UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04367

Columbia Funds Series Trust I

(Exact name of registrant as specified in charter)

One Financial Center, Boston, Massachusetts 02111

(Address of principal executive offices) (Zip code)

Scott R. Plummer

5228 Ameriprise Financial Center

Minneapolis, MN 55474

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-612-671-1947

Date of fiscal year end: December 31

Date of reporting period: December 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Columbia Real Estate Equity Fund

Annual Report for the Period Ended December 31, 2010

Table of Contents

The views expressed in this report reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Fund. References to specific securities should not be construed as a recommendation or investment advice.

President’s Message

Dear Shareholder:

The Columbia Management story began over 100 years ago, and today, we are one of the nation’s largest dedicated asset managers. The recent acquisition by Ameriprise Financial, Inc. brings together the talents, resources and capabilities of Columbia Management with those of RiverSource Investments, Threadneedle (acquired by Ameriprise in 2003) and Seligman Investments (acquired by Ameriprise in 2008) to build a best-in-class asset management business that we believe is truly greater than its parts.

RiverSource Investments traces its roots to 1894 when its then newly-founded predecessor, Investors Syndicate, offered a face-amount savings certificate that gave small investors the opportunity to build a safe and secure fund for retirement, education or other special needs. A mutual fund pioneer, Investors Syndicate launched Investors Mutual Fund in 1940. In the decades that followed, its mutual fund products and services lineup grew to include a full spectrum of styles and specialties. More than 110 years later, RiverSource continues to be a trusted financial products leader.

Threadneedle, a leader in global asset management and one of Europe’s largest asset managers, offers sophisticated international experience from a dedicated U.K. management team. Headquartered in London, it is named for Threadneedle Street in the heart of the city’s financial district, where British investors pioneered international and global investing. Threadneedle was acquired in 2003 and today operates as an affiliate of Columbia Management.

Seligman Investments’ beginnings date back to the establishment of the investment firm J. & W. Seligman & Co. in 1864. In the years that followed, Seligman played a major role in the geographical expansion and industrial development of the United States. In 1874, President Ulysses S. Grant named Seligman as fiscal agent for the U.S. Navy — an appointment that would last through World War I. Seligman helped finance the westward path of the railroads and the building of the Panama Canal. The firm organized its first investment company in 1929 and began managing its first mutual fund in 1930. In 2008, J. & W. Seligman & Co. Incorporated was acquired and Seligman Investments became an offering brand of RiverSource Investments, LLC.

We are proud of the rich and distinctive history of these firms, the strength and breadth of products and services they offer, and the combined cultures of pioneering spirit and forward thinking. Together we are committed to providing more for our shareholders than ever before.

| n | | A singular focus on our shareholders. Our business is asset management, so investors are our first priority. We dedicate our resources to identifying timely investment opportunities and provide a comprehensive choice of equity, fixed-income and alternative investments to help meet your individual needs. |

| n | | First-class research and thought leadership. We are dedicated to helping you take advantage of today’s opportunities and anticipate tomorrow’s. We stay abreast of the latest investment trends and ideas, using our collective insight to evaluate events and transform them into solutions you can use. |

| n | | A disciplined investment approach. We aren’t distracted by passing fads. Our teams adhere to a rigorous investment process that helps ensure the integrity of our products and enables you and your financial advisor to match our solutions to your objectives with confidence. |

When you choose Columbia Management, you can be confident that we will take the time to understand your needs and help you and your financial advisor identify the solutions that are right for you. Because at Columbia Management, we don’t consider ourselves successful unless you are.

Sincerely,

J. Kevin Connaughton

President, Columbia Funds

Investors should consider the investment objectives, risks, charges and expenses of a mutual fund carefully before investing. For a free prospectus, which contains this and other important information about the funds, visit www.columbiamanagement.com. The prospectus should be read carefully before investing.

Columbia Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA, and managed by Columbia Management Investment Advisers, LLC.

© 2011 Columbia Management Investment Advisers, LLC. All rights reserved.

Fund Profile – Columbia Real Estate Equity Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiamanagement.com for daily and most recent month-end performance updates.

Summary

1-year return as of 12/31/10

| | |

| |

| | +26.04% Class A shares (without sales charge) |

| |

| | +27.95% FTSE NAREIT Equity REITs Index |

Summary

| n | | For the 12-month period that ended December 31, 2010, the fund’s Class A shares returned 26.04% without sales charge. |

| n | | The fund’s return lagged its benchmark, the FTSE NAREIT Equity REITs Index,1 and the average return of the funds in its peer group, the Lipper Real Estate Funds Classification.2 |

| n | | The fund’s overweight in the office real estate group and an emphasis on lower-risk, more defensive stocks in the residential sector accounted for its modest shortfall to these comparative measures. |

Portfolio Management

Arthur Hurley has managed the fund since September 2006. From 2006 until joining Columbia Management Investment Advisers, LLC in May 2010, Mr. Hurley was associated with the fund’s previous adviser or its predecessors as an investment professional.

| 1 | The FTSE National Association of Real Estate Investment Trusts (NAREIT) Equity REITs Index tracks performance of all publicly traded equity real estate investment trusts (REITs). |

| 2 | Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the fund. Lipper makes no adjustment for the effect of sales loads. |

Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

1

Economic Update – Columbia Real Estate Equity Fund

Summary

For the 12-month period that ended December 31, 2010

| | n | | The U.S. stock market, as measured by the S&P 500 Index, delivered solid returns, despite a summer correction. Emerging market stocks, as measured by the MSCI Emerging Markets Index (Net), outperformed U.S. stocks as well as stock markets in developed foreign markets, as measured by the MSCI EAFE Index (Net). | |

| | |

| S&P Index | | MSCI Emerging Markets Index |

| |

| |

|

15.06% | | 18.88% |

| | |

| MSCI EAFE Index | | |

| | |

| | |

| |

| | |

7.75% | | |

| | n | | Modest economic growth and relatively low interest rates boosted bond market returns until the final months of the period. The Barclays Capital Aggregate Bond Index delivered solid results. High-yield bonds was the leading fixed-income sector, as measured by the JPMorgan Developed BB High Yield Index. | |

| | |

| Barclays Aggregate Index | | JPMorgan Index |

| |

| |

|

6.54% | | 12.86% |

The U.S. economy expanded at a modest pace in 2010, as measured by gross domestic product (GDP). Yet, growth was strong enough to allay fears of a relapse into recession. GDP expanded by 3.7% in the first quarter of 2010, 1.7% in the second quarter, 2.6% in the third quarter and 3.2% in the fourth quarter. With the Federal Reserve Board providing additional monetary stimulus to shore up economic growth and the extension of key tax cuts for the next two years, economists are revising 2011 expectations upward. In addition, there is evidence that consumers are starting to feel more confident. Even though job growth has not met expectations, the unemployment rate fell to 9.4% in December.

Consumer spending on cars, clothing and other goods generally trended higher throughout the year. Holiday spending rose 5.5% between November 5 and December 24, in all retail categories, excluding automobiles, compared with the same period in 2009, according to MasterCard Advisors’ SpendingPulse, which tracks spending on all transactions including cash. Analysts say that an increase in personal savings and a decline in consumer debt gave consumers confidence to spend a little more this year. The personal savings rate edged higher, ending November, the last month for which data was available, at 5.7%. Personal income also increased modestly during the year.

News on the job front was mostly positive in 2010. A good portion of the jobs added in March, April and May were temporary, government-sponsored census positions, which began to unwind in June, July and August. However, private sector payroll employment trended modestly higher, massive layoffs declined and job growth turned solidly positive, with the addition of 384,000 new jobs in the last quarter of the year.

Despite some glimmers of improvement early in the year, the housing market remained troublesome. Both new and existing home sales fell after a federal tax credit for new and repeat homebuyers expired. Distressed properties pressured prices. And foreclosures continued — another drag on prices. The inventory of unsold new homes rose from 7.2 months to 10.5 months over the one-year period, according to the National Association of Realtors, raising concerns that a meaningful turnaround in housing could remain elusive for months to come.

Reports from the business side of the economy were generally positive. A key measure of the nation’s manufacturing situation — the Institute for Supply Management’s Index — took a somewhat surprising turn higher in the final months of the period. Industrial production was disappointingly flat at year end, while the amount of manufacturing capacity utilized — a key measure of the health of the manufacturing sector — inched higher.

