GALAPAGOS PARTNERS SELECT EQUITY FUND |

LETTER TO SHAREHOLDERS | June 15, 2016 |

Dear Fellow Galapagos Partners Select Equity Fund Shareholder:

I am pleased to report on our performance and investment outlook for the fiscal period ended May 31, 2016.

PERFORMANCE SUMMARY

From inception on December 30, 2014 through May 31, 2016, the Galapagos Partners Select Equity Fund (the “Fund”) delivered a return of -10.30% versus a benchmark return of +0.01% for the Russell 3000 Index (the ���Russell”) and +3.92% for the S&P 500 TR Index (the S&P 500). For the six months ended May 31, 2016, the Fund delivered a return of -7.05% versus a benchmark return of +1.29% for the Russell and +1.93% for the S&P 500. The Fund’s underperformance for the six month period is largely due to an overweight energy allocation during the oil bear market, however some of that underperformance has been made up recently with oil prices rising.

GALAPAGOS PARTNERS’ PHILOSOPHY

The Fund seeks to outperform its benchmark by targeting investments that include a number of firms whose share prices might be influenced by high insider buying, spun-off divisions, reduced float, and activist shareholders, as well as by focusing on firms with strong valuations or growth potential, such as those companies exhibiting strong free cash flow and/or dividend growth. This is the adviser’s long-term thesis. Additionally, we will rotate into sectors or countries across the globe depending upon the adviser’s perceived opportunities.

INVESTMENT ENVIRONMENT

There is a large difference in opinion in the economy amongst analysts. The Federal Reserve (the “Fed”) believes that the economy is strong enough for one or two rate hikes in 2016, down from their projection of four at the beginning of the year. However, the Fed fund futures market is projecting less than a 50% chance of a single rate hike this year.

The Fed is stuck in a cycle that will make it difficult for them to raise rates. The issue is that as the Fed becomes more hawkish, investors grow concerned with a stronger dollar and tightening conditions. This inevitably leads to an equity pullback where the Fed has to calm investors down by being more accommodative. The more dovish positioning causes the dollar to fall and conditions to ease, with equities usually rallying as a result. The cycle then repeats itself.

It is unclear which direction the market will head at this point. Folks who are bearish have many arguments including elevated stock market valuations, several quarters of declining earnings, Brexit, increasing debt around the world along with negative interest rates, companies buying back their stock instead of reinvesting or paying down debt,

1

etc. Folks who are bullish can point to the lack of attractive alternatives due to interest rates levels, oil prices stabilizing, earnings expecting to improve in the back half of the year, high inflation tail risk, and the level of bearishness currently in the market usually being a contrarian indicator.

PERFORMANCE DISCUSSION

The Fund performed below expectations for the six-month period ended May 31, 2016 but has been doing better recently. The underperformance occurred in late 2015 and during the beginning of 2016 as the price of oil collapsed. The Fund was overweight energy at the time, which hurt performance but we think the Fund’s positioning will pay off in the long term as oil prices recover. The Fund underperformed its benchmarks during the period as the Fund was down 7.05% compared to +1.29% for the Russell and +1.93% for the S&P 500.

The Fund’s biggest winners and losers based on contribution to return were mostly in the energy space. The biggest winner for the Fund over this timeframe was Energy Transfer Partners (ETP). We saw ETP as a quality name that was oversold and took advantage. It was bought for just under $20 and sold for almost $29 a few weeks later. ETP was a short term trade because we already had a large allocation to Energy Transfer Equity (ETE), which is the parent company of ETP and has the potential for larger price appreciation. The other biggest winners were Enterprise Product Partners (EPD) and Great Western Bancorp (GWB). EPD is another energy name that benefitted from the upturn in oil prices and having a strong balance sheet. GWB is a well-managed regional bank that has been making all-time highs after declining with the rest of the bank sector at the start of the year.

The Fund’s biggest losers for the period were Kinder Morgan (KMI), Energy Transfer Equity (ETE), and Palo Alto Networks (PANW). KMI and ETE suffered as energy prices collapsed. We sold the Fund’s position in KMI after management cut its dividend by 75%. We remain invested in ETE as we believe there is still large upside, however we have reduced the size of this position as there is still risk with the Williams merger and it is 200% off its low. PANW is a high growth company but its growth expectations have recently suffered. We sold the Fund’s position due to the changed outlook and because it is a high beta stock that will suffer if there is a big downturn.

Given the Fund’s portfolio characteristics, we are confident that the Fund owns better companies, on average, than the market. The portfolio characteristics are shown below:

* | Bench represents the S&P 500 in the table above |

2

INVESTMENT OUTLOOK

It is unclear which direction the market will head at this point, but we continue to believe that our focus on selecting a portfolio with superior valuation metrics will lead to shareholder value over the long-term.

Sincerely,

Stephen Lack

Managing Partner/Chief Investment Officer

Galapagos Partners L.P.

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-800-592-7722.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus, please visit our website at www.apexcmfund.com or call 1-800-592-7722 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Galapagos Partners Select Equity Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. For a complete list of securities held by the Fund as of May 31, 2016, please see the Schedule of Investments section of the Semi-Annual Report. The opinions of the Adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

GALAPAGOS PARTNERS SELECT EQUITY FUND

PORTFOLIO INFORMATION

May 31, 2016 (Unaudited)

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

Security Description | % of

Net Assets |

Enterprise Products Partners, L.P. | 7.1% |

Alerian MLP ETF | 3.8% |

Great Western Bancorp, Inc. | 2.9% |

Boeing Company (The) | 2.8% |

CGI Group, Inc. - Class A | 2.7% |

Star Gas Partners, L.P. | 2.6% |

F5 Networks, Inc. | 2.4% |

RMR Group, Inc. (The) - Class A | 2.4% |

Lincoln National Corporation | 2.3% |

Energy Transfer Equity, L.P. | 2.3% |

4

GALAPAGOS PARTNERS SELECT EQUITY FUND

SCHEDULE OF INVESTMENTS

May 31, 2016 (Unaudited) |

COMMON STOCKS — 79.8% | | Shares | | | Value | |

Consumer Discretionary — 6.1% | | | | | | |

Auto Components — 2.1% | | | | | | |

Lear Corporation | | | 571 | | | $ | 67,812 | |

| | | | | | | | | |

Automobiles — 2.0% | | | | | | | | |

General Motors Company | | | 2,063 | | | | 64,531 | |

| | | | | | | | | |

Multi-line Retail — 2.0% | | | | | | | | |

Target Corporation | | | 927 | | | | 63,759 | |

| | | | | | | | | |

Consumer Staples — 2.0% | | | | | | | | |

Food & Staples Retailing — 2.0% | | | | | | | | |

Wal-Mart Stores, Inc. | | | 902 | | | | 63,844 | |

| | | | | | | | | |

Energy — 13.5% | | | | | | | | |

Energy Equipment & Services — 0.1% | | | | | | | | |

SAExploration Holdings, Inc. (a) | | | 4,006 | | | | 2,283 | |

| | | | | | | | | |

Oil, Gas & Consumable Fuels — 13.4% | | | | | | | | |

Diamondback Energy, Inc. (a) | | | 713 | | | | 64,847 | |

Energy Transfer Equity, L.P. | | | 5,786 | | | | 73,135 | |

Enterprise Products Partners, L.P. | | | 8,185 | | | | 227,216 | |

Valero Energy Corporation | | | 1,184 | | | | 64,765 | |

| | | | | | | | 429,963 | |

Financials — 19.9% | | | | | | | | |

Banks — 6.8% | | | | | | | | |

Great Western Bancorp, Inc. | | | 2,744 | | | | 93,351 | |

JPMorgan Chase & Company | | | 991 | | | | 64,683 | |

Sierra Bancorp | | | 3,530 | | | | 60,963 | |

| | | | | | | | 218,997 | |

Insurance — 6.3% | | | | | | | | |

AmTrust Financial Services, Inc. | | | 2,414 | | | | 64,019 | |

Lincoln National Corporation | | | 1,619 | | | | 74,231 | |

Prudential Financial, Inc. | | | 811 | | | | 64,272 | |

| | | | | | | | 202,522 | |

Real Estate Investment Trusts (REITs) — 4.5% | | | | | | | | |

Ares Commercial Real Estate Corporation | | | 5,761 | | | | 69,017 | |

RMR Group, Inc. (The) - Class A | | | 2,571 | | | | 76,204 | |

| | | | | | | | 145,221 | |

5

GALAPAGOS PARTNERS SELECT EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 79.8% (Continued) | | Shares | | | Value | |

