56 |

| |

| Total Return2 | 14.14% | 35.17% | 15.56% | 4.15% | 16.31% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $7,179 | $7,126 | $6,711 | $6,736 | $7,999 |

| Ratio of Total Expenses to Average Net Assets3 | 0.38% | 0.37% | 0.35% | 0.39% | 0.33% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 1.33% | 1.49% | 1.80% | 1.34% | 1.59%1 |

| Portfolio Turnover Rate | 38% | 40% | 68% | 49% | 50% |

1 Net investment income per share and the ratio of net investment income to average net assets include $.036 and 0.29%, respectively, resulting from a cash payment received in connection with the merger of Schering-Plough Corp. and Merck & Co. in November 2009.

2 Total returns do not include account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable account service fees.

3 Includes performance-based investment advisory fee increases (decreases) of 0.03%, 0.02%, (0.01%), 0.03%, and (0.03%). |

|

|

|

|

See accompanying Notes, which are an integral part of the Financial Statements.

21

Windsor Fund

Financial Highlights

| | | | | |

| Admiral Shares | | | | | |

| |

| For a Share Outstanding | | | Year Ended October 31, |

| Throughout Each Period | 2014 | 2013 | 2012 | 2011 | 2010 |

| Net Asset Value, Beginning of Period | $65.81 | $49.47 | $43.59 | $42.37 | $37.01 |

| Investment Operations | | | | | |

| Net Investment Income | 1.016 | . 924 | . 900 | . 664 | . 6851 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | 8.314 | 16.329 | 5.844 | 1.171 | 5.348 |

| Total from Investment Operations | 9.330 | 17.253 | 6.744 | 1.835 | 6.033 |

| Distributions | | | | | |

| Dividends from Net Investment Income | (.970) | (. 913) | (. 864) | (. 615) | (. 673) |

| Distributions from Realized Capital Gains | — | — | — | — | — |

| Total Distributions | (.970) | (. 913) | (. 864) | (. 615) | (. 673) |

| Net Asset Value, End of Period | $74.17 | $65.81 | $49.47 | $43.59 | $42.37 |

| |

| Total Return | 14.24% | 35.32% | 15.71% | 4.26% | 16.44% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $10,884 | $9,144 | $5,795 | $4,994 | $4,680 |

| Ratio of Total Expenses to Average Net Assets2 | 0.28% | 0.27% | 0.25% | 0.29% | 0.22% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 1.43% | 1.59% | 1.90% | 1.44% | 1.70%1 |

| Portfolio Turnover Rate | 38% | 40% | 68% | 49% | 50% |

1 Net investment income per share and the ratio of net investment income to average net assets include $.120 and 0.29%, respectively, resulting from a cash payment received in connection with the merger of Schering-Plough Corp. and Merck & Co. in November 2009.

2 Includes performance-based investment advisory fee increases (decreases) of 0.03%, 0.02%, (0.01%), 0.03%, and (0.03%). |

|

|

See accompanying Notes, which are an integral part of the Financial Statements.

22

Windsor Fund

Notes to Financial Statements

Vanguard Windsor Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund offers two classes of shares: Investor Shares and Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market. Counterparty risk involving futures is mitigated because a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades futures contracts on an exchange, monitors the financial strength of its clearing brokers and clearinghouse, and has entered into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

23

Windsor Fund

Futures contracts are valued at their quoted daily settlement prices. The aggregate settlement values of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

During the year ended October 31, 2014, the fund’s average investments in long and short futures contracts represented 1% and 0% of net assets, respectively, based on the average of aggregate settlement values at each quarter-end during the period

4. Repurchase Agreements: The fund enters into repurchase agreements with institutional counterparties. Securities pledged as collateral to the fund under repurchase agreements are held by a custodian bank until the agreements mature. Each agreement requires that the market value of the collateral be sufficient to cover payments of interest and principal. The fund further mitigates its counterparty risk by entering into repurchase agreements only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master repurchase agreements with its counterparties. The master repurchase agreements provide that, in the event of a counter-party’s default (including bankruptcy), the fund may terminate any repurchase agreements with that counterparty, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund. Such action may be subject to legal proceedings, which may delay or limit the disposition of collateral.

5. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (October 31, 2011–2014), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

6. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

7. Securities Lending: To earn additional income, the fund lends its securities to qualified institutional borrowers. Security loans are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counterparty risk by entering into securities lending transactions only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master securities lending agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund; however, such actions may be subject to legal proceedings. While collateral mitigates counterparty risk, in the absence of a default the fund may experience delays and costs in recovering the securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability in the Statement of Net Assets for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan.

8. Credit Facility: The fund and certain other funds managed by The Vanguard Group participate in a $2.89 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds

24

Windsor Fund

are charged administrative fees and an annual commitment fee of 0.06% of the undrawn amount of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate equal to the higher of the federal funds rate or LIBOR reference rate plus an agreed-upon spread.

The fund had no borrowings outstanding at October 31, 2014, or at any time during the period then ended.

9. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses) and shareholder reporting. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. Wellington Management Company, LLP, and Pzena Investment Management, LLC, each provide investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee of Wellington Management Company, LLP, is subject to quarterly adjustments based on performance for the preceding three years relative to the S&P 500 Index. The basic fee of Pzena Investment Management, LLC, is subject to quarterly adjustments based on performance since October 31, 2012, relative to the Russell 1000 Value Index.

The Vanguard Group manages the cash reserves of the fund on an at-cost basis.