Stocks moved higher despite summer setback

Against a strengthening economic backdrop, a stock market rally that began early in 2009 continued into 2010 despite a summer setback linked to a debt crisis brewing in Europe, which raised concerns among U.S. investors. These fears were short-lived and stocks regained their footing in September 2010, moving higher through the end of the year.

2

Economic Update (continued) – Columbia Real Estate Equity Fund

The S&P 500 Index1 returned 15.06% for the 12-month period. Outside the United States, stock market returns were mixed. The MSCI EAFE Index (Net),2 a broad gauge of stock market performance in foreign developed markets, returned 7.75% (in U.S. dollars) for the period, as concerns about the impact of a bailout for weak euro zone economies weighed on the markets. Emerging stock markets were more resilient. The MSCI Emerging Markets Index (Net)3 returned 18.88% (in U.S. dollars) for the

12-month period.

Bonds delivered solid returns

As the economy strengthened, bonds delivered solid returns. The Barclays Capital Aggregate Bond Index4 returned 6.54%. The high-yield bond market led the fixed-income markets. For the 12 months covered by this report, the JPMorgan Developed BB High Yield Index5 returned 12.86%. Despite rising yields in the second half of the year, the Treasury market was also positive. The Barclays Capital U.S. Treasury Index6 returned 5.87%. However, municipal bonds struggled in the final months of the period, as interest rates inched higher and issue supply surged ahead of the expiration of the Buy America Bonds program. Nevertheless, the Barclays Capital Municipal Bond Index7 gained 2.38% for the period. Despite positive economic activity, the Federal Reserve Board (the Fed) kept a key short-term interest rate — the federal funds rate — close to zero.

Past performance is no guarantee of future results.

| 1 | The Standard & Poor’s (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks. |

| 2 | The Morgan Stanley Capital International Europe, Australasia, Far East (MSCI EAFE) Index (Net) is a free float- adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada. As of May 27, 2010, the MSCI EAFE Index (Net) consisted of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom. |

| 3 | The Morgan Stanley Capital International Emerging Markets (MSCI EM) Index (Net) is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. As of May 27, 2010, the MSCI EM Index (Net) consisted of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand and Turkey. |

| 4 | The Barclays Capital Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar-denominated and non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity. |

| 5 | The JPMorgan Developed BB High Yield Index is an unmanaged index designed to mirror the investable universe of the U.S. dollar developed, BB-rated, high yield corporate debt market. |

| 6 | The Barclays Capital U.S. Treasury Index includes public obligations of the U.S. Treasury. Treasury bills are excluded by the maturity constraint. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS, are excluded. STRIPS are excluded from the index because their inclusion would result in double-counting. |

| 7 | The Barclays Capital Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. |

Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

3

Performance Information – Columbia Real Estate Equity Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiamanagement.com for daily and most recent month-end performance updates.

| | | | |

| Net asset value per share as of | |

| |

12/31/10 ($) | | | | |

Class A | | | 12.41 | |

Class B | | | 12.43 | |

Class C | | | 12.40 | |

Class I | | | 12.42 | |

Class R | | | 12.40 | |

Class W | | | 12.41 | |

Class Z | | | 12.43 | |

| Distributions declared per share | |

| |

01/01/10 – 12/31/10 ($) | | | | |

Class A | | | 0.26 | |

Class B | | | 0.18 | |

Class C | | | 0.18 | |

Class I | | | 0.12 | |

Class R | | | 0.10 | |

Class W | | | 0.10 | |

Class Z | | | 0.29 | |

|

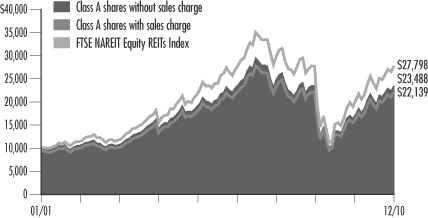

| Performance of a $10,000 investment 01/01/01 – 12/31/10 |

The chart above shows the change in value of a hypothetical $10,000 investment in Class A shares of Columbia Real Estate Equity Fund during the stated time period, and does not reflect the deduction of taxes that a shareholder may pay on fund distributions or on the redemption of fund shares.

| | | | | | | | |

Performance of a $10,000 investment 01/01/01 – 12/31/10 | |

| Sales charge | | without | | | with | |

Class A | | | 23,488 | | | | 22,139 | |

Class B | | | 22,124 | | | | 22,124 | |

Class C | | | 22,107 | | | | 22,107 | |

Class I | | | n/a | | | | n/a | |

Class R | | | n/a | | | | n/a | |

Class W | | | n/a | | | | n/a | |

Class Z | | | 24,035 | | | | n/a | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Average annual total return as of 12/31/10 (%) | |

| Share class | | A | | | B | | | C | | | I | | | R | | | W | | | Z | |

| Inception | | 11/01/02 | | | 11/01/02 | | | 10/13/03 | | | 9/27/10 | | | 9/27/10 | | | 9/27/10 | | | 04/01/94 | |

| Sales charge | | without | | | with | | | without | | | with | | | without | | | with | | | without | | | without | | | without | | | without | |

1-year | | | 26.04 | | | | 18.84 | | | | 25.07 | | | | 20.07 | | | | 25.02 | | | | 24.02 | | | | n/a | | | | n/a | | | | n/a | | | | 26.29 | |

5-year | | | 2.77 | | | | 1.56 | | | | 2.01 | | | | 1.83 | | | | 2.01 | | | | 2.01 | | | | n/a | | | | n/a | | | | n/a | | | | 3.03 | |

10-year/Life | | | 8.91 | | | | 8.27 | | | | 8.26 | | | | 8.26 | | | | 8.26 | | | | 8.26 | | | | 6.52 | | | | 6.36 | | | | 6.51 | | | | 9.17 | |

The “with sales charge” returns include the maximum initial sales charge of 5.75% for Class A shares and the applicable contingent deferred sales charge of 5.00% in the first year, declining to 1.00% in the sixth year, and eliminated thereafter for Class B shares and 1.00% for Class C shares in the first year only. The “without sales charge” returns do not include the effect of sales charges. If they had, returns would be lower.

Performance results reflect any fee waivers or reimbursements of fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower.

All results shown assume reinvestment of distributions. Class I and Z shares are sold at net asset value with no distribution and service (Rule 12b-1) fees. Class R and W shares are sold at net asset value with a distribution (12b-1) fee. Class I, R, W, and Z shares have limited eligibility and the investment minimum requirements may vary. Please see the fund’s prospectuses for details. Performance for different share classes will vary based on differences in sales charges and fees associated with each class.

The tables do not reflect the deduction of taxes that a shareholder may pay on fund distributions or on the redemption of fund shares.

Class A, Class B and Class C are newer classes of shares. Class A and Class B share performance information includes the returns of Class Z shares (the oldest existing share class) for periods prior to their inception. Class C share performance information includes returns of Class B shares for the period from November 1, 2002 through October 12, 2003, and the returns of Class Z shares for periods prior thereto. These returns reflect differences in sales charges, but have not been restated to reflect any differences in expenses (such as distribution and service (Rule 12b-1) fees) between Class Z shares and the newer classes of shares. If differences in expenses had been reflected, the returns shown for periods prior to the inception of the newer classes of shares would have been lower, since the newer classes of shares are subject to distribution and service (Rule 12b-1) fees. Class A and Class B shares were initially offered on November 1, 2002, Class C shares were initially offered on October 13, 2003, Class I, Class R and Class W shares were initially offered on September 27, 2010, and Class Z shares were initially offered on April 1, 1994.