Financials — 19.9% (Continued) | | | | | | |

Thrifts & Mortgage Finance — 2.3% | | | | | | |

Essent Group Ltd. (a) | | | 3,273 | | | $ | 71,548 | |

| | | | | | | | | |

Health Care — 14.9% | | | | | | | | |

Biotechnology — 3.9% | | | | | | | | |

Gilead Sciences, Inc. | | | 747 | | | | 65,034 | |

United Therapeutics Corporation (a) | | | 517 | | | | 61,559 | |

| | | | | | | | 126,593 | |

Health Care Providers & Services — 4.4% | | | | | | | | |

Cigna Corporation | | | 537 | | | | 68,795 | |

McKesson Corporation | | | 393 | | | | 71,974 | |

| | | | | | | | 140,769 | |

Life Sciences Tools & Services — 4.4% | | | | | | | | |

ICON plc (a) | | | 1,024 | | | | 72,130 | |

INC Research Holdings, Inc. - Class A (a) | | | 1,570 | | | | 68,311 | |

| | | | | | | | 140,441 | |

Pharmaceuticals — 2.2% | | | | | | | | |

Taro Pharmaceutical Industries Ltd. (a) | | | 494 | | | | 72,183 | |

| | | | | | | | | |

Industrials — 7.7% | | | | | | | | |

Aerospace & Defense — 7.2% | | | | | | | | |

Boeing Company (The) | | | 717 | | | | 90,449 | |

Huntington Ingalls Industries, Inc. | | | 464 | | | | 71,182 | |

Spirit AeroSystems Holdings, Inc. - Class A (a) | | | 1,487 | | | | 69,562 | |

| | | | | | | | 231,193 | |

Marine — 0.5% | | | | | | | | |

Pangaea Logistics Solutions Ltd. (a) | | | 6,700 | | | | 15,343 | |

| | | | | | | | | |

Information Technology — 11.0% | | | | | | | | |

Communications Equipment — 2.4% | | | | | | | | |

F5 Networks, Inc. (a) | | | 699 | | | | 77,030 | |

| | | | | | | | | |

IT Services — 2.7% | | | | | | | | |

CGI Group, Inc. - Class A (a) | | | 1,838 | | | | 85,982 | |

| | | | | | | | | |

Software — 5.9% | | | | | | | | |

Check Point Software Technologies Ltd. (a) | | | 744 | | | | 63,218 | |

CyberArk Software Ltd. (a) | | | 1,415 | | | | 64,269 | |

FireEye, Inc. (a) | | | 3,993 | | | | 63,569 | |

| | | | | | | | 191,056 | |

6

GALAPAGOS PARTNERS SELECT EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 79.8% (Continued) | | Shares | | | Value | |

Materials — 2.1% | | | | | | |

Chemicals — 2.1% | | | | | | |

Trinseo S.A. (a) | | | 1,412 | | | $ | 66,491 | |

| | | | | | | | | |

Utilities — 2.6% | | | | | | | | |

Gas Utilities — 2.6% | | | | | | | | |

Star Gas Partners, L.P. | | | 9,831 | | | | 84,448 | |

| | | | | | | | | |

Total Common Stocks (Cost $2,505,659) | | | | | | $ | 2,562,009 | |

| |

EXCHANGE-TRADED FUNDS — 3.8% | | Shares | | | Value | |

Energy — 3.8% | | | | | | |

Alerian MLP ETF (Cost $120,777) | | | 9,915 | | | $ | 121,062 | |

| |

MONEY MARKET FUNDS — 26.1% | | Shares | | | Value | |

Invesco Short-Term Investments Trust - Treasury Portfolio - Institutional Shares, 0.24% (b) (Cost $839,594) | | | 839,594 | | | $ | 839,594 | |

| | | | | | | | | |

Total Investments at Value — 109.7% (Cost $3,466,030) | | | | | | $ | 3,522,665 | |

| | | | | | | | | |

Liabilities in Excess of Other Assets — (9.7%) | | | | | | | (310,069 | ) |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 3,212,596 | |

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of May 31, 2016. |

See accompanying notes to financial statements. |

7

GALAPAGOS PARTNERS SELECT EQUITY FUND

STATEMENT OF ASSETS AND LIABILITIES

May 31, 2016 (Unaudited) |

ASSETS | | | |

Investments in securities: | | | |

At acquisition cost | | $ | 3,466,030 | |

At value (Note 2) | | $ | 3,522,665 | |

Dividends receivable | | | 1,719 | |

Receivable from Adviser (Note 4) | | | 8,827 | |

Other assets | | | 8,570 | |

Total assets | | | 3,541,781 | |

| | | | | |

LIABILITIES | | | | |

Payable for investment securities purchased | | | 319,832 | |

Payable to administrator (Note 4) | | | 6,530 | |

Other accrued expenses | | | 2,823 | |

Total liabilities | | | 329,185 | |

| | | | | |

NET ASSETS | | $ | 3,212,596 | |

| | | | | |

NET ASSETS CONSIST OF: | | | | |

Paid-in capital | | $ | 3,864,967 | |

Accumulated net investment income | | | 34,925 | |

Accumulated net realized losses from security transactions | | | (743,931 | ) |

Net unrealized appreciation on investments | | | 56,635 | |

NET ASSETS | | $ | 3,212,596 | |

| | | | | |

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | | | 358,024 | |

| | | | | |

Net asset value, offering price and redemption price per share (Note 2) | | $ | 8.97 | |

See accompanying notes to financial statements. |

8

GALAPAGOS PARTNERS SELECT EQUITY FUND

STATEMENT OF OPERATIONS

For the Six Months Ended May 31, 2016 (Unaudited) |

INVESTMENT INCOME | | | |

Dividend income | | $ | 47,473 | |

| | | | | |

EXPENSES | | | | |

Investment advisory fees (Note 4) | | | 21,139 | |

Professional fees | | | 16,060 | |

Fund accounting fees (Note 4) | | | 13,176 | |

Administration fees (Note 4) | | | 13,000 | |

Compliance fees (Note 4) | | | 6,000 | |

Transfer agent fees (Note 4) | | | 6,000 | |

Trustees' fees and expenses (Note 4) | | | 5,597 | |

Registration and filing fees | | | 4,146 | |

Custody and bank service fees | | | 3,651 | |

Printing of shareholder reports | | | 2,992 | |

Insurance expense | | | 2,060 | |

Postage and supplies | | | 1,441 | |

Other expenses | | | 3,524 | |

Total expenses | | | 98,786 | |

Less fee reductions and expense reimbursements by the Adviser (Note 4) | | | (73,419 | ) |

Net expenses | | | 25,367 | |

| | | | | |

NET INVESTMENT INCOME | | | 22,106 | |

| | | | | |

REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | | | | |

Net realized losses from security transactions | | | (260,867 | ) |

Net change in unrealized appreciation (depreciation) on investments | | | (84,027 | ) |

NET REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | | | (344,894 | ) |

| | | | | |

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (322,788 | ) |

See accompanying notes to financial statements. |

9

GALAPAGOS PARTNERS SELECT EQUITY FUND

STATEMENTS OF CHANGES IN NET ASSETS |

| | Six Months

Ended

May 31, 2016

(Unaudited) | | | Period Ended

November 30, 2015 (a) | |

FROM OPERATIONS | | | | | | |

Net investment income | | $ | 22,106 | | | $ | 8,525 | |

Net realized losses from security transactions | | | (260,867 | ) | | | (484,299 | ) |

Net change in unrealized appreciation (depreciation) on investments | | | (84,027 | ) | | | 140,662 | |

Net decrease in net assets resulting from operations | | | (322,788 | ) | | | (335,112 | ) |

| | | | | | | | | |

CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 31,237 | | | | 5,036,117 | |

Payments for shares redeemed | | | (653,003 | ) | | | (543,855 | ) |

Net increase (decrease) in net assets resulting from capital share transactions | | | (621,766 | ) | | | 4,492,262 | |

| | | | | | | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | | | (944,554 | ) | | | 4,157,150 | |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of period | | | 4,157,150 | | | | — | |

