UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: | 811-5445 |

| Name of Registrant: | Vanguard Fenway Funds |

| Address of Registrant: | P.O. Box 2600 |

| Valley Forge, PA 19482 | |

| Name and address of agent for service: | Heidi Stam, Esquire |

| P.O. Box 876 | |

| Valley Forge, PA 19482 | |

| Registrant’s telephone number, including area code: | (610) 669-1000 |

| Date of fiscal year end: | September 30 |

| Date of reporting period: | October 1, 2008 – September 30, 2009 |

Item 1: Reports to Shareholders

![]()

| Vanguard Equity Income Fund |

| Annual Report |

| September 30, 2009 |

> Vanguard Equity Income Fund returned about –9%, as a rally in the second

half of the year failed to offset the fund’s steep decline in the first half.

> The fund’s heavy allocation to financials, typically a rich vein of dividend-paying

stocks, was the fund’s—and the market’s—biggest trouble spot.

> The fund’s dividend yield has declined from 2008 levels, in large part because

cash-strapped companies have trimmed dividend payouts.

| Contents | |

| Your Fund’s Total Returns | 1 |

| President’s Letter | 2 |

| Advisors’ Report | 8 |

| Results of Proxy Voting | 11 |

| Fund Profile | 13 |

| Performance Summary | 14 |

| Financial Statements | 16 |

| Your Fund’s After-Tax Returns | 30 |

| About Your Fund’s Expenses | 31 |

| Glossary | 33 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the

risks of investing in your fund are spelled out in the prospectus.

Cover photograph: Veronica Coia.

Your Fund’s Total Returns

| Fiscal Year Ended September 30, 2009 | ||

| Ticker | Total | |

| Symbol | Returns | |

| Vanguard Equity Income Fund | ||

| Investor Shares | VEIPX | –9.12% |

| Admiral™ Shares1 | VEIRX | –9.05 |

| FTSE High Dividend Yield Index | –9.02 | |

| Equity Income Funds Average2 | –6.36 |

| Your Fund’s Performance at a Glance | ||||

| September 30, 2008–September 30, 2009 | ||||

| Distributions Per Share | ||||

| Starting | Ending | Income | Capital | |

| Share Price | Share Price | Dividends | Gains | |

| Vanguard Equity Income Fund | ||||

| Investor Shares | $20.02 | $17.40 | $0.587 | $0.112 |

| Admiral Shares | 41.97 | 36.46 | 1.270 | 0.235 |

1 A lower-cost class of shares available to many longtime shareholders and to those with significant investments in the fund.

2 Derived from data provided by Lipper Inc.

1

President’s Letter

Dear Shareholder,

During the 12 months ended September 30, 2009, Vanguard Equity Income Fund returned about –9%, a disappointing number that incorporates a dramatic six-month decline and a powerful six-month rally. The fund performed in line with its benchmark index, but trailed its equity income fund peers.

At the end of the period, the fund’s Investor Shares had a 30-day SEC yield of 2.80% (Admiral Shares: 2.90%), significantly higher than the stock market’s yield. Both the fund’s and the stock market’s yields have declined over the past year, a reflection of big dividend cuts across corporate America.

After a precipitous fall, stock markets rebound

In recent months, the financial markets have performed so strongly that it’s almost hard to remember that less than a year ago the global financial system stood on the brink of collapse. Since then, markets have pulled back from the abyss. Although unemployment remains near generational highs, and the prospects of a robust recovery seem dim, the global economy has begun to grind into gear.

2

Reminders of the markets’ dark days are nevertheless apparent in the index returns for both the past 12 months and the past three years. Over both periods, U.S. stocks recorded negative returns. Global stocks did better over the past 12 months, recouping their late-2008 losses thanks to general strength in developed economies and a powerful rally in emerging markets. Over the past three years, however, international stocks posted a modestly negative return.

The bond market’s turnabout has been equally dramatic

The stock market’s collapse and recovery echo even more dramatic developments in the bond market. At the end of 2008,

as the credit markets nearly ceased to function, the difference between the yields of corporate bonds and Treasury bonds spiked to levels last seen during the Great Depression.

The Federal Reserve and its central bank counterparts around the world responded with aggressive monetary stimulus efforts, while global governments opened the fiscal taps. Investors first tiptoed, then stampeded, back into the market, boosting bond prices and bringing down yields. Over the past 12 months, taxable U.S. bonds returned more than 10%; municipal securities did even better, returning almost 15%, as measured by the Barclays Capital Municipal Bond Index.

| Market Barometer | |||

| Average Annual Total Returns | |||

| Periods Ended September 30, 2009 | |||

| One Year | Three Years | Five Years | |

| Stocks | |||

| Russell 1000 Index (Large-caps) | –6.14% | –5.10% | 1.49% |

| Russell 2000 Index (Small-caps) | –9.55 | –4.57 | 2.41 |

| Dow Jones U.S. Total Stock Market Index | –5.83 | –4.58 | 1.93 |

| MSCI All Country World Index ex USA (International) | 6.43 | –0.78 | 8.59 |

| Bonds | |||

| Barclays Capital U.S. Aggregate Bond Index | |||

| (Broad taxable market) | 10.56% | 6.41% | 5.13% |

| Barclays Capital Municipal Bond Index | 14.85 | 5.13 | 4.78 |

| Citigroup 3-Month Treasury Bill Index | 0.39 | 2.63 | 2.96 |

| CPI | |||

| Consumer Price Index | –1.29% | 2.10% | 2.61% |

3

The Fed’s rescue campaign has imposed a heavy price on short-term savings vehicles such as money market funds. In December 2008, the Fed reduced its target for the federal funds rate, a benchmark for the interest rates paid by money market instruments and other very short-term securities, to between 0% and 0.25%. The Fed has said it expects to maintain its target at this level “for an extended period.”

As the financial crisis intensified, bank stocks caused pain

Like its benchmark index and mutual fund peers, Vanguard Equity Income Fund typically has a sizable allocation to banks, brokerages, and other financial

stocks. These companies have traditionally been a reliable source of dividend income. During the past 12 months, however, they were one of the bleakest corners of the capital markets.

When these stocks collapsed in late 2008, Vanguard Equity Income Fund had nowhere to hide. Many of these same stocks have since rebounded, but their prices remain well below earlier highs, helping to keep the fund’s 12-month return at about –9%. As global economies contracted, materials and industrial stocks, both sensitive to the rhythms of the business cycle, also put pressure on performance.

| Expense Ratios1 | |||

| Your Fund Compared With Its Peer Group | |||

| Investor | Admiral | Equity Income | |

| Shares | Shares | Funds Average | |

| Equity Income Fund | 0.37% | 0.24% | 1.34% |

1 The fund expense ratios shown are from the prospectus dated January 15, 2009, and represent estimated costs for the current fiscal year

based on the fund’s net assets as of the prospectus date. For the fiscal year ended September 30, 2009, the fund’s expense ratios were

0.36% for Investor Shares and 0.24% for Admiral Shares. The peer-group ratio is derived from data provided by Lipper Inc. and captures

information through year-end 2008.