4

Understanding Your Expenses – Columbia Real Estate Equity Fund

Estimating your actual expenses

To estimate the expenses that you paid over the period, first you will need your account balance at the end of the period:

| | n | | For shareholders who receive their account statements from Columbia Management Investment Services Corp., your account balance is available online at www.columbiamanagement.com or by calling Shareholder Services at 800.345.6611. | |

| | n | | For shareholders who receive their account statements from their financial intermediary, contact your financial intermediary to obtain your account balance. | |

| | 1. | Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6. | |

| | 2. | In the section of the table below titled “Expenses paid during the period,” locate the amount for your share class. You will find this number in the column labeled “Actual.” Multiply this number by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period. | |

If the value of your account falls below the minimum initial

investment requirement applicable to you, your account may be subject to a $20 annual fee. This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

As a fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees or exchange fees. There are also ongoing costs, which generally include investment advisory fees, distribution and service (Rule 12b-1) fees and other fund expenses. The information on this page is intended to help you understand the ongoing costs of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your fund’s expenses by share class

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in each share class during the period. The information in the following table is based on an initial investment of $1,000, which is invested at the beginning of the period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the “Actual” column is calculated using the fund’s actual operating expenses and total return for the period. The amount listed in the “Hypothetical” column for each share class assumes that the return each year is 5% before expenses and is calculated based on the fund’s actual operating expenses. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during this period.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing costs of investing in the fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 07/01/10 – 12/31/10 | |

| | | | |

| | | Account value at the

beginning of the period ($) | | | Account value at the end of the period ($) | | | Expenses paid during the period ($) | | | Fund’s annualized

expense ratio (%) | |

| | | Actual | | | Hypothetical | | | Actual | | | Hypothetical | | | Actual | | | Hypothetical | | | Actual | |

Class A | | | 1,000.00 | | | | 1,000.00 | | | | 1,199.30 | | | | 1,018.70 | | | | 7.15 | | | | 6.56 | | | | 1.29 | |

Class B | | | 1,000.00 | | | | 1,000.00 | | | | 1,194.50 | | | | 1,014.92 | | | | 11.28 | | | | 10.36 | | | | 2.04 | |

Class C | | | 1,000.00 | | | | 1,000.00 | | | | 1,193.90 | | | | 1,014.92 | | | | 11.28 | | | | 10.36 | | | | 2.04 | |

Class I | | | 1,000.00 | | | | 1,000.00 | | | | 1,065.20 | * | | | 1,020.37 | | | | 2.58 | * | | | 4.89 | | | | 0.96 | |

Class R | | | 1,000.00 | | | | 1,000.00 | | | | 1,063.60 | * | | | 1,016.33 | | | | 4.73 | * | | | 8.94 | | | | 1.76 | |

Class W | | | 1,000.00 | | | | 1,000.00 | | | | 1,065.10 | * | | | 1,019.06 | | | | 3.28 | * | | | 6.21 | | | | 1.22 | |

Class Z | | | 1,000.00 | | | | 1,000.00 | | | | 1,200.40 | | | | 1,019.96 | | | | 5.77 | | | | 5.30 | | | | 1.04 | |

Expenses paid during the period are equal to the annualized expense ratio for the share class, multiplied by the average account value over the period, then multiplied by the number of days in the fund’s most recent fiscal half-year and divided by 365.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees. Therefore, the hypothetical examples provided may not help you determine the relative total costs of owning shares of different funds. If these transaction costs were included, your costs would have been higher.

| * | For the period September 27, 2010 through December 31, 2010. Class I, Class R and Class W shares commenced operations on September 27, 2010. |

5

Portfolio Manager’s Report – Columbia Real Estate Equity Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiamanagement.com for daily and most recent month-end performance updates.

| | | | |

| Top 10 holdings | | | |

| |

as of 12/31/10 (%) | | | | |

Simon Property Group, Inc. | | | 8.1 | |

Health Care REIT, Inc. | | | 5.6 | |

Alexandria Real Estate Equities, Inc. | | | 5.0 | |

Entertainment Properties Trust | | | 4.3 | |

ProLogis | | | 4.2 | |

Equity Lifestyle Properties, Inc. | | | 4.0 | |

Duke Realty Corp. | | | 4.0 | |

National Retail Properties, Inc. | | | 4.0 | |

Mid-America Apartment Communities, Inc. | | | 3.4 | |

AvalonBay Communities, Inc. | | | 3.4 | |

| | | | |

| Top sectors | | | |

| |

as of 12/31/10 (%) | | | | |

Retail REITs | | | 27.0 | |

Specialized REITs | | | 21.4 | |

Residential REITs | | | 20.5 | |

Office REITs | | | 15.4 | |

Hotel Resorts & Cruise Lines | | | 5.6 | |

Industrial REITs | | | 5.5 | |

Diversified REITs | | | 2.2 | |

Leisure Facilities | | | 1.1 | |

Real Estate Services | | | 1.0 | |

The fund is actively managed and the composition of its portfolio will change over time. Information provided is calculated as a percentage of net assets.

Portfolio Manager’s Report

For the 12-month period that ended December 31, 2010, the fund’s Class A shares returned 26.04% without sales charge. The fund’s benchmark, the FTSE NAREIT Equity REITs Index, returned 27.95%. The average return of the fund’s peer group, the Lipper Real Estate Funds Classification, was 27.60%. In a favorable environment for real estate investment trusts (REITs), the fund achieved solid positive returns. It trailed its benchmark by a small margin due to an overweight in the office group as well as its emphasis on lower-risk, slower-growth properties in the residential sector, which lagged as the economic outlook brightened.

Strengthening economy boosted real estate sector

Signs of an improving economy helped support real estate investments in 2010, in general, but particularly in areas where rental income tends to respond more quickly to a changing environment, such as for lodging institutions and apartments. These shorter-lease properties were among the segment’s best performers. Although the fund was underweight in the group, a position in Starwood Hotels & Resorts Worldwide, Inc. (1.5% of net assets) boosted performance. Starwood gained greater pricing power in setting nightly room rates as the economic climate improved and demand increased. A position in CBL & Associates Properties, Inc. (1.8% of net assets), owner and operator of shopping malls, also benefited from improved utilization rates and greater demand for retail space as consumer spending increased. The fund had less exposure than the benchmark to diversified and industrial REITs, which also helped performance when those groups were hurt by deteriorating rent trends.

A sizeable position in the office sector detracted from performance as investors shifted away from longer-lease duration assets to shorter-lease duration assets, such as lodging and apartments. Stock selection within the residential sector also hurt performance as lower risk, lower growth stocks underperformed their higher-growth peers. In this regard, an overweight relative to the benchmark in Equity Lifestyle Properties, Inc. (4.0% of net assets), an owner of manufactured home communities, detracted from relative performance. Although the stock gained ground, it underperformed the benchmark as investors favored names with exposure to residential markets that were perceived to offer greater growth opportunities. Nationwide Health Properties, Inc. (1.4% of net assets), a REIT that invests in long-term care and medical office facilities, also lost favor as investors traded defensive names for those with more exposure to the economic recovery.

Strategic effort to increase fund’s yield

Given the current environment of generally low interest rates, we sought to increase the dividend yield of the fund. Through security selection, we placed moderately more importance on the dividend yield of individual securities and sought out REITs with relatively low payout ratios and strong balance sheets.

Looking ahead: opportunities and risks

We anticipate continued improvements in the fundamental outlook for real estate investment trusts, given our expectation of a sustained expansion of the economy and

6

Portfolio Manager’s Report (continued) – Columbia Real Estate Equity Fund

improved conditions in the capital markets. Moreover, REITs have the advantage of lower capital costs and greater access to capital, compared to private real estate investors. Nevertheless, some challenges cloud the outlook. First, employment trends need to improve in order to sustain a widespread recovery in underlying REIT fundamentals. Second, any increase in interest rates could undermine property values and make other income-oriented investments appear more attractive. Given these mixed influences affecting real estate investing, we believe it makes sense to have exposure to both defensive properties and to growth-oriented real estate investments, with a tilt in favor of growth opportunities.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings. The outlook for the fund may differ from those presented for other Columbia Funds.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments.

The fund may be subject to the same types of risks associated with direct ownership of real estate, including the decline of property values due to general, local and regional economic conditions. In addition, the fund’s share price will likely be subject to more volatility than the overall stock market because it concentrates in real estate stocks.

