UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811- 524 |

| |

| The Dreyfus/Laurel Funds Trust | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Michael A. Rosenberg, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6000 |

| |

Date of fiscal year end: | 05/31 | |

Date of reporting period: | 05/31/2012 | |

| | | | | | | |

The following N-CSR relates only to Dreyfus Equity Income Fund and Dreyfus Emerging Markets Debt Local Currency Fund and does not affect the other series of the Registrant, which have different fiscal year ends and, therefore, different N-CSR reporting requirements. Separate N-CSR Forms will be filed for these series, as appropriate.

FORM N-CSR

Item 1. Reports to Stockholders.

Dreyfus

Equity Income Fund

ANNUAL REPORT May 31, 2012

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

| |

| | Contents |

| |

| | THE FUND |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Fund Performance |

| 8 | Understanding Your Fund’s Expenses |

| 8 | Comparing Your Fund’s Expenses |

| With Those of Other Funds |

| 9 | Statement of Investments |

| 14 | Statement of Assets and Liabilities |

| 15 | Statement of Operations |

| 16 | Statement of Changes in Net Assets |

| 18 | Financial Highlights |

| 21 | Notes to Financial Statements |

| 31 | Report of Independent Registered |

| | Public Accounting Firm |

| 32 | Important Tax Information |

| 33 | Information About the Renewal of |

| | the Fund’s Management Agreement |

| 38 | Board Members Information |

| 40 | Officers of the Fund |

| |

| FOR MORE INFORMATION |

|

| | Back Cover |

Dreyfus

Equity Income Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Equity Income Fund, covering the 12-month period from June 1, 2011, through May 31, 2012. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

The market rebound that drove stock prices higher during the fall and winter seemed to sputter toward the end of the first quarter 2012, primarily due to a resurgent European debt crisis and renewed U.S. economic concerns, including disappointing employment data. Consequently, stocks ended the reporting period with low or negative returns, on average, with steeper declines among smaller companies and more mild losses for large-cap stocks.

Despite the market’s recent swoon, we believe that trends in many of the more economically sensitive areas of the U.S. economy remain favorable. For example, in the automobile industry, new cars offer improved gas mileage, the average age of the auto fleet is old, and credit is widely available at a time when household debt-service ratios have dropped sharply. Even residential construction has moved into a sustainable uptrend, in our opinion, as employment has expanded and homebuilders have seen a rise in orders. On the other hand, net exports may prove to be a slight drag on domestic growth since the economy in the United States is stronger than in many of its trading partners. On the whole, we expect near-trend growth in the U.S. economy for the remainder of 2012.

As always, we encourage you to discuss our observations with your financial advisor.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

June 15, 2012

2

DISCUSSION OF FUND PERFORMANCE

For the period of June 1, 2011, through May 31, 2012, as provided by Jocelin A. Reed, CFA, Portfolio Manager

Market and Fund Performance Overview

For the 12-month period ended May 31, 2012, Dreyfus Equity Income Fund’s Class A shares produced a total return of 3.18%, Class C shares returned 2.47% and Class I shares returned 3.47%.1 In comparison, the fund’s benchmark, the Standard & Poor’s 500 Composite Stock Price Index (the “S&P 500 Index”), provided a total return of –0.43% for the same period.2

Market weakness stemming from global macroeconomic concerns over the reporting period’s first half was balanced by a rebound over the second half.The fund produced higher returns than its benchmark, chiefly due to successful security selections in the consumer staples, energy, health care and information technology sectors.

The Fund’s Investment Approach

The fund seeks total return consisting of capital appreciation and income. To pursue its goal, the fund invests primarily in equity securities, with a particular focus on dividend-paying stocks and other investments and investment techniques that provide income.When selecting securities, we use a computer model to identify and rank stocks within an industry or sector. Next, based on fundamental analysis, we generally select what we believe to be the most attractive of the higher ranked securities. We manage risk by diversifying the fund’s investments across companies and industries, seeking to limit the potential adverse impact of a decline in any one stock or industry.

Changing Economic Data Fueled Market Volatility

Equity markets floundered early in the reporting period, mainly due to a debt crisis in Greece that threatened other members of the European Union and uncertainties regarding the sustainability of the U.S. economic recovery.These issues led investors to avoid many of the market’s riskier areas, and they focused instead on traditionally defensive investments,

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

including dividend-paying stocks. Fortunately, many of these concerns abated in the fall when U.S. employment trends improved and European policymakers announced measures to address the region’s debt crisis. Investors grew more tolerant of risk, and they shifted their attention from traditional safe havens to riskier assets.

However, new developments in the spring of 2012 called some of these positive influences into question. The U.S. labor market’s rebound slowed markedly as the public sector shed jobs and employment gains in the private sector proved more anemic than expected. Austerity measures designed to relieve fiscal pressures in Europe encountered political resistance, raising questions regarding proposed bailouts and the region’s economic prospects. These threats to global growth caused most stock market averages, including the S&P 500 Index, to decline in April and May, erasing earlier gains.

Dividend Payers Benefited from Investors’ Caution

Over the first half of the reporting period, investors abandoned riskier investments in favor of perceived safe havens, including the stocks of well-established companies with consistent earnings, healthy balance sheets and generous dividend yields.Although risk appetites expanded and dividend-paying stocks generally underperformed market averages over the first five months of 2012, it was not enough to fully offset earlier gains.

The fund fared particularly well in the traditionally defensive consumer staples sector, where retailing giant Wal-Mart Stores and tobacco producers Philip Morris International and Altria Group attracted investment capital with strong cash flows, stock buyback programs and dividend increases. In the energy sector, relative performance was bolstered by a focus on better-performing integrated oil producers, including Exxon Mobil, Chevron and ConocoPhillips. Overweighted exposure to the health care sector proved beneficial, as large pharmaceutical developers Eli Lilly & Co. and Bristol-Myers-Squibb gained value in the flight to quality. We maintained an underweighted position in information technology companies, few of which pay dividends. Among those that do, the fund scored successes with microchip maker Intel and software giant Microsoft.The fund also established a small position in electronics innovator Apple in anticipation of the company initiating a dividend.

4

Finally, the fund avoided the brunt of weakness in the financials sector, especially among large, diversified financial institutions that have suffered from corporate governance and oversight issues.

Disappointments during the reporting period were concentrated in the industrials sector, where mailing equipment specialist Pitney Bowes was hurt by a muted growth forecast. Directories publisher R.R. Donnelly encountered intensifying competitive pressures that led to sharp declines in its stock price. Automotive components manufacturer Autoliv lost value due to global economic concerns.

A Growth-Oriented Investment Posture

Although we have remained cautious in an environment of heightened economic uncertainty, we are optimistic regarding the prospects for dividend-paying stocks. U.S. dividend payment ratios have remained low compared to global averages, suggesting strong potential for further dividend increases. In addition, U.S. stocks ended the reporting period with attractive valuations relative to historical norms.As of the reporting period’s end, our bottom-up security selection process has found a number of attractive dividend-paying opportunities in the telecommunications services and utilities sector, but fewer among information technology companies.