4

The impact of the financial crisis on stock prices was one disappointment. Its impact on dividends was another. As companies struggled to stabilize their balance sheets, many cut their dividends. At the start of the year, the fund’s Investor Shares had a 30-day SEC yield of 3.79%; a year later, the figure was 2.80%. Standard & Poor’s reported that in the three months ended September 30, 2009, 113 U.S. companies cut their dividends, the highest number since the third quarter of 1982.

Bright spots included stocks in the telecommunications, health care, and technology sectors, which produced positive returns for the full 12 months. Tech stocks began to lead the market higher in March 2009, as companies

that had deferred necessary investment in technologies began to open their wallets. Despite their positive returns, the fund’s tech stocks failed to keep pace with the broader sector’s rally.

Talented management and low costs have kept fund ahead of the pack

Although the fund’s 12-month returns were notably weaker than the average return of its peer group, it’s unwise to make too much of one-year results. As long as the fund’s advisors, Wellington Management Company and Vanguard Quantitative Equity Group, continue to execute the same strategy that, in our judgment, will produce long-term success, we place much more weight on the long-term returns.

| Total Returns | |

| Ten Years Ended September 30, 2009 | |

| Average | |

| Annual Return | |

| Equity Income Fund Investor Shares | 3.03% |

| Spliced Equity Income Index1 | 3.28 |

| Equity Income Funds Average2 | 2.13 |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance

may be lower or higher than the performance data cited. For performance data current to the most recent month-

end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal

value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

1 Russell 1000 Value Index through July 31, 2007; FTSE High Dividend Yield Index thereafter.

2 Derived from data provided by Lipper Inc.

5

A long-term perspective gives investors a sense of how the fund has performed through a variety of market environments. During the past 10 years—an environment that was much tougher than a typical decade-long stretch—the Investor Shares of Vanguard Equity Income Fund returned 3.03%, 0.9 percentage point more than the peer-group average. In addition to the skills of its advisors, that margin highlights the value of low costs. Vanguard Equity Income’s cost advantage might give it a head start of 0.8 to 1.2 percentage points on some of its peer funds.

Although the fund finished a few steps behind its benchmark index over the past decade, it’s worth noting that until July 2007, the fund’s benchmark was inconsistent with its equity income mandate. The Russell 1000 Value Index includes a number of stocks that pay no dividends.

A word on expenses

The fund’s expense ratio has risen over the past fiscal year. The explanation is threefold.

| Investment insight | |||

| The conflict between cost and yield | |||

| When a stock in your fund’s portfolio pays a dividend, that money has two places | |||

| to go: to your account or to the fund company’s ledger. | |||

| During the 12 months ended September 30, 2009, equity income funds had an | |||

| average distributed yield—the past year’s income distributions divided by their | |||

| September 30 NAV—of 2.54%, according to data from Lipper Inc. Over the same | |||

| period, Vanguard Equity Income Fund’s distributed yield was 3.37%. | |||

| You can chalk up much of the difference to costs. In the table below, we add the | |||

| expense ratio to the 12-month distributed yield for both Vanguard Equity Income | |||

| Fund and the peer-group average. The resulting “gross yields”—the dividend yields | |||

| before expenses—are similar. | |||

| After costs, however, the much less expensive Vanguard Equity Income Fund provided | |||

| its shareholders with a much more generous yield than the typical fund. | |||

| Estimated | 12-month | ||

| gross yield | Expense ratio | distribution yield | |

| Vanguard Equity Income Fund Investor Shares | 3.73% | 0.36% | 3.37% |

| Equity Income Funds Average | 3.88 | 1.34 | 2.54 |

| Source: Derived from data provided by Lipper Inc. | |||

6

First, as the value of fund assets has declined, the fund’s fixed expenses have accounted for a modestly higher percentage of fund assets. Second, the Vanguard funds’ contracts with external advisors typically include breakpoint pricing. As assets rise above a breakpoint threshold, advisory fees are paid at a lower rate. When assets fall, as they have during fiscal 2009, a smaller portion of assets is subject to the lower rate, causing the overall rate to increase.

Finally, Vanguard’s contracts with external advisors generally include an incentive-fee provision that is contingent on the advisors’ performance relative to their benchmarks. This fee structure helps to ensure that the interests of the fund shareholders and advisors remain aligned. Over the past year, the advisory fee increased as the fund’s relative performance improved. The fund’s financial statements include more information about Vanguard Equity Income Fund’s incentive fee.

Important lessons from an unsettled period

The past year’s market tumult has provided a powerful, if not entirely welcome, lesson in the critical importance of balance, diversification, and a commitment to a long-term plan. When

the stock market tumbled in late 2008 and early 2009, the diversification benefits of a bond allocation became crystal clear. During the past six months, the stock market’s powerful rally has underscored the benefit of sticking with your long-term equity allocation through the inevitable moments of anxiety and doubt.

Where do we go from here? Although it seems as if the worst is behind us, the financial markets’ short-term direction is impossible to forecast with accuracy. The best response to this uncertainty is, again, a plan based on reasonable long-term return and risk expectations that you can stick with through periods of market turmoil. For income-oriented investors, Vanguard Equity Income Fund can play an important role in such a plan.

Thank you for entrusting your assets to Vanguard.

Sincerely,

F. William McNabb III

President and Chief Executive Officer

October 15, 2009

7

Advisors’ Report

For the fiscal year ended September 30, the Equity Income Fund returned about –9%, reflecting the combined results of your fund’s two independent investment advisors. The use of two advisors provides exposure to distinct, yet complementary, investment approaches, enhancing the diversification of your fund. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the percentage of the fund’s assets each manages, and a brief description of their investment strategies are presented in the table below. The advisors have also prepared a discussion of the investment environment that existed during the fiscal year and of how their portfolio positioning reflects this assessment. These comments were prepared on October 21, 2009.

Wellington Management Company, LLP

Portfolio Manager:

W. Michael Reckmeyer, III, CFA,

Senior Vice President

The economy appears to be rebounding from one of the worst economic downturns in recent history in response to massive government fiscal and monetary stimulus programs. The result has been a significantly improved corporate bond market and surging stock markets. This directly benefits consumers’ wealth and confidence, but importantly allows companies to recapitalize their balance sheets.

The key consideration going forward is the magnitude and sustainability of the recovery. Several headwinds remain, which leads us to conclude that economic growth will be moderate. The unwinding of federal stimulus programs, high debt

| Vanguard Equity Income Fund Investment Advisors | |||

| Fund Assets Managed | |||

| Investment Advisor | % | $ Million | Investment Strategy |

| Wellington Management | 61 | 2,347 | A fundamental approach to seeking desirable stocks. |

| Company, LLP | Our selections typically offer above-average dividend | ||

| yields, below-average valuations, and the potential | |||

| for dividend increases in the future. | |||

| Vanguard Quantitative | 36 | 1,418 | Employs a quantitative fundamental management |

| Equity Group | approach, using models that assess valuation, growth | ||

| prospects, management decisions, market sentiment, | |||

| and earnings quality of companies as compared with | |||

| their peers. | |||

| Cash Investments | 3 | 134 | These short-term reserves are invested by Vanguard |

| in equity index products to simulate investment in | |||

| stocks. Each advisor also may maintain a modest | |||

| cash position. | |||

8

levels and unemployment, a lack of wage gains, and the possibility of higher taxes all may curtail consumer spending.