7

Investment Portfolio – Columbia Real Estate Equity Fund

December 31, 2010

Common Stocks – 98.6%

| | | | | | | | |

| | | Shares | | | Value ($) | |

| Consumer Discretionary – 2.6% | |

| Hotels, Restaurants & Leisure – 2.6% | | | | | |

Starwood Hotels & Resorts Worldwide, Inc. | | | 94,552 | | | | 5,746,870 | |

Vail Resorts, Inc. (a) | | | 76,167 | | | | 3,963,731 | |

| | | | | | | | |

Hotels, Restaurants & Leisure Total | | | | 9,710,601 | |

| | | | | | | | |

Consumer Discretionary Total | | | | | | | 9,710,601 | |

| | | | | | | | |

| Financials – 96.0% | | | | | |

| Real Estate Investment Trusts (REITs) – 95.0% | |

Alexandria Real Estate Equities, Inc. | | | 259,200 | | | | 18,988,992 | |

AMB Property Corp. | | | 147,300 | | | | 4,670,883 | |

American Campus Communities, Inc. | | | 292,100 | | | | 9,277,096 | |

Apartment Investment & Management Co., Class A | | | 409,800 | | | | 10,589,232 | |

AvalonBay Communities, Inc. | | | 112,700 | | | | 12,684,385 | |

Boardwalk Real Estate Investment Trust CAD (b) | | | 151,137 | | | | 6,270,141 | |

Boston Properties, Inc. | | | 70,036 | | | | 6,030,100 | |

CBL & Associates Properties, Inc. | | | 376,104 | | | | 6,581,820 | |

Cousins Properties, Inc. | | | 989,800 | | | | 8,254,932 | |

Developers Diversified Realty Corp. | | | 600,000 | | | | 8,454,000 | |

DiamondRock Hospitality Co. (a) | | | 892,100 | | | | 10,705,200 | |

Digital Realty Trust, Inc. | | | 198,850 | | | | 10,248,729 | |

Douglas Emmett, Inc. | | | 431,300 | | | | 7,159,580 | |

Duke Realty Corp. | | | 1,216,000 | | | | 15,151,360 | |

Entertainment Properties Trust | | | 350,106 | | | | 16,192,402 | |

Equity Lifestyle Properties, Inc. | | | 271,491 | | | | 15,184,492 | |

Equity Residential Property Trust | | | 187,244 | | | | 9,727,326 | |

Extra Space Storage, Inc. | | | 531,052 | | | | 9,240,305 | |

Federal Realty Investment Trust | | | 104,653 | | | | 8,155,608 | |

General Growth Properties, Inc. | | | 683,400 | | | | 10,579,032 | |

Getty Realty Corp. | | | 294,000 | | | | 9,196,320 | |

Health Care REIT, Inc. | | | 440,307 | | | | 20,976,225 | |

Host Hotels & Resorts, Inc. | | | 376,619 | | | | 6,730,182 | |

LaSalle Hotel Properties | | | 312,200 | | | | 8,242,080 | |

Mid-America Apartment Communities, Inc. | | | 200,932 | | | | 12,757,173 | |

National Retail Properties, Inc. | | | 565,100 | | | | 14,975,150 | |

Nationwide Health Properties, Inc. | | | 146,600 | | | | 5,333,308 | |

ProLogis | | | 1,097,193 | | | | 15,843,467 | |

Public Storage | | | 109,364 | | | | 11,091,697 | |

Ramco-Gershenson Properties Trust | | | 397,407 | | | | 4,947,717 | |

Simon Property Group, Inc. | | | 308,848 | | | | 30,727,287 | |

U-Store-It Trust | | | 655,700 | | | | 6,248,821 | |

Weingarten Realty Investors | | | 303,900 | | | | 7,220,664 | |

| | | | | | | | |

Real Estate Investment Trusts (REITs) Total | | | | | | | 358,435,706 | |

| | | | | | | | |

| | | Shares | | | Value ($) | |

| Real Estate Management & Development – 1.0% | |

Jones Lang LaSalle, Inc. | | | 43,691 | | | | 3,666,549 | |

| | | | | | | | |

Real Estate Management & Development Total | | | | | | | 3,666,549 | |

| | | | | | | | |

Financials Total | | | | | | | 362,102,255 | |

| | | | | | | | |

Total Common Stocks

(cost of $293,042,239) | | | | 371,812,856 | |

| | | | | | | | |

|

Convertible Preferred Stock – 0.5% | |

| | | | | | | | |

| Financials – 0.5% | | | | | | | | |

| Real Estate Investment Trusts (REITs) – 0.5% | |

Alexandria Real Estate Equities, Inc., Series D, 7.000% | | | 82,100 | | | | 2,031,975 | |

| | | | | | | | |

Real Estate Investment Trusts (REITs) Total | | | | | | | 2,031,975 | |

| | | | | | | | |

Financials Total | | | | | | | 2,031,975 | |

| | | | | | | | |

Total Convertible Preferred Stock

(cost of $2,054,963) | | | | 2,031,975 | |

| | | | | | | | |

|

Short-Term Obligation – 0.7% | |

| | | Par ($) | | | | |

Repurchase agreement with Fixed Income Clearing Corp., dated 12/31/10, due 01/03/11 at 0.150%, collateralized by a U.S. Treasury obligation maturing 08/15/19, market value $2,658,600 (repurchase proceeds $2,603,033) | | | 2,603,000 | | | | 2,603,000 | |

| | | | | | | | |

Total Short-Term Obligation

(cost of $2,603,000) | | | | 2,603,000 | |

| | | | | | | | |

Total Investments – 99.8%

(cost of $297,700,202) (c) | | | | | | | 376,447,831 | |

| | | | | | | | |

Other Assets & Liabilities, Net – 0.2% | | | | 839,152 | |

| | | | | | | | |

Net Assets – 100.0% | | | | | | | 377,286,983 | |

Notes to Investment Portfolio:

| (a) | Non-income producing security. |

| (b) | This security denominated in Canadian dollars. |

| (c) | Cost for federal income tax purposes is $298,650,330. |

See Accompanying Notes to Financial Statements.

8

Columbia Real Estate Equity Fund

December 31, 2010

The following table summarizes the inputs used, as of December 31, 2010, in valuing the Fund’s assets:

| | | | | | | | | | | | | | | | |

Description | | Quoted Prices

(Level 1) | | | Other

Significant

Observable

Inputs

(Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | | | Total | |

Total Common Stocks | | $ | 371,812,856 | | | $ | — | | | $ | — | | | $ | 371,812,856 | |

Total Convertible Preferred Stock | | | 2,031,975 | | | | — | | | | — | | | | 2,031,975 | |

Total Short-Term Obligation | | | — | | | | 2,603,000 | | | | — | | | | 2,603,000 | |

| | | | | | | | | | | | | | | | |

Total Investments | | $ | 373,844,831 | | | $ | 2,603,000 | | | $ | — | | | $ | 376,447,831 | |

| | | | | | | | | | | | | | | | |

The Fund’s assets assigned to the Level 2 input category represent certain short-term obligations which are valued using amortized cost, an income approach which converts future cash flows to a present value based upon the discount or premium at purchase.

There were no significant transfers of financial assets between Levels 1 and 2 during the period.

For more information on valuation inputs, please refer to the Security Valuation section in the accompanying Notes to Financial Statements.

At December 31, 2010, the Fund held investments in the following sectors:

| | | | |

Sector (Unaudited) | | % of

Net Assets | |

Financials | | | 96.5 | |

Consumer Discretionary | | | 2.6 | |

| | | | |

| | | 99.1 | |

Short-Term Obligation | | | 0.7 | |

Other Assets & Liabilities, Net | | | 0.2 | |

| | | | |

| | | 100.0 | |

| | | | |

| | |

Acronym | | Name |

| CAD | | Canadian Dollar |

See Accompanying Notes to Financial Statements.

9

Statement of Assets and Liabilities – Columbia Real Estate Equity Fund

December 31, 2010

| | | | | | |

| | | | | ($) | |

| Assets | | Investments, at cost | | | 297,700,202 | |

| | | | | | |

| | Investments, at value | | | 376,447,831 | |

| | Cash | | | 447 | |

| | Receivable for: | | | | |

| | Investments sold | | | 944,534 | |

| | Fund shares sold | | | 307,544 | |

| | Dividends | | | 1,538,017 | |

| | Interest | | | 11 | |

| | Trustees’ deferred compensation plan | | | 49,558 | |

| | Prepaid expenses | | | 4,464 | |

| | | | | | |

| | Total Assets | | | 379,292,406 | |

| | |

| Liabilities | | Payable for: | | | | |

| | Investments purchased | | | 1,007,569 | |

| | Fund shares repurchased | | | 540,322 | |

| | Investment advisory fee | | | 234,321 | |

| | Pricing and bookkeeping fees | | | 8,531 | |

| | Transfer agent fee | | | 90,732 | |

| | Trustees’ fees | | | 5,105 | |

| | Custody fee | | | 3,480 | |

| | Distribution and service fees | | | 13,774 | |

| | Chief compliance officer expenses | | | 306 | |

| | Trustees’ deferred compensation plan | | | 49,558 | |

| | Other liabilities | | | 51,725 | |

| | | | | | |

| | Total Liabilities | | | 2,005,423 | |

| | |

| | | | | | |

| | Net Assets | | | 377,286,983 | |

| | |

| Net Assets Consist of | | Paid-in capital | | | 299,539,076 | |

| | Overdistributed net investment income | | | (849,468 | ) |

| | Accumulated net realized loss | | | (150,371 | ) |

| | Net unrealized appreciation (depreciation) on: | | | | |

| | Investments | | | 78,747,629 | |

| | Foreign currency translations | | | 117 | |

| | | | | | |

| | Net Assets | | | 377,286,983 | |

See Accompanying Notes to Financial Statements.

