UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3462

The Flex-funds Trust

6125 Memorial Drive

Dublin, OH 43017

Bruce McKibben

c/o The Flex-funds Trust

6125 Memorial Drive

Dublin, OH 43017

Registrant’s telephone number, including area code: 800-325-3539

Date of fiscal year end: December 31, 2008

Date of reporting period: December 31, 2008

Item 1. Report to Stockholders.

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

TABLE OF CONTENTS

|

Our Mission Statement Every day, our mission is to exceed, with integrity, passion, and discipline, the expectations of our shareholders’ and clients’ overall investment experience. Core Values The Client/Shareholder Is Our #1 Priority Always remember whom we are serving. Our livelihood depends on providing a superior overall investment experience that exceeds the expectation of our shareholders and clients. Clarity Of Purpose Our organization has a clear, well-defined vision. All of our associates are committed to and understand how they will contribute to that vision. Communication We expect open and effective communication, full reporting, including good and bad news, and constructive feedback. Integrity We insist upon honesty and adhere to the highest ethical standards. Excellence/ Innovation Our associates strive each day for excellence in the work they perform, seek innovative ways to solve problems and introduce new ideas to take advantage of opportunities. We are a “Think Outside The Box” company. Associate Well-Being We value the success and well-being of our associates. We recognize and reward our associates’ contributions. Respect For Others Respect all people, value the differences among them and treat them as you would like to be treated. Seek First To Understand When interacting with others, place curiosity and understanding of their perspective FIRST, setting aside preconceived opinions and quick judgment. Teamwork We are a synergistic organization that works as a team to exceed our objectives. Profit We are profitable. Profitability enhances our services and capabilities, and affords everyone the opportunity to further their financial well-being. |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

LETTER TO SHAREHOLDERS

Although 2008 began in the midst of a credit crisis spurred on by the deteriorating housing market, few investors anticipated the events that would unfurl. Among other incidents, the year was witness to financial and credit market turmoil, a complete transformation of Wall Street, record-setting bankruptcies, continued pressures in the housing market, a bubble (followed by a subsequent burst) in energy and commodity prices, and a deepening recession. While the current situation is challenging, governments and central banks around the world have responded with creative solutions designed to limit the impact of the extraordinary events taking place.

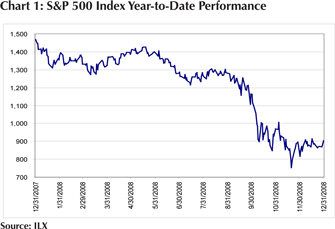

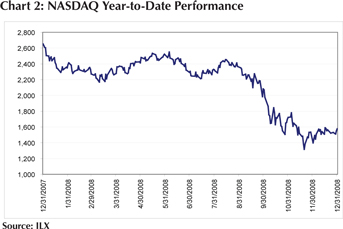

The stock market reflected the challenges facing the credit markets and global economy in 2008. Record point movements and volatility have characterized the year, especially during the third and fourth quarter. For example, the Dow recorded its largest one-day point loss in history, of nearly 778 points during the third quarter. Additionally, from October 2003 to January 2008 there were only two days that the S&P 500 gained or lost 2% or more. From September 4, 2008 to December 31, 2008, there were 48 days that the S&P 500 gained or lost 2% or more. The record point losses and volatility have combined to deliver the second worst annual performance since 1926 for the S&P 500. For the year ending December 31, 2008, the return for the S&P 500 was -37% while the NASDAQ Composite Index returned -39.98% (see Charts 1 and 2). The following pages will provide a brief summary on economic and financial events, an explanation of the strategies we employed, what we anticipate for 2009, and the performance of our Funds versus the overall market during the past year.

2008: The Year in Review

The series of events that transpired during 2008 will be discussed in the decades that follow. Detailed explanations of these events would be too long for this letter, but even an abbreviated listing is staggering.

* Multiple financial firm failures and bailouts. 2008 was witness to numerous bank failures that shook investor confidence and altered the Wall Street landscape. The Federal Reserve, through an arranged takeover by JP Morgan Chase, hastily rescued Bear Stearns in March. In July, IndyMac Bancorp failed and was taken over by the Federal Deposit Insurance Corporation (FDIC).

On September 7, Fannie Mae and Freddie Mac were placed in federal conservatorship in the wake of mounting losses. On September 14, Merrill Lynch agreed to be acquired by Bank of America. On September 15, Lehman Brothers, an investment bank that reportedly had never had a losing year in its 158-year history, became the largest firm in history to declare bankruptcy. On September 16, AIG accepted the terms of a Federal Reserve rescue package. Washington Mutual was placed into receivership on September 25, becoming the largest bank failure in U.S. history, and was subsequently acquired by JP Morgan Chase. On September 29, Wachovia agreed to an acquisition by Citigroup and, subsequently, by Wells Fargo. During November, the U.S. Government moved to guarantee hundreds of billions of Citigroup’s toxic assets.

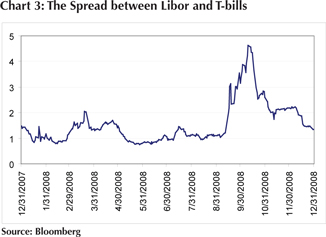

* Frozen credit markets results in government action. Continued woes in the housing market and multiple bank failures culminated in a severe shortage of credit and liquidity in the markets during September. Banks and institutional investors, both keen on avoiding exposure to the next bank failure, acutely restricted the extension of credit. As a result, several measures of credit availability indicated severe shortages (see Chart 3). The Bush Administration, led by Treasury Secretary Henry Paulson, received the approval from Congress to use $800 billion in bailout funds in an attempt to restore confidence. Originally devised as a solution to address the system-wide failure, the bailout funds have actually been used to directly inject capital into the banking system to encourage lending.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 1 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

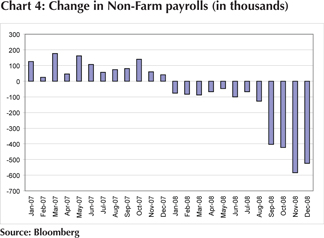

* Declining payrolls and rising unemployment. The sluggish economy has taken its toll on the job market. Employers reduced nonfarm payrolls every month of 2008 (see Chart 4), which has resulted in cumulative job losses of 2.6 million for the full year. As a result, the unemployment rate increased significantly, and now stands at 7.2% as of December, compared to 4.9% at the beginning of the year. More recent readings on the job market have been dismal as well with weekly initial jobless claims remaining well above 500,000 for most of December. The early signs of trouble in the job market, which deteriorated well before declines in GDP, spurred the National Bureau of Economic Research to declare that the current recession began over a year ago in December 2007.

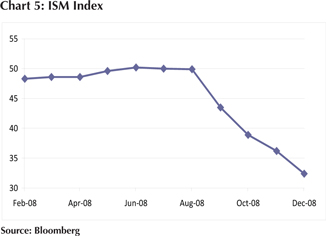

* Outlook for GDP weakening. The most recent reading on GDP shows a decline of 0.5% for the third quarter, driven substantially by a decline in consumer spending, which fell 3.8% and is the largest single component of GDP. As revealed by the minutes from its most recent meeting, the Federal Reserve has revised its expectations for economic activity downward, and expects moderate economic contraction through the first half of 2009. Recent data points concerning gauges of the manufacturing and service sector support the Fed’s evaluation of the economic situation. The ISM Manufacturing Index, which is a gauge of manufacturing activity, came in at 32 during the month of December (see Chart 5). A reading below 50 indicates contraction while a reading above 50 indicates expansion.