Globally, economic growth appears to be on the mend. China’s economic growth remains strong, driven largely by aggressive fiscal stimulus programs. Europe also appears to be passing an important inflection point, suggesting that better economic activity is ahead.

Over the past 12 months, we repositioned the portfolio to be more cyclical by adding to our holdings in the industrials, consumer discretionary, and technology sectors.

We also increased our exposure to the health care sector as valuations became more attractive. We reduced holdings in utilities and telecommunication services. In keeping with our philosophy, changes to the portfolio’s positioning were largely done on a bottom-up basis. During this economic crisis, company valuations in the more defensive sectors became stretched, creating opportunities to sell out of these companies and reinvest into ones with more attractive valuations.

We continue to focus on higher-quality companies with a dividend orientation. While dividend reductions have been more pronounced during this downturn, we continue to believe in the importance of dividends to the portfolio’s total return, and as economic growth improves we should see an increase in dividend payments.

Our largest purchases over the 12 months included pharmaceutical companies Johnson & Johnson and Merck, financial company Wells Fargo, and energy company Occidental Petroleum. Our sales included firms that reached or approached our target prices, such as Consolidated Edison, as well as firms with fundamental disappointments, such as Abbott Laboratories, U.S. Bancorp, and Verizon Communications.

Vanguard Quantitative Equity Group

Portfolio Manager:

James P. Stetler, Principal

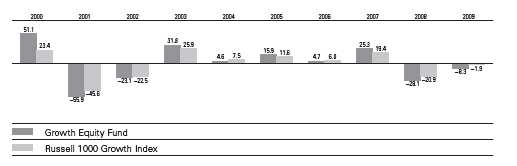

The fiscal year has been a roller-coaster ride for the Equity Income Fund and the equity markets in general. The credit crisis that began in 2007 accelerated with the failure of Lehman Brothers late in 2008. Equity markets plunged for the first six months of the fund’s fiscal year by more than 31% as measured by the Russell 3000 Index. Value stocks fared worse than their growth counterparts, returning –35.6% vs. –26.6% for growth-oriented companies.

As government rescue and stimulus plans were announced and it became apparent that the financial markets were not going to implode, the second half of the fiscal year witnessed a dramatic snapback. The Russell 3000 reversed course and climbed back more than 35%, leaving the total return of the U.S. equity market for the

9

12-month period at about –6%. Growth stocks, as they did last year, outperformed value stocks by a margin of more than 8 percentage points.

Although the worst recession in decades has not been declared officially over, many investment professionals are indicating that it may have come to an end during the third quarter of this year. [On October 29, the Commerce Department announced that the economy had grown by 3.5% in the three months through September.] However, the challenges that lie ahead are many and are not easily resolved. Rising unemployment, the state of credit markets, and massive government deficits are just a few of the issues that need to be addressed in order for long-term economic growth to be restored.

In reviewing the performance of our portfolio for the year, it is clear that our investment process struggled. We have five components in our company evaluation process: valuation, quality, growth, management decisions, and market sentiment. Valuation measures the price we will pay for a stock’s earnings or cash flow. Our quality score separates cheap stocks that deserve their low valuation because of poor margins from their more profitable peers. Our growth

indicator differentiates between companies with low valuations resulting from poor growth prospects and firms with more attractive prospects. Since actions often speak louder than words, another component evaluates the decisions corporate managers make to enhance shareholder value. Finally, our market sentiment score measures the market’s overall evaluation of the company’s value.

Our company ranking process was ineffective during this period because the market did not reward the metrics we deem important to superior performance: low valuation, balance sheet quality, attractive growth prospects, and positive market sentiment. Some are calling the market recovery a “junk rally” as those companies with poor prospects that had fallen the most during the onset of the crisis rallied the most during the market snapback.

Our stock selection was strongest in the telecommunications sector, led by CenturyTel. Our selections were most disappointing in the financial, consumer discretionary, and industrial sectors as companies such as Wells Fargo, ArvinMeritor, and Caterpillar did not perform as expected.

10

Results of Proxy Voting

At a special meeting of shareholders on July 2, 2009, fund shareholders approved the following two proposals:

Proposal 1—Elect trustees for each fund.*

The individuals listed in the table below were elected as trustees for each fund. All trustees with the exception of Messrs. McNabb and Volanakis (both of whom already served as directors of The Vanguard Group, Inc.) served as trustees to the funds prior to the shareholder meeting.

| Percentage | |||

| Trustee | For | Withheld | For |

| John J. Brennan | 381,461,550 | 10,736,721 | 97.3% |

| Charles D. Ellis | 375,348,055 | 16,850,216 | 95.7% |

| Emerson U. Fullwood | 377,280,677 | 14,917,594 | 96.2% |

| Rajiv L. Gupta | 381,215,106 | 10,983,165 | 97.2% |

| Amy Gutmann | 381,699,062 | 10,499,209 | 97.3% |

| JoAnn Heffernan Heisen | 381,602,478 | 10,595,793 | 97.3% |

| F. William McNabb III | 381,115,414 | 11,082,857 | 97.2% |

| André F. Perold | 377,090,732 | 15,107,539 | 96.1% |

| Alfred M. Rankin, Jr. | 381,547,990 | 10,650,281 | 97.3% |

| Peter F. Volanakis | 381,683,908 | 10,514,362 | 97.3% |

| * Results are for all funds within the same trust. |

Proposal 2—Update and standardize the funds’ fundamental policies regarding:

(a) Purchasing and selling real estate.

(b) Issuing senior securities.

(c) Borrowing money.

(d) Making loans.

(e) Purchasing and selling commodities.

(f) Concentrating investments in a particular industry or group of industries.

(g) Eliminating outdated fundamental investment policies not required by law.

The revised fundamental policies are clearly stated and simple, yet comprehensive, making oversight and compliance more efficient than under the former policies. The revised fundamental policies will allow the funds to respond more quickly to regulatory and market changes, while avoiding the costs and delays associated with successive shareholder meetings.

| Broker | Percentage | ||||

| Equity Income Fund | For | Abstain | Against | Non-Votes | For |

| 2a | 104,254,548 | 3,415,494 | 4,614,017 | 11,093,723 | 84.5% |

| 2b | 103,827,681 | 3,790,086 | 4,666,291 | 11,093,724 | 84.2% |

| 2c | 102,305,178 | 3,627,679 | 6,351,203 | 11,093,723 | 82.9% |

| 2d | 102,657,448 | 3,700,020 | 5,926,592 | 11,093,723 | 83.2% |

| 2e | 97,392,950 | 3,619,045 | 11,272,065 | 11,093,723 | 78.9% |

| 2f | 103,405,799 | 3,750,918 | 5,127,343 | 11,093,723 | 83.8% |

| 2g | 104,774,445 | 3,602,106 | 3,907,506 | 11,093,725 | 84.9% |

11

Fund shareholders did not approve this proposal:

Proposal 3—Institute procedures to prevent holding investments in companies that, in the judgment of the board, substantially contribute to genocide or crimes against humanity, the most egregious violations of human rights.