10

Statement of Assets and Liabilities (continued) – Columbia Real Estate Equity Fund

December 31, 2010

| | | | | | |

| | | | | | |

| Class A | | Net assets | | $ | 27,511,112 | |

| | Shares outstanding | | | 2,217,495 | |

| | Net asset value per share | | $ | 12.41 | (a) |

| | Maximum sales charge | | | 5.75 | % |

| | Maximum offering price per share ($12.41/0.9425) | | $ | 13.17 | (b) |

| | |

| Class B | | Net assets | | $ | 2,985,691 | |

| | Shares outstanding | | | 240,222 | |

| | Net asset value and offering price per share | | $ | 12.43 | (a) |

| | |

| Class C | | Net assets | | $ | 6,900,124 | |

| | Shares outstanding | | | 556,482 | |

| | Net asset value and offering price per share | | $ | 12.40 | (a) |

| | |

| Class I (c) | | Net assets | | $ | 35,387,722 | |

| | Shares outstanding | | | 2,848,391 | |

| | Net asset value, offering and redemption price per share | | $ | 12.42 | |

| | |

| Class R (c) | | Net assets | | $ | 2,639 | |

| | Shares outstanding | | | 213 | |

| | Net asset value, offering and redemption price per share | | $ | 12.40 | (d) |

| | |

| Class W (c) | | Net assets | | $ | 2,641 | |

| | Shares outstanding | | | 213 | |

| | Net asset value, offering and redemption price per share | | $ | 12.41 | (e) |

| | |

| Class Z | | Net assets | | $ | 304,497,054 | |

| | Shares outstanding | | | 24,498,686 | |

| | Net asset value, offering and redemption price per share | | $ | 12.43 | |

| (a) | Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge. |

| (b) | On sales of $50,000 or more the offering price is reduced. |

| (c) | Class I, Class R and Class W shares commenced operations on September 27, 2010. |

| (d) | Net asset value rounds to $12.40 per share due to fractional shares outstanding. |

| (e) | Net asset value rounds to $12.41 per share due to fractional shares outstanding. |

See Accompanying Notes to Financial Statements.

11

Statement of Operations – Columbia Real Estate Equity Fund

For the Year Ended December 31, 2010

| | | | | | |

| | | | | ($) (a) | |

| Investment Income | | Dividends | | | 7,864,747 | |

| | Interest | | | 4,433 | |

| | Foreign taxes withheld | | | (67,558 | ) |

| | | | | | |

| | Total Investment Income | | | 7,801,622 | |

| | |

| Expenses | | Investment advisory fee | | | 2,589,427 | |

| | Distribution fee: | | | | |

| | Class B | | | 24,265 | |

| | Class C | | | 44,792 | |

| | Class R | | | 3 | |

| | Service fee: | | | | |

| | Class A | | | 55,762 | |

| | Class B | | | 8,089 | |

| | Class C | | | 14,930 | |

| | Class W | | | 2 | |

| | Transfer agent fee – Class A, Class B, Class C, Class R, Class W and Class Z | | | 547,068 | |

| | Pricing and bookkeeping fees | | | 94,050 | |

| | Trustees’ fees | | | 32,131 | |

| | Custody fee | | | 14,062 | |

| | Chief compliance officer expenses | | | 1,246 | |

| | Other expenses | | | 250,813 | |

| | | | | | |

| | Expenses before interest expense | | | 3,676,640 | |

| | Interest expense | | | 913 | |

| | | | | | |

| | Total Expenses | | | 3,677,553 | |

| | |

| | Expense reductions | | | (58 | ) |

| | | | | | |

| | Net Expenses | | | 3,677,495 | |

| | |

| | | | | | |

| | Net Investment Income | | | 4,124,127 | |

| | |

| Net Realized and Unrealized Gain (Loss) on Investments and Foreign Currency | | Net realized gain (loss) on: | | | | |

| | Investments | | | 53,184,060 | |

| | Foreign currency transactions | | | 7,103 | |

| | Net realized loss on violation of investment restriction (See Note 10) | | | (7,545 | ) |

| | Reimbursement of realized loss on violation of investment restriction (See Note 10) | | | 7,545 | |

| | | | | | |

| | Net realized gain | | | 53,191,163 | |

| | |

| | Net change in unrealized appreciation (depreciation) on: | | | | |

| | Investments | | | 19,302,073 | |

| | Foreign currency translations | | | 257 | |

| | | | | | |

| | Net change in unrealized appreciation (depreciation) | | | 19,302,330 | |

| | | | | | |

| | Net Gain | | | 72,493,493 | |

| | |

| | | | | | |

| | Net Increase Resulting from Operations | | | 76,617,620 | |

| (a) | Class I, Class R and Class W shares commenced operations on September 27, 2010. |

See Accompanying Notes to Financial Statements.

12

Statement of Changes in Net Assets – Columbia Real Estate Equity Fund

| | | | | | | | | | | | | | |

| Increase (Decrease) in Net Assets | | | | Year Ended

December 31,

2010 ($)(a)(b) | | | Period From

September 1,

2009 through

December 31,

2009 ($)(c) | | | Year Ended

August 31,

2009 ($) | |

| Operations | | Net investment income | | | 4,124,127 | | | | 2,048,366 | | | | 6,478,152 | |

| | Net realized gain (loss) on investments and foreign currency transactions | | | 53,191,163 | | | | 24,306,236 | | | | (91,398,068 | ) |

| | Net change in unrealized appreciation (depreciation) on investments and foreign currency translations | | | 19,302,330 | | | | 7,629,618 | | | | (8,110,279 | ) |

| | | | | | | | | | | | | | |

| | Net increase (decrease) resulting from operations | | | 76,617,620 | | | | 33,984,220 | | | | (93,030,195 | ) |

| | | | |

| Distributions to Shareholders | | From net investment income: | | | | | | | | | | | | |

| | Class A | | | (531,336 | ) | | | (217,802 | ) | | | (551,971 | ) |

| | Class B | | | (47,805 | ) | | | (29,707 | ) | | | (117,661 | ) |

| | Class C | | | (95,953 | ) | | | (33,297 | ) | | | (110,966 | ) |

| | Class I | | | (50,957 | ) | | | — | | | | — | |

| | Class R | | | (20 | ) | | | — | | | | — | |

| | Class W | | | (22 | ) | | | — | | | | — | |

| | Class Z | | | (7,975,040 | ) | | | (3,425,286 | ) | | | (8,341,582 | ) |

| | From return of capital: | | | | | | | | | | | | |

| | Class A | | | — | | | | (151,558 | ) | | | (299,968 | ) |

| | Class B | | | — | | | | (29,124 | ) | | | (73,441 | ) |

| | Class C | | | — | | | | (33,092 | ) | | | (72,111 | ) |

| | Class Z | | | — | | | | (2,168,787 | ) | | | (4,249,735 | ) |

| | | | | | | | | | | | | | |

| | Total distributions to shareholders | | | (8,701,133 | ) | | | (6,088,653 | ) | | | (13,817,435 | ) |

| | | | |

| | Net Capital Stock Transactions | | | 9,449,400 | | | | 9,494,663 | | | | 51,156,494 | |

| | Increase from Regulatory Settlements | | | 22,629 | | | | — | | | | — | |

| | | | | | | | | | | | | | |

| | Total increase (decrease) in net assets | | | 77,388,516 | | | | 37,390,230 | | | | (55,691,136 | ) |

| | | | |

| Net Assets | | Beginning of period | | | 299,898,467 | | | | 262,508,237 | | | | 318,199,373 | |

| | End of period | | | 377,286,983 | | | | 299,898,467 | | | | 262,508,237 | |

| | Undistributed (overdistributed) net investment income at end of period | | | (849,468 | ) | | | (387,652 | ) | | | 1,268,255 | |

| (a) | Class I, Class R and Class W shares commenced operations on September 27, 2010. |

| (b) | Class I, Class R and Class W shares reflect activity for the period September 27, 2010 through December 31, 2010 |

| (c) | The fund changed its fiscal year end from August 31 to December 31. |

See Accompanying Notes to Financial Statements.