End of period | | $ | 3,212,596 | | | $ | 4,157,150 | |

| | | | | | | | | |

ACCUMULATED NET INVESTMENT INCOME | | $ | 34,925 | | | $ | 12,819 | |

| | | | | | | | | |

CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 3,668 | | | | 488,198 | |

Shares redeemed | | | (76,294 | ) | | | (57,548 | ) |

Net increase (decrease) in shares outstanding | | | (72,626 | ) | | | 430,650 | |

Shares outstanding at beginning of period | | | 430,650 | | | | — | |

Shares outstanding at end of period | | | 358,024 | | | | 430,650 | |

(a) | Represents the period from the commencement of operations (December 30, 2014) through November 30, 2015. |

See accompanying notes to financial statements. |

10

GALAPAGOS PARTNERS SELECT EQUITY FUND

FINANCIAL HIGHLIGHTS |

Per Share Data for a Share Outstanding Throughout Each Period |

| | Six Months

Ended

May 31, 2016

(Unaudited) | | | Period

Ended

November 30,

2015 (a) | |

Net asset value at beginning of period | | $ | 9.65 | | | $ | 10.00 | |

| | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | |

Net investment income | | | 0.07 | | | | 0.02 | |

Net realized and unrealized losses on investments | | | (0.75 | ) | | | (0.37 | ) |

Total from investment operations | | | (0.68 | ) | | | (0.35 | ) |

| | | | | | | | | |

Net asset value at end of period | | $ | 8.97 | | | $ | 9.65 | |

| | | | | | | | | |

Total return (b) | | | (7.05% | )(c) | | | (3.50% | )(c) |

| | | | | | | | | |

Net assets at end of period (000's) | | $ | 3,213 | | | $ | 4,157 | |

| | | | | | | | | |

Ratios/supplementary data: | | | | | | | | |

Ratio of total expenses to average net assets (e) | | | 5.85 | %(d) | | | 6.82 | %(d) |

| | | | | | | | | |

Ratio of net expenses to average net assets (e) (f) | | | 1.50 | %(d) | | | 1.50 | %(d) |

| | | | | | | | | |

Ratio of net investment income to average net assets (e) (f) (g) | | | 1.31 | %(d) | | | 0.38 | %(d) |

| | | | | | | | | |

Portfolio turnover rate | | | 149 | %(c) | | | 1,244 | %(c) |

(a) | Represents the period from the commencement of operations (December 30, 2014) through November 30, 2015. |

(b) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses. |

(c) | Not annualized. |

(d) | Annualized. |

(e) | Ratios do not reflect the Fund’s proportionate share of expenses of the underlying investment companies in which the Fund invests. |

(f) | Ratio was determined after advisory fee reductions and/or expense reimbursements (Note 4). |

(g) | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying investment companies in which the Fund invests. |

See accompanying notes to financial statements. |

11

GALAPAGOS PARTNERS SELECT EQUITY FUND

NOTES TO FINANCIAL STATEMENTS

May 31, 2016 (Unaudited)

1. Organization

Galapagos Partners Select Equity Fund (the “Fund”) is a diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report. The Fund commenced operations on December 30, 2014.

The investment objective of the Fund is capital appreciation.

2. Significant Accounting Policies

The following is a summary of the Fund’s significant accounting policies used in the preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). As an investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update 2013-08, the Fund follows accounting and reporting guidance under FASB Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.”

Securities valuation – The Fund values its portfolio securities at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open for business. The Fund values its listed securities on the basis of the security’s last sale price on the primary exchange, if available, otherwise at the exchange’s most recently quoted mean price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with procedures established by and under the general supervision of the Board of Trustees (the “Board”). Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s net asset value (“NAV”) may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

12

GALAPAGOS PARTNERS SELECT EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued) |

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

● | Level 1 – quoted prices in active markets for identical securities |

● | Level 2 – other significant observable inputs |

● | Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments as of May 31, 2016:

| | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Investments in Securities: | | | | | | | | | | | | |

Common Stocks | | $ | 2,562,009 | | | $ | — | | | $ | — | | | $ | 2,562,009 | |

Exchange-Traded Funds | | | 121,062 | | | | — | | | | — | | | | 121,062 | |

Money Market Funds | | | 839,594 | | | | — | | | | — | | | | 839,594 | |

Total | | $ | 3,522,665 | | | $ | — | | | $ | — | | | $ | 3,522,665 | |

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by industry type. As of May 31, 2016, the Fund did not have any transfers between Levels. In addition, the Fund did not have derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of May 31, 2016. It is the Fund’s policy to recognize transfers between Levels at the end of the reporting period.

Share valuation – The NAV per share of the Fund is calculated daily by dividing the total value of the Fund’s assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of the Fund is equal to the NAV per share.

Investment income – Dividend income is recorded on the ex-dividend date. Interest income is accrued as earned.

Security transactions – Security transactions are accounted for on the trade date. Realized gains and losses on securities sold are determined on a specific identification basis.

13

GALAPAGOS PARTNERS SELECT EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued) |

Common expenses – Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on the relative net assets of each series or the nature of the services performed and the relative applicability to each series.

Distributions to shareholders – The Fund will distribute to shareholders any net investment income and net realized capital gains at least once each year. The amount of such dividends and distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to shareholders are recorded on the ex-dividend date. There were no distributions paid to shareholders during the periods ended May31, 2016 and November 30, 2015.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax – The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986 (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of May 31, 2016:

Tax cost of portfolio investments | | $ | 3,462,371 | |

Gross unrealized appreciation | | $ | 136,920 | |

Gross unrealized depreciation | | | (76,626 | ) |

Net unrealized appreciation on investments | | | 60,294 | |

Accumulated ordinary income | | | 22,106 | |

Other losses | | | (296,321 | ) |

Capital loss carryforward | | | (438,450 | ) |

Accumulated deficit | | $ | (652,371 | ) |

14

GALAPAGOS PARTNERS SELECT EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued) |

The difference between the federal income tax cost of portfolio investments and the financial statement cost of portfolio investments is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are primarily due to the tax deferral of losses on wash sales and the tax treatment of income and capital gains on publicly-traded partnerships held by the Fund.

As of November 30, 2015, the Fund had a short-term capital loss carryforward of $438,450 for federal income tax purposes. This capital loss carryforward, which does not expire, may be utilized in the current and future years to offset net realized capital gains, if any, prior to distributing such gains to shareholders.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for the current year and the tax period ended November 30, 2015 and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Fund identifies its major tax jurisdiction as U.S. Federal.

3. Investment Transactions

During the six months ended May 31, 2016, cost of purchases and proceeds from sales of investment securities, other than short-term investments, were $4,702,309 and $5,604,322, respectively.

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by Galapagos Partners, L.P. (the “Adviser”) pursuant to the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, the Fund pays the Adviser an advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.25% of its average daily net assets.

Pursuant to an Expense Limitation Agreement (“ELA”) between the Fund and the Adviser, the Adviser has agreed, until March 31, 2017, to reduce investment advisory fees and reimburse other operating expenses to limit total annual operating expenses of the Fund (exclusive of brokerage costs, taxes, interest, costs to organize the Fund, acquired fund fees and expenses, extraordinary expenses such as litigation and merger or reorganization costs, and other expenses not incurred in the ordinary course of the Fund’s business and amounts, if any, payable pursuant to a plan adopted in accordance with Rule 12b-1 under the Investment Company Act of 1940 (the “1940 Act”), as amended) to an amount not exceeding 1.50% of the Fund’s average daily net assets. Accordingly, during the six months ended May 31, 2016, the Adviser did not collect any of its advisory fees and, in addition, reimbursed other operating expenses totaling $52,280.

15

GALAPAGOS PARTNERS SELECT EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued) |

Under the terms of the ELA, investment advisory fee reductions and expense reimbursements by the Adviser are subject to recoupment by the Adviser for a period of three years after such fees and expenses were incurred, provided the recoupments do not cause total annual operating expenses of the Fund to exceed 1.50% of the average daily net assets. As of May 31, 2016, the Adviser may seek recoupment of investment advisory fee reductions and expense reimbursements in the amount of $185,396 no later than the dates stated below:

November 30, 2018 | May 31, 2019 | Total |

$111,977 | $73,419 | $185,396 |

The principal executive officer of the Fund is also an officer of the Adviser.

