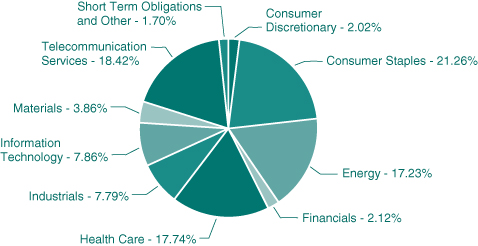

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number (811-07168)

Hennessy Funds Trust

(Exact name of registrant as specified in charter)

7250 Redwood Blvd., Suite 200

Novato, CA 94945

(Address of principal executive offices) (Zip code)

Neil J. Hennessy

Hennessy Advisors, Inc.

7250 Redwood Blvd., Suite 200

Novato, CA 94945

(Name and address of agent for service)

800-966-4354

Registrant's telephone number, including area code

Date of fiscal year end: October 31, 2011

Date of reporting period: April 30, 2011

Item 1. Reports to Stockholders.

HENNESSY FUNDS

SEMI-ANNUAL REPORT

APRIL 30, 2011

Hennessy Cornerstone Growth Fund

Hennessy Cornerstone Growth Fund, Series II

Hennessy Focus 30 Fund

Hennessy Cornerstone Large Growth Fund

Hennessy Cornerstone Value Fund

Hennessy Total Return Fund

Hennessy Balanced Fund

Contents

| Letter to shareholders | 1 |

| Performance overview | |

| Hennessy Cornerstone Growth Fund | 4 |

| Hennessy Cornerstone Growth Fund, Series II | 6 |

| Hennessy Focus 30 Fund | 8 |

| Hennessy Cornerstone Large Growth Fund | 10 |

| Hennessy Cornerstone Value Fund | 12 |

| Hennessy Total Return Fund | 14 |

| Hennessy Balanced Fund | 15 |

| Financial statements | |

| Schedules of investments | |

| Hennessy Cornerstone Growth Fund | 17 |

| Hennessy Cornerstone Growth Fund, Series II | 22 |

| Hennessy Focus 30 Fund | 27 |

| Hennessy Cornerstone Large Growth Fund | 32 |

| Hennessy Cornerstone Value Fund | 37 |

| Hennessy Total Return Fund | 43 |

| Schedule of Reverse Repurchase Agreements | 47 |

| Hennessy Balanced Fund | 48 |

| Statements of assets and liabilities | 52 |

| Statements of operations | 54 |

| Statements of changes in net assets | 56 |

| Statement of cash flows – Hennessy Total Return Fund | 63 |

| Financial highlights | |

| Hennessy Cornerstone Growth Fund | 64 |

| Hennessy Cornerstone Growth Fund, Series II | 68 |

| Hennessy Focus 30 Fund | 72 |

| Hennessy Cornerstone Large Growth Fund | 76 |

| Hennessy Cornerstone Value Fund | 80 |

| Hennessy Total Return Fund | 84 |

| Hennessy Balanced Fund | 86 |

| Notes to the financial statements | 89 |

| Expense example | 99 |

| Proxy voting policy | 101 |

| Quarterly Filings on Form N-Q | 101 |

| Directors and Officers | 101 |

| Board approval of continuation | |

| of investment advisory agreements | 102 |

June, 2011

Dear Hennessy Funds Shareholder:

When I last wrote to you, I discussed the themes of low confidence and lack of clarity from Washington that dominated the fiscal year ended October 31, 2010. And here we are, six months into our current fiscal year, and those themes are still front and center and affecting the recovery of our financial markets. We could add the global impact of the earthquake and tsunami in Japan, the political unrest in the Middle East and North Africa, the deadly storms and flooding in the southern part of the U.S. and fires in the state of Texas that all occurred during the last quarter to the events holding back market performance. However, despite all these global and national hurdles, what truly stands out to me is that our markets have been resilient. Through all this negativity, our economy continues to fight its way back to health.