June 15, 2012

Equity funds are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

1 Total return includes reinvestment of dividends and any capital gains paid, and does not take

into consideration the maximum initial sales charge in the case of Class A shares, or the

applicable contingent deferred sales charge imposed on redemptions in the case of Class C shares.

Had these charges been reflected, returns would have been lower. Past performance is no guarantee

of future results. Share price and investment return fluctuate such that upon redemption, fund

shares may be worth more or less than their original cost. Return figures provided reflect the

absorption of certain fund expenses by The Dreyfus Corporation pursuant to an undertaking in

effect through October 1, 2012, at which time it may be extended, terminated or modified. Had

these expenses not been absorbed, the fund’s returns would have been lower.

2 SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where applicable, capital

gain distributions.The Standard & Poor’s 500 Composite Stock Price Index is a widely accepted,

unmanaged index of U.S. stock market performance. Investors cannot invest directly in any index.

The Fund 5

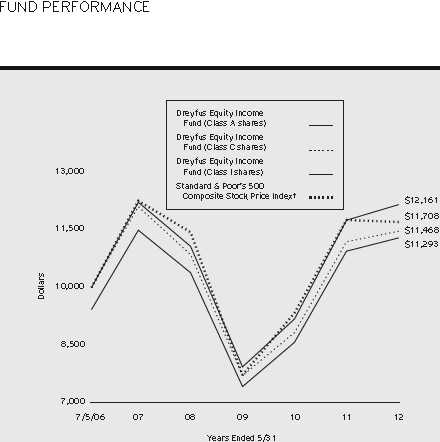

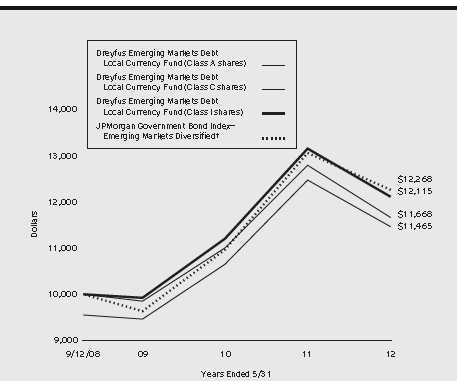

Comparison of change in value of $10,000 investment in Dreyfus Equity Income Fund Class

shares, Class C shares and Class I shares and the Standard & Poor’s 500 Composite Stock

Price Index

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a $10,000 investment made in Class A, Class C and Class I shares of Dreyfus Equity

Income Fund on 7/5/06 (inception date) to a $10,000 investment made in the Standard & Poor’s 500 Composite

Stock Price Index (the “Index”) on that date.All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A

shares and all other applicable fees and expenses on all classes.The fund primarily seeks total return by investing in

stocks, focusing on dividend-paying stocks and other instruments that provide income.The Index is a widely accepted,

unmanaged index of U.S. stock market performance.These factors can contribute to the Index potentially outperforming

the fund. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest

directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is

contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

| | | | | |

| Average Annual Total Returns as of 5/31/12 | | |

| |

| | Inception | | From |

| | Date | 1Year | Inception |

| Class A shares | | | |

| with maximum sales charge (5.75%) | 7/5/06 | –2.78% | 2.08% |

| without sales charge | 7/5/06 | 3.18% | 3.10% |

| Class C shares | | | |

| with applicable redemption charge † | 7/5/06 | 1.48% | 2.35% |

| without redemption | 7/5/06 | 2.47% | 2.35% |

| Class I shares | 7/5/06 | 3.47% | 3.37% |

| Standard & Poor’s 500 | | | |

| Composite Stock Price Index | 6/30/06 | –0.43% | 2.70%†† |

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not

reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the

date of purchase.

For comparative purposes, the value of the Index as of 6/30/06 is used as the beginning value on 7/5/06.

The Fund 7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Equity Income Fund from December 1, 2011 to May 31, 2012. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment

assuming actual returns for the six months ended May 31, 2012

| | | | | | |

| | | Class A | | Class C | | Class I |

| Expenses paid per $1,000† | $ | 5.92 | $ | 9.77 | $ | 4.64 |

| Ending value (after expenses) | $ | 1,059.80 | $ | 1,056.20 | $ | 1,060.80 |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment

assuming a hypothetical 5% annualized return for the six months ended May 31, 2012

| | | | | | |

| | | Class A | | Class C | | Class I |

| Expenses paid per $1,000† | $ | 5.81 | $ | 9.57 | $ | 4.55 |

| Ending value (after expenses) | $ | 1,019.25 | $ | 1,015.50 | $ | 1,020.50 |

† Expenses are equal to the fund’s annualized expense ratio of 1.15% for Class A, 1.90% for Class C and .90%

for Class I, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half

year period).

8

STATEMENT OF INVESTMENTS

May 31, 2012

| | |

| Common Stocks—99.4% | Shares | Value ($) |

| Consumer Discretionary—7.9% | | |

| American Eagle Outfitters | 3,990 | 77,047 |

| Foot Locker | 19,900 | 631,626 |

| Garmin | 4,200 | 180,432 |

| Genuine Parts | 1,720 | 108,360 |

| H&R Block | 83,640 | 1,277,183 |

| Hasbro | 2,060 | 72,965 |

| Home Depot | 12,490 | 616,257 |

| Leggett & Platt | 10,220 | 212,474 |

| Mattel | 9,870 | 307,253 |

| McDonald’s | 1,650 | 147,411 |

| McGraw-Hill | 4,140 | 179,593 |

| News, Cl. A | 28,500 | 547,200 |

| Viacom, Cl. B | 6,040 | 288,289 |

| | | 4,646,090 |

| Consumer Staples—15.0% | | |

| Altria Group | 51,370 | 1,653,600 |

| Archer-Daniels-Midland | 2,250 | 71,730 |

| Campbell Soup | 8,650 | 274,205 |

| Coca-Cola Enterprises | 3,000 | 82,080 |

| ConAgra Foods | 24,330 | 611,899 |

| CVS Caremark | 16,020 | 719,939 |

| Dr. Pepper Snapple Group | 8,960 | 369,690 |

| Kroger | 11,070 | 243,651 |

| Lorillard | 1,480 | 182,928 |

| Philip Morris International | 21,440 | 1,811,894 |

| Procter & Gamble | 1,550 | 96,549 |

| SUPERVALU | 39,350 | 177,862 |

| Wal-Mart Stores | 36,490 | 2,401,772 |

| Walgreen | 6,340 | 193,497 |

| | | 8,891,296 |

The Fund 9

STATEMENT OF INVESTMENTS (continued)