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides fund administration, fund accounting, compliance and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including but not limited to postage, supplies and costs of pricing the Fund’s portfolio securities.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

Certain officers and a Trustee of the Trust are also officers of Ultimus and the Distributor.

TRUSTEE COMPENSATION

Each Trustee who is not an “interested person” of the Trust (“Independent Trustee”) receives from the Fund a fee of $500 for each Board meeting attended plus reimbursement of travel and other meeting-related expenses. Each Independent Trustee also receives a $500 annual retainer from the Fund. Trustees affiliated with the Adviser or Ultimus are not compensated by the Fund for their services.

PRINCIPAL HOLDERS OF FUND SHARES

As of May 31, 2016, the following shareholders owned of record 5% or more of the outstanding shares of the Fund:

Name of Record Owner | % Ownership |

Charles Schwab & Co., Inc. (for the benefit of its customers) | 64% |

Lack Holdings, Inc. | 14% |

Clifford B. Sondock | 6% |

Birdwood Associates Limited Partner | 6% |

16

GALAPAGOS PARTNERS SELECT EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued) |

A beneficial owner of 25% or more of the Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholder’s meeting.

5. Investments in Money Market Mutual Funds

In order to maintain sufficient liquidity to implement investment strategies, or for temporary defensive purposes, the Fund may invest a significant portion of its assets in shares of one or more money market mutual funds. As of May 31, 2016, the Fund had 26.1% of the value of its net assets invested in a single money market mutual fund registered under the 1940 Act. An investment in a money market mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency, entity or person. While investor losses in money market mutual funds have been rare, they are possible. In addition, the Fund incurs additional indirect expenses due to acquired fund fees and other costs to the extent it invests in shares of money market mutual funds.

6. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events except as reflected in the following paragraph.

Effective September 26, 2016 (the “Effective Date”) the Fund will change its name to “Galapagos Partners Select Fund” and remove the following principal investment policy: “Under normal circumstances, the Fund will invest at least 80% of its net assets (including the amount of any borrowings for investment purposes) in U.S. and foreign equity securities listed on U.S. stock exchanges.” Therefore on and after the Effective Date the Fund will no longer be required to meet the 80% investment policy.

17

GALAPAGOS PARTNERS SELECT EQUITY FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited) |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (December 1, 2015) and held until the end of the period (May 31, 2016).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the U.S. Securities and Exchange Comission (“SEC”) requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

18

GALAPAGOS PARTNERS SELECT EQUITY FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued) |

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning Account Value December 1, 2015 | Ending Account Value May 31, 2016 | Net

Expense Ratio (a) | Expenses Paid During Period (b) |

Based on Actual Fund Return | $ 1,000.00 | $ 929.50 | 1.50% | $ 7.24 |

Based on Hypothetical 5% Return (before expenses) | $ 1,000.00 | $ 1,017.50 | 1.50% | $ 7.57 |

(a) | Annualized, based on the Fund’s most recent one-half year expenses. |

(b) | Expenses are equal to the Fund’s annualized net expense ratio multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half year period). |

OTHER INFORMATION (Unaudited)

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-800-592-7722, or on the SEC’s website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-800-592-7722, or on the SEC’s website at http://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. These filings are available upon request by calling 1-800-592-7722. Furthermore, you may obtain a copy of the filings on the SEC’s website at http://www.sec.gov. The Trust’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

19

This Page Intentionally Left Blank

This Page Intentionally Left Blank

LYRICAL U.S. VALUE EQUITY FUND

Institutional Class (LYRIX)

Investor Class (LYRBX)

LYRICAL U.S. HEDGED VALUE FUND

Institutional Class (LYRHX)

Investor Class (LYRDX)

Semi-Annual Report

May 31, 2016

(Unaudited)

LYRICAL FUNDS

LETTER TO SHAREHOLDERS | June 13, 2016 |

Dear Fellow Shareholders,

Enclosed is the semi-annual report to shareholders of the Lyrical U.S. Value Equity Fund (the “Value Fund”) and Lyrical U.S. Hedged Value Fund (the “Hedged Value Fund”) (collectively, the “Funds”). On behalf of the Funds and their investment adviser, Lyrical Asset Management LP, I would like to thank you for your investment.

Lyrical U.S. Value Equity Fund

Since its launch on February 4, 2013 through the period ended May 31, 2016, the Value Fund – Institutional Class has produced a cumulative total return of +60.42%, compared to the +50.49% cumulative total return for the S&P 500 Index (the “S&P 500”). For the six months ended May 31, 2016, the Value Fund – Institutional Class produced a total return of -0.60% compared to the total return for the S&P 500 of +1.93%. The Value Fund’s biggest winners for the six month period ended May 31, 2016 were AVGO (+19%), NCR (+14%), and GLW (+13%). The biggest losers were HTZ (-39%), WDC (-24%) and ARRS (-21%). The Value Fund maintains its positions in all of these largest winners and detractors.

In analyzing the Value Fund’s portfolio’s performance attribution, we find it helpful to examine both the investment success rate and any skew in the distribution of returns. Our success rate has been high over the life of the Value Fund, as 77% of the Fund’s investments posted gains, and 63% outperformed the S&P 500. Skew has also been a positive factor, as the Fund’s outperformers have outperformed by 44%, while our underperformers have underperformed by 37%. For the six month period ended May 31, 2016, the Value Fund’s underperformance is explained by a lower success rate, as only 53% of the Fund’s investments posted gains, and only 41% outperformed the S&P 500. For the six month period skew has been a negative factor as the Fund’s outperformers have outperformed by 7%, while our underperformers have underperformed by 12%.

During the life of the Value Fund we have sold fourteen positions, as four companies announced they were being acquired, nine approached our estimates of fair value, and for one we lost conviction in our thesis. For each sale we added a new position from our pipeline of opportunities. We are still finding attractive stock opportunities to add to the portfolio, even as some of our existing positions begin to approach our estimates of fair value.

As of the reporting date, the valuation of the Value Fund’s portfolio is 13.0x next twelve months consensus earnings. The S&P 500 has a valuation of 16.6x on this same basis, a premium of 28%.

Lyrical U.S. Hedged Value Fund

In July 2014, we launched the Hedged Value Fund as a liquid alternatives product that employs a similar long portfolio as the Value Fund. Sector ETF hedges are used on the short side to create a portfolio that aims to maintain net long exposures of 50%. This provides a hedged option for those wishing exposure to the long portfolio but unwilling to accept unhedged equity market exposure.

1

Since its launch on July 14, 2014 through May 31, 2016, the Hedged Value Fund – Institutional Class has produced a cumulative total return of -6.14%, compared to the +10.39% cumulative total return for the S&P 500. For the six months ended May 31, 2016, the Hedged Value Fund – Institutional Class produced a total return of -0.69% compared to the total return for the S&P 500 of +1.93%. In rising equity markets one should expect Hedged Value Fund’s performance to lag that of the S&P 500, as it did for both the above periods, as the Fund’s hedges detract from total return.

Lyrical Asset Management’s Investment Philosophy and Portfolio Construction

As there have been a significant number of new investors since our previous letter to the Funds’ shareholders, we’d like to briefly outline our investment philosophy and portfolio construction approach.

We believe our strategy and approach to investing differentiates us from other investment managers, even those that share a value approach to investing. We are deep value investors and by this we mean that we look to invest in companies that trade significantly below intrinsic value. This separates us from other value managers who focus on relative value or core value approaches and whose portfolio characteristics have higher Price/Earnings, Price/Book and Price/Cash Flow multiples. We assess valuation based on current price relative to long-term normalized earnings, which contrasts us to those that rely on Price/Book or dividend yield. We only invest in what we consider to be quality businesses that we believe should earn good returns on invested capital, and avoid volatile businesses and companies with excessive leverage. Other value investors may consider owning any business regardless of quality if they believe the price is low enough. Lastly, we only invest in businesses we can understand, and avoid those that are excessively complex or require specialized technical knowledge, even though they may appear cheap from a high-level perspective.