13

|

| Statement of Changes in Net Assets (continued) – Columbia Real Estate Equity Fund |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Capital Stock Activity | |

| | | Year Ended

December 31, 2010 | | | Period From

September 1, 2009

through

December 31, 2009 (c) | | | Year Ended

August 31, 2009 | |

| | | Shares | | | Dollars ($) | | | Shares | | | Dollars ($) | | | Shares | | | Dollars ($) | |

Class A | | | | | | | | | | | | | | | | | | | | | | | | |

Subscriptions | | | 909,223 | | | | 10,332,381 | | | | 148,133 | | | | 1,400,964 | | | | 897,568 | | | | 7,501,890 | |

Distributions reinvested | | | 40,227 | | | | 466,486 | | | | 36,378 | | | | 347,579 | | | | 103,384 | | | | 796,102 | |

Redemptions | | | (543,168 | ) | | | (6,044,112 | ) | | | (251,800 | ) | | | (2,376,319 | ) | | | (733,801 | ) | | | (5,988,913 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) | | | 406,282 | | | | 4,754,755 | | | | (67,289 | ) | | | (627,776 | ) | | | 267,151 | | | | 2,309,079 | |

| | | | | | |

Class B | | | | | | | | | | | | | | | | | | | | | | | | |

Subscriptions | | | 15,589 | | | | 179,794 | | | | 4,866 | | | | 44,893 | | | | 26,122 | | | | 254,768 | |

Distributions reinvested | | | 3,404 | | | | 39,297 | | | | 5,598 | | | | 53,604 | | | | 22,182 | | | | 170,811 | |

Redemptions | | | (110,506 | ) | | | (1,256,435 | ) | | | (46,753 | ) | | | (442,409 | ) | | | (194,445 | ) | | | (1,599,367 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net decrease | | | (91,513 | ) | | | (1,037,344 | ) | | | (36,289 | ) | | | (343,912 | ) | | | (146,141 | ) | | | (1,173,788 | ) |

| | | | | | |

Class C | | | | | | | | | | | | | | | | | | | | | | | | |

Subscriptions | | | 226,594 | | | | 2,494,066 | | | | 126,941 | | | | 1,237,016 | | | | 97,202 | | | | 833,369 | |

Distributions reinvested | | | 7,494 | | | | 86,990 | | | | 6,394 | | | | 61,091 | | | | 22,330 | | | | 170,897 | |

Redemptions | | | (151,955 | ) | | | (1,693,165 | ) | | | (49,543 | ) | | | (470,948 | ) | | | (196,401 | ) | | | (1,646,317 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) | | | 82,133 | | | | 887,891 | | | | 83,792 | | | | 827,159 | | | | (76,869 | ) | | | (642,051 | ) |

| | | | | | |

Class I (a)(b) | | | | | | | | | | | | | | | | | | | | | | | | |

Subscriptions | | | 2,855,527 | | | | 34,553,546 | | | | — | | | | — | | | | — | | | | — | |

Distributions reinvested | | | 4,171 | | | | 50,933 | | | | — | | | | — | | | | — | | | | — | |

Redemptions | | | (11,307 | ) | | | (138,200 | ) | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase | | | 2,848,391 | | | | 34,466,279 | | | | — | | | | — | | | | — | | | | — | |

| | | | | | |

Class R (a)(b) | | | | | | | | | | | | | | | | | | | | | | | | |

Subscriptions | | | 213 | | | | 2,500 | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase | | | 213 | | | | 2,500 | | | | — | | | | — | | | | — | | | | — | |

| | | | | | |

Class W (a)(b) | | | | | | | | | | | | | | | | | | | | | | | | |

Subscriptions | | | 225 | | | | 2,650 | | | | — | | | | — | | | | — | | | | — | |

Redemptions | | | (12 | ) | | | (150 | ) | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase | | | 213 | | | | 2,500 | | | | — | | | | — | | | | — | | | | — | |

| | | | | | |

Class Z | | | | | | | | | | | | | | | | | | | | | | | | |

Subscriptions | | | 8,883,775 | | | | 101,334,335 | | | | 2,795,492 | | | | 26,785,491 | | | | 15,480,870 | | | | 128,665,264 | |

Distributions reinvested | | | 401,949 | | | | 4,657,790 | | | | 334,240 | | | | 3,200,691 | | | | 976,848 | | | | 7,579,012 | |

Redemptions | | | (11,894,503 | ) | | | (135,619,306 | ) | | | (2,147,820 | ) | | | (20,346,990 | ) | | | (10,673,077 | ) | | | (85,581,022 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) | | | (2,608,779 | ) | | | (29,627,181 | ) | | | 981,912 | | | | 9,639,192 | | | | 5,784,641 | | | | 50,663,254 | |

| (a) | Class I, Class R and Class W shares commenced operations on September 27, 2010. |

| (b) | Class I, Class R and Class W shares reflect activity for the period September 27, 2010 through December 31, 2010 |

| (c) | The Fund changed its fiscal year end from August 31 to December 31. |

See Accompanying Notes to Financial Statements.

14

Financial Highlights – Columbia Real Estate Equity Fund

Selected data for a share outstanding throughout each period is as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | Year Ended

December 31, | | | Period Ended

December 31, | | | Year Ended August 31, | |

| | 2010 | | | 2009 (a) | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net Asset Value, Beginning of Period | | $ | 10.07 | | | $ | 9.11 | | | $ | 13.85 | | | $ | 20.72 | | | $ | 29.07 | | | $ | 27.84 | |

| | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (b) | | | 0.12 | | | | 0.06 | | | | 0.22 | | | | 0.29 | | | | 0.22 | | | | 0.39 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 2.48 | | | | 1.10 | | | | (4.46 | ) | | | (1.10 | ) | | | 1.24 | | | | 4.90 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 2.60 | | | | 1.16 | | | | (4.24 | ) | | | (0.81 | ) | | | 1.46 | | | | 5.29 | |

| | | | | | |

Less Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.26 | ) | | | (0.12 | ) | | | (0.33 | ) | | | (0.16 | ) | | | (0.33 | ) | | | (0.78 | ) |

From net realized gains | | | — | | | | — | | | | — | | | | (5.90 | ) | | | (9.48 | ) | | | (3.28 | ) |

From return of capital | | | — | | | | (0.08 | ) | | | (0.17 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.26 | ) | | | (0.20 | ) | | | (0.50 | ) | | | (6.06 | ) | | | (9.81 | ) | | | (4.06 | ) |

| | | | | | |

Increase from regulatory settlements | | | — | (c) | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | |

Net Asset Value, End of Period | | $ | 12.41 | | | $ | 10.07 | | | $ | 9.11 | | | $ | 13.85 | | | $ | 20.72 | | | $ | 29.07 | |

Total return (d) | | | 26.04 | %(i) | | | 12.86 | %(e) | | | (29.89 | )% | | | (5.46 | )% | | | 1.72 | % | | | 21.66 | % |

| | | | | | |

Ratios to Average Net Assets/ Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net expenses before interest expense (f) | | | 1.27 | % | | | 1.39 | %(g) | | | 1.31 | % | | | 1.28 | % | | | 1.21 | % | | | 1.19 | % |

Interest expense | | | — | %(h) | | | — | | | | — | | | | — | %(h) | | | — | %(h) | | | — | %(h) |

Net expenses (f) | | | 1.27 | % | | | 1.39 | %(g) | | | 1.31 | % | | | 1.28 | % | | | 1.21 | % | | | 1.19 | % |

Net investment income (f) | | | 1.04 | % | | | 1.99 | %(g) | | | 2.69 | % | | | 1.93 | % | | | 0.84 | % | | | 1.45 | % |

Portfolio turnover rate | | | 108 | % | | | 32 | %(e) | | | 110 | % | | | 78 | % | | | 67 | % | | | 10 | % |

Net assets, end of period (000s) | | $ | 27,511 | | | $ | 18,245 | | | $ | 17,114 | | | $ | 22,321 | | | $ | 31,069 | | | $ | 44,685 | |

| (a) | The Fund changed its fiscal year end from August 31 to December 31. Per share data and total return reflect activity from September 1, 2009 through December 31, 2009. |

| (b) | Per share data was calculated using the average shares outstanding during the period. |

| (c) | Rounds to less than $0.01 per share. |

| (d) | Total return at net asset value assuming all distributions reinvested and no initial sales charge or contingent deferred sales charge. |

| (f) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (h) | Rounds to less than 0.01%. |

| (i) | Total return includes a reimbursement of a loss experienced by the Fund due to a compliance violation. This reimbursement had an impact of less than 0.01% on total return. |

See Accompanying Notes to Financial Statements.