| | | |

| Common Stocks (continued) | Shares | Value ($) |

| Energy—6.9% | | |

| Chevron | 11,960 | 1,175,788 |

| ConocoPhillips | 17,315 | 903,150 |

| Diamond Offshore Drilling | 1,140 | 66,325 |

| Exxon Mobil | 13,560 | 1,066,223 |

| Halliburton | 7,990 | 240,179 |

| Marathon Oil | 7,400 | 184,334 |

| Phillips 66 | 8,657a | 259,970 |

| Schlumberger | 2,900 | 183,425 |

| | | 4,079,394 |

| Financial—12.6% | | |

| Aflac | 6,850 | 274,548 |

| American Express | 9,020 | 503,587 |

| Annaly Capital Management | 92,810b | 1,542,502 |

| Ares Capital | 71,250 | 1,075,162 |

| Capitol Federal Financial | 36,690 | 427,438 |

| Chimera Investment | 202,800b | 567,840 |

| Commonwealth REIT | 6,760b | 119,314 |

| Hospitality Properties Trust | 34,740b | 816,737 |

| JPMorgan Chase & Co. | 21,105 | 699,631 |

| LPL Investment Holdings | 9,300 | 301,134 |

| MetLife | 12,850 | 375,349 |

| People’s United Financial | 33,410 | 388,558 |

| Piedmont Office Realty Trust, Cl. A | 17,940b | 296,189 |

| Prudential Financial | 1,805 | 83,842 |

| | | 7,471,831 |

| Health Care—12.1% | | |

| Abbott Laboratories | 1,480 | 91,449 |

| Baxter International | 2,870 | 145,279 |

| Bristol-Myers Squibb | 50,110 | 1,670,667 |

| Eli Lilly & Co. | 48,920 | 2,003,274 |

| Humana | 1,470 | 112,293 |

| Johnson & Johnson | 2,350 | 146,711 |

10

| | | |

| Common Stocks (continued) | Shares | Value ($) |

| Health Care (continued) | | |

| Merck & Co. | 16,110 | 605,414 |

| Pfizer | 89,807 | 1,964,079 |

| Thoratec | 2,250a | 68,265 |

| WellPoint | 4,950 | 333,581 |

| | | 7,141,012 |

| Industrial—9.8% | | |

| Cummins | 1,120 | 108,584 |

| General Dynamics | 1,660 | 106,257 |

| General Electric | 81,800 | 1,561,562 |

| Iron Mountain | 2,550 | 72,293 |

| Lockheed Martin | 1,660 | 137,448 |

| PACCAR | 2,370 | 89,041 |

| Pitney Bowes | 150,915 | 2,058,481 |

| R.R. Donnelley & Sons | 72,400 | 779,024 |

| Raytheon | 2,070 | 104,162 |

| Union Pacific | 1,000 | 111,400 |

| United Parcel Service, Cl. B | 6,720 | 503,597 |

| Waste Management | 4,900 | 158,956 |

| | | 5,790,805 |

| Information Technology—16.2% | | |

| Activision Blizzard | 13,760 | 161,542 |

| Apple | 4,860a | 2,807,768 |

| Intel | 81,145 | 2,096,787 |

| International Business Machines | 2,090 | 403,161 |

| Maxim Integrated Products | 19,105 | 480,682 |

| Microchip Technology | 24,880 | 771,778 |

| Microsoft | 67,385 | 1,966,968 |

| Oracle | 13,090 | 346,492 |

| Paychex | 7,350 | 220,280 |

| QUALCOMM | 4,100 | 234,971 |

| VeriSign | 1,800a | 68,814 |

| | | 9,559,243 |

The Fund 11

STATEMENT OF INVESTMENTS (continued)