* Housing fundamentals remain weak. Home prices in major U.S. cities plummeted by a record 18% in October according to S&P/Case-Shiller, bringing prices back down to their early-2004 levels. Home prices declined every month through October 2008, and as home values decline further coupled with the losses in the equity markets, the wealth effect many homeowners feel also diminishes which results in less overall spending. Compounding this problem is the rising number of homes going into foreclosure, high inventory levels, and the emerging tendency for modified mortgages to become distressed once again. The housing market continues to present an obstacle to an economic recovery, and remains at the core of the ongoing credit crisis.

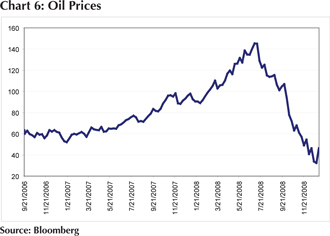

* Volatile energy and commodity prices. While there has been dramatic volatility in the equity markets, it has been common place in the energy and commodity markets as well. For example, oil prices rose from approximately $96 per barrel at the beginning of 2008 to a peak of $147 per barrel in mid-July, and have since fallen to approximately $40 at the end of December, a 73% decline from its peak price (see Chart 6). From its July highs, this represents a savings of nearly $1 billion per day in the U.S. The price of gold has also experienced wide swings, and has ranged from approximately $700 to $1,000 per ounce in 2008, and ended the year at $882 per ounce. While the heightened level of prices during the first half of the year gave way to inflationary concerns, the decline in prices in the second half of 2008 combined with generally falling asset prices and de-leveraging is now causing deflationary concerns.

* High expectations for the incoming President. Barack Obama’s victory in the presidential election as well as the formation of his cabinet has removed a key source of uncertainty heading into 2009. A strong Democratic performance in congressional elections also gives President-elect Obama a strong base in both houses of congress to pass legislation. Among the first pieces of legislation expected to pass is an economic stimulus package purported to be approximately $800 billion, and will be implemented in part to create jobs through an overhaul of the nation’s infrastructure.

| | |

Page 2 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

* Domestic automakers facing bankruptcy. By the end of 2008, it became apparent that Detroit automakers were facing cash shortages as the demand for vehicles dampened amid the economic slump. While Ford maintained that it has enough cash to last through 2009, General Motors and Chrysler were in need of emergency funds to avoid bankruptcy. As a result, the Bush Administration provided over $13 billion in bailout funds to see the two companies through the first quarter of 2009. Uncertainty remains over the future of the automakers, with the problem effectively being passed to the incoming administration of President-elect Obama.

Our Investment Approach

Equity Funds

Each quarter of 2008 was witness to periods of heightened volatility that presented a difficult environment for investors.

We employed various tactics and strategies throughout the year in response to the changing economic and securities market environment. For instance, our asset allocation model that attempts to identify the risk of the stock market detected a change from a low risk environment to a more cautious environment in mid-January, 2008. Consequently, we established a 25% defensive position in The Muirfield Fund® and the equity portion of The Defensive Balanced Fund in mid-January and maintained this posture until late September. In late September and early October, we increased our defensive posture to approximately 50% as the stock market began to react negatively to the events surrounding the credit crisis and mounting economic challenges. As the stock market began to stabilize from late October through late November, we gradually began to increase our exposure to the stock market, finishing the year with a 59% allocation to the stock market in The Muirfield Fund® and the equity portion of The Defensive Balanced Fund.

We also took an active approach toward managing our exposure to growth versus value investments and across the range of market capitalization in our fund-of-funds based mutual funds. We began the year with an overweight in growth investments and placed an emphasis on the shares of mid-cap companies. The positioning served performance well until the beginning of the third quarter, which coincided with a significant change in market leadership. More specifically, value stocks staged a remarkable recovery in mid-July after under-performing the market for most of the prior year, and was driven by financial stocks that rebounded as investors bet on a bottom coupled with government imposed restrictions on short-selling certain financial stocks. Mid-July also witnessed a collapse in commodity prices as concerns over global demand emerged as a result of economic weakness in many of the world’s largest economies. A change in leadership also took place across the spectrum of market capitalization, with small-cap companies unexpectedly performing the best during the third quarter followed by large-cap stocks then mid-cap stocks. During the third quarter, we established a position in small-cap stocks due to relative valuations as well as favorable historical performance during recessions. As the third quarter progressed we also reduced our overweight in growth investments until we were essentially neutral to growth versus value in recognition of increasing market volatility that was leading to frequent changes in market leadership. During the fourth quarter we continued to add incremental exposure to value investments and finished the year slightly overweighted toward value.

We also managed industry sector exposure throughout the year as well, which has been largely characterized by our decision to underweight the financial sector for the entire year even as we shifted toward value investments. In addition, through the third quarter we maintained overweights to the energy and industrial materials sectors. As economic fundamentals deteriorated, we shifted our sector overweights to traditionally defensive sectors such as consumer staples, utilities and health care. Another aspect of our investment posture is characterized by the decision to allocate funds in markets outside of the U.S. We maintained exposure to developed as well as emerging international markets until the third quarter, when we began reducing and ultimately eliminating all direct international holdings. This coincided with the rapid deterioration in global economic fundamentals as well as the strengthening of the dollar.

Fixed Income Funds

In 2008, the underlying theme in the credit markets was, “flight to quality.” Uncertainty throughout global economies and capital markets was cited as the ultimate culprit. Confidence took its first hit when the value of lower quality securitized mortgage products and their derivatives, created and issued within the past several years, came under intense scrutiny. As questions began to swirl around these products, questions surrounding their value became clouded. Throughout the year the uncertainty mounted and ultimately the credit markets became frozen. Investors became wary of each other and their involvement in these markets, resulting in fear that ebbed and flowed throughout most of the year. U.S. Treasury securities, which are synonymous with safety, became the product of choice for investors looking to protect their money. U.S. Treasuries realized

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 3 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

unprecedented gains in 2008 as investors scrambled for these securities. Several times during the fourth quarter of 2008, fervor for U.S. Treasury bills reached such extreme levels that yields were actually quoted as being negative. This means that investors were actually paying the government more than they would receive at the maturity of the security. The difference between the yields of various fixed-income securities versus U.S. Treasury securities (spreads) widened significantly at various points throughout the year. We believe this created investment opportunities in certain areas of the fixed-income market. Throughout the year, we maneuvered our position in The U.S. Government Bond Fund to capitalize on yield opportunities without compromising safety. For the majority of the year, The U.S. Government Bond Fund was invested in U.S. Government agency securities (e.g., Federal Home Loan Corporation). These securities provided a higher yield than U.S. Treasuries, but lagged U.S. Treasuries in capital appreciation. As the year progressed we invested a portion in other areas that offered higher yields, such as investment grade corporate bonds.

For the 23rd consecutive calendar year, The Flex-funds® Money Market Fund performance was in the top 10% of iMoneyNet first-tier retail money market funds. The Fund’s strong performance was accomplished by maintaining its focus on high-quality money market securities and expense controls.

2009: Challenges and Opportunities Abound

It appears that the year ahead will present a number of challenges as well as opportunities regarding the financial markets and economy. Many anticipate that the current economic situation will worsen before experiencing any improvements, especially since the housing market remains weak, credit markets have not yet returned to a normal functioning status, and the unemployment rate seems destined to move higher. The Federal Reserve currently anticipates that GDP will range from a decline of 0.2% to an increase of 1.1% in 2009, and that the unemployment rate will have a range of approximately 7.1% to 7.6%.