We construct our portfolio purely bottom up and without regard to what is or is not contained in a benchmark. We are concerned with concentration risk, and have strict limits on how much capital can be invested in any one position or any one industry. Our long portfolio is constructed to be diversified across approximately 33 positions, giving us exposure to many different types of companies and situations without sacrificing our strict investment standards.

Thank you for your continued trust and interest in Lyrical Asset Management.

Sincerely,

Andrew Wellington

Portfolio Manager

2

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-888-884-8099.

An investor should consider the investment objectives, risks, charges and expenses of the Funds carefully before investing. The Funds’ prospectus contains this and other important information. To obtain a copy of the Funds’ prospectus please call 1-888-884-8099 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Funds are distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Funds that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Funds, may be sold at any time, and may no longer be held by the Funds. For a complete list of securities held by the Funds as of May 31, 2016, please see the Schedules of Investments and Schedule of Securities Sold Short sections of the Semi-Annual Report. The opinions of the Funds’ adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Funds and the market in general and statements of the Funds’ plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

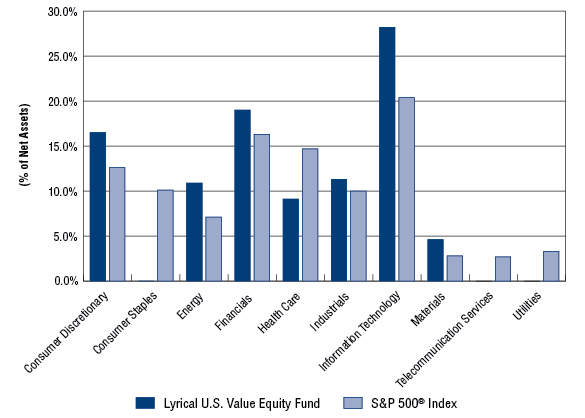

LYRICAL U.S. VALUE EQUITY FUND

PORTFOLIO INFORMATION

May 31, 2016 (Unaudited)

Lyrical U.S. Value Equity Fund vs S&P 500® Index

Sector Diversification

Top Ten Equity Holdings

Security Description | % of

Net Assets |

Broadcom Ltd. | 6.4% |

Aetna, Inc. | 4.9% |

Aflac, Inc. | 4.7% |

Comcast Corporation - Class A | 4.6% |

Corning, Inc. | 4.4% |

Johnson Controls, Inc. | 4.2% |

Anthem, Inc. | 4.2% |

Eaton Corporation plc | 4.2% |

Liberty Interactive Corporation QVC Group - Series A | 4.1% |

EOG Resources, Inc. | 4.0% |

4

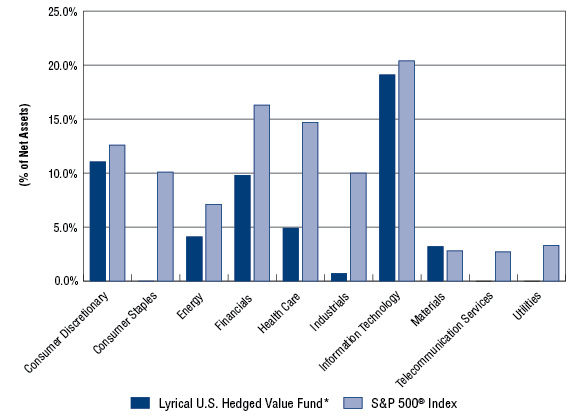

LYRICAL U.S. HEDGED VALUE FUND

PORTFOLIO INFORMATION

May 31, 2016 (Unaudited)

Lyrical U.S. Hedged Value Fund vs S&P 500® Index

Sector Diversification

* | The percentages above for Lyrical U.S. Hedged Value Fund represent the net percentages for the Fund and are computed by taking the net dollar exposure, including short positions, and dividing by the net assets of the Fund. |

Top Ten Long Positions

Security Description | % of

Net Assets |

Broadcom Ltd. | 8.5% |

Aetna, Inc. | 5.9% |

Comcast Corporation - Class A | 5.2% |

Aflac, Inc. | 5.0% |

Anthem, Inc. | 4.9% |

Corning, Inc. | 4.4% |

TE Connectivity Ltd. | 4.3% |

Liberty Interactive Corporation QVC Group - Series A | 4.3% |

Johnson Controls, Inc. | 4.1% |

Celanese Corporation - Series A | 4.0% |

5

LYRICAL U.S. VALUE EQUITY FUND

SCHEDULE OF INVESTMENTS

May 31, 2016 (Unaudited) | |

COMMON STOCKS — 99.6% | | Shares | | | Value | |

Consumer Discretionary — 16.5% | | | | | | |

Auto Components — 7.8% | | | | | | |

Goodyear Tire & Rubber Company (The) | | | 910,780 | | | $ | 25,474,517 | |

Johnson Controls, Inc. | | | 984,328 | | | | 43,458,081 | |

Tenneco, Inc. (a) | | | 204,299 | | | | 10,974,942 | |

| | | | | | | | 79,907,540 | |

Internet & Catalog Retail — 4.1% | | | | | | | | |

Liberty Interactive Corporation QVC Group - Series A (a) | | | 1,567,535 | | | | 42,292,094 | |

| | | | | | | | | |

Media — 4.6% | | | | | | | | |

Comcast Corporation - Class A | | | 756,877 | | | | 47,910,314 | |

| | | | | | | | | |

Energy — 10.9% | | | | | | | | |

Energy Equipment & Services — 3.0% | | | | | | | | |

National Oilwell Varco, Inc. | | | 929,787 | | | | 30,636,482 | |

| | | | | | | | | |

Oil, Gas & Consumable Fuels — 7.9% | | | | | | | | |

EOG Resources, Inc. | | | 504,560 | | | | 41,051,002 | |

Suncor Energy, Inc. | | | 1,469,419 | | | | 40,629,435 | |

| | | | | | | | 81,680,437 | |

Financials — 19.0% | | | | | | | | |

Capital Markets — 3.8% | | | | | | | | |

Ameriprise Financial, Inc. | | | 388,340 | | | | 39,482,528 | |

| | | | | | | | | |

Insurance — 15.2% | | | | | | | | |

Aflac, Inc. | | | 700,437 | | | | 48,652,354 | |

AmTrust Financial Services, Inc. | | | 562,749 | | | | 14,924,104 | |

Assurant, Inc. | | | 236,058 | | | | 20,629,109 | |

Lincoln National Corporation | | | 762,490 | | | | 34,960,166 | |

Willis Towers Watson plc | | | 287,204 | | | | 36,767,856 | |

| | | | | | | | 155,933,589 | |

Health Care — 9.1% | | | | | | | | |

Health Care Providers & Services — 9.1% | | | | | | | | |

Aetna, Inc. | | | 442,960 | | | | 50,156,361 | |

Anthem, Inc. | | | 326,832 | | | | 43,194,117 | |

| | | | | | | | 93,350,478 | |

Industrials — 11.3% | | | | | | | | |

Construction & Engineering — 1.4% | | | | | | | | |

AECOM (a) | | | 459,439 | | | | 14,752,586 | |

6

LYRICAL U.S. VALUE EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 99.6% (Continued) | | Shares | | | Value | |