The trustees recommended a vote against the proposal because it called for procedures that duplicate existing practices and procedures of the Vanguard funds.

| Broker | Percentage | ||||

| Vanguard Fund | For | Abstain | Against | Non-Votes | For |

| Equity Income Fund | 16,478,591 | 5,163,754 | 90,641,702 | 11,093,736 | 13.4% |

12

Equity Income Fund

Fund Profile

As of September 30, 2009

| Portfolio Characteristics | |||

| Comparative | Broad | ||

| Fund | Index1 | Index2 | |

| Number of Stocks | 163 | 485 | 4,324 |

| Median Market Cap | $55.1B | $44.6B | $29.0B |

| Price/Earnings Ratio | 17.3x | 23.6x | 27.9x |

| Price/Book Ratio | 2.0x | 1.8x | 2.1x |

| Yield3 | 3.2% | 1.9% | |

| Investor Shares | 2.8% | ||

| Admiral Shares | 2.9% | ||

| Return on Equity | 19.9% | 18.0% | 19.1% |

| Earnings Growth Rate | 2.2% | –1.3% | 9.6% |

| Foreign Holdings | 3.9% | 0.0% | 0.0% |

| Turnover Rate | 51% | — | — |

| Expense Ratio4 | — | — | |

| Investor Shares | 0.37% | ||

| Admiral Shares | 0.24% | ||

| Short-Term Reserves | 0.4% | — | — |

| Sector Diversification (% of equity exposure) | |||

| Comparative | Broad | ||

| Fund | Index1 | Index2 | |

| Consumer Discretionary | 8.8% | 7.6% | 10.1% |

| Consumer Staples | 10.9 | 10.7 | 9.9 |

| Energy | 9.5 | 6.7 | 11.0 |

| Financials | 22.1 | 23.9 | 16.7 |

| Health Care | 11.1 | 11.8 | 12.9 |

| Industrials | 14.9 | 14.1 | 10.6 |

| Information Technology | 6.5 | 5.0 | 18.2 |

| Materials | 4.2 | 5.0 | 3.9 |

| Telecommunication | |||

| Services | 4.6 | 6.5 | 2.9 |

| Utilities | 7.4 | 8.7 | 3.8 |

| Volatility Measures5 | ||

| Fund Versus | Fund Versus | |

| Spliced Index6 | Broad Index2 | |

| R-Squared | 0.99 | 0.91 |

| Beta | 0.90 | 0.88 |

| Ten Largest Holdings7 (% of total net assets) | ||

| JPMorgan Chase & Co. | diversified financial services | 4.5% |

| Wells Fargo & Co. | diversified banks | 3.5 |

| Johnson & Johnson | pharmaceuticals | 3.4 |

| Chevron Corp. | integrated oil & gas | 3.3 |

| AT&T Inc. | integrated telecommunication services | 3.0 |

| Pfizer Inc. | pharmaceuticals | 3.0 |

| General Electric Co. | industrial conglomerates | 2.8 |

| Merck & Co. Inc. | pharmaceuticals | 2.3 |

| Intel Corp. | semiconductors | 2.3 |

| Philip Morris International Inc. | tobacco | 2.1 |

| Top Ten | 30.2% | |

Investment Focus

1 FTSE High Dividend Yield

2 Dow Jones U.S. Total Stock Market Index.

3 30-day SEC yield for the fund; annualized dividend yield for the indexes. See the Glossary.

4 The expense ratios shown are from the prospectus dated January 15, 2009, and represent estimated costs for the current fiscal year based

on the fund’s net assets as of the prospectus date. For the fiscal year ended September 30, 2009, the expense ratios were 0.36% for

Investor Shares and 0.24% for Admiral Shares.

5 For an explanation of R-squared, beta, and other terms used here, see the Glossary.

6 Russell 1000 Value Index through July 31, 2007; FTSE High Dividend Yield Index thereafter.

7 The holdings listed exclude any temporary cash investments and equity index products.

13

Equity Income Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

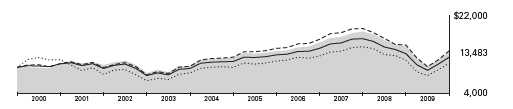

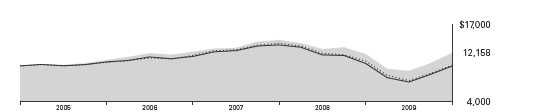

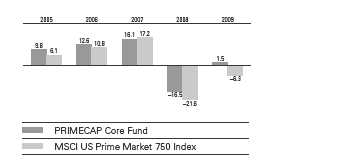

Cumulative Performance: September 30, 1999–September 30, 2009

Initial Investment of $10,000

| Average Annual Total Returns | Final Value | |||

| Periods Ended September 30, 2009 | of a $10,000 | |||

| One Year | Five Years | Ten Years | Investment | |

| Equity Income Fund Investor Shares1 | –9.12% | 1.93% | 3.03% | $13,483 |

| Dow Jones U.S. Total Stock Market Index | –5.83 | 1.93 | 0.94 | 10,978 |

| Spliced Equity Income Index2 | –9.02 | 2.25 | 3.28 | 13,805 |

| Equity Income Funds Average3 | –6.36 | 1.69 | 2.13 | 12,347 |

| Final Value | ||||

| Since | of a $100,000 | |||

| One Year | Five Years | Inception4 | Investment | |

| Equity Income Fund Admiral Shares | –9.05% | 2.06% | 2.36% | $120,911 |

| Dow Jones U.S. Total Stock Market Index | –5.83 | 1.93 | 1.66 | 114,303 |

| Spliced Equity Income Index2 | –9.02 | 2.25 | 2.80 | 125,200 |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

2 Russell 1000 Value Index through July 31, 2007; FTSE High Dividend Yield Index thereafter.

3 Derived from data provided by Lipper Inc.

4 Performance for the fund’s Admiral Shares and its comparative standards is calculated since the inception of the share class:

August 13, 2001.

14

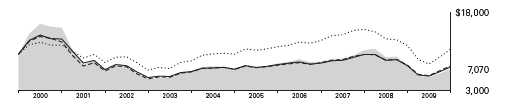

Equity Income Fund

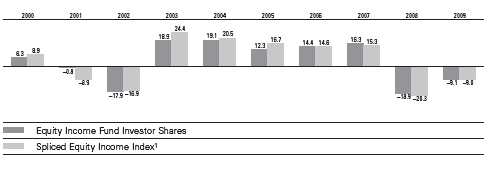

Fiscal-Year Total Returns (%): September 30, 1999–September 30, 2009

1 Russell 1000 Value Index through July 31, 2007; FTSE High Dividend Yield Index thereafter.

Note: See Financial Highlights tables for dividend and capital gains information.