We believe there are several key market and economic factors to monitor in 2009. The process of reducing debt levels among consumers and businesses alike will continue to have an impact on asset prices. However, the Federal Reserve has employed creative and unconventional tactics to offset the full impact of the de-leveraging process. The Federal Reserve has also played an important role in easing stresses that have been prominent in the credit markets, and we will continue to monitor credit spreads since further narrowing is needed to return to longer-term averages. We will also search for signs of stabilization in the housing market, which we believe will portend a recovery in the broader economy.

While the aforementioned challenges appear daunting, especially given the impact of these events during 2008, it is important to note that the equity markets are forward-looking in nature. In other words, equity markets tend to anticipate future economic activity, and thus tend to recover many months before the broader economy experiences recovery. As a result, we are constantly reviewing our models and other quantitative factors in search of opportunities to adjust our market exposures that will benefit our shareholders.

For now, we believe many uncertainties remain in the economy and the financial markets. Therefore, we are maintaining a partially defensive position in The Muirfield Fund® and The Defensive Balanced Fund. Going forward, we will continue to monitor conditions carefully and look for opportunities to adjust our weights among growth and value stocks, large-, mid-, and small-caps, and domestic and international investments in order to enhance returns and manage risk for our clients. We will also continue to proactively manage our sector exposures, and will make adjustments as we modify our outlook for the economy and financial markets. On the following pages you will find a review of how our Mutual Funds have performed. Please read the commentaries to learn more about the investment decisions that were made during the past year.

These are trying times in the financial services industry. Since 1974, Meeder Financial has navigated through periods of extremely difficult market environments. On behalf of all of the associates at Meeder Asset Management and The Flex-funds®, I thank you for the continued trust and confidence you have placed in our investment management services and be assured that we are 100% committed to working with you and helping you achieve your most important financial goals

|

| Sincerely, |

|

Robert S. Meeder, Jr. President The Flex-funds® December 31, 2008 |

| | |

Page 4 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

2008 Mutual Fund Commentary

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 5 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

The Money Market Fund

Annual Market Perspective

FORTHE 23RDCONSECUTIVEYEAR, THE FLEX-FUNDS® MONEY MARKET FUNDPERFORMANCEWASINTHETOP 10%OFIMONEYNETFIRST-TIERRETAILMONEYMARKETFUNDS.

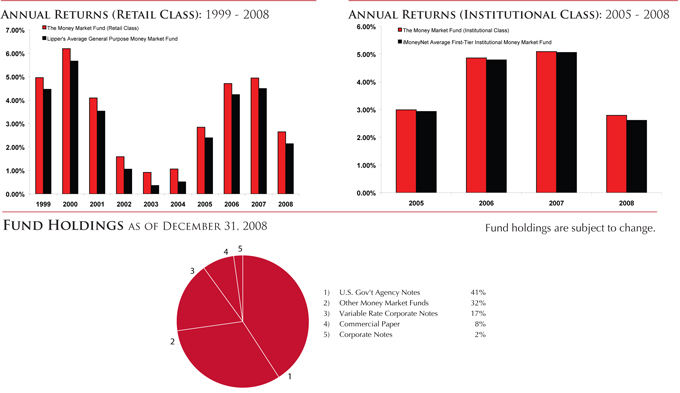

The Retail Class of The Flex-funds® Money Market Fund (the Fund) continued to rank among the top general-purpose money market funds in the country during the year ended December 31, 2008, according to iMoneyNet, Inc., The Retail Class of The Flex-funds® Money Market Fund closed the quarter with a 1.76% 7-day compound yield. The average first-tier retail money market fund finished the quarter with a 0.90% 7-day compound yield. For the 23rd consecutive year, The Flex-funds® Money Market Fund performance was in the top 10% of iMoneyNet first-tier retail money market funds.

The fourth quarter of 2008 capped off what was a rugged year in the capital markets all around the world. Short-term investment markets came to a halt as the credit crisis peaked between the third and fourth quarters, which quickened the pace of migration to safer investments. This ultimately pushed yields on short-term investments to unprecedented lows by the time the quarter came to a close. For example, the 90-day U.S. Treasury Bill started the quarter yielding less than one percent (0.90%), yet during the quarter would actually turn negative (-0.04%). Investors were willing to pay the government in order to hold these securities. Top rated commercial paper on average realized an even greater slump declining from 4.50% to under one percent (0.46%) by quarter end.

Our investment strategy focused on high quality investments and supported a longer than average weighted average maturity. As the quarter progressed we continued to overweight U.S. Government agency securities while we reduced our holdings in corporate debt securities. At the end of the year the Fund’s composition was as follows: 41% U.S. Government agency securities, 27% corporate debt securities and 32% in other money market funds. We also maintained a longer duration throughout the year relative to the benchmark, which aided performance as interest rate levels declined. The strategy served the Fund well as the retail class finished 2008 in the top ten percent versus its peers according to iMoneyNet, Inc.

As we start into 2009 we believe the Fund is positioned properly to perform well. As always, the quality of the Fund’s investments will remain top priority as credit quality concerns may persist. We believe actions taken by the U.S. Government to quell the credit crisis should prove successful, however effects of a stagnant economy may linger. With a weak economy at hand, short-term interest rates should remain under pressure in the upcoming quarter. Again, a longer than average weighted average maturity should prove beneficial. We will monitor the markets and our strategy continuously keeping in mind the best interest of our shareholders.

| | |

Page 6 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | Since

Inception | |

The Money Market Fund

(Retail Class) | | 2.65 | % | | 3.23 | % | | 3.38 | % | | 4.92 | %1 |

Lipper’s Average General Purpose Money Market Fund | | 2.14 | % | | 2.75 | % | | 2.87 | % | | 4.36 | %2 |

Current & Effective Yields | | 7-day Compound Yield: 1.76%* | | | 7-day Simple Yield: 1.75%* | |

The Money Market Fund

(Institutional Class) | | 2.79 | % | | N/A | | | N/A | | | 3.92 | %3 |

iMoneyNet Average First-Tier

Institutional Money Market Fund | | 2.61 | % | | N/A | | | N/A | | | 3.84 | %4 |

Current & Effective Yields | | 7-day Compound Yield: 1.91%* | | | 7-day Simple Yield: 1.89%* | |

1 | Inception date for the Retail class of The Money Market Fund was 3/27/85. |

2 | Performance results for the Lipper Average General Purpose Money Market Fund is from 3/31/85 through 12/31/08. |

3 | Inception date for the Institutional class of The Money Market Fund was 12/28/04. |

4 | Performance results for the iMoneyNet Average First-Tier Institutional Money Market Fund is from 12/28/04 through 12/31/08. |

| * | For the seven-day period ended December 31, 2008, yield quotations more closely reflect the current earnings of The Money Market Fund than do total return quotations. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of both the retail class and the institutional class of The Money Market Fund during the periods shown above. Investments in The Money Market Fund are neither insured nor guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in The Money Market Fund. Source for average general purpose money market fund data: Lipper, Inc. Source for average first-tier institutional money market fund data: iMoneyNet, Inc.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 7 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

The U.S. Government Bond Fund

Annual Market Perspective

THE U.S. GOVERNMENT BOND FUNDISONEOFLESSTHAN 2%OF

INTERMEDIATE-TERM U.S. GOVERNMENT BOND FUNDSTHATEXCEEDEDTHE

BARCLAYS CAPITAL INTERMEDIATE-TERM GOVERNMENT CREDIT INDEX

FOREACHOFTHEPAST 3YEARS.