Industrials — 11.3% (Continued) | | | | | | |

Electrical Equipment — 4.2% | | | | | | |

Eaton Corporation plc | | | 694,132 | | | $ | 42,779,355 | |

| | | | | | | | | |

Road & Rail — 2.5% | | | | | | | | |

Avis Budget Group, Inc. (a) | | | 355,287 | | | | 10,658,610 | |

Hertz Global Holdings, Inc. (a) | | | 1,514,877 | | | | 14,679,158 | |

| | | | | | | | 25,337,768 | |

Trading Companies & Distributors — 3.2% | | | | | | | | |

AerCap Holdings N.V. (a) | | | 709,541 | | | | 27,735,958 | |

MRC Global, Inc. (a) | | | 353,817 | | | | 5,020,663 | |

| | | | | | | | 32,756,621 | |

Information Technology — 28.2% | | | | | | | | |

Communications Equipment — 1.2% | | | | | | | | |

ARRIS International plc (a) | | | 499,550 | | | | 12,039,155 | |

| | | | | | | | | |

Electronic Equipment, Instruments & Components — 8.3% | | | | | | | | |

Corning, Inc. | | | 2,153,743 | | | | 44,991,691 | |

TE Connectivity Ltd. | | | 682,914 | | | | 40,974,840 | |

| | | | | | | | 85,966,531 | |

IT Services — 3.4% | | | | | | | | |

Western Union Company (The) | | | 1,795,413 | | | | 34,920,783 | |

| | | | | | | | | |

Semiconductors & Semiconductor Equipment — 7.5% | | | | | | | | |

Broadcom Ltd. | | | 423,746 | | | | 65,409,433 | |

Microsemi Corporation (a) | | | 336,589 | | | | 11,386,806 | |

| | | | | | | | 76,796,239 | |

Software — 3.3% | | | | | | | | |

Symantec Corporation | | | 1,973,017 | | | | 34,251,575 | |

| | | | | | | | | |

Technology Hardware, Storage & Peripherals — 4.5% | | | | | | | | |

NCR Corporation (a) | | | 572,816 | | | | 17,688,558 | |

Western Digital Corporation | | | 606,956 | | | | 28,247,732 | |

| | | | | | | | 45,936,290 | |

Materials — 4.6% | | | | | | | | |

Chemicals — 3.6% | | | | | | | | |

Celanese Corporation - Series A | | | 518,279 | | | | 36,528,304 | |

| | | | | | | | | |

Containers & Packaging — 1.0% | | | | | | | | |

Owens-Illinois, Inc. (a) | | | 564,093 | | | | 10,661,358 | |

| | | | | | | | | |

Total Common Stocks (Cost $982,282,103) | | | | | | $ | 1,023,920,027 | |

7

LYRICAL U.S. VALUE EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued) | |

MONEY MARKET FUNDS — 0.5% | | Shares | | | Value | |

Fidelity Institutional Money Market Portfolio - Class I, 0.33% (b) (Cost $5,549,908) | | | 5,549,908 | | | $ | 5,549,908 | |

| | | | | | | | | |

Total Investments at Value — 100.1% (Cost $987,832,011) | | | | | | $ | 1,029,469,935 | |

| | | | | | | | | |

Liabilities in Excess of Other Assets — (0.1%) | | | | | | | (1,269,700 | ) |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 1,028,200,235 | |

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of May 31, 2016. |

See accompanying notes to financial statements. |

8

LYRICAL U.S. HEDGED VALUE FUND

SCHEDULE OF INVESTMENTS

May 31, 2016 (Unaudited) | |

COMMON STOCKS — 103.8% | | Shares | | | Value | |

Consumer Discretionary — 17.3% | | | | | | |

Auto Components — 7.8% | | | | | | |

Goodyear Tire & Rubber Company (The) (a) | | | 1,288 | | | $ | 36,025 | |

Johnson Controls, Inc. (a) | | | 1,248 | | | | 55,099 | |

Tenneco, Inc. (b) | | | 283 | | | | 15,203 | |

| | | | | | | | 106,327 | |

Internet & Catalog Retail — 4.3% | | | | | | | | |

Liberty Interactive Corporation QVC Group - Series A (a)(b) | | | 2,156 | | | | 58,169 | |

| | | | | | | | | |

Media — 5.2% | | | | | | | | |

Comcast Corporation - Class A (a) | | | 1,110 | | | | 70,263 | |

| | | | | | | | | |

Energy — 9.0% | | | | | | | | |

Energy Equipment & Services — 2.1% | | | | | | | | |

National Oilwell Varco, Inc. (a) | | | 871 | | | | 28,699 | |

| | | | | | | | | |

Oil, Gas & Consumable Fuels — 6.9% | | | | | | | | |

EOG Resources, Inc. (a) | | | 585 | | | | 47,596 | |

Suncor Energy, Inc. (a) | | | 1,657 | | | | 45,816 | |

| | | | | | | | 93,412 | |

Financials — 19.3% | | | | | | | | |

Capital Markets — 3.8% | | | | | | | | |

Ameriprise Financial, Inc. (a) | | | 509 | | | | 51,750 | |

| | | | | | | | | |

Insurance — 15.5% | | | | | | | | |

Aflac, Inc. (a) | | | 989 | | | | 68,696 | |

AmTrust Financial Services, Inc. (a) | | | 771 | | | | 20,447 | |

Assurant, Inc. (a) | | | 352 | | | | 30,761 | |

Lincoln National Corporation | | | 1,021 | | | | 46,813 | |

Willis Towers Watson plc (a) | | | 346 | | | | 44,295 | |

| | | | | | | | 211,012 | |

Health Care — 10.8% | | | | | | | | |

Health Care Providers & Services — 10.8% | | | | | | | | |

Aetna, Inc. (a) | | | 701 | | | | 79,375 | |

Anthem, Inc. (a) | | | 507 | | | | 67,005 | |

| | | | | | | | 146,380 | |

Industrials — 11.4% | | | | | | | | |

Construction & Engineering — 1.4% | | | | | | | | |

AECOM (a)(b) | | | 577 | | | | 18,528 | |

9

LYRICAL U.S. HEDGED VALUE FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 103.8% (Continued) | | Shares | | | Value | |

Industrials — 11.4% (Continued) | | | | | | |

Electrical Equipment — 3.8% | | | | | | |

Eaton Corporation plc (a) | | | 842 | | | $ | 51,892 | |

| | | | | | | | | |

Road & Rail — 2.7% | | | | | | | | |

Avis Budget Group, Inc. (a)(b) | | | 527 | | | | 15,810 | |

Hertz Global Holdings, Inc. (a)(b) | | | 2,158 | | | | 20,911 | |

| | | | | | | | 36,721 | |

Trading Companies & Distributors — 3.5% | | | | | | | | |

AerCap Holdings N.V. (a)(b) | | | 1,052 | | | | 41,123 | |

MRC Global, Inc. (a)(b) | | | 508 | | | | 7,208 | |

| | | | | | | | 48,331 | |

Information Technology — 30.9% | | | | | | | | |

Communications Equipment — 1.2% | | | | | | | | |

ARRIS International plc (b) | | | 703 | | | | 16,943 | |

| | | | | | | | | |

Electronic Equipment, Instruments & Components — 8.7% | | | | | | | | |

Corning, Inc. (a) | | | 2,880 | | | | 60,163 | |

TE Connectivity Ltd. (a) | | | 975 | | | | 58,500 | |

| | | | | | | | 118,663 | |

IT Services — 3.8% | | | | | | | | |

Western Union Company (The) (a) | | | 2,662 | | | | 51,776 | |

| | | | | | | | | |

Semiconductors & Semiconductor Equipment — 9.7% | | | | | | | | |

Broadcom Ltd. (a) | | | 748 | | | | 115,461 | |

Microsemi Corporation (b) | | | 466 | | | | 15,765 | |

| | | | | | | | 131,226 | |

Software — 3.4% | | | | | | | | |

Symantec Corporation (a) | | | 2,628 | | | | 45,622 | |

| | | | | | | | | |

Technology Hardware, Storage & Peripherals — 4.1% | | | | | | | | |

NCR Corporation (b) | | | 836 | | | | 25,816 | |

Western Digital Corporation (a) | | | 656 | | | | 30,530 | |

| | | | | | | | 56,346 | |

Materials — 5.1% | | | | | | | | |

Chemicals — 4.0% | | | | | | | | |

Celanese Corporation - Series A (a) | | | 774 | | | | 54,551 | |

| | | | | | | | | |

Containers & Packaging — 1.1% | | | | | | | | |

Owens-Illinois, Inc. (a)(b) | | | 824 | | | | 15,574 | |

| | | | | | | | | |

Total Common Stocks (Cost $1,501,414) | | | | | | $ | 1,412,185 | |

10

LYRICAL U.S. HEDGED VALUE FUND

SCHEDULE OF INVESTMENTS (Continued) | |

MONEY MARKET FUNDS — 0.4% | | Shares | | | Value | |

Invesco Liquid Assets Portfolio (The) - Institutional Class, 0.44% (c) (Cost $4,681) | | | 4,681 | | | $ | 4,681 | |

| | | | | | | | | |

Total Investments at Value — 104.2% (Cost $1,506,095) | | | | | | $ | 1,416,866 | |

| | | | | | | | | |

Liabilities in Excess of Other Assets (d) — (4.2%) | | | | | | | (56,492 | ) |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 1,360,374 | |