15

Financial Highlights – Columbia Real Estate Equity Fund

Selected data for a share outstanding throughout each period is as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended

December 31, | | | Period Ended

December 31, | | | Year Ended August 31, | |

| Class B Shares | | 2010 | | | 2009 (a) | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net Asset Value, Beginning of Period | | $ | 10.09 | | | $ | 9.12 | | | $ | 13.85 | | | $ | 20.76 | | | $ | 29.09 | | | $ | 27.85 | |

| | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (b) | | | 0.02 | | | | 0.04 | | | | 0.16 | | | | 0.20 | | | | 0.03 | | | | 0.19 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 2.50 | | | | 1.10 | | | | (4.46 | ) | | | (1.14 | ) | | | 1.24 | | | | 4.90 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 2.52 | | | | 1.14 | | | | (4.30 | ) | | | (0.94 | ) | | | 1.27 | | | | 5.09 | |

| | | | | | |

Less Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.18 | ) | | | (0.09 | ) | | | (0.26 | ) | | | (0.07 | ) | | | (0.12 | ) | | | (0.57 | ) |

From net realized gains | | | — | | | | — | | | | — | | | | (5.90 | ) | | | (9.48 | ) | | | (3.28 | ) |

From return of capital | | | — | | | | (0.08 | ) | | | (0.17 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.18 | ) | | | (0.17 | ) | | | (0.43 | ) | | | (5.97 | ) | | | (9.60 | ) | | | (3.85 | ) |

| | | | | | |

Increase from regulatory settlements | | | — | (c) | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | |

Net Asset Value, End of Period | | $ | 12.43 | | | $ | 10.09 | | | $ | 9.12 | | | $ | 13.85 | | | $ | 20.76 | | | $ | 29.09 | |

Total return (d) | | | 25.07 | %(i) | | | 12.57 | %(e) | | | (30.38 | )% | | | (6.21 | )% | | | 0.99 | % | | | 20.78 | % |

| | | | | | |

Ratios to Average Net Assets/Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net expenses before interest expense (f) | | | 2.02 | % | | | 2.14 | %(g) | | | 2.06 | % | | | 2.03 | % | | | 1.96 | % | | | 1.94 | % |

Interest expense | | | — | %(h) | | | — | | | | — | | | | — | %(h) | | | — | %(h) | | | — | %(h) |

Net expenses (f) | | | 2.02 | % | | | 2.14 | %(g) | | | 2.06 | % | | | 2.03 | % | | | 1.96 | % | | | 1.94 | % |

Net investment income (f) | | | 0.21 | % | | | 1.22 | %(g) | | | 1.96 | % | | | 1.30 | % | | | 0.10 | % | | | 0.72 | % |

Portfolio turnover rate | | | 108 | % | | | 32 | %(e) | | | 110 | % | | | 78 | % | | | 67 | % | | | 10 | % |

Net assets, end of period (000s) | | $ | 2,986 | | | $ | 3,348 | | | $ | 3,356 | | | $ | 7,123 | | | $ | 9,663 | | | $ | 13,309 | |

| (a) | The Fund changed its fiscal year end from August 31 to December 31. Per share data and total return reflect activity from September 1, 2009 through December 31, 2009. |

| (b) | Per share data was calculated using the average shares outstanding during the period. |

| (c) | Rounds to less than $0.01 per share. |

| (d) | Total return at net asset value assuming all distributions reinvested and no contingent deferred sales charge. |

| (f) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (h) | Rounds to less than 0.01%. |

| (i) | Total return includes a reimbursement of a loss experienced by the Fund due to a compliance violation. This reimbursement had an impact of less than 0.01% on total return. |

See Accompanying Notes to Financial Statements.

16

Financial Highlights – Columbia Real Estate Equity Fund

Selected data for a share outstanding throughout each period is as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended

December 31, | | | Period Ended

December 31, | | | Year Ended August 31, | |

| Class C Shares | | 2010 | | | 2009 (a) | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net Asset Value, Beginning of Period | | $ | 10.07 | | | $ | 9.10 | | | $ | 13.82 | | | $ | 20.72 | | | $ | 29.06 | | | $ | 27.83 | |

| | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (b) | | | 0.03 | | | | 0.04 | | | | 0.16 | | | | 0.19 | | | | 0.03 | | | | 0.18 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 2.48 | | | | 1.10 | | | | (4.45 | ) | | | (1.12 | ) | | | 1.23 | | | | 4.90 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 2.51 | | | | 1.14 | | | | (4.29 | ) | | | (0.93 | ) | | | 1.26 | | | | 5.08 | |

| | | | | | |

Less Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.18 | ) | | | (0.09 | ) | | | (0.26 | ) | | | (0.07 | ) | | | (0.12 | ) | | | (0.57 | ) |

From net realized gains | | | — | | | | — | | | | — | | | | (5.90 | ) | | | (9.48 | ) | | | (3.28 | ) |

From return of capital | | | — | | | | (0.08 | ) | | | (0.17 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.18 | ) | | | (0.17 | ) | | | (0.43 | ) | | | (5.97 | ) | | | (9.60 | ) | | | (3.85 | ) |

| | | | | | |

Increase from regulatory settlements | | | — | (c) | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | |

Net Asset Value, End of Period | | $ | 12.40 | | | $ | 10.07 | | | $ | 9.10 | | | $ | 13.82 | | | $ | 20.72 | | | $ | 29.06 | |

Total return (d) | | | 25.02 | %(i) | | | 12.60 | %(e) | | | (30.37 | )% | | | (6.18 | )% | | | 0.94 | % | | | 20.75 | % |

| | | | | | |

Ratios to Average Net Assets/Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net expenses before interest expense (f) | | | 2.02 | % | | | 2.14 | %(g) | | | 2.06 | % | | | 2.03 | % | | | 1.96 | % | | | 1.94 | % |

Interest expense | | | — | %(h) | | | — | | | | — | | | | — | %(h) | | | — | %(h) | | | — | %(h) |

Net expenses (f) | | | 2.02 | % | | | 2.14 | %(g) | | | 2.06 | % | | | 2.03 | % | | | 1.96 | % | | | 1.94 | % |

Net investment income (f) | | | 0.28 | % | | | 1.37 | %(g) | | | 1.95 | % | | | 1.26 | % | | | 0.11 | % | | | 0.66 | % |

Portfolio turnover rate | | | 108 | % | | | 32 | %(e) | | | 110 | % | | | 78 | % | | | 67 | % | | | 10 | % |

Net assets, end of period (000s) | | $ | 6,900 | | | $ | 4,777 | | | $ | 3,553 | | | $ | 6,462 | | | $ | 8,263 | | | $ | 5,486 | |

| (a) | The Fund changed its fiscal year end from August 31 to December 31. Per share data and total return reflect activity from September 1, 2009 through December 31, 2009. |

| (b) | Per share data was calculated using the average shares outstanding during the period. |

| (c) | Rounds to less than $0.01 per share. |

| (d) | Total return at net asset value assuming all distributions reinvested and no contingent deferred sales charge. |

| (f) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (h) | Rounds to less than 0.01%. |

| (i) | Total return includes a reimbursement of a loss experienced by the Fund due to a compliance violation. This reimbursement had an impact of less than 0.01% on total return. |

See Accompanying Notes to Financial Statements.