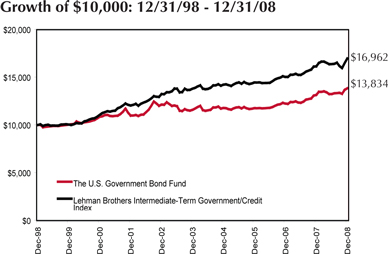

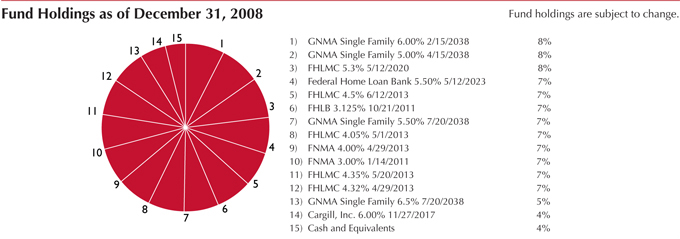

The Flex-funds® U.S. Government Bond Fund (the Fund) returned 5.16% for the full year compared against the benchmark return of 5.07%. Flight to quality ruled the fixed-income markets for all of 2008. As fears mounted that the economy would continue to weaken at the hands of the credit crisis, U.S. Treasury and Government Agency fixed-income securities appreciated in price. For a majority of 2008, spreads between U.S. Treasury securities and U.S. Government agency securities maintained above average yield spreads. We have attempted to take advantage of this dislocation between the security types by purchasing U.S. Government agency products. We also maintained a longer duration throughout the year relative to the benchmark, which aided performance as interest rate levels declined.

As we move into a new year and the first quarter of 2009, we anticipate economic weakness to persist. Even with stimulus activities from the U.S. Government and the Federal Reserve we believe the credit crisis will suppress growth adding to the length of the current recessionary environment. As mentioned above, investments in the Fund remain in U.S. Government agency securities as we believe they offer an attractive spread over U.S. Treasury securities. A move to add some high quality investment grade corporate bonds has been addressed as the Fund can hold a small portion of these securities (up to 20%). A move to add corporate bonds to the Fund would be based on the current attractive spreads offered by these securities. We believe the mix of these securities combined with our duration position should allow us to provide solid performance to our shareholders. We will continue to monitor economic data and our models for potential changes.

| | |

Page 8 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The U.S. Government Bond Fund1 | | 5.16 | % | | 3.61 | % | | 3.30 | % | | 1.01 | % | | 1.72 | % |

Lehman Bros. Intermediate-Term | | | | | | | | | | | | | | | |

Government/Credit Index2 | | 5.07 | % | | 4.21 | % | | 5.43 | % | | — | | | — | |

1 | The inception date of The U.S. Government Bond Fund is 12/31/1988. |

2 | The Lehman Brothers Intermediate-Term Government/Credit Index is an unmanaged index of fixed-rate bonds issued by the U.S. Government and its agencies that are rated investment-grade or higher, have one to ten years remaining until maturity, and at least $100 million outstanding. The Lehman Brothers Intermediate-Term Government/Credit Index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The U.S. Government Bond Fund during the periods shown above. Source for index data: Morningstar, Inc.

The Growth of $10,000 chart compares The U.S. Government Bond Fund’s value to the Lehman Brothers Intermediate-Term Government/Credit Index. The chart is intended to give you a general idea of how the Fund performed compared to this benchmark over the period from December 31, 1998 to December 31, 2008. An understanding of the differences between the Fund and this index is important. The Lehman Brothers Intermediate-Term Government/Credit Index is a hypothetical unmanaged index of fixed-rate bonds issued by the U.S. Government and its agencies that are rated investment-grade or higher, have one to ten years remaining until maturity, and at least $100 million outstanding. This index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 9 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

The Muirfield Fund®

Annual Market Perspective

THE MUIRFIELD FUND®HASMAINTAINEDADEFENSIVEPOSITIONINCASH

EQUIVALENTSECURITIESOFATLEAST 25%SINCE JANUARY 2008.

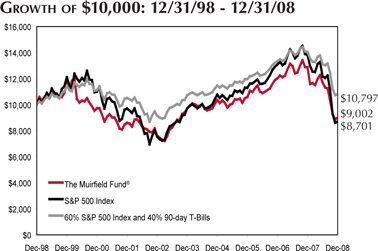

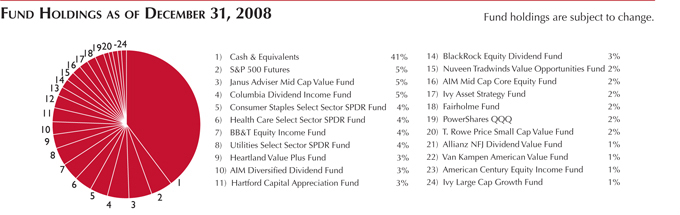

The Flex-funds Muirfield Fund® returned –30.07% for the 12 months ending December 31, 2008. By comparison, the S&P 500 Index declined -37.00%.

Since mid-January of 2008, The Muirfield Fund® has been invested in a partially defensive position. We initially established a 25% defensive position and have maintained a cash position of at least 25% and up to 55% as a result of deterioration in our trend and technical factors in our quantitative models.

As was discussed in the President’s letter, the prevailing theme during 2008, and particularly during the fourth quarter, was the intense focus on the impact from the credit crisis and the severity of the spillover into a weak economy already in the midst of a recession. While bankruptcies and failures slowed in the financial sector, distress spread to the domestic auto industry that turned to the government for funds to continue operations. As the stock market began to react more negatively to the events surrounding the credit crisis and mounting economic challenges, we increased our defensive posture in late September and early October. As the stock market began to demonstrate stability in late October through late November, we gradually began to increase our exposure toward the market. We ended the year with a 59% allocation to the equity market.

We actively managed our investment posture throughout the year as indications from our investment models changed. We began the year with an overweight in growth investments, and gradually shifted to a more neutral stance among value investments in recognition of increasing market volatility. We established a position in small-cap stocks in the third quarter as well due to attractive relative valuations and favorable historical small-cap performance during recessions, although this position harmed performance during the fourth quarter. We also managed our sector exposure, which has been largely characterized by our decision to underweight the financial sector for the entire year. In addition, we maintained overweights in the materials and energy sectors, which benefited performance until the third quarter, at which point we rotated to traditionally defensive sectors. Finally, we maintained exposure to developed as well as emerging international markets until the third quarter, when we began reducing and ultimately eliminating all direct international holdings.

| | |

Page 10 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The Muirfield Fund®1 | | -30.07 | % | | -1.50 | % | | -1.05 | % | | 1.38 | % | | 1.88 | % |

S&P 500 Index2 | | -37.00 | % | | -2.19 | % | | -1.38 | % | | — | | | — | |

60/40 Index3 | | -23.15 | % | | 0.15 | % | | 0.77 | % | | — | | | — | |

1 | Inception date for The Muirfield Fund® is 8/10/88. |

2 | The S&P 500 Index is a widely recognized unmanaged index of common stock prices that does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

3 | The 60/40 Index is comprised of 60% S&P 500 Index & 40% 90-day T-bills. This index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Muirfield Fund® during the periods shown above. Source for index data: Morningstar, Inc.