For the year ended October 31, 2014, the aggregate investment advisory fee represented an effective annual basic rate of 0.13% of the fund’s average net assets, before an increase of $4,612,000 (0.03%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund based on methods approved by the board of trustees. The fund has committed to invest up to 0.40% of its net assets in Vanguard. At October 31, 2014, the fund had contributed capital of $1,781,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.71% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the year ended October 31, 2014, these arrangements reduced the fund’s expenses by $231,000 (an annual rate of 0.00% of average net assets).

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

25

Windsor Fund

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

| | | |

The following table summarizes the market value of the fund’s investments as of October 31, 2014, based on the inputs used to value them:

|

|

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 16,995,585 | 618,280 | — |

| Temporary Cash Investments | 289,984 | 230,599 | — |

| Futures Contracts—Assets1 | 2,020 | — | — |

| Futures Contracts—Liabilities1 | (46) | — | — |

| Total | 17,287,543 | 848,879 | — |

| 1 Represents variation margin on the last day of the reporting period. |

F. At October 31, 2014, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | | ($000) |

| | | | Aggregate | |

| | | Number of | Settlement | Unrealized |

| | | Long (Short) | Value | Appreciation |

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| E-mini S&P 500 Index | December 2014 | 1,378 | 138,585 | 4,731 |

| S&P 500 Index | December 2014 | 63 | 31,680 | 554 |

| | | | | 5,285 |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

During the year ended October 31, 2014, the fund realized net foreign currency losses of $376,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized gains to undistributed net investment income.

The fund used a tax accounting practice to treat a portion of the price of capital shares redeemed during the year as distributions from realized capital gains. Accordingly, the fund has reclassified $29,704,000 from accumulated net realized gains to paid-in capital.

26

Windsor Fund

The fund used capital loss carryforwards of $774,686,000 to offset taxable capital gains realized during the year ended October 31, 2014, reducing the amount of capital gains that would otherwise be available to distribute to shareholders. For tax purposes, at October 31, 2014, the fund had $80,322,000 of ordinary income and $790,138,000 of long-term capital gains available for distribution.

At October 31, 2014, the cost of investment securities for tax purposes was $13,895,637,000. Net unrealized appreciation of investment securities for tax purposes was $4,238,811,000, consisting of unrealized gains of $4,554,912,000 on securities that had risen in value since their purchase and $316,101,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the year ended October 31, 2014, the fund purchased $6,368,949,000 of investment securities and sold $6,524,853,000 of investment securities, other than temporary cash investments.

I. Capital share transactions for each class of shares were:

| | | | | |

| | | | | Year Ended October 31, |

| | | 2014 | | | 2013 |

| | Amount | Shares | | Amount | Shares |

| | ($000) | (000) | | ($000) | (000) |

| Investor Shares | | | | | |

| Issued | 534,926 | 25,704 | | 628,746 | 36,860 |

| Issued in Lieu of Cash Distributions | 89,500 | 4,227 | | 107,480 | 6,843 |

| Redeemed | (1,434,685) | (68,755) | | (2,365,686) | (135,989) |

| Net Increase (Decrease)—Investor Shares | (810,259) | (38,824) | | (1,629,460) | (92,286) |

| Admiral Shares | | | | | |

| Issued | 1,389,863 | 19,755 | | 1,967,049 | 33,059 |

| Issued in Lieu of Cash Distributions | 128,650 | 1,799 | | 100,424 | 1,885 |

| Redeemed | (973,030) | (13,763) | | (748,983) | (13,120) |

| Net Increase (Decrease) —Admiral Shares | 545,483 | 7,791 | | 1,318,490 | 21,824 |

J. Management has determined that no material events or transactions occurred subsequent to October 31, 2014, that would require recognition or disclosure in these financial statements.

27

Report of Independent Registered

Public Accounting Firm

To the Board of Trustees of Vanguard Windsor Funds and the Shareholders of Vanguard Windsor Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard Windsor Fund (constituting a separate portfolio of Vanguard Windsor Funds, hereafter referred to as the “Fund”) at October 31, 2014, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2014 by correspondence with the custodians and brokers, by agreement to the underlying ownership records of the transfer agent and the application of alternative auditing procedures where securities purchased had not been received, provide a reasonable basis for our opinion.

/s/PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

December 11, 2014

| |

| Special 2014 tax information (unaudited) for Vanguard Windsor Fund |

This information for the fiscal year ended October 31, 2014, is included pursuant to provisions of the Internal Revenue Code.

The fund distributed $29,704,000 as capital gain dividends (from net long-term capital gains) to shareholders during the fiscal year.

The fund distributed $231,070,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 82.6% of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

28

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2014. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

The table shows returns for Investor Shares only; returns for other share classes will differ. Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| | | | |

| Average Annual Total Returns: Windsor Fund Investor Shares | | | |

| Periods Ended October 31, 2014 | | | |

| |

| | One | Five | Ten |

| | Year | Years | Years |

| Returns Before Taxes | 14.14% | 16.65% | 7.55% |

| Returns After Taxes on Distributions | 13.80 | 16.35 | 6.78 |

| Returns After Taxes on Distributions and Sale of Fund Shares | 8.26 | 13.50 | 6.13 |

29

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

30

| | | |

| Six Months Ended October 31, 2014 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Windsor Fund | 4/30/2014 | 10/31/2014 | Period |

| Based on Actual Fund Return | | | |

| Investor Shares | $1,000.00 | $1,049.54 | $2.01 |

| Admiral Shares | 1,000.00 | 1,049.91 | 1.50 |

| Based on Hypothetical 5% Yearly Return | | | |

| Investor Shares | $1,000.00 | $1,023.24 | $1.99 |

| Admiral Shares | 1,000.00 | 1,023.74 | 1.48 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for that period are 0.39% for Investor Shares and 0.29% for Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

31

Glossary