| | |

| Common Stocks (continued) | Shares | Value ($) |

| Materials—5.0% | | |

| CF Industries Holdings | 1,200 | 205,152 |

| Freeport-McMoRan Copper & Gold | 22,440 | 718,978 |

| Southern Copper | 66,256 | 1,884,983 |

| Steel Dynamics | 14,980 | 157,889 |

| | | 2,967,002 |

| Telecommunication Services—6.2% | | |

| AT&T | 55,160 | 1,884,817 |

| Verizon Communications | 43,070 | 1,793,435 |

| | | 3,678,252 |

| Utilities—7.7% | | |

| Ameren | 13,210 | 426,815 |

| American Electric Power | 52,660 | 2,027,937 |

| Consolidated Edison | 3,090 | 186,512 |

| Entergy | 1,030 | 66,466 |

| Exelon | 8,100 | 299,538 |

| NextEra Energy | 1,710 | 111,731 |

| Pepco Holdings | 11,540 | 219,952 |

| Public Service Enterprise Group | 25,960 | 809,692 |

| Southern | 2,950 | 135,435 |

| TECO Energy | 10,550 | 183,570 |

| Wisconsin Energy | 2,390 | 90,438 |

| | | 4,558,086 |

| Total Common Stocks | | |

| (cost $57,950,989) | | 58,783,011 |

12

| | | | | | |

| Other Investment—.6% | | Shares | | Value ($) |

| Registered Investment Company; | | | | |

| Dreyfus Institutional Preferred | | | | |

| Plus Money Market Fund | | | | |

| (cost $354,849) | | 354,849 | c | 354,849 |

| |

| Total Investments (cost $58,305,838) | | 100.0 | % | 59,137,860 |

| |

| Liabilities, Less Cash and Receivables | | (.0 | %) | (28,417) |

| |

| Net Assets | | 100.0 | % | 59,109,443 |

| |

| REIT—Real Estate Investment Trust | | | | |

| a | Non-income producing security. | | | | |

| b | Investment in real estate investment trust. | | | | |

| c | Investment in affiliated money market mutual fund. | | | |

| |

| |

| |

| Portfolio Summary (Unaudited)† | | | |

| | Value (%) | | | Value (%) |

| Information Technology | 16.2 | Utilities | | 7.7 |

| Consumer Staples | 15.0 | Energy | | 6.9 |

| Financial | 12.6 | Telecommunication Services | | 6.2 |

| Health Care | 12.1 | Materials | | 5.0 |

| Industrial | 9.8 | Money Market Investment | | .6 |

| Consumer Discretionary | 7.9 | | | 100.0 |

| |

| † | Based on net assets. | | | | |

| See notes to financial statements. | | | | |

The Fund 13

STATEMENT OF ASSETS AND LIABILITIES

May 31, 2012

| | | |

| | | Cost | Value |

| Assets ($): | | | |

| Investments in securities—See Statement of Investments: | | |

| Unaffiliated issuers | | 57,950,989 | 58,783,011 |

| Affiliated issuers | | 354,849 | 354,849 |

| Dividends receivable | | | 247,609 |

| Receivable for shares of Beneficial Interest subscribed | | 116,270 |

| Prepaid expenses | | | 37,144 |

| | | | 59,538,883 |

| Liabilities ($): | | | |

| Due to The Dreyfus Corporation and affiliates—Note 3(c) | | 61,470 |

| Cash overdraft due to Custodian | | | 135,927 |

| Payable for investment securities purchased | | | 172,312 |

| Payable for shares of Beneficial Interest redeemed | | | 6,469 |

| Accrued expenses | | | 53,262 |

| | | | 429,440 |

| Net Assets ($) | | | 59,109,443 |

| Composition of Net Assets ($): | | | |

| Paid-in capital | | | 57,717,089 |

| Accumulated undistributed investment income—net | | | 219,315 |

| Accumulated net realized gain (loss) on investments | | | 341,017 |

| Accumulated net unrealized appreciation | | | |

| (depreciation) on investments | | | 832,022 |

| Net Assets ($) | | | 59,109,443 |

| |

| |

| Net Asset Value Per Share | | | |

| | Class A | Class C | Class I |

| Net Assets ($) | 51,753,790 | 4,147,611 | 3,208,042 |

| Shares Outstanding | 3,932,705 | 318,393 | 243,111 |

| Net Asset Value Per Share ($) | 13.16 | 13.03 | 13.20 |

| |

| See notes to financial statements. | | | |

14

| | |

| STATEMENT OF OPERATIONS | |

| Year Ended May 31, 2012 | |

| |

| |

| |

| |

| Investment Income ($): | |

| Income: | |

| Cash dividends: (net of $75 foreign taxes withheld at source): | |

| Unaffiliated issuers | 1,126,512 |

| Affiliated issuers | 427 |

| Income from securities lending—Note 1(b) | 1,699 |

| Total Income | 1,128,638 |

| Expenses: | |

| Management fee—Note 3(a) | 201,807 |

| Shareholder servicing costs—Note 3(c) | 88,669 |

| Custodian fees—Note 3(c) | 79,100 |

| Registration fees | 47,243 |

| Auditing fees | 35,709 |

| Distribution fees—Note 3(b) | 16,252 |

| Prospectus and shareholders’ reports | 14,523 |

| Legal fees | 9,684 |

| Trustees’ fees and expenses—Note 3(d) | 1,779 |

| Loan commitment fees—Note 2 | 234 |

| Miscellaneous | 13,076 |

| Total Expenses | 508,076 |

| Less—reduction in management fee due to undertakings—Note 3(a) | (173,158) |

| Less—reduction in fees due to earnings credits—Note 3(c) | (34) |

| Net Expenses | 334,884 |

| Investment Income—Net | 793,754 |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | |

| Net realized gain (loss) on investments | 399,856 |

| Net unrealized appreciation (depreciation) on investments | 636,225 |

| Net Realized and Unrealized Gain (Loss) on Investments | 1,036,081 |

| Net Increase in Net Assets Resulting from Operations | 1,829,835 |

| |

| See notes to financial statements. | |

The Fund 15

STATEMENT OF CHANGES IN NET ASSETS

| | | | |

| | | Year Ended May 31, |

| | 2012 | 2011 |

| Operations ($): | | |

| Investment income—net | 793,754 | 48,447 |

| Net realized gain (loss) on investments | 399,856 | 346,153 |

| Net unrealized appreciation | | |

| (depreciation) on investments | 636,225 | 307,194 |

| Net Increase (Decrease) in Net Assets | | |

| Resulting from Operations | 1,829,835 | 701,794 |

| Dividends to Shareholders from ($): | | |

| Investment income—net: | | |

| Class A Shares | (508,071) | (31,860) |

| Class C Shares | (37,078) | (5,123) |

| Class I Shares | (31,601) | (1,801) |

| Net realized gain on investments: | | |

| Class A Shares | (227,036) | — |

| Class C Shares | (13,908) | — |

| Class I Shares | (6,810) | — |

| Total Dividends | (824,504) | (38,784) |

| Beneficial Interest Transactions ($): | | |

| Net proceeds from shares sold: | | |

| Class A Shares | 55,138,094 | 2,004,280 |

| Class C Shares | 3,914,501 | 678,007 |

| Class I Shares | 4,041,781 | 23,503 |

| Dividends reinvested: | | |

| Class A Shares | 680,085 | 12,745 |

| Class C Shares | 32,683 | 2,675 |

| Class I Shares | 19,829 | 913 |

| Cost of shares redeemed: | | |

| Class A Shares | (7,352,475) | (1,456,332) |

| Class C Shares | (740,925) | (176,017) |

| Class I Shares | (927,086) | (57,808) |

| Increase (Decrease) in Net Assets from | | |

| Beneficial Interest Transactions | 54,806,487 | 1,031,966 |

| Total Increase (Decrease) in Net Assets | 55,811,818 | 1,694,976 |

| Net Assets ($): | | |

| Beginning of Period | 3,297,625 | 1,602,649 |

| End of Period | 59,109,443 | 3,297,625 |

| Undistributed investment income—net | 219,315 | 11,429 |

16

| | | | |

| | | Year Ended May 31, |

| | 2012 | 2011 |

| Capital Share Transactions: | | |

| Class A | | |

| Shares sold | 4,259,332 | 169,627 |

| Shares issued for dividends reinvested | 52,382 | 1,079 |

| Shares redeemed | (553,800) | (113,433) |

| Net Increase (Decrease) in Shares Outstanding | 3,757,914 | 57,273 |

| Class C | | |

| Shares sold | 303,986 | 56,288 |

| Shares issued for dividends reinvested | 2,561 | 227 |

| Shares redeemed | (57,847) | (14,269) |

| Net Increase (Decrease) in Shares Outstanding | 248,700 | 42,246 |

| Class I | | |

| Shares sold | 306,304 | 2,067 |

| Shares issued for dividends reinvested | 1,532 | 78 |

| Shares redeemed | (70,156) | (4,357) |

| Net Increase (Decrease) in Shares Outstanding | 237,680 | (2,212) |

| |

| See notes to financial statements. | | |

The Fund 17

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated.All information (except portfolio turnover rate) reflects financial results for a single fund share.Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | | | | | | |

| | | Year Ended May 31, | |

| Class A Shares | 2012 | 2011 | 2010 | 2009 | 2008 |

| Per Share Data ($): | | | | | |

| Net asset value, beginning of period | 13.23 | 10.52 | 9.24 | 13.17 | 15.00 |

| Investment Operations: | | | | | |

| Investment income—neta | .39 | .23 | .16 | .19 | .19 |

| Net realized and unrealized | | | | | |

| gain (loss) on investments | .01 | 2.66 | 1.27 | (3.93) | (1.63) |

| Total from Investment Operations | .40 | 2.89 | 1.43 | (3.74) | (1.44) |

| Distributions: | | | | | |

| Dividends from investment income—net | (.36) | (.18) | (.15) | (.19) | (.18) |

| Dividends from net realized | | | | | |

| gain on investments | (.11) | — | — | — | (.21) |

| Total Distributions | (.47) | (.18) | (.15) | (.19) | (.39) |

| Net asset value, end of period | 13.16 | 13.23 | 10.52 | 9.24 | 13.17 |

| Total Return (%)b | 3.18 | 27.70 | 15.55 | (28.60) | (9.59) |

| Ratios/Supplemental Data (%): | | | | | |

| Ratio of total expenses | | | | �� | |

| to average net assets | 1.80 | 5.40 | 9.40 | 11.74 | 8.79 |

| Ratio of net expenses | | | | | |

| to average net assets | 1.19 | 1.50 | 1.50 | 1.50 | 1.50 |

| Ratio of net investment income | | | | | |

| to average net assets | 2.99 | 1.85 | 1.49 | 1.95 | 1.38 |

| Portfolio Turnover Rate | 66.38 | 121.84 | 76.05 | 29.06 | 14.52 |

| Net Assets, end of period ($ x 1,000) | 51,754 | 2,312 | 1,236 | 957 | 1,307 |

a Based on average shares outstanding at each month end.

b Exclusive of sales charge.

See notes to financial statements.