The Growth of $10,000 chart compares the value of The Muirfield Fund® to the S&P 500 Index, the Fund’s broad-based benchmark, and to an index composed of 60% of the S&P 500 Index and 40% of 90-day T-bills (“the 60/40 index”). The chart is intended to give you a general idea of how the Fund performed compared to these indices over the period from December 31, 1998 to December 31, 2008. An understanding of the differences between the Fund and these indices is important. The benchmark indices are hypothetical unmanaged indices of common stocks and 90-day T-bills that do not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 11 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

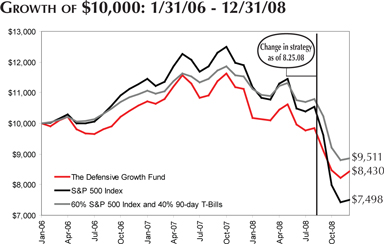

The Defensive Balanced Fund (formerly The Defensive Growth Fund)

Annual Market Perspective

ACHANGEINSTRATEGYDURING AUGUSTINCLUDESANALLOCATIONTO

FIXEDINCOMESECURITIESOFATLEAST 30%ATALLTIMES.

The Defensive Balanced Fund (the Fund) returned –24.16% for the 12 months ending December 31, 2008. By comparison, the S&P 500 Index declined -37.00%. The Defensive Balanced Fund was previously known as The Defensive Growth Fund until August 25, 2008. At that point, the Fund’s strategy was altered to include an allocation to fixed income securities of at least 30% at all times.

Since mid-January of 2008, the equity portion of The Defensive Balanced Fund has been invested in a partially defensive position. We initially established a 25% defensive position and have maintained a cash position of at least 25% and up to 55% as a result of deterioration in our trend and technical factors in our quantitative models. Regarding our fixed income allocation, we predominantly held government agency securities, but gradually increased our position in corporate debt instruments. As of December 31, our fixed income allocation was comprised of 65% government agency securities and 35% corporate debt obligations.

As was discussed in the President’s letter, the prevailing theme during 2008, and particularly during the fourth quarter, was the intense focus on the impact from the credit crisis and the severity of the spillover into a weak economy already in the midst of a recession. While bankruptcies and failures slowed in the financial sector, distress spread to the domestic auto industry that turned to the government for funds to continue operations.

We actively managed our equity exposure throughout the year as indications from our investment models changed. We began the year with an overweight in growth investments, and gradually shifted to a more neutral stance among value investments in recognition of increasing market volatility. We established a position in small-cap stocks in the third quarter as well due to attractive relative valuations and favorable historical small-cap performance during recessions, although this position harmed performance during the fourth quarter. We also managed our sector exposure, which has been largely characterized by our decision to underweight the financial sector for the entire year. In addition, we maintained overweights in the materials and energy sectors, which benefited performance until the third quarter, at which point we rotated to traditionally defensive sectors. Finally, we maintained exposure to developed as well as emerging international markets until the third quarter, when we began reducing and ultimately eliminating all direct international holdings.

| | |

Page 12 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | |

| | | 8/25/08 to

12/31/08* | | | 1 Year | | | Since

Inception | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The Defensive Balanced Fund | | -14.70 | % | | -24.16 | % | | -5.69 | %1 | | 1.39 | % | | 1.80 | % |

S&P 500 Index2 | | -29.39 | % | | -37.00 | % | | -9.40 | % | | — | | | — | |

Blended Index3 | | -12.30 | % | | -17.54 | % | | 1.70 | % | | — | | | — | |

1 | Inception date for The Defensive Balanced Fund is 1/31/06. |

2 | The S&P 500 Index is a widely recognized unmanaged index of common stock prices that does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

3 | The Blended Index is comprised of 70% 60/40 Index and 30% Lehman Brothers Intermediate-Term Government/Credit Index. The 60/40 Index is comprised of 60% S&P 500 Index and 40% 90-day T-bills. Lehman Brothers Intermediate-Term Government/Credit Index is an unmanaged index of fixed-rate bonds issued by the U.S. Government and its agencies that are rated investment grade or higher and have one to ten years remaining until maturity and at least $100 million outstanding. These indices do not take into account the deduction of expenses associated with a mutual fund such as investment management and accounting fees. An investor cannot invest directly in an index. |

* | On August 25, 2008, The Defensive Growth Fund became known as The Defensive Balanced Fund and its investment strategy changed. This Fund will always invest at least 30% and may invest up to 70% of its assets primarily in equity mutual funds. In addition, this Fund will always invest at least 30% and may invest up to 70% of its assets primarily in investment grade bonds, money market instruments, or exchange traded funds. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Defensive Balanced Fund during the periods shown above. Source for index data: Morningstar, Inc.

The Growth of $10,000 chart compares The Defensive Balanced Fund’s value to the S&P 500 Index, the Fund’s broad-based benchmark, and to the Blended Index which is comprised of 70% 60/40 Index and 30% Lehman Brothers Intermediate-Term Government/Credit Index. The chart is intended to give you a general idea of how the Fund performed compared to these indices over the period from its inception on January 31, 2006 through December 31, 2008. An understanding of the differences between the Fund and these indices is important. The benchmark indices are hypothetical unmanaged indices of common stock that do not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 13 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

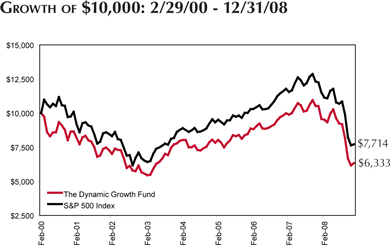

The Dynamic Growth Fund

Annual Market Perspective

OURDELIBERATEUNDERWEIGHTOFTHEFINANCIALSECTORALLOWED THE DYNAMIC GROWTH FUNDTOLARGELYCIRCUMVENTTURMOILINTHEBANKINGINDUSTRY.

Although 2008 began in the midst of a credit crisis spurred on by the deteriorating housing market, few investors anticipated the events that would unfurl. Among other incidents, the year was witness to financial and credit market turmoil, a complete transformation of Wall Street, record-setting bankruptcies, continued pressures in the housing market, a bubble (followed by a subsequent burst) in energy and commodity prices, and a deepening recession.

We took an active approach toward managing our exposure to growth versus value investments. We began the year with an overweight in growth investments and placed an emphasis on the shares of mid-cap companies. The positioning served performance well until the beginning of the third quarter, which coincided with a significant change in market leadership. More specifically, value stocks staged a remarkable recovery in mid-July after under-performing the market for most of the prior year, which was driven by financial stocks that rebounded as investors bet on a bottom coupled with government imposed restrictions on short-selling certain financial stocks. During the third quarter, we established a position in small-cap stocks due to relative valuations as well as favorable historical performance during recessions. As the third quarter progressed we also reduced our overweight in growth investments until we were essentially neutral to growth versus value in recognition of increasing market volatility that was leading to frequent changes in market leadership. During the fourth quarter we continued to add incremental exposure to value investments and finished the year slightly overweighted toward value.

We also managed industry sector exposure throughout the year as well, which has been largely characterized by our decision to underweight the financial sector for the entire year even as we shifted toward value investments. In addition, through the third quarter we maintained overweights to the energy and industrial materials sectors. As demand for energy and commodity products receded, these overweight positions contributed to our under performance against the S&P 500 benchmark for the year. As economic fundamentals deteriorated, we shifted our sector overweights to traditionally defensive sectors such as consumer staples, utilities and health care. We also maintained exposure to developed as well as emerging international markets until the third quarter, when we began reducing and ultimately eliminating all direct international holdings. This coincided with the rapid deterioration in global economic fundamentals as well as the strengthening of the dollar.

| | |

Page 14 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Year | | | Since

Inception | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The Dynamic Growth Fund | | -39.77 | % | | -4.05 | % | | -5.04 | %1 | | 1.32 | % | | 1.86 | % |

S&P 500 Index2 | | -37.00 | % | | -2.19 | % | | -2.89 | % | | — | | | — | |

1 | Inception date for The Dynamic Growth Fund is 2/29/00. |

2 | The S&P 500 Index is a widely recognized unmanaged index of common stock prices that does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Dynamic Growth Fund during the periods shown above. Source for index data: Morningstar, Inc.