17

Financial Highlights – Columbia Real Estate Equity Fund

Selected data for a share outstanding throughout the period is as follows:

| | | | |

| | | Period Ended

December 31, | |

| Class I Shares | | 2010 (a) | |

Net Asset Value, Beginning of Period | | $ | 11.77 | |

| |

Income from Investment Operations: | | | | |

Net investment income (b) | | | 0.07 | |

Net realized and unrealized gain on investments and foreign currency | | | 0.70 | |

| | | | |

Total from investment operations | | | 0.77 | |

| |

Less Distributions to Shareholders: | | | | |

From net investment income | | | (0.12 | ) |

| |

Net Asset Value, End of Period | | $ | 12.42 | |

Total return (c)(d)(h) | | | 6.52 | % |

| |

Ratios to Average Net Assets/Supplemental Data: | | | | |

Net expenses before interest expense (e)(f) | | | 0.96 | % |

Interest expense (f)(g) | | | — | % |

Net expenses (e)(f) | | | 0.96 | % |

Net investment income (e)(f) | | | 2.34 | % |

Portfolio turnover rate (d) | | | 108 | % |

Net assets, end of period (000s) | | $ | 35,388 | |

| (a) | Class I shares commenced operations on September 27, 2010. Per share data and total return reflect activity from that date. |

| (b) | Per share data was calculated using the average shares outstanding during the period. |

| (c) | Total return at net asset value assuming all distributions reinvested. |

| (e) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (g) | Rounds to less than 0.01%. |

| (h) | Total return includes a reimbursement of a loss experienced by the Fund due to a compliance violation. This reimbursement had an impact of less than 0.01% on total return. |

See Accompanying Notes to Financial Statements.

18

Financial Highlights – Columbia Real Estate Equity Fund

Selected data for a share outstanding throughout the period is as follows:

| | | | |

| | | Period Ended

December 31, | |

| Class R Shares | | 2010 (a) | |

Net Asset Value, Beginning of Period | | $ | 11.75 | |

| |

Income from Investment Operations: | | | | |

Net investment loss (b) | | | (0.07 | ) |

Net realized and unrealized gain on investments and foreign currency | | | 0.82 | |

| | | | |

Total from investment operations | | | 0.75 | |

| |

Less Distributions to Shareholders: | | | | |

From net investment income | | | (0.10 | ) |

| |

Net Asset Value, End of Period | | $ | 12.40 | |

Total return (c)(d)(h) | | | 6.36 | % |

| |

Ratios to Average Net Assets/Supplemental Data: | | | | |

Net expenses before interest expense (e)(f) | | | 1.76 | % |

Interest expense (f) (g) | | | — | % |

Net expenses (e)(f) | | | 1.76 | % |

Net investment loss (e)(f) | | | (2.20 | )% |

Portfolio turnover rate (d) | | | 108 | % |

Net assets, end of period (000s) | | $ | 3 | |

| (a) | Class R shares commenced operations on September 27, 2010. Per share data and total return reflect activity from that date. |

| (b) | Per share data was calculated using the average shares outstanding during the period. |

| (c) | Total return at net asset value assuming all distributions reinvested. |

| (e) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (g) | Rounds to less than 0.01%. |

| (h) | Total return includes a reimbursement of a loss experienced by the Fund due to a compliance violation. This reimbursement had an impact of less than 0.01% on total return. |

See Accompanying Notes to Financial Statements.

19

Financial Highlights – Columbia Real Estate Equity Fund

Selected data for a share outstanding throughout the period is as follows:

| | | | |

| | | Period Ended

December 31, | |

| Class W Shares | | 2010 (a) | |

Net Asset Value, Beginning of Period | | $ | 11.75 | |

| |

Income from Investment Operations: | | | | |

Net investment loss (b) | | | (0.05 | ) |

Net realized and unrealized gain on investments and foreign currency | | | 0.81 | |

| | | | |

Total from investment operations | | | 0.76 | |

| |

Less Distributions to Shareholders: | | | | |

From net investment income | | | (0.10 | ) |

| |

Net Asset Value, End of Period | | $ | 12.41 | |

Total return (c)(d)(h) | | | 6.51 | % |

| |

Ratios to Average Net Assets/Supplemental Data: | | | | |

Net expenses before interest expense (e)(f) | | | 1.22 | % |

Interest expense (f)(g) | | | — | % |

Net expenses (e)(f) | | | 1.22 | % |

Net investment loss (e)(f) | | | (1.64 | )% |

Portfolio turnover rate (d) | | | 108 | % |

Net assets, end of period (000s) | | $ | 3 | |

| (a) | Class W shares commenced operations on September 27, 2010. Per share data and total return reflect activity from that date. |

| (b) | Per share data was calculated using the average shares outstanding during the period. |

| (c) | Total return at net asset value assuming all distributions reinvested. |

| (e) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (g) | Rounds to less than 0.01%. |

| (h) | Total return includes a reimbursement of a loss experienced by the Fund due to a compliance violation. This reimbursement had an impact of less than 0.01% on total return. |

See Accompanying Notes to Financial Statements.

20

Financial Highlights – Columbia Real Estate Equity Fund

Selected data for a share outstanding throughout each period is as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended

December 31, | | | Period Ended

December 31, | | | Year Ended August 31, | |

| Class Z Shares | | 2010 | | | 2009 (a) | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net Asset Value, Beginning of Period | | $ | 10.09 | | | $ | 9.13 | | | $ | 13.88 | | | $ | 20.74 | | | $ | 29.10 | | | $ | 27.86 | |

| | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (b) | | | 0.14 | | | | 0.07 | | | | 0.24 | | | | 0.33 | | | | 0.29 | | | | 0.48 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 2.49 | | | | 1.10 | | | | (4.47 | ) | | | (1.10 | ) | | | 1.22 | | | | 4.88 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 2.63 | | | | 1.17 | | | | (4.23 | ) | | | (0.77 | ) | | | 1.51 | | | | 5.36 | |

| | | | | | |

Less Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.29 | ) | | | (0.13 | ) | | | (0.35 | ) | | | (0.19 | ) | | | (0.39 | ) | | | (0.84 | ) |

From net realized gains | | | — | | | | — | | | | — | | | | (5.90 | ) | | | (9.48 | ) | | | (3.28 | ) |

From return of capital | | | — | | | | (0.08 | ) | | | (0.17 | ) | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.29 | ) | | | (0.21 | ) | | | (0.52 | ) | | | (6.09 | ) | | | (9.87 | ) | | | (4.12 | ) |

| | | | | | |

Increase from regulatory settlements | | | — | (c) | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | |

Net Asset Value, End of Period | | $ | 12.43 | | | $ | 10.09 | | | $ | 9.13 | | | $ | 13.88 | | | $ | 20.74 | | | $ | 29.10 | |

Total return (d) | | | 26.29 | %(i) | | | 12.97 | %(e) | | | (29.71 | )% | | | (5.21 | )% | | | 1.95 | % | | | 21.99 | % |

| | | | | | |

Ratios to Average Net Assets/ Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net expenses before interest expense (f) | | | 1.02 | % | | | 1.14 | %(g) | | | 1.06 | % | | | 1.03 | % | | | 0.96 | % | | | 0.94 | % |

Interest expense | | | — | %(h) | | | — | | | | — | | | | — | %(h) | | | — | %(h) | | | — | %(h) |

Net expenses (f) | | | 1.02 | % | | | 1.14 | %(g) | | | 1.06 | % | | | 1.03 | % | | | 0.96 | % | | | 0.94 | % |

Net investment income (f) | | | 1.23 | % | | | 2.28 | %(g) | | | 2.96 | % | | | 2.17 | % | | | 1.11 | % | | | 1.78 | % |

Portfolio turnover rate | | | 108 | % | | | 32 | %(e) | | | 110 | % | | | 78 | % | | | 67 | % | | | 10 | % |

Net assets, end of period (000s) | | $ | 304,497 | | | $ | 273,528 | | | $ | 238,485 | | | $ | 282,293 | | | $ | 377,388 | | | $ | 578,899 | |

| (a) | The Fund changed its fiscal year end from August 31 to December 31. Per share data and total return reflect activity from September 1, 2009 through December 31, 2009. |

| (b) | Per share data was calculated using the average shares outstanding during the period. |

| (c) | Rounds to less than $0.01 per share. |

| (d) | Total return at net asset value assuming all distributions reinvested. |

| (f) | The benefits derived from expense reductions had an impact of less than 0.01%. |

| (h) | Rounds to less than 0.01%. |

| (i) | Total return includes a reimbursement of a loss experienced by the Fund due to a compliance violation. This reimbursement had an impact of less than 0.01% on total return. |

See Accompanying Notes to Financial Statements.

21

Notes to Financial Statements – Columbia Real Estate Equity Fund

December 31, 2010

Note 1. Organization

Columbia Real Estate Equity Fund (the Fund), a series of Columbia Funds Series Trust I (the Trust), is a non-diversified fund. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust.

Investment Objective

The Fund seeks capital appreciation and above-average income by investing, under normal market conditions, at least 80% of its net assets (plus any borrowings for investment purposes) in stocks of companies principally engaged in the real estate industry, including real estate investment trusts (REITs).

Fund Shares