18

| | | | | | | | | | |

| | | Year Ended May 31, | |

| Class C Shares | 2012 | 2011 | 2010 | 2009 | 2008 |

| Per Share Data ($): | | | | | |

| Net asset value, beginning of period | 13.10 | 10.43 | 9.18 | 13.12 | 14.96 |

| Investment Operations: | | | | | |

| Investment income—neta | .30 | .13 | .09 | .11 | .09 |

| Net realized and unrealized | | | | | |

| gain (loss) on investments | .01 | 2.65 | 1.26 | (3.92) | (1.62) |

| Total from Investment Operations | .31 | 2.78 | 1.35 | (3.81) | (1.53) |

| Distributions: | | | | | |

| Dividends from investment income—net | (.27) | (.11) | (.10) | (.13) | (.10) |

| Dividends from net realized | | | | | |

| gain on investments | (.11) | — | — | — | (.21) |

| Total Distributions | (.38) | (.11) | (.10) | (.13) | (.31) |

| Net asset value, end of period | 13.03 | 13.10 | 10.43 | 9.18 | 13.12 |

| Total Return (%)b | 2.47 | 26.79 | 14.57 | (29.07) | (10.28) |

| Ratios/Supplemental Data (%): | | | | | |

| Ratio of total expenses | | | | | |

| to average net assets | 2.96 | 6.19 | 10.13 | 13.47 | 9.82 |

| Ratio of net expenses | | | | | |

| to average net assets | 2.00 | 2.25 | 2.25 | 2.25 | 2.25 |

| Ratio of net investment income | | | | | |

| to average net assets | 2.30 | 1.09 | .78 | 1.21 | .66 |

| Portfolio Turnover Rate | 66.38 | 121.84 | 76.05 | 29.06 | 14.52 |

| Net Assets, end of period ($ x 1,000) | 4,148 | 913 | 286 | 129 | 127 |

a Based on average shares outstanding at each month end.

b Exclusive of sales charge.

See notes to financial statements.

The Fund 19

| | | | | | | | | | |

| FINANCIAL HIGHLIGHTS (continued) | | | | | |

| |

| |

| |

| |

| | | Year Ended May 31, | |

| Class I Shares | 2012 | 2011 | 2010 | 2009 | 2008a |

| Per Share Data ($): | | | | | |

| Net asset value, beginning of period | 13.26 | 10.54 | 9.25 | 13.19 | 15.01 |

| Investment Operations: | | | | | |

| Investment income—netb | .42 | .25 | .18 | .22 | .22 |

| Net realized and unrealized | | | | | |

| gain (loss) on investments | .02 | 2.67 | 1.28 | (3.95) | (1.62) |

| Total from Investment Operations | .44 | 2.92 | 1.46 | (3.73) | (1.40) |

| Distributions: | | | | | |

| Dividends from investment income—net | (.39) | (.20) | (.17) | (.21) | (.21) |

| Dividends from net realized | | | | | |

| gain on investments | (.11) | — | — | — | (.21) |

| Total Distributions | (.50) | (.20) | (.17) | (.21) | (.42) |

| Net asset value, end of period | 13.20 | 13.26 | 10.54 | 9.25 | 13.19 |

| Total Return (%) | 3.47 | 28.04 | 15.73 | (28.35) | (9.40) |

| Ratios/Supplemental Data (%): | | | | | |

| Ratio of total expenses | | | | | |

| to average net assets | 1.60 | 5.25 | 9.28 | 11.55 | 8.78 |

| Ratio of net expenses | | | | | |

| to average net assets | .93 | 1.25 | 1.25 | 1.25 | 1.25 |

| Ratio of net investment income | | | | | |

| to average net assets | 3.31 | 2.07 | 1.72 | 2.19 | 1.63 |

| Portfolio Turnover Rate | 66.38 | 121.84 | 76.05 | 29.06 | 14.52 |

| Net Assets, end of period ($ x 1,000) | 3,208 | 72 | 81 | 53 | 75 |

a Effective June 1, 2007, Class R shares were redesignated as Class I shares.

b Based on average shares outstanding at each month end.

See notes to financial statements.

20

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Equity Income Fund (the “fund”) is a separate diversified series of The Dreyfus/Laurel Funds Trust (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering five series, including the fund.The fund’s investment objective is to seek total return (consisting of capital appreciation and income).The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of NewYork Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares. The fund is authorized to issue an unlimited number of $.001 par value shares of Beneficial Interest in each of the following classes of shares: Class A, Class C and Class I. Class A and Class C shares are sold primarily to retail investors through financial intermediaries and bear a distribution fee and/or shareholder services fee. Class A shares are subject to a sales charge imposed at the time of purchase. Class C shares are subject to a contingent deferred sales charge (“CDSC”) imposed on Class C shares redeemed within one year of purchase. Class I shares are sold primarily to bank trust departments and other financial service providers (including The Bank of NewYork Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus), acting on behalf of customers having a qualified trust or an investment account or relationship at such institution, and bear no distribution or shareholder services fees. Class I shares are offered without a front-end sales charge or CDSC. Other differences between the classes include the services offered to and the expenses

The Fund 21

NOTES TO FINANCIAL STATEMENTS (continued)

borne by each class, the allocation of certain transfer agency costs and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Trust accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e. the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value.This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

22

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

Investments in securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices, except for open short positions, where the asked price is used for valuation purposes. Bid price is used when no asked price is available. Registered investment companies that are not traded on an exchange are valued at their net asset value. All of the preceding securities are categorized within Level 1 of the fair value hierarchy.

Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securi-

The Fund 23

NOTES TO FINANCIAL STATEMENTS (continued)

ties and other appropriate indicators, such as prices of relevant American Depository Receipts and futures contracts. Utilizing these techniques may result in transfers between Level 1 and Level 2 of the fair value hierarchy.

When market quotations or official closing prices are not readily available, or are determined not to reflect accurately fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded (for example, a foreign exchange or market), but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Board of Trustees. Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers.These securities are either categorized as Level 2 or 3 depending on the relevant inputs used.

For restricted securities where observable inputs are limited, assumptions about market activity and risk are used and are categorized within Level 3 of the fair value hierarchy.

The following is a summary of the inputs used as of May 31, 2012 in valuing the fund’s investments:

| | | | |

| | | Level 2—Other | Level 3— | |

| | Level 1— | Significant | Significant | |

| | Unadjusted | Observable | Unobservable | |

| | Quoted Prices | Inputs | Inputs | Total |

| Assets ($) | | | | |

| Investments in Securities: | | | |

| Equity Securities— | | | | |

| Domestic† | 58,783,011 | — | — | 58,783,011 |

| Mutual Funds | 354,849 | — | — | 354,849 |

† See Statement of Investments for additional detailed categorizations.