(a) | All or a portion of the shares have been committed as collateral for open short positions (Note 2). |

(b) | Non-income producing security. |

(c) | The rate shown is the 7-day effective yield as of May 31, 2016. |

(d) | Includes cash held as margin deposits for open short positions. |

See accompanying notes to financial statements. |

11

LYRICAL U.S. HEDGED VALUE FUND

SCHEDULE OF SECURITIES SOLD SHORT

May 31, 2016 (Unaudited) | |

EXCHANGE-TRADED FUNDS — 50.7% | | Shares | | | Value | |

Consumer Discretionary Select Sector SPDR® Fund (The) | | | 1,017 | | | $ | 80,587 | |

Energy Select Sector SPDR® Fund (The) | | | 997 | | | | 66,669 | |

Financial Select Sector SPDR® Fund (The) | | | 5,457 | | | | 129,386 | |

Health Care Select Sector SPDR® Fund (The) | | | 1,121 | | | | 79,972 | |

Industrial Select Sector SPDR® Fund (The) | | | 2,615 | | | | 146,257 | |

Materials Select Sector SPDR® Fund (The) | | | 561 | | | | 26,333 | |

Technology Select Sector SPDR® Fund (The) | | | 3,622 | | | | 160,129 | |

Total Securities Sold Short — 50.7% (Proceeds $679,090) | | | | | | $ | 689,333 | |

See accompanying notes to financial statements. |

12

LYRICAL FUNDS

STATEMENTS OF ASSETS AND LIABILITIES

May 31, 2016 (Unaudited) | |

| | Lyrical U.S.

Value Equity Fund | | | Lyrical U.S. Hedged Value Fund | |

ASSETS | | | | | | |

Investments in securities: | | | | | | |

At acquisition cost | | $ | 987,832,011 | | | $ | 1,506,095 | |

At value (Note 2) | | $ | 1,029,469,935 | | | $ | 1,416,866 | |

Deposits with brokers for securities sold short (Note 2) | | | — | | | | 617,655 | |

Dividends receivable | | | 1,018,288 | | | | 1,429 | |

Receivable for capital shares sold | | | 600,987 | | | | 150 | |

Receivable from Adviser (Note 4) | | | — | | | | 15,968 | |

Other assets | | | 49,293 | | | | 10,655 | |

Total assets | | | 1,031,138,503 | | | | 2,062,723 | |

| | | | | | | | | |

LIABILITIES | | | | | | | | |

Securities sold short, at value (Note 2) (proceeds $— and $679,090 respectively) | | | — | | | | 689,333 | |

Payable for capital shares redeemed | | | 1,722,471 | | | | — | |

Payable to Adviser (Note 4) | | | 1,065,471 | | | | — | |

Payable to administrator (Note 4) | | | 84,320 | | | | 8,010 | |

Accrued distribution fees (Note 4) | | | 20,255 | | | | — | |

Accrued brokerage expense on securities sold short (Note 2) | | | — | | | | 176 | |

Other accrued expenses | | | 45,751 | | | | 4,830 | |

Total liabilities | | | 2,938,268 | | | | 702,349 | |

| | | | | | | | | |

NET ASSETS | | $ | 1,028,200,235 | | | $ | 1,360,374 | |

| | | | | | | | | |

NET ASSETS CONSIST OF: | | | | | | | | |

Paid-in capital | | $ | 970,280,826 | | | $ | 1,452,255 | |

Accumulated net investment income (loss) | | | 10,033,973 | | | | (557 | ) |

Accumulated net realized gains from security transactions | | | 6,247,512 | | | | 8,148 | |

Net unrealized appreciation (depreciation) on: | | | | | | | | |

Investments | | | 41,637,924 | | | | (89,229 | ) |

Securities sold short | | | — | | | | (10,243 | ) |

NET ASSETS | | $ | 1,028,200,235 | | | $ | 1,360,374 | |

| | | | | | | | | |

NET ASSET VALUE PER SHARE: | | | | | | | | |

INSTITUTIONAL CLASS | | | | | | | | |

Net assets applicable to Institutional Class | | $ | 969,418,322 | | | $ | 770,673 | |

Institutional Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | | | 64,081,925 | | | | 82,822 | |

Net asset value, offering price and redemption price per share (Note 2) | | $ | 15.13 | | | $ | 9.31 | |

INVESTOR CLASS | | | | | | | | |

Net assets applicable to Investor Class | | $ | 58,781,913 | | | $ | 589,701 | |

Investor Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | | | 3,896,261 | | | | 63,668 | |

Net asset value, offering price and redemption price per share (Note 2) | | $ | 15.09 | | | $ | 9.26 | |

See accompanying notes to financial statements. |

13

LYRICAL FUNDS

STATEMENTS OF OPERATIONS

Six Months Ended May 31, 2016 (Unaudited) | |

| | Lyrical U.S. Value Equity Fund | | | Lyrical U.S. Hedged Value Fund | |

INVESTMENT INCOME | | | | | | |

Dividend income | | $ | 16,671,775 | | | $ | 22,004 | |

Foreign withholding taxes on dividends | | | (98,625 | ) | | | (117 | ) |

Total investment income | | | 16,573,150 | | | | 21,887 | |

| | | | | | | | | |

EXPENSES | | | | | | | | |

Investment advisory fees (Note 4) | | | 5,646,005 | | | | 10,276 | |

Administration fees (Note 4) | | | 319,349 | | | | 13,500 | |

Distribution fees - Investor Class (Note 4) | | | 117,857 | | | | 723 | |

Registration and filing fees | | | 69,009 | | | | 5,660 | |

Fund accounting fees (Note 4) | | | 53,222 | | | | 16,567 | |

Custody and bank service fees | | | 50,954 | | | | 3,329 | |

Transfer agent fees (Note 4) | | | 41,816 | | | | 12,000 | |

Compliance fees (Note 4) | | | 46,356 | | | | 6,000 | |

Professional fees | | | 18,611 | | | | 15,911 | |

Postage and supplies | | | 22,721 | | | | 2,547 | |

Trustees' fees and expenses (Note 4) | | | 5,597 | | | | 5,597 | |

Printing of shareholder reports | | | 6,781 | | | | 2,592 | |

Dividend expense on securities sold short (Note 2) | | | — | | | | 7,474 | |

Insurance expense | | | 2,032 | | | | 2,032 | |

Prime brokerage expense on securities sold short (Note 2) | | | — | | | | 2,645 | |

Other expenses | | | 6,849 | | | | 7,636 | |

Total expenses | | | 6,407,159 | | | | 114,489 | |

Fee reductions and expense reimbursements by Adviser (Note 4) | | | — | | | | (92,045 | ) |

Net expenses | | | 6,407,159 | | | | 22,444 | |

| | | | | | | | | |

NET INVESTMENT INCOME (LOSS) | | | 10,165,991 | | | | (557 | ) |

| | | | | | | | | |

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS AND SECURITIES SOLD SHORT | | | | | | | | |

Net realized gains (losses) from: | | | | | | | | |

Investments | | | 9,295,254 | | | | 12,555 | |

Securities sold short | | | — | | | | (1,443 | ) |

Net change in unrealized appreciation (depreciation) on: | | | | | | | | |

Investments | | | 26,713,051 | | | | (28,911 | ) |

Securities sold short | | | — | | | | 4,470 | |

NET REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS AND SECURITIES SOLD SHORT | | | 36,008,305 | | | | (13,329 | ) |

| | | | | | | | | |

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 46,174,296 | | | $ | (13,886 | ) |

See accompanying notes to financial statements. |

14

LYRICAL U.S. VALUE EQUITY FUND

STATEMENTS OF CHANGES IN NET ASSETS | |

| | Six Months

Ended

May 31, 2016

(Unaudited) | | | Year

Ended

November 30, 2015 | |

FROM OPERATIONS | | | | | | |

Net investment income | | $ | 10,165,991 | | | $ | 1,440,862 | |

Net realized gains from security transactions | | | 9,295,254 | | | | 12,579,532 | |

Net change in unrealized appreciation (depreciation) on investments | | | 26,713,051 | | | | (31,320,202 | ) |