15

Equity Income Fund

Financial Statements

Statement of Net Assets

As of September 30, 2009

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at www.sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| Market | ||

| Value• | ||

| Shares | ($000) | |

| Common Stocks (97.4%)1 | ||

| Consumer Discretionary (8.5%) | ||

| Home Depot Inc. | 3,062,200 | 81,577 |

| McDonald’s Corp. | 1,111,005 | 63,405 |

| Genuine Parts Co. | 1,145,400 | 43,594 |

| Sherwin-Williams Co. | 614,900 | 36,992 |

| VF Corp. | 200,000 | 14,486 |

| Mattel Inc. | 751,200 | 13,867 |

| Whirlpool Corp. | 141,600 | 9,906 |

| Fortune Brands Inc. | 214,500 | 9,219 |

| McGraw-Hill Cos. Inc. | 335,600 | 8,437 |

| Gannett Co. Inc. | 656,028 | 8,207 |

| DR Horton Inc. | 700,400 | 7,992 |

| Hasbro Inc. | 194,800 | 5,406 |

| Limited Brands Inc. | 309,800 | 5,264 |

| Tupperware Brands Corp. | 125,800 | 5,022 |

| H&R Block Inc. | 253,100 | 4,652 |

| Cooper Tire & Rubber Co. | 253,074 | 4,449 |

| Darden Restaurants Inc. | 125,000 | 4,266 |

| Cracker Barrel Old Country | ||

| Store Inc. | 54,700 | 1,882 |

| Brinker International Inc. | 92,500 | 1,455 |

| Lennar Corp. Class A | 17,000 | 242 |

| Newell Rubbermaid Inc. | 13,200 | 207 |

| 330,527 | ||

| Consumer Staples (10.5%) | ||

| Philip Morris | ||

| International Inc. | 1,718,655 | 83,767 |

| Nestle SA ADR | 1,419,500 | 60,506 |

| Kimberly-Clark Corp. | 752,575 | 44,387 |

| Altria Group Inc. | 2,019,155 | 35,961 |

| Coca-Cola Co. | 644,582 | 34,614 |

| Sysco Corp. | 1,229,688 | 30,558 |

| PepsiCo Inc. | 497,500 | 29,183 |

| General Mills Inc. | 373,100 | 24,020 |

| Kraft Foods Inc. | 753,389 | 19,792 |

| Lorillard Inc. | 170,000 | 12,631 |

| ConAgra Foods Inc. | 465,700 | 10,096 |

| Clorox Co. | 157,800 | 9,282 |

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| Hershey Co. | 198,500 | 7,714 | |