The Growth of $10,000 chart compares The Dynamic Growth Fund’s value to the S&P 500 Index, the Fund’s broad-based benchmark. The chart is intended to give you a general idea of how the Fund performed compared to this benchmark over the period from its inception on February 29, 2000 to December 31, 2008. An understanding of the differences between the Fund and this index is important. The S&P 500 Index is a hypothetical unmanaged index of common stocks that does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 15 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

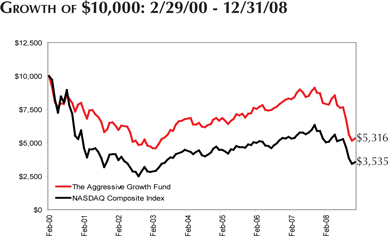

The Aggressive Growth Fund

Annual Market Perspective

DEFENSIVESECTORALLOCATIONAIDEDOUTPERFORMANCEAGAINSTTHEBENCHMARKFOR 2008.

We began 2008 with an overweight in growth investments and placed an emphasis on the shares of mid-cap companies. The positioning served performance well until the beginning of the third quarter, which coincided with a significant change in market leadership. More specifically, value stocks staged a remarkable recovery in mid-July after under-performing the market for most of the prior year, and was driven by financial stocks that rebounded as investors bet on a bottom coupled with government imposed restrictions on short-selling certain financial stocks. Mid-July also witnessed a collapse in commodity prices as concerns over global demand emerged as a result of economic weakness in many of the world’s largest economies.

During the third quarter, we established a position in small-cap stocks due to relative valuations as well as favorable historical performance during recessions. As the third quarter progressed we also reduced our overweight in growth investments until we were essentially neutral to growth versus value in recognition of increasing market volatility that was leading to frequent changes in market leadership. During the fourth quarter we continued to add incremental exposure to value investments and finished the year slightly overweighted toward value.

We also managed industry sector exposure throughout the year as well, which has been largely characterized by our decision to underweight the financial sector for the entire year even as we shifted toward value investments. In addition, through the third quarter we maintained overweights to the energy and industrial materials sectors. While this positioning benefited performance during the first half of 2008, it detracted from performance during the third quarter as global demand for energy and commodity products waned. As economic fundamentals deteriorated, we shifted our sector overweights to traditionally defensive sectors such as consumer staples, utilities, and health care. We also maintained exposure to developed as well as emerging international markets until the third quarter, when we began reducing and ultimately eliminating all direct international holdings. This coincided with the rapid deterioration in global economic fundamentals as well as the strengthening of the dollar.

| | |

Page 16 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Year | | | Since

Inception | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The Aggressive Growth Fund | | -38.98 | % | | -4.42 | % | | -6.90 | %1 | | 1.70 | % | | 1.76 | % |

NASDAQ Composite Index2 | | -39.98 | % | | -3.95 | % | | -11.09 | % | | — | | | — | |

1 | Inception date for The Aggressive Growth Fund is 2/29/00. |

2 | The NASDAQ Composite Index is a broad-based capitalization-weighted index of all Nasdaq National Market and small-cap stocks that does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Aggressive Growth Fund during the periods shown above. Source for index data: Morningstar, Inc.

The Growth of $10,000 chart compares The Aggressive Growth Fund’s value to the Nasdaq Composite Index, the Fund’s broad-based benchmark. The chart is intended to give you a general idea of how the Fund performed compared to this benchmark over the period from its inception on February 29, 2000 to December 31, 2008. An understanding of the differences between the Fund and this index is important. The Nasdaq Composite Index is a hypothetical unmanaged index of small-cap and Nasdaq National Market stocks that does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 17 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

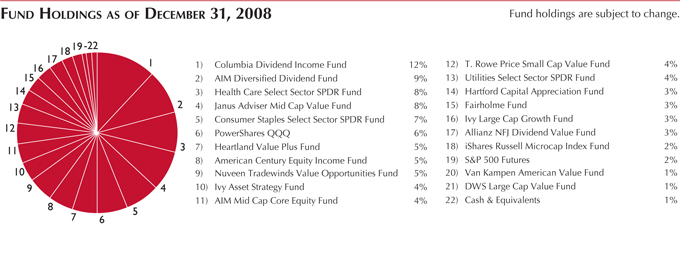

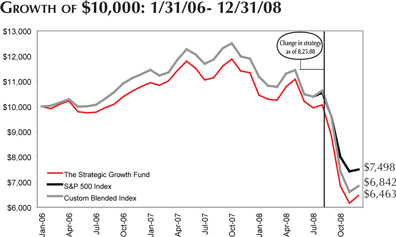

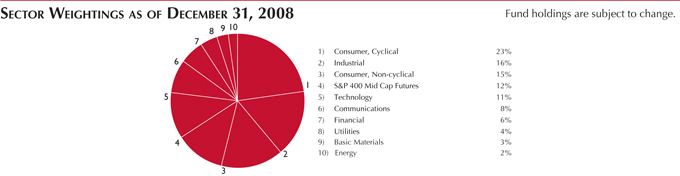

The Strategic Growth Fund (formerly The Focused Growth Fund)

Annual Market Perspective

THECHANGEININVESTMENTSTRATEGYDURING AUGUSTENSUREDBROADEXPOSURETONUMEROUSASSETCLASSES.

The Strategic Growth Fund (the Fund) was previously known as The Focused Growth Fund until August of 2008, at which point the strategy and investment mix of the Fund was altered. The Strategic Growth Fund is now designed to hold fixed allocations across six distinct investment categories, although the mix of investments selected to represent the investment category is variable and actively managed. Before August 25, 2008, the Fund was comprised of exchange-traded funds with an investment style similar to that of The Dynamic Growth Fund.

The fixed allocations were determined by examining an optimal asset allocation strategy, and as a result the current target allocation mix is comprised of the following: 25% large-cap holdings, 20% mid-cap holdings, 17.5% international holdings, 12.5% small-cap holdings, 12.5% real estate holdings, and 12.5% commodities holdings. Since the Fund’s change in strategy during August, it has underperformed the benchmark S&P 500 Index as a result of poor performance among the commodities and real estate investment trust asset classes. However, the Fund’s performance against a custom benchmark, which is based upon the aforementioned fixed asset allocations, is more favorable. Since the Fund’s change in strategy, it has returned approximately -36% versus the custom benchmark return of approximately -35.5%.