24

In May 2011, FASB issued Accounting Standards Update (“ASU”) No. 2011-04 “Amendments to Achieve Common FairValue Measurement and Disclosure Requirements in GAAP and International Financial Reporting Standards (“IFRS”)” (“ASU 2011-04”). ASU 2011-04 includes common requirements for measurement of and disclosure about fair value between GAAP and IFRS. ASU 2011-04 will require reporting entities to disclose the following information for fair value measurements categorized within Level 3 of the fair value hierarchy: quantitative information about the unobservable inputs used in the fair value measurement, the valuation processes used by the reporting entity and a narrative description of the sensitivity of the fair value measurement to changes in unobservable inputs and the interrelationships between those unobservable inputs. In addition, ASU 2011-04 will require reporting entities to make disclosures about amounts and reasons for all transfers in and out of Level 1 and Level 2 fair value measurements.The new and revised disclosures are effective for interim and annual reporting periods beginning after December 15, 2011. At this time, management is evaluating the implications of ASU 2011-04 and its impact on the financial statements.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

Pursuant to a securities lending agreement withThe Bank of NewYork Mellon the fund may lend securities to qualified institutions. It is the fund’s policy that, at origination, all loans are secured by collateral of at least 102% of the value of U.S. securities loaned and 105% of the value of foreign securities loaned. Collateral equivalent to at least 100% of the market value of securities on loan is maintained at all times. Collateral is either in the form of cash, which can be invested in certain money

The Fund 25

NOTES TO FINANCIAL STATEMENTS (continued)

market mutual funds managed by the Manager, U.S. Government and Agency securities or letters of credit.The fund is entitled to receive all income on securities loaned, in addition to income earned as a result of the lending transaction.Although each security loaned is fully collateralized, the fund bears the risk of delay in recovery of, or loss of rights in, the securities loaned should a borrower fail to return the securities in a timely manner. During the period ended May 31, 2012,The Bank of New York Mellon earned $728 from lending portfolio securities, pursuant to the securities lending agreement.

(c) Affiliated issuers: Other investment companies advised by Dreyfus are considered to be “affiliated” with the fund.

The fund may invest in shares of certain affiliated investment companies also advised or managed by Dreyfus. Investments in affiliated investment companies for the period ended May 31, 2012 were as follows:

| | | | | | | |

| Affiliated | | | | | | | |

| Investment | Value | | | | Value | | Net |

| Company | 5/31/2011 | ($) | Purchases ($) | Sales ($) | 5/31/2012 | ($) | Assets (%) |

| Dreyfus | | | | | | | |

| Institutional | | | | | | | |

| Preferred | | | | | | | |

| Plus Money | | | | | | | |

| Market Fund | 65,000 | | 22,269,513 | 21,979,664 | 354,849 | | .6 |

| Dreyfus | | | | | | | |

| Institutional | | | | | | | |

| Cash | | | | | | | |

| Advantage | | | | | | | |

| Fund | 212,049 | | 5,753,392 | 5,965,441 | — | | — |

| Total | 277,049 | | 28,022,905 | 27,945,105 | 354,849 | | .6 |

(d) Dividends to shareholders: Dividends are recorded on the ex-dividend date. Dividends from investment income-net are declared and paid monthly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

26

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended May 31, 2012, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the four-year period ended May 31, 2012 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At May 31, 2012, the components of accumulated earnings on a tax basis were as follows: undistributed ordinary income $795,376, undistributed capital gains $16,828 and unrealized appreciation $580,150.

The tax character of distributions paid to shareholders during the fiscal periods ended May 31, 2012 and May 31, 2011were as follows: ordinary income $739,412 and $38,784 and long-term capital gains $85,092 and $0, respectively.

During the period ended May 31, 2012, as a result of permanent book to tax differences, primarily due to the tax treatment for real estate investment trusts, the fund decreased accumulated undistributed investment income-net by $9,118 and increased accumulated net realized gain (loss) on investments by the same amount. Net assets and net asset value per share were not affected by this reclassification.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $225 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon (each, a “Facility”), each to be utilized primarily for temporary

The Fund 27

NOTES TO FINANCIAL STATEMENTS (continued)

or emergency purposes, including the financing of redemptions. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing. During the period ended May 31, 2012, the fund did not borrow under the Facilities.

NOTE 3—Management Fee and Other Transactions With Affiliates:

(a) Pursuant to a management agreement with the Manager, the management fee is computed at the annual rate of .75% of the value of the fund’s average daily net assets and is payable monthly.The Manager has contractually agreed from December 1, 2011 until October 1, 2012, to waive receipt of its fees and/or assume the expenses of the fund so that annual direct fund operating expenses (excluding Rule 12b-1 fees, shareholder services fees, taxes, interest, brokerage commissions, commitment fees on borrowings and extraordinary expenses) do not exceed .90% of the value of the fund’s average daily net assets.The Manager had contractually agreed from June 1, 2011 until November 30, 2011, to waive receipt of its fees and/or assume the expenses of the fund so that annual direct fund operating expenses (exclusive of certain expenses as described above) did not exceed 1.25% of the value of the fund’s average daily net assets.The expense reimbursement, pursuant to the undertakings, amounted to $173,158 during the period ended May 31, 2012.

During the period ended May 31, 2012, the Distributor retained $14,697 from commissions earned on sales of the fund’s Class A shares and $441 from CDSC’s on redemptions of the fund’s Class C shares.

(b) Under the Distribution Plan (the “Plan”) adopted pursuant to Rule 12b-1 under the Act, Class C shares pay the Distributor for distributing its shares at an annual rate of .75% of the value of the average daily net assets of Class C shares. During the period ended May 31, 2012, Class C shares were charged $16,252 pursuant to the Plan.

28

(c) Under the Shareholder Services Plan, Class A and Class C shares pay the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services.The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts.The Distributor may make payments to Service Agents (a securities dealer, financial institution or other industry professional) in respect of these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended May 31, 2012, Class A and Class C shares were charged $58,536 and $5,417, respectively, pursuant to the Shareholder Services Plan.

Under its terms, the Plan and Shareholder Services Plan shall remain in effect from year to year, provided such continuance is approved annually by a vote of a majority of those Trustees who are not “interested persons” of theTrust and who have no direct or indirect financial interest in the operation of or in any agreement related to the Plan or Shareholder Services Plan.

The fund compensates DreyfusTransfer, Inc., a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing personnel and facilities to perform transfer agency and cash management services for the fund. During the period ended May 31, 2012, the fund was charged $8,021 pursuant to the transfer agency agreement, which is included in Shareholder servicing costs in the Statement of Operations.

The fund compensatesThe Bank of NewYork Mellon under a custody agreement for providing custodial services for the fund. During the period ended May 31, 2012, the fund was charged $79,100 pursuant to the custody agreement.

The fund has arrangements with the transfer agent and the custodian whereby the fund may receive earnings credits when positive cash

The Fund 29

NOTES TO FINANCIAL STATEMENTS (continued)

balances are maintained, which are used to offset transfer agency and custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

Prior to May 29, 2012, the fund compensated The Bank of NewYork Mellon under cash management agreements for performing cash management services related to fund subscriptions and redemptions. During the period ended May 31, 2012, the fund was charged $889 pursuant to the cash management agreements, which is included in Shareholder servicing costs in the Statement of Operations.These fees were partially offset by earnings credits of $34.