| Sara Lee Corp. | 520,400 | 5,797 | |

| Kellogg Co. | 8,400 | 414 | |

| 408,722 | |||

| Energy (9.0%) | |||

| Chevron Corp. | 1,805,300 | 127,147 | |

| BP PLC ADR | 1,065,000 | 56,690 | |

| ConocoPhillips | 1,175,300 | 53,077 | |

| Occidental Petroleum Corp. | 594,100 | 46,578 | |

| Total SA ADR | 599,700 | 35,538 | |

| Marathon Oil Corp. | 820,600 | 26,177 | |

| Southern Union Co. | 187,500 | 3,898 | |

| Spectra Energy Corp. | 67,700 | 1,282 | |

| 350,387 | |||

| Exchange-Traded Fund (1.1%) | |||

| ^,2 | Vanguard Value ETF | 963,400 | 44,393 |

| Financials (21.6%) | |||

| JPMorgan Chase & Co. | 3,979,300 | 174,373 | |

| Wells Fargo & Co. | 4,874,173 | 137,354 | |

| Bank of America Corp. | 4,007,328 | 67,804 | |

| Goldman Sachs Group Inc. | 267,100 | 49,240 | |

| ACE Ltd. | 805,000 | 43,035 | |

| PNC Financial Services | |||

| Group Inc. | 818,382 | 39,765 | |

| Bank of New York | |||

| Mellon Corp. | 1,361,870 | 39,481 | |

| Chubb Corp. | 691,462 | 34,857 | |

| Toronto-Dominion Bank | 474,900 | 30,607 | |

| Unum Group | 1,210,900 | 25,962 | |

| Aflac Inc. | 554,200 | 23,687 | |

| US Bancorp | 985,736 | 21,548 | |

| Allstate Corp. | 692,300 | 21,198 | |

| Travelers Cos. Inc. | 357,900 | 17,619 | |

| BB&T Corp. | 464,800 | 12,661 | |

| Hudson City Bancorp Inc. | 672,600 | 8,845 | |

| Axis Capital Holdings Ltd. | 283,400 | 8,553 | |

| T Rowe Price Group Inc. | 179,400 | 8,199 | |

16

| Equity Income Fund | ||

| Market | ||

| Value• | ||

| Shares | ($000) | |

| Endurance Specialty | ||

| Holdings Ltd. | 223,700 | 8,158 |

| American Express Co. | 231,800 | 7,858 |

| Federated Investors Inc. | ||

| Class B | 289,157 | 7,625 |

| New York Community | ||

| Bancorp Inc. | 633,400 | 7,233 |

| NYSE Euronext | 231,100 | 6,676 |

| Waddell & | ||

| Reed Financial Inc. | 222,500 | 6,330 |

| Bank of Hawaii Corp. | 145,300 | 6,036 |

| Protective Life Corp. | 238,400 | 5,107 |

| Ameriprise Financial Inc. | 138,002 | 5,014 |

| NBT Bancorp Inc. | 156,258 | 3,522 |

| Morgan Stanley | 100,000 | 3,088 |

| MetLife Inc. | 80,200 | 3,053 |

| Oriental Financial | ||

| Group Inc. | 113,100 | 1,436 |

| GAMCO Investors Inc. | 30,600 | 1,398 |

| GFI Group Inc. | 148,553 | 1,074 |

| Advance America Cash | ||

| Advance Centers Inc. | 137,141 | 768 |

| First American Corp. | 15,000 | 486 |

| United Bankshares Inc. | 15,900 | 312 |

| 839,962 | ||

| Health Care (10.6%) | ||

| Johnson & Johnson | 2,200,305 | 133,977 |

| Pfizer Inc. | 7,068,731 | 116,987 |

| Merck & Co. Inc. | 2,879,214 | 91,070 |

| Bristol-Myers Squibb Co. | 989,732 | 22,289 |

| Wyeth | 350,900 | 17,047 |

| Eli Lilly & Co. | 513,149 | 16,949 |

| GlaxoSmithKline PLC ADR | 413,400 | 16,333 |

| 414,652 | ||

| Industrials (14.5%) | ||

| General Electric Co. | 6,622,572 | 108,743 |

| 3M Co. | 946,400 | 69,844 |

| Waste Management Inc. | 1,520,700 | 45,347 |

| Eaton Corp. | 611,500 | 34,605 |

| Stanley Works | 804,600 | 34,348 |

| Republic Services Inc. | ||

| Class A | 1,222,700 | 32,487 |

| Illinois Tool Works Inc. | 716,800 | 30,615 |

| Caterpillar Inc. | 567,100 | 29,109 |

| PACCAR Inc. | 732,000 | 27,604 |

| Ingersoll-Rand PLC | 834,600 | 25,597 |

| United Parcel Service Inc. | ||

| Class B | 359,200 | 20,284 |

| Honeywell International Inc. | 456,162 | 16,946 |

| Tyco International Ltd. | 380,700 | 13,127 |

| Northrop Grumman Corp. | 244,413 | 12,648 |

| Schneider Electric SA | 108,584 | 11,048 |

| Dover Corp. | 273,300 | 10,593 |

| Briggs & Stratton Corp. | 418,200 | 8,117 |

| Pitney Bowes Inc. | 320,900 | 7,974 |

| Market | ||

| Value• | ||

| Shares | ($000) | |

| Boeing Co. | 117,400 | 6,357 |

| Hubbell Inc. Class B | 107,800 | 4,528 |

| Apogee Enterprises Inc. | 265,675 | 3,991 |

| Raytheon Co. | 80,400 | 3,857 |

| Emerson Electric Co. | 70,500 | 2,826 |

| Federal Signal Corp. | 185,715 | 1,335 |

| Deluxe Corp. | 56,500 | 966 |

| Deere & Co. | 9,900 | 425 |

| 563,321 | ||

| Information Technology (6.0%) | ||

| Intel Corp. | 4,547,500 | 88,995 |

| Microsoft Corp. | 2,771,100 | 71,744 |

| Texas Instruments Inc. | 1,067,700 | 25,294 |

| Automatic Data | ||

| Processing Inc. | 342,000 | 13,441 |

| Analog Devices Inc. | 359,300 | 9,909 |

| Diebold Inc. | 243,500 | 8,018 |

| Maxim Integrated | ||

| Products Inc. | 437,800 | 7,942 |

| Xilinx Inc. | 257,400 | 6,028 |

| Linear Technology Corp. | 131,700 | 3,639 |

| 235,010 | ||

| Materials (4.0%) | ||

| EI Du Pont de | ||

| Nemours & Co. | 1,204,127 | 38,701 |

| Packaging Corp. | ||

| of America | 1,297,800 | 26,475 |

| Air Products & | ||

| Chemicals Inc. | 294,100 | 22,816 |

| PPG Industries Inc. | 384,100 | 22,358 |

| Eastman Chemical Co. | 144,000 | 7,710 |

| Bemis Co. Inc. | 258,900 | 6,708 |

| Glatfelter | 543,500 | 6,239 |

| Temple-Inland Inc. | 352,200 | 5,783 |

| Stepan Co. | 74,000 | 4,446 |

| Compass Minerals | ||

| International Inc. | 71,500 | 4,406 |

| Sonoco Products Co. | 138,800 | 3,823 |

| Sensient | ||

| Technologies Corp. | 103,127 | 2,864 |

| Dow Chemical Co. | 70,200 | 1,830 |

| Lubrizol Corp. | 24,100 | 1,722 |

| Worthington Industries Inc. | 68,700 | 955 |

| Innophos Holdings Inc. | 32,818 | 607 |

| 157,443 | ||

| Telecommunication Services (4.4%) | ||

| AT&T Inc. | 4,346,005 | 117,386 |

| Verizon | ||

| Communications Inc. | 1,479,628 | 44,788 |

| CenturyTel Inc. | 189,546 | 6,369 |

| Qwest Communications | ||

| International Inc. | 913,200 | 3,479 |

| Windstream Corp. | 30,100 | 305 |

| 172,327 | ||

17

Equity Income Fund

| Market | ||

| Value• | ||

| Shares | ($000) | |

| Utilities (7.2%) | ||

| FPL Group Inc. | 997,766 | 55,106 |

| Dominion | ||

| Resources Inc. | 1,501,030 | 51,785 |

| Exelon Corp. | 571,600 | 28,363 |

| American Electric | ||

| Power Co. Inc. | 749,700 | 23,233 |

| Northeast Utilities | 836,000 | 19,847 |

| Entergy Corp. | 215,800 | 17,234 |

| Edison International | 512,000 | 17,193 |

| Public Service Enterprise | ||

| Group Inc. | 396,520 | 12,466 |

| FirstEnergy Corp. | 254,200 | 11,622 |

| NiSource Inc. | 665,300 | 9,241 |

| Atmos Energy Corp. | 261,910 | 7,381 |

| UGI Corp. | 287,300 | 7,200 |

| National Fuel Gas Co. | 109,000 | 4,993 |

| Avista Corp. | 232,684 | 4,705 |

| AGL Resources Inc. | 70,000 | 2,469 |

| PG&E Corp. | 51,700 | 2,093 |

| PNM Resources Inc. | 179,000 | 2,091 |

| Sempra Energy | 26,600 | 1,325 |

| Southern Co. | 39,300 | 1,245 |

| DPL Inc. | 42,400 | 1,107 |

| 280,699 | ||

| Total Common Stocks | ||

| (Cost $3,643,182) | 3,797,443 |

| Market | ||

| Value• | ||

| Shares | ($000) | |

| Temporary Cash Investments (2.8%)1 | ||

| Money Market Fund (2.1%) | ||

| 3,4 Vanguard Market Liquidity | ||

| Fund, 0.267% | 82,196,256 | 82,196 |

| Face | ||

| Amount | ||

| ($000) | ||

| Repurchase Agreement (0.4%) | ||

| Goldman Sachs & Co. | ||

| 0.050%, 10/1/09 | ||

| (Dated 9/30/09, | ||

| Repurchase Value | ||

| $13,000,000, | ||

| collateralized by | ||

| Federal National | ||

| Mortgage Assn. | ||

| 5.500%, 1/1/39) | 13,000 | 13,000 |

| U.S. Government and Agency Obligations (0.3%) | ||

| 5,6 Federal Home Loan | ||

| Bank Discount Notes, | ||

| 0.220%, 3/26/10 | 12,000 | 11,989 |

| Total Temporary Cash Investments | ||

| (Cost $107,183) | 107,185 | |

| Total Investments (100.2%) | ||

| (Cost $3,750,365) | 3,904,628 | |

| Other Assets and Liabilities (–0.2%) | ||

| Other Assets | 14,834 | |

| Liabilities4 | (20,893) | |

| (6,059) | ||

| Net Assets (100%) | 3,898,569 | |

18

Equity Income Fund

| At September 30, 2009, net assets consisted of: | |

| Amount | |

| ($000) | |

| Paid-in Capital | 4,535,134 |

| Overdistributed Net Investment Income | (4,554) |

| Accumulated Net Realized Losses | (787,546) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 154,263 |

| Futures Contracts | 1,272 |

| Net Assets | 3,898,569 |

| Investor Shares—Net Assets | |

| Applicable to 139,294,573 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 2,423,298 |

| Net Asset Value Per Share— | |

| Investor Shares | $17.40 |

| Admiral Shares—Net Assets | |

| Applicable to 40,459,726 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 1,475,271 |

| Net Asset Value Per Share— | |

| Admiral Shares | $36.46 |

• See Note A in Notes to Financial Statements.

^ Part of security position is on loan to broker-dealers. The total value of securities on loan is $318,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures

investments, the fund’s effective common stock and temporary cash investment positions represent 99.7% and 0.5%, respectively, of

net assets.

2 Considered an affiliated company of the fund as the issuer is another member of The Vanguard Group.

3 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the

7-day yield.

4 Includes $331,000 of collateral received for securities on loan.

5 Securities with a value of $11,989,000 have been segregated as initial margin for open futures contracts.

6 The issuer operates under a congressional charter; its securities are not backed by the full faith and credit of the U.S. government.