The Fund’s performance during the first half of 2008 was impacted favorably from our overweight positions in growth and mid-cap investments, as well as our underweight toward the financial sector. Subsequent to the change in investment strategy, we experienced favorable results from our holdings in various asset classes. For example, our large-cap holding of Columbia Dividend Income returned –13.61% during the fourth quarter of 2008 compared against the benchmark S&P 500 return of –21.95%. We experienced less favorable performance with other funds such as the Hartford Capital Appreciation Fund, which returned –26.09%.

| | |

Page 18 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | |

| | | 8/25/08 to

12/31/08* | | | 1 Year | | | Since

Inception | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The Strategic Growth Fund | | -36.05 | % | | -43.00 | % | | -13.90 | %1 | | 1.39 | % | | 1.92 | % |

S&P 500 Index2 | | -29.39 | % | | -37.00 | % | | -9.40 | % | | — | | | — | |

Custom Blended Index3 | | -35.56 | % | | -42.51 | % | | -12.19 | % | | — | | | — | |

1 | Inception date for The Strategic Growth Fund is 1/31/06. |

2 | The S&P 500 Index is a widely recognized unmanaged index of common stock prices that does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

3 | The Custom Blended Index is comprised of 25% S&P 500, 20% S&P Midcap 400, 12.5% Russell 2000, 12.5% Dow Jones Wilshire Real Estate Investment Trust, 12.5% Goldman Sachs Commodity Index, 12% Morgan Stanley Capital International Europe, Australasia, and Far East, and 5.5% Morgan Stanley Capital International Europe Emerging Markets Index. These indices do not take into account the deduction of expenses associated with a mutual fund such as investment management and accounting fees. An investor cannot invest directly in an index. |

| * | On August 25, 2008, The Focused Growth Fund became known as The Strategic Growth Fund and its investment strategy changed. This Fund will pursue its goal by investing primarily in open-end or closed-end investment companies that seek capital growth or appreciation without regard to current income. In addition, this fund will always have set allocations to U.S. large-cap equities, U.S. mid-cap equities, U.S. small-cap equities, non-U.S./International (including emerging markets) equities, real estate equities and commodity based equities. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Strategic Growth Fund during the periods shown above. Source for index data: Morningstar, Inc.

The Growth of $10,000 chart compares The Strategic Growth Fund’s value to the S&P 500 Index, the Fund’s broad-based benchmark, and the Custom Blended Index, which is described above. The chart is intended to give you a general idea of how the Fund performed compared to these indices over the period from its inception on January 31, 2006 to December 31, 2008. An understanding of the differences between the Fund and these indices is important. The benchmark indices are hypothetical unmanaged indices of common stock that do not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 19 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

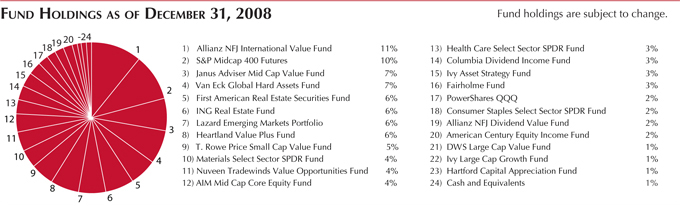

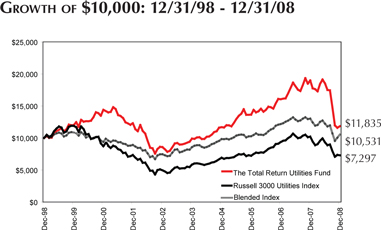

The Total Return Utilities Fund (formerly The Socially Responsible Utilities Fund)

Annual Market Perspective

WEBELIEVETHATNONEOFOURCOMPANIESARESTRESSEDBYCONDITIONSINTHEFINANCIALMARKETS,ANDTHEYARESOLIDENTERPRISESWITHVALUABLELONG-TERMASSETS.

Relative to other kinds of utility and infrastructure investments, The Total Return Utilities Fund went from the head of the pack during the first half of the year to the back of the pack during the last two quarters. We also experienced perhaps our worst relative year in a history of consistently solid returns. However, our Fund is not that different from the way it appeared at the beginning of the year, or the beginning of 2007 for that matter. The simple fact is that investor selling at the end of the third quarter and into the fourth quarter was broad-based, without much regard for sector, company fundamentals, or long-term prospects.

Performance on a relative basis was favorable during the first half of the year compared against the Russell 3000 Utilities Index. However, the second half proved challenging, particularly during the fourth quarter, and led to under performance for the full year. Three areas that degraded returns the most in the fourth quarter were energy-related, foreign telecom, and infrastructure enablers. Energy-related stocks were obviously impacted by the astonishing declines in commodity prices, a factor that we hardly expect to see repeated in coming quarters, though we did miss the potential magnitude of decline in the second half of 2008. Foreign telecom negatively impacted performance due to the combination of slowing usage and currency declines. Additionally, infrastructure enablers experienced sharp declines, and we believe the declines may be attributable to the aggressive character of investors in these stocks, since these are among the best-positioned companies for global upgrades in telecom and electric grid infrastructure.

Still, none of our companies are stressed by conditions in the financial markets, and they are solid enterprises with valuable long-term assets. Our outperforming stocks during the year embodied the themes of solid market position, inelastic recurring revenues, and a visible growth path. During the third quarter, we believe the valuations experienced among the holdings were extraordinary, especially in the context of the revenue sources for these companies, which diminish least of any sector when the economy is soft. However, the stock prices have experienced significant declines just as much as elsewhere into the fourth quarter, but this has not dissuaded us from our opinion that long-term investors will look back on this moment as an extraordinary buying opportunity.

| | |

Page 20 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Year | | | 10 Year | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The Total Return Utilities Fund1 | | -37.63 | % | | 3.65 | % | | 1.70 | % | | 1.90 | % | | 2.10 | % |

Blended Index2 | | -19.16 | % | | 4.21 | % | | 0.52 | % | | — | | | — | |

Russell 3000 Utilities Index3 | | -28.48 | % | | 4.58 | % | | -3.10 | % | | — | | | — | |

1 | Inception date for The Total Return Utilities Fund is 6/21/1995. |

2 | The Blended Index is comprised of 60% of the Russell 3000 Utilities Index and 40% of the Lehman Bros. Long Credit Index. One cannot invest directly in an index. |

3 | The Russell 3000 Utilities Index is a market capitalization-weighted index that is comprised of utility stocks that are included in the Russell 3000 Index. This index does not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Total Return Utilities Fund during the periods shown above. Because The Total Return Utilities Fund concentrates its investments in public utility companies, the value of the Fund’s shares may fluctuate more than if invested in a greater number of industries. Changes in interest rates may also affect the value of Utility stocks, and rising interest rates can be expected to reduce the Fund’s net asset value. Source for index data: Bloomberg, LP.

The Growth of $10,000 chart compares The Total Return Utilities Fund’s value to the Russell 3000 Utilities Index, the Fund’s broad-based benchmark, and to the Blended Index (comprised of 60% of the Russell 3000 Utilities Index and 40% of the Lehman Bros. Long Credit Index). The chart is intended to give you a general idea of how the Fund performed compared to these benchmarks over the period from December 31, 1998 to December 31, 2008. An understanding of the differences between the Fund and these indices is important. The benchmark indices do not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 21 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

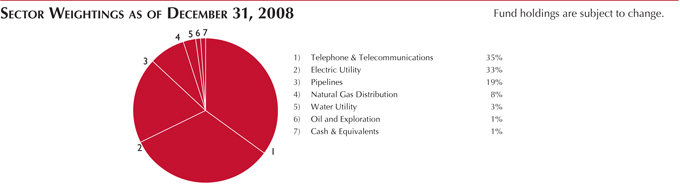

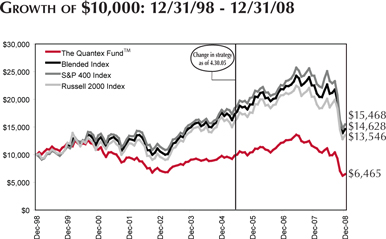

The Quantex Fund™

Annual Market Perspective

THE QUANTEX FUND®EMPLOYSAQUANTITATIVEINVESTMENTMODELTOSELECTSTOCKSOFCOMPANIESTHATHAVEDECLINEDSIGNIFICANTLYINPRICEANDOFSMALL,UP-AND-COMINGCOMPANIES.