Many developed nations, including the U.S., are grappling with high deficits, stagnant or falling home prices and stubbornly high unemployment rates, and this is causing some investors to fear that growth here in the U.S. is just not on firm footing yet. Many investors do, on the other hand, feel optimistic that an economic recovery is clearly underway, and that can be seen in the strong performance of the major U.S. indices. For example, the Dow Jones Industrial Average and the S&P 500 Indices each returned approximately 16-17% for the six-month period ended April 30, 2011. And, we are once again seeing high-quality stocks, those with strong fundamentals and growth potential, returning to favor and leading the market. I think that this past six-month period can best be characterized as a battle between fear and optimism in the financial markets.

There are some heroes in this battle of fear and optimism, and those definitely include U.S. corporations. Many companies are lean and productive. They have strong balance sheets and are growing stronger each quarter. The facts are that consumer spending is improving and the interest rate environment remains favorable. Here at Hennessy, we believe that the financial markets are still undervalued and are poised for long-term, moderate growth. We are enthusiastic about the outlook for the equity market and believe that it should continue to grow even through this onslaught of negativity.

I honestly believe that the average investor is bewildered by the volatile responses of Wall Street to the ebb-and-flow of what is basic economic data. But Wall Street is not the lone villain in this market drama. Unfortunately, we still don’t have any clear and actionable direction from our leaders in Washington, and in my opinion, this could

HENNESSY FUNDS 1-800-966-4354

continue to hinder economic recovery. Many U.S. companies are making a tremendous amount of money, but they are not hiring to grow their businesses until the rules and regulations and taxes are clearly laid out. How can the market make a strong recovery if Business and the Investor are sidelined by uncertainty and fear?

I would like to answer that. At Hennessy, we use history as our guide to running a business and to investing. I believe that the solution to many of our economic problems is not very complex. Throughout our history, the United States has not been a nation of “savers.” We are consumers. I believe that if taxes were lowered, average Americans would have more money in their pockets, and they may feel more comfortable spending. That increase in demand would cause a need for a rise in inventories, and companies would need to supply those inventories by increasing production, which of course, means hiring and job growth.

Even without lowered taxes the economy is forging ahead. The majority of companies continue to navigate through the mine field of uncertainty, while still making plenty of money for their shareholders. I believe that with strong leadership and clarity from our government, companies should begin to gain confidence, to reinvest in their business models, and most importantly to hire, which should lead to an expanded and sustainable economic recovery.

When I hear our elected officials discuss “Too Big to Fail” when describing our financial institutions, I am in dismay. The U.S. Government is following the exact path that these financial companies took to their eventual demise. These financial firms leveraged themselves to the hilt (think growing U.S. deficit) by continuing to borrow, and then they were bailed out by TARP. I am here to tell you that there is no TARP for the U.S. Government; rather the bailout will come in the form of an increased burden on each of us taxpayers.

Despite the continued fear and uncertainty in the current markets, I continue to fall on the side of optimism and I believe the recovery is real and should just get stronger as we, as a nation, address the issues facing us. As always, we will continue to manage money for the long term, in the sole interest of our shareholders. At Hennessy Funds, we pride ourselves on serving each of our investors directly, so please don’t ever hesitate to contact us at 800-966-4354 if we can answer any questions or can be of service.

Best regards,

Neil J. Hennessy

Portfolio Manager & Chief Investment Officer

LETTER TO SHAREHOLDERS

Past performance does not guarantee future results.

Mutual fund investing involves risk. Principal loss is possible.

Opinions expressed are those of Neil Hennessy and are subject to change, are not guaranteed and should not be considered investment advice.

The Dow Jones Industrial Average and S&P 500 are unmanaged indices commonly used to measure performance of U.S. stocks and assume reinvestment of dividends. You cannot invest directly in an index.