During the period ended May 31, 2012, the fund was charged $6,565 for services performed by the Chief Compliance Officer and his staff.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $37,565, Rule 12b-1 distribution plan fees $2,627, shareholder services plan fees $11,799, custodian fees $27,000, chief compliance officer fees $2,652 and transfer agency per account fees $2,910, which are offset against an expense reimbursement currently in effect in the amount of $23,083.

(d) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities, during the period ended May 31, 2012, amounted to $72,501,441 and $17,939,522, respectively.

At May 31, 2012, the cost of investments for federal income tax purposes was $58,557,710; accordingly, accumulated net unrealized appreciation on investments was $580,150, consisting of $2,927,946 gross unrealized appreciation and $2,347,796 gross unrealized depreciation.

30

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

The Board of Trustees and Shareholders The Dreyfus/Laurel Funds Trust

We have audited the accompanying statement of assets and liabilities of Dreyfus Equity Income Fund (the “Fund”), a series of The Dreyfus/Laurel FundsTrust, including the statement of investments, as of May 31, 2012, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended.These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of May 31, 2012, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus Equity Income Fund, as of May 31, 2012, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

New York, New York

July 26, 2012

The Fund 31

IMPORTANT TAX INFORMATION (Unaudited)

For federal tax purposes, the fund reports the maximum amount allowable but not less than 72.20% of ordinary income dividends paid during the fiscal year ended May 31, 2012 as eligible for the corporate dividends received deduction provided under Section 243 of the Internal Revenue Code in accordance with Section 854(b)(1)(A) of the Internal Revenue Code. Also, the fund reports the maximum amount allowable but not less than $666,772 as ordinary income dividends paid during the fiscal year ended May 31, 2012 as qualified dividend income in accordance with Section 854(b)(1)(B) of the Internal Revenue Code. Shareholders will receive notification in early 2013 of the percentage applicable to the preparation of their 2012 income tax returns.Also, the fund reports the maximum amount allowable but not less than $.0362 per share as a capital gain dividend paid on December 15, 2011 in accordance with Section 852(b)(3)(C) of the Internal Revenue Code.Also, the fund reports the maximum amount allowable but not less than $.0692 as a short-term capital gain dividend paid on December 15, 2011 in accordance with Sections 871(k)(2) and 881(e) of the Internal Revenue Code.

32

INFORMATION ABOUT THE RENEWAL OF THE

FUND’S MANAGEMENT AGREEMENT (Unaudited)

At a meeting of the fund’s Board of Trustees held on February 15-16, 2012, the Board considered the renewal of the fund’s Management Agreement pursuant to which Dreyfus provides the fund with investment advisory and administrative services (the “Agreement”). The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from representatives of Dreyfus. In considering the renewal of the Agreement, the Board considered all factors that it believed to be relevant, including those discussed below. The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund.The Board considered information previously provided to them in presentations from Dreyfus representatives regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex, and Dreyfus representatives confirmed that there had been no material changes in this information. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each distribution channel, including the distribution channel(s) for the fund.

The Board also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements.The Board also considered Dreyfus’ extensive administrative, accounting, and compliance infrastructures. The Board also considered portfolio management’s brokerage policies and practices (including policies and practices regarding soft dollars) and the standards applied in seeking best execution.

The Fund 33

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio.The Board reviewed reports prepared by Lipper, Inc. (“Lipper”), an independent provider of investment company data, which included information comparing (1) the fund’s performance with the performance of a group of comparable funds (the “Performance Group”) and with a broader group of funds (the “Performance Universe”), all for various periods ended December 31, 2011, and (2) the fund’s actual and contractual management fees and total expenses with those of a group of comparable funds (the “Expense Group”) and with a broader group of funds (the “Expense Universe”), the information for which was derived in part from fund financial statements available to Lipper as of the date of its analysis. Dreyfus previously had furnished the Board with a description of the methodology Lipper used to select the Performance Group and Performance Universe and the Expense Group and Expense Universe.

Dreyfus representatives stated that the usefulness of performance comparisons may be affected by a number of factors, including different investment limitations that may be applicable to the fund and comparison funds. The Board discussed the results of the comparisons and noted that the fund’s total return performance was variously above and below the Performance Group medians and above the Performance Universe medians for the various periods, except for the five-year period when the fund’s performance was slightly below the Performance Universe median. The Board also noted that the fund ranked first in the Performance Group for the one-year period. Dreyfus also provided a comparison of the fund’s calendar year total returns to the returns of the fund’s benchmark index.

The Board also reviewed the range of actual and contractual management fees and total expenses of the Expense Group and Expense Universe funds and discussed the results of the comparisons.The Board noted that the fund’s contractual management fee was at the Expense Group median, the fund’s actual management fee (which was waived to zero pursuant to an agreement with Dreyfus) was below the Expense

34

Group and Expense Universe medians and the fund’s total expense ratio was above the Expense Group and Expense Universe medians.

Dreyfus representatives noted that Dreyfus has contractually agreed to waive receipt of its fees and/or assume the expenses of the fund, until October 1, 2012, so that annual direct fund operating expenses (excluding Rule 12b-1 fees, shareholder services fees, taxes, interest, brokerage commissions, commitment fees on borrowings, acquired fund fees and extraordinary expenses) do not exceed 0.90% of the fund’s average daily net assets.

Dreyfus representatives reviewed with the Board the management or investment advisory fees (1) paid by funds advised or administered by Dreyfus that are in the same Lipper category as the fund and (2) paid to Dreyfus or the Dreyfus-affiliated primary employer of the fund’s primary portfolio manager(s) for advising any separate accounts and/or other types of client portfolios that are considered to have similar investment strategies and policies as the fund (the “Similar Clients”), and explained the nature of the Similar Clients.They discussed differences in fees paid and the relationship of the fees paid in light of any differences in the services provided and other relevant factors. The Board considered the relevance of the fee information provided for the Similar Clients to evaluate the appropriateness and reasonableness of the fund’s management fee.

Analysis of Profitability and Economies of Scale. Dreyfus representatives reviewed the expenses allocated and profit received by Dreyfus and the resulting profitability percentage for managing the fund, and the method used to determine the expenses and profit. The Board concluded that the profitability results were not unreasonable, given the services rendered and service levels provided by Dreyfus. The Board also noted the expense limitation arrangement and its effect on Dreyfus’ profitability. The Board previously had been provided with information prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the prof-

The Fund 35

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

itability of, individual funds and the entire Dreyfus fund complex.The consulting firm also had analyzed where any economies of scale might emerge in connection with the management of a fund.

The Board’s counsel stated that the Board should consider the profitability analysis (1) as part of their evaluation of whether the fees under the Agreement bear a reasonable relationship to the mix of services provided by Dreyfus, including the nature, extent and quality of such services, and (2) in light of the relevant circumstances for the fund and the extent to which economies of scale would be realized if the fund grows and whether fee levels reflect these economies of scale for the benefit of fund shareholders. Dreyfus representatives noted that a discussion of economies of scale is predicated on a fund having achieved a substantial size. Dreyfus representatives also noted that, as a result of shared and allocated costs among funds in the Dreyfus fund complex, the extent of economies of scale could depend substantially on the level of assets in the complex as a whole, so that increases and decreases in complex-wide assets can affect potential economies of scale in a manner that is disproportionate to, or even in the opposite direction from, changes in the fund’s asset level.The Board also considered potential benefits to Dreyfus from acting as investment adviser and noted the soft dollar arrangements in effect for trading the fund’s investments.