For 2008, the composition of The Quantex Fund™ (the Fund) was overweighted in consumer goods and underweighted in energy, with an overall tilt toward value investments. The position in consumer goods contributed slightly to performance while the position in energy detracted from performance for the full year. While the shares of energy companies generally experienced favorable returns through the first half of 2008, the second half of the year witnessed downward pressure on share prices as global demand for energy products deteriorated. Additionally, the shares of small and mid-cap companies performed worse during the fourth quarter compared to the shares of large-cap companies, but outperformed large-cap companies for the full year.

For the full year, Family Dollar Stores was the best performing stock in the Fund, with an increase of nearly 39%. Hasbro, a toy and game manufacturer, also experienced positive returns for the full year with an increase of nearly 17%. Relative to our benchmark, we also benefited from the performance of pharmaceutical companies, with King Pharmaceuticals returning approximately 4% and Watson Pharmaceuticals returning approximately –2%. The worst performing stocks during 2008 included Circuit City, which entered bankruptcy, and Ambac Financial group, which was severely impacted by the credit crisis. Consumer products companies, such as Liz Claiborne Inc. and Brunswick Corporation, as well as several real estate investment trust companies harmed our performance for the year.

We have consistently employed our quantitative stock selection process for The Quantex Fund™ since April 30, 2005. We utilize rankings from our financial model to determine which 100 securities are to be held in the Fund on an annual basis. As a result, the Fund is rebalanced once each year in January. For 2009, the updated composition of the Fund displays large overweights in hardware (a technology sub-sector) and consumer services, and underweights in health care and energy. From a broader standpoint, the Fund has a 24% allocation to information technology, 45% allocation to the service economy, and 31% to the manufacturing economy. Additionally, there is a strong preference for value holdings in the 2009 composition, with mid-cap value companies comprising 36% of the Fund, followed by small-cap value with 23%, and mid-cap core with 22% of the composition.

| | |

Page 22 | | The Flex-funds® 2008 Annual Report | December 31, 2008 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

PERFORMANCE PERSPECTIVE

Period & Average Annual Total Returns as of December 31, 2008

| | | | | | | | | | | | | | | | | | |

| | | 1 Year | | | 4/30/05 to

12/31/08* | | | 5 Year | | | 10 Year | | | Net Expense

Ratio+ | | | Gross Expense

Ratio+ | |

The Quantex Fund™1 | | -43.12 | % | | -9.25 | % | | -6.56 | % | | -4.27 | % | | 1.56 | % | | 2.09 | % |

Blended Index2 | | -34.98 | % | | -2.86 | % | | -0.44 | % | | 3.88 | % | | — | | | — | |

Russell 2000 Index3 | | -33.79 | % | | -2.68 | % | | -0.89 | % | | 3.07 | % | | — | | | — | |

S&P 400 Mid-Cap Index4 | | -36.23 | % | | -3.04 | % | | -0.09 | % | | 4.45 | % | | — | | | — | |

1 | The inception date of The Quantex FundTM is 3/20/1985. |

2 | The Blended Index consists of 50% Russell 2000 Index and 50% S&P 400 Mid-Cap Index. One cannot invest directly in an index. |

3 | The Russell 2000 Index is a market-capitalization weighted index measuring performance of the smallest 2,000 companies, on a market capitalization basis, in the Russell 3000 Index. One cannot invest directly in an index. |

4 | The S&P 400 Mid-Cap Index is an unmanaged index of common stock prices of mid-sized companies. One cannot invest directly in an index. |

* | The Quantex Fund™ was previously known as The Highlands Growth Fund. On April 30, 2005, The Highlands Growth Fund changed its name to The Quantex Fund™, also changing the Fund’s investment objective and strategies. The Highlands Growth Fund focused on large-cap equities, while The Quantex Fund™ utilizes quantitative investment strategies that invest primarily in small- and mid-cap equities. Due to this change in strategies on April 30, 2005, the S&P 500 Index is a more comparative index for Fund performance prior to April 30, 2005. The Russell 2000 Index and S&P 400 Mid-Cap Index are more comparative indices for Fund performance after April 30, 2005. |

+ | The Net and Gross Expense Ratios are percentages of the Fund’s average net assets as they are shown in the most current Fund’s Prospectus. The Net Expense Ratio includes all waivers, reimbursements and expenses paid indirectly. |

Performance quoted represents past performance. Past Performance does not guarantee future results. All performance figures represent average annual total returns for the periods ended December 31, 2008, and assume reinvestment of all dividend and capital gain distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Current month-end performance may be obtained at www.flexfunds.com or by calling 1.800.325.3539. Management fees were waived and/or expenses were reimbursed in order to reduce the operating expenses of The Quantex Fund™ during the periods shown above. Source for index data: Morningstar, Inc.

The Quantex Fund™ was previously known as The Highlands Growth Fund. On April 30, 2005, The Highlands Growth Fund changed its name to The Quantex Fund™, also changing the Fund’s investment objective and strategies. Due to this, the Russell 2000 Index and the S&P 400 Mid-Cap Index are more comparative indices for Fund performance.

The Growth of $10,000 chart compares the value of The Quantex Fund™ to the S&P 400 Mid-Cap Index, the Russell 2000 Index, and a Blended Index (comprised of 50% Russell 2000 and 50% S&P 400 Mid-Cap). The chart is intended to give you a general idea of how the Fund performed compared to these benchmarks over the period from December 31, 1998 to December 31, 2008. An understanding of the differences between the Fund and these indices is important. The benchmark indices do not take into account the deduction of expenses associated with a mutual fund, such as investment management and accounting fees. One cannot invest directly in an index.

Past performance does not guarantee future results. The chart and the table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| | |

The Flex-funds® 2008 Annual Report | December 31, 2008 | | Page 23 |

| | |

| The Flex-funds® | | 2008 Annual Report | December 31, 2008 |

Shareholder Expense Analysis (Unaudited)

Shareholders of mutual funds pay ongoing expenses, such as advisory fees, distribution and service fees (12b-1 fees) and other fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples below are based on an investment of $1,000 invested at the beginning of the period and held for the six-month period from June 30, 2008 to December 31, 2008.

ACTUAL EXPENSES

| | | | | | | | | | | | |

| | | Beginning

Account Value

(6/30/2008) | | Ending

Account Value

(12/31/2008) | | Expenses Paid

During Period1

(6/30/2008 -

12/31/2008) | | Expense Ratio

(Annualized) | |

The Muirfield Fund® | | $ | 1,000.00 | | $ | 769.70 | | $ | 6.14 | | 1.38 | % |

The Dynamic Growth Fund | | | 1,000.00 | | | 658.60 | | | 5.67 | | 1.36 | % |

The Aggressive Growth Fund | | | 1,000.00 | | | 679.80 | | | 6.50 | | 1.54 | % |

The Defensive Balanced Fund | | | 1,000.00 | | | 845.70 | | | 7.10 | | 1.53 | % |

The Strategic Growth Fund | | | 1,000.00 | | | 633.40 | | | 6.45 | | 1.57 | % |

The Quantex Fund™ | | | 1,000.00 | | | 654.90 | | | 7.53 | | 1.81 | % |

The Total Return Utilities Fund | | | 1,000.00 | | | 639.80 | | | 8.33 | | 2.02 | % |

The U.S. Government Bond Fund | | | 1,000.00 | | | 1,044.80 | | | 5.09 | | 0.99 | % |

The Money Market Fund - Retail Class | | | 1,000.00 | | | 1,011.00 | | | 2.53 | | 0.50 | % |

The Money Market Fund - Institutional Class | | | 1,000.00 | | | 1,011.70 | | | 2.02 | | 0.40 | % |