ADR—American Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

19

Equity Income Fund

Statement of Operations

| Year Ended | |

| September 30, 2009 | |

| ($000) | |

| Investment Income | |

| Income | |

| Dividends1,2 | 139,692 |

| Interest2 | 794 |

| Security Lending | 369 |

| Total Income | 140,855 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 2,705 |

| Performance Adjustment | 535 |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 4,679 |

| Management and Administrative—Admiral Shares | 1,510 |

| Marketing and Distribution—Investor Shares | 610 |

| Marketing and Distribution—Admiral Shares | 344 |

| Custodian Fees | 55 |

| Auditing Fees | 26 |

| Shareholders’ Reports and Proxies—Investor Shares | 241 |

| Shareholders’ Reports and Proxies—Admiral Shares | 20 |

| Trustees’ Fees and Expenses | 7 |

| Total Expenses | 10,732 |

| Expenses Paid Indirectly | (128) |

| Net Expenses | 10,604 |

| Net Investment Income | 130,251 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold2 | (734,390) |

| Futures Contracts | (36,043) |

| Foreign Currencies | (11) |

| Realized Net Gain (Loss) | (770,444) |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 218,786 |

| Futures Contracts | 4,664 |

| Foreign Currencies | 23 |

| Change in Unrealized Appreciation (Depreciation) | 223,473 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (416,720) |

1 Dividends are net of foreign withholding taxes of $918,000.

2 Dividend income, interest income, and realized net gain (loss) from affiliated companies of the fund were $1,327,000, $628,000, and $0,

respectively.

See accompanying Notes, which are an integral part of the Financial Statements.

20

Equity Income Fund

Statement of Changes in Net Assets

| Year Ended September 30, | ||

| 2009 | 2008 | |

| ($000) | ($000) | |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net Investment Income | 130,251 | 167,213 |

| Realized Net Gain (Loss) | (770,444) | 43,919 |

| Change in Unrealized Appreciation (Depreciation) | 223,473 | (1,257,213) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (416,720) | (1,046,081) |

| Distributions | ||

| Net Investment Income | ||

| Investor Shares | (79,799) | (101,519) |

| Admiral Shares | (51,186) | (68,969) |

| Realized Capital Gain1 | ||

| Investor Shares | (14,956) | (170,339) |

| Admiral Shares | (9,460) | (112,961) |

| Total Distributions | (155,401) | (453,788) |

| Capital Share Transactions | ||

| Investor Shares | 136,361 | 86,183 |

| Admiral Shares | (3,445) | 49,809 |

| Net Increase (Decrease) from Capital Share Transactions | 132,916 | 135,992 |

| Total Increase (Decrease) | (439,205) | (1,363,877) |

| Net Assets | ||

| Beginning of Period | 4,337,774 | 5,701,651 |

| End of Period2 | 3,898,569 | 4,337,774 |

1 Includes fiscal 2008 short-term gain distributions totaling $32,961,000. Short-term gain distributions are treated as ordinary income

dividends for tax purposes.

2 Net Assets—End of Period includes undistributed (overdistributed) net investment income of ($4,554,000) and ($3,809,000).

See accompanying Notes, which are an integral part of the Financial Statements.

21

Equity Income Fund

Financial Highlights

| Investor Shares | |||||

| For a Share Outstanding | Year Ended September 30, | ||||

| Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 |

| Net Asset Value, Beginning of Period | $20.02 | $27.01 | $25.21 | $23.73 | $22.82 |

| Investment Operations | |||||

| Net Investment Income | .585 | .770 | .733 | .703 | .653 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | (2.506) | (5.617) | 3.215 | 2.541 | 2.069 |

| Total from Investment Operations | (1.921) | (4.847) | 3.948 | 3.244 | 2.722 |

| Distributions | |||||

| Dividends from Net Investment Income | (.587) | (.785) | (.730) | (.710) | (.640) |

| Distributions from Realized Capital Gains | (.112) | (1.358) | (1.418) | (1.054) | (1.172) |

| Total Distributions | (.699) | (2.143) | (2.148) | (1.764) | (1.812) |

| Net Asset Value, End of Period | $17.40 | $20.02 | $27.01 | $25.21 | $23.73 |

| Total Return1 | –9.12% | –18.92% | 16.29% | 14.39% | 12.27% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $2,423 | $2,626 | $3,445 | $3,035 | $2,934 |

| Ratio of Total Expenses to | |||||

| Average Net Assets2 | 0.36% | 0.30% | 0.29% | 0.31% | 0.32% |

| Ratio of Net Investment Income to | |||||

| Average Net Assets | 3.76% | 3.30% | 2.79% | 2.94% | 2.80% |

| Portfolio Turnover Rate | 51% | 55% | 51% | 26% | 42% |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

2 Includes performance-based investment advisory fee increases (decreases) of 0.02%, 0.00%, 0.00%, (0.01%), and (0.01%).

See accompanying Notes, which are an integral part of the Financial Statements.

22

Equity Income Fund

Financial Highlights

| Admiral Shares | |||||

| For a Share Outstanding | Year Ended September 30, | ||||

| Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 |

| Net Asset Value, Beginning of Period | $41.97 | $56.62 | $52.84 | $49.74 | $47.83 |

| Investment Operations | |||||

| Net Investment Income | 1.264 | 1.673 | 1.601 | 1.545 | 1.434 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | (5.269) | (11.772) | 6.746 | 5.324 | 4.338 |

| Total from Investment Operations | (4.005) | (10.099) | 8.347 | 6.869 | 5.772 |

| Distributions | |||||

| Dividends from Net Investment Income | (1.270) | (1.705) | (1.595) | (1.560) | (1.406) |

| Distributions from Realized Capital Gains | (.235) | (2.846) | (2.972) | (2.209) | (2.456) |

| Total Distributions | (1.505) | (4.551) | (4.567) | (3.769) | (3.862) |

| Net Asset Value, End of Period | $36.46 | $41.97 | $56.62 | $52.84 | $49.74 |

| Total Return | –9.05% | –18.82% | 16.44% | 14.55% | 12.42% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $1,475 | $1,711 | $2,256 | $1,783 | $1,417 |

| Ratio of Total Expenses to | |||||

| Average Net Assets1 | 0.24% | 0.18% | 0.17% | 0.17% | 0.19% |

| Ratio of Net Investment Income to | |||||

| Average Net Assets | 3.88% | 3.42% | 2.91% | 3.08% | 2.96% |

| Portfolio Turnover Rate | 51% | 55% | 51% | 26% | 42% |

| 1 Includes performance-based investment advisory fee increases (decreases) of 0.02%, 0.00%, 0.00%, (0.01%), and (0.01%). | |||||

See accompanying Notes, which are an integral part of the Financial Statements.

23

Equity Income Fund

Notes to Financial Statements

Vanguard Equity Income Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund offers two classes of shares: Investor Shares and Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, tenure, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluat ing changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

24

Equity Income Fund

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

4. Repurchase Agreements: The fund may invest in repurchase agreements. Securities pledged as collateral for repurchase agreements are held by a custodian bank until the agreements mature. Each agreement requires that the market value of the collateral be sufficient to cover payments of interest and principal; however, in the event of default or bankruptcy by the other party to the agreement, retention of the collateral may be subject to legal proceedings.

5. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (September 30, 2006–2009), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

6. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

7. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents the income earned on investing cash collateral, less expenses associated with the loan.

8. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses), shareholder reporting, and proxies. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. Wellington Management Company, LLP , provides investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee for Wellington Management Company, LLP, is subject to quarterly adjustments based on the fund’s performance for the preceding three years relative to the Lipper Equity Income Average for periods prior to April 1, 2008, and the new benchmark, the FTSE High Dividend Yield Index, beginning April 1, 2008. The benchmark change will be fully phased in by March 2011.

25

Equity Income Fund

The Vanguard Group provides investment advisory services to a portion of the fund on an at-cost basis; the fund paid Vanguard advisory fees of $408,000 for the year ended September 30, 2009.

For the year ended September 30, 2009, the aggregate investment advisory fee represented an effective annual basic rate of 0.08% of the fund’s average net assets, before an increase of $535,000 (0.02%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At September 30, 2009, the fund had contributed capital of $818,000 to Vanguard (included in Other Assets), representing 0.02% of the fund’s net assets and 0.33% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. The fund’s custodian bank has also agreed to reduce its fees when the fund maintains cash on deposit in the non-interest-bearing custody account. For the year ended September 30, 2009, these arrangements reduced the fund’s management and administrative expenses by $127,000 and custodian fees by $1,000. The total expense reduction represented an effective annual rate of 0.00% of the fund’s average net assets.

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the fund’s investments as of September 30, 2009, based on the inputs used to value them:

| Level 1 | Level 2 | Level 3 | |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 3,786,395 | 11,048 | — |

| Temporary Cash Investments | 82,196 | 24,989 | — |

| Futures Contracts—Liabilities1 | (164) | — | — |

| Total | 3,868,427 | 36,037 | — |

1 Represents variation margin on the last day of the reporting period.

26

Equity Income Fund

F. At September 30, 2009, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| ($000) | ||||

| Number of | Aggregate | Unrealized | ||

| Long (Short) | Settlement | Appreciation | ||

| Futures Contracts | Expiration | Contracts | Value | (Depreciation) |

| S&P 500 Index | December 2009 | 327 | 86,074 | 1,272 |

| E-mini S&P 500 Index | December 2009 | 91 | 4,791 | — |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

During the year ended September 30, 2009, the fund realized net foreign currency losses of $11,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized losses to undistributed net investment income.

For tax purposes, at September 30, 2009, the fund had $3,991,000 of ordinary income available for distribution. The fund had available capital loss carryforwards totaling $55,116,000 to offset future net capital gains through September 30, 2017. In addition, the fund realized losses of $727,490,000 during the period from November 1, 2008, through September 30, 2009, which are deferred and will be treated as realized for tax purposes in fiscal 2010.

At September 30, 2009, the cost of investment securities for tax purposes was $3,754,051,000. Net unrealized appreciation of investment securities for tax purposes was $150,577,000, consisting of unrealized gains of $435,764,000 on securities that had risen in value since their purchase and $285,187,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the year ended September 30, 2009, the fund purchased $1,881,461,000 of investment securities and sold $1,732,472,000 of investment securities, other than temporary cash investments.

27

Equity Income Fund

I. Capital share transactions for each class of shares were:

| Year Ended September 30, | ||||

| 2009 | 2 008 | |||

| Amount | Shares | Amount | Shares | |

| ($000) | (000) | ($000) | (000) | |

| Investor Shares | ||||

| Issued | 571,703 | 37,049 | 451,252 | 19,519 |

| Issued in Lieu of Cash Distributions | 86,878 | 5,584 | 250,105 | 10,727 |

| Redeemed | (522,220) | (34,497) | (615,174) | (26,649) |

| Net Increase (Decrease)—Investor Shares | 136,361 | 8,136 | 86,183 | 3,597 |

| Admiral Shares | ||||

| Issued | 297,028 | 9,259 | 280,117 | 5,772 |

| Issued in Lieu of Cash Distributions | 49,009 | 1,503 | 152,414 | 3,117 |

| Redeemed | (349,482) | (11,079) | (382,722) | (7,963) |

| Net Increase (Decrease)—Admiral Shares | (3,445) | (317) | 49,809 | 926 |

J. In preparing the financial statements as of September 30, 2009, management considered the impact of subsequent events occurring through November 10, 2009, for potential recognition or disclosure in these financial statements.

28

Report of Independent Registered

Public Accounting Firm

To the Trustees of Vanguard Fenway Funds and the Shareholders of Vanguard Equity Income Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard Equity Income Fund (the “Fund”) at September 30, 2009, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statement s in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at September 30, 2009 by correspondence with the custodians and brokers, and by agreement to the underlying ownership records for Vanguard Market Liquidity Fund, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

November 10, 2009

Special 2009 tax information (unaudited) for Vanguard Equity Income Fund

This information for the fiscal year ended September 30, 2009, is included pursuant to provisions of the Internal Revenue Code.

The fund distributed $24,436,000 as capital gain dividends (from net long-term capital gains) to shareholders during the fiscal year.

The fund distributed $130,985,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 98.3% of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

29

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2009. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

The table shows returns for Investor Shares only; returns for other share classes will differ. Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| Average Annual Total Returns: Equity Income Fund Investor Shares1 | |||

| Periods Ended September 30, 2009 | |||

| One | Five | Ten | |

| Year | Years | Years | |

| Returns Before Taxes | –9.12% | 1.93% | 3.03% |

| Returns After Taxes on Distributions | –9.72 | 0.69 | 1.75 |

| Returns After Taxes on Distributions and Sale of Fund Shares | –5.27 | 1.61 | 2.27 |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

30

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the fund’s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading “Expenses Paid During Period.”

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund’s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

| Six Months Ended September 30, 2009 | |||

| Beginning | Ending | Expenses | |

| Account Value | Account Value | Paid During | |

| Equity Income Fund | 3/31/2009 | 9/30/2009 | Period1 |

| Based on Actual Fund Return | |||

| Investor Shares | $1,000.00 | $1,315.29 | $2.03 |

| Admiral Shares | 1,000.00 | 1,315.64 | 1.39 |

| Based on Hypothetical 5% Yearly Return | |||

| Investor Shares | $1,000.00 | $1,023.31 | $1.78 |

| Admiral Shares | 1,000.00 | 1,023.87 | 1.22 |

1 The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for

that period are 0.35% for Investor Shares and 0.24% for Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to the

annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent

six-month period, then divided by the number of days in the most recent 12-month period.

31

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include the account service fee described in the prospectus. If such a fee were applied to your account, your costs would be higher. Your fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

32

Glossary

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. The percentage of a fund’s average net assets used to pay its annual administrative and advisory expenses. These expenses directly reduce returns to investors.

Foreign Holdings. The percentage of a fund represented by stocks or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

33

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (in the case of bonds) or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC y ield.

34

This page intentionally left blank.

The People Who Govern Your Fund