Net increase (decrease) in net assets resulting from operations | | | 46,174,296 | | | | (17,299,808 | ) |

| | | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | | | | | | | | |

From net investment income, Institutional Class | | | (1,403,762 | ) | | | (168,471 | ) |

From net investment income, Investor Class | | | (6,340 | ) | | | — | |

From net realized gains, Institutional Class | | | (14,083,967 | ) | | | (11,690,275 | ) |

From net realized gains, Investor Class | | | (1,469,251 | ) | | | (193,318 | ) |

Decrease in net assets from distributions to shareholders | | | (16,963,320 | ) | | | (12,052,064 | ) |

| | | | | | | | | |

CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Institutional Class | | | | | | | | |

Proceeds from shares sold | | | 576,171,995 | | | | 339,352,309 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 11,534,459 | | | | 9,377,973 | |

Payments for shares redeemed | | | (241,620,578 | ) | | | (282,422,299 | ) |

Net increase in Institutional Class net assets from capital share transactions | | | 346,085,876 | | | | 66,307,983 | |

| | | | | | | | | |

Investor Class | | | | | | | | |

Proceeds from shares sold | | | 57,442,392 | | | | 118,329,002 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 1,458,715 | | | | 181,114 | |

Payments for shares redeemed | | | (57,954,564 | ) | | | (59,563,305 | ) |

Net increase in Investor Class net assets from capital share transactions | | | 946,543 | | | | 58,946,811 | |

| | | | | | | | | |

TOTAL INCREASE IN NET ASSETS | | | 376,243,395 | | | | 95,902,922 | |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of period | | | 651,956,840 | | | | 556,053,918 | |

End of period | | $ | 1,028,200,235 | | | $ | 651,956,840 | |

| | | | | | | | | |

ACCUMULATED NET INVESTMENT INCOME | | $ | 10,033,973 | | | $ | 1,278,084 | |

See accompanying notes to financial statements. |

15

LYRICAL U.S. VALUE EQUITY FUND

STATEMENTS OF CHANGES IN NET ASSETS (Continued) | |

| | Six Months

Ended

May 31, 2016

(Unaudited) | | | Year

Ended

November 30, 2015 | |

CAPITAL SHARE ACTIVITY | | | | | | |

Institutional Class | | | | | | |

Shares sold | | | 42,258,821 | | | | 21,132,995 | |

Shares issued in reinvestment of distributions to shareholders | | | 750,525 | | | | 592,967 | |

Shares redeemed | | | (16,716,439 | ) | | | (17,510,391 | ) |

Net increase in shares outstanding | | | 26,292,907 | | | | 4,215,571 | |

Shares outstanding at beginning of period | | | 37,789,018 | | | | 33,573,447 | |

Shares outstanding at end of period | | | 64,081,925 | | | | 37,789,018 | |

| | | | | | | | | |

Investor Class | | | | | | | | |

Shares sold | | | 3,797,000 | | | | 7,202,116 | |

Shares issued in reinvestment of distributions to shareholders | | | 94,924 | | | | 11,470 | |

Shares redeemed | | | (3,937,844 | ) | | | (3,826,599 | ) |

Net increase (decrease) in shares outstanding | | | (45,920 | ) | | | 3,386,987 | |

Shares outstanding at beginning of period | | | 3,942,181 | | | | 555,194 | |

Shares outstanding at end of period | | | 3,896,261 | | | | 3,942,181 | |

See accompanying notes to financial statements. |

16

LYRICAL U.S. HEDGED VALUE FUND

STATEMENTS OF CHANGES IN NET ASSETS | |

| | Six Months

Ended

May 31, 2016

(Unaudited) | | | Year

Ended

November 30, 2015 | |

FROM OPERATIONS | | | | | | |

Net investment loss | | $ | (557 | ) | | $ | (22,709 | ) |

Net realized gains (losses) from: | | | | | | | | |

Investments | | | 12,555 | | | | 21,575 | |

Securities sold short | | | (1,443 | ) | | | (3,393 | ) |

Net change in unrealized appreciation (depreciation) on: | | | | | | | | |

Investments | | | (28,911 | ) | | | (60,317 | ) |

Securities sold short | | | 4,470 | | | | 2,207 | |

Net decrease in net assets resulting from operations | | | (13,886 | ) | | | (62,637 | ) |

| | | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | | | | | | | | |

From net realized gains, Institutional Class | | | (6,246 | ) | | | (54 | ) |

From net realized gains, Investor Class | | | (4,994 | ) | | | (57 | ) |

Decrease in net assets from distributions to shareholders | | | (11,240 | ) | | | (111 | ) |

| | | | | | | | | |

CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Institutional Class | | | | | | | | |

Proceeds from shares sold | | | — | | | | 220,000 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 6,087 | | | | 54 | |

Net increase in Institutional Class net assets from capital share transactions | | | 6,087 | | | | 220,054 | |

| | | | | | | | | |

Investor Class | | | | | | | | |

Proceeds from shares sold | | | 12,473 | | | | 126,747 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 4,784 | | | | 54 | |

Payments for shares redeemed | | | (33,274 | ) | | | (94,359 | ) |

Net increase (decrease) in Investor Class net assets from capital share transactions | | | (16,017 | ) | | | 32,442 | |

| | | | | | | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | | | (35,056 | ) | | | 189,748 | |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of period | | | 1,395,430 | | | | 1,205,682 | |

End of period | | $ | 1,360,374 | | | $ | 1,395,430 | |

| | | | | | | | | |

ACCUMULATED NET INVESTMENT LOSS | | $ | (557 | ) | | $ | — | |

See accompanying notes to financial statements. |

17

LYRICAL U.S. HEDGED VALUE FUND

STATEMENTS OF CHANGES IN NET ASSETS (Continued) | |

| | Six Months

Ended

May 31, 2016

(Unaudited) | | | Year

Ended

November 30, 2015 | |

CAPITAL SHARE ACTIVITY | | | | | | |

Institutional Class | | | | | | |

Shares sold | | | — | | | | 21,883 | |

Shares issued in reinvestment of distributions to shareholders | | | 645 | | | | 6 | |

Net increase in shares outstanding | | | 645 | | | | 21,889 | |

Shares outstanding at beginning of period | | | 82,177 | | | | 60,288 | |

Shares outstanding at end of period | | | 82,822 | | | | 82,177 | |

| | | | | | | | | |

Investor Class | | | | | | | | |

Shares sold | | | 1,375 | | | | 12,770 | |

Shares issued in reinvestment of distributions to shareholders | | | 508 | | | | 6 | |

Shares redeemed | | | (3,931 | ) | | | (9,763 | ) |

Net increase (decrease) in shares outstanding | | | (2,048 | ) | | | 3,013 | |

Shares outstanding at beginning of period | | | 65,716 | | | | 62,703 | |

Shares outstanding at end of period | | | 63,668 | | | | 65,716 | |

See accompanying notes to financial statements. |

18

LYRICAL U.S. VALUE EQUITY FUND

INSTITUTIONAL CLASS

FINANCIAL HIGHLIGHTS | |

Per Share Data for a Share Outstanding Throughout Each Period: | |

| | Six Months

Ended

May 31, 2016

(Unaudited) | | | Year

Ended

November 30, 2015 | | | Year

Ended

November 30, 2014 | | | Period

Ended

November 30,

2013 (a) | |

Net asset value at beginning of period | | $ | 15.63 | | | $ | 16.29 | | | $ | 13.78 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 0.15 | | | | 0.04 | | | | (0.00 | )(b) | | | 0.00 | (b) |

Net realized and unrealized gains (losses) on investments | | | (0.24 | ) | | | (0.35 | ) | | | 2.66 | | | | 3.78 | |

Total from investment operations | | | (0.09 | ) | | | (0.31 | ) | | | 2.66 | | | | 3.78 | |

| | | | | | | | | | | | | | | | | |

Less distributions: | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | (0.04 | ) | | | (0.00 | )(b) | | | (0.00 | )(b) | | | — | |

Distributions from net realized gains | | | (0.37 | ) | | | (0.35 | ) | | | (0.15 | ) | | | — | |

Total distributions | | | (0.41 | ) | | | (0.35 | ) | | | (0.15 | ) | | | — | |

| | | | | | | | | | | | | | | | | |