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to the renewal of the Agreement. Based on the discussions and considerations as described above, the Board concluded and determined as follows.

The Board concluded that the nature, extent and quality of the services provided by Dreyfus are adequate and appropriate.

The Board generally was satisfied with the fund’s performance.

The Board concluded that the fee paid to Dreyfus was reasonable in light of the considerations described above.

36

The Board determined that the economies of scale which may accrue to Dreyfus and its affiliates in connection with the management of the fund had been adequately considered by Dreyfus in connection with the fee rate charged to the fund pursuant to the Agreement and that, to the extent in the future it were determined that material economies of scale had not been shared with the fund, the Board would seek to have those economies of scale shared with the fund.

The Board considered these conclusions and determinations, along with information received on a routine and regular basis throughout the year. In addition, it should be noted that the Board’s consideration of the contractual fee arrangements for this fund had the benefit of a number of years of reviews of prior or similar agreements during which lengthy discussions took place between the Board and Dreyfus representatives. Certain aspects of the arrangements may receive greater scrutiny in some years than in others, and the Board’s conclusions may be based, in part, on their consideration of the same or similar arrangements in prior years.The Board determined that renewal of the Agreement was in the best interests of the fund and its shareholders.

The Fund 37

BOARD MEMBERS INFORMATION (Unaudited)

38

Once elected all Board Members serve for an indefinite term, but achieve Emeritus status upon reaching age 80.The

address of the Board Members and Officers is c/o The Dreyfus Corporation, 200 Park Avenue, NewYork, NewYork

10166.Additional information about the Board Members is available in the fund’s Statement of Additional Information

which can be obtained from Dreyfus free of charge by calling this toll free number: 1-800-DREYFUS.

J.Tomlinson Fort, Emeritus Board Member

The Fund 39

OFFICERS OF THE FUND (Unaudited)

40

The Fund 41

For More Information

Telephone Call your financial representative or 1-800-DREYFUS

Mail The Dreyfus Family of Funds, 144 Glenn Curtiss Boulevard, Uniondale, NY 11556-0144

The fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q. The fund’s Forms N-Q are available on the SEC’s website at http://www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the fund uses to determine how to vote proxies relating to portfolio securities, and information regarding how the fund voted these proxies for the 12-month period ended June 30 is available at http://www.dreyfus.com and on the SEC’s website at http://www.sec.gov. The description of the policies and procedures is also available without charge, upon request, by calling 1-800-DREYFUS.

|

| © 2012 MBSC Securities Corporation |

Dreyfus

Emerging Markets Debt

Local Currency Fund

ANNUAL REPORT May 31, 2012

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

| |

| | Contents |

| |

| | THE FUND |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Fund Performance |

| 8 | Understanding Your Fund’s Expenses |

| 8 | Comparing Your Fund’s Expenses |

| With Those of Other Funds |

| 9 | Statement of Investments |

| 14 | Statement of Assets and Liabilities |

| 15 | Statement of Operations |

| 16 | Statement of Changes in Net Assets |

| 18 | Financial Highlights |

| 21 | Notes to Financial Statements |

| 39 | Report of Independent Registered |

| | Public Accounting Firm |

| 40 | Important Tax Information |

| 41 | Information About the Renewal of |

| | the Fund’s Management Agreement |

| 46 | Board Members Information |

| 48 | Officers of the Fund |

| |

| FOR MORE INFORMATION |

|

| | Back Cover |

Dreyfus

Emerging Markets Debt

Local Currency Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Emerging Markets Debt Local Currency Fund, covering the 12-month period from June 1, 2011, through May 31, 2012. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

The market rebound that drove prices of stocks and some bonds higher early in the reporting period seemed to sputter and die in the spring of 2012, primarily due to a resurgent European debt crisis and renewed U.S. economic concerns, including disappointing employment data. Consequently, stocks gave back many of the gains they previously had achieved, but they still ended the reporting period with positive returns, on average. Bonds generally fared better, gaining value as long-term interest rates fell in a challenging economic climate.

Despite the markets’ recent swoon and a resurgent European debt crisis, we do not anticipate a global recession. Instead, we continue to expect worldwide economic growth of about 3% for 2012, with an economic decline in Southern Europe, slight declines or slight growth for several quarters in the United Kingdom and much of Northern Europe, near-trend growth in the United States and sustained but slower growth in China and other emerging market countries.

As always, we encourage you to discuss our observations with your financial advisor.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

June 15, 2012

2

DISCUSSION OF FUND PERFORMANCE

For the period from June 1, 2011 through, May 31, 2012, as provided by Alexander Kozhemiakin and Javier Murcio, Primary Portfolio Managers

Fund and Market Performance Overview

For the 12-month period ended May 31, 2012, Dreyfus Emerging Markets Debt Local Currency Fund’s Class A shares produced a total return of –8.12%, Class C shares returned –8.83% and Class I shares returned –7.94%.1 In comparison, the fund’s benchmark, the JPMorgan Government Bond Index – Emerging Markets Diversified (the “Index”), produced a –6.11% total return for the same period.2 Emerging markets encountered heightened volatility as investors reacted to global economic developments, particularly a debt crisis in Europe.The fund produced lower returns than its benchmark, largely due to overweight exposure to the Mexican peso and underweight positions in the Colombian peso and Peruvian nuevo sol.

The Fund’s Investment Approach

The fund seeks to maximize total return.To pursue its goal, the fund normally invests at least 80% of its assets in emerging market bonds and other debt instruments denominated in the local currency of issue, and in derivative instruments that provide investment exposure to such securities.

When choosing investments, we employ in-depth fundamental country analysis supported by the discipline of quantitative valuation models. A “top down” analysis of macroeconomics and financial and political variables guides country and currency allocations.We also consider technical market factors and the global risk environment.We seek to identify shifts in country fundamentals and consider the risk-adjusted attractiveness of currency and duration returns for each emerging market country.

Macroeconomic Developments Fueled Market Volatility

When the reporting period began, emerging markets were reeling from the impact of a sovereign debt crisis in Europe and uncertainties regarding the sustainability of the U.S. economic recovery. In addition, inflationary pressures in China led to remedial measures from the country’s policymakers, sparking concerns about an economic slowdown in a major engine of global growth.These worries led investors away from

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

riskier assets, including emerging-markets currencies and debt securities. Instead, they flocked to traditional safe havens in developed markets.

After heightened volatility over the reporting period’s first half, emerging-markets currencies and bonds generally rebounded from late December through the end of the first quarter of 2012, when investor sentiment was bolstered by quantitative easing in Europe, encouraging U.S. economic news and the growing likelihood of a “soft landing” in China. However, these positive influences were called into question in the spring when austerity measures in Europe encountered political resistance, raising questions about the region’s economic prospects. These threats to global growth caused most emerging-market currencies and bonds to again decline against the U.S. dollar in April and May.

Mexico, Colombia and Peru Weighed on Performance