HENNESSY FUNDS 1-800-966-4354

Hennessy Cornerstone Growth Fund

Original Class Shares (HFCGX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | One | Five | Ten |

| | Months | Year | Years | Years |

| Hennessy Cornerstone | | | | |

| Growth Fund – Original Class | 20.04% | 16.42% | -6.44% | 4.81% |

| Russell 2000 Index | 23.73% | 22.20% | 3.89% | 7.34% |

| S&P 500 Index | 16.36% | 17.22% | 2.95% | 2.82% |

Gross expense ratio: 1.34%

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. The gross expense ratio presented is that from the most recent prospectus.

PERFORMANCE NARRATIVE

The Hennessy Cornerstone Growth Fund returned 20.04% for the six-month period ended April 30, 2011, underperforming its benchmark, the Russell 2000 Index, which returned 23.73%, but outperforming the S&P 500 Index, which returned 16.36%, for the same period. Prior to its rebalance in the winter, the Fund underperformed the benchmark and after the rebalance it has subsequently outperformed the benchmark. Before the rebalance took place, we had a positive allocation effect led by the portfolio’s overweight position in the Energy sector and underweight position in the Financial sector. This was offset by individual stock selection within the portfolio, which dragged down its relative returns. Prior to the rebalance, the best performing stock was American Axel & Manufacturing Holdings (AXL), which issued a better than expected Q3 ‘10 earnings report, while the worst performer was Global Cash Access Holdings (GCA), as the company delivered weak earnings for Q3 and lowered guidance going forward. Post-rebalance, the Fund’s relative outperformance versus its benchmark was driven largely by security selection. We had a slight underperformance to the benchmark due to an overweight allocation to the Consumer Discretionary sector and an underweight position in the Health Care sector, but this was more than made up for by the positive contribution from security selection. The top performing company after the rebalance was Sauer-Danfoss (SHS), which rose sharply after strong Q4 ‘10 earnings, while the worst performing stock was CPI Corp. (CPY), which issued a worse than expected earnings for Q4 ‘10. In general, stocks within the Energy, Materials and Industrial sectors were positive contributors to relative returns.

PERFORMANCE REVIEW — HENNESSY CORNERSTONE GROWTH FUND

Hennessy Cornerstone Growth Fund

Institutional Class Shares (HICGX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | | Since Inception |

| | Months | One Year | (3/3/08) |

| Hennessy Cornerstone | | | |

| Growth Fund – Institutional Class | 20.25% | 16.87% | -2.23% |

| Russell 2000 Index | 23.73% | 22.20% | 9.26% |

| S&P 500 Index | 16.36% | 17.22% | 3.02% |

Gross expense ratio: 1.09%. Net expense ratio: 0.98%. The expense ratio is contractually capped at 0.98% indefinitely.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced. The expense ratios presented are that from the most recent prospectus.

The S&P 500 Index and Russell 2000 Index are unmanaged indices commonly used to measure the performance of U.S. Stocks. You cannot invest directly in an index. Small and medium-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies. Investments in foreign securities involve greater volatility and political, economic and currency risk and differences in accounting methods. References to specific securities should not be considered a recommendation to buy or sell any security. Fund holdings and sector allocations are subject to change. Please refer to the included Schedule of Investments.

HENNESSY FUNDS 1-800-966-4354

Hennessy Cornerstone Growth Fund, Series II

Original Class Shares (HENLX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | One | Five | Since Inception |

| | Months | Year | Years | (7/1/05) |

| Hennessy Cornerstone Growth | | | | |

| Fund, Series II – Original Class | 21.02% | 19.39% | -8.24% | -3.24% |

| Russell 2000 Growth Index | 27.07% | 30.29% | 5.14% | 8.11% |

| S&P 500 Index | 16.36% | 17.22% | 2.95% | 4.44% |

Gross expense ratio: 1.62%.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. The gross expense ratio presented is that from the most recent prospectus.

PERFORMANCE NARRATIVE

The Hennessy Cornerstone Growth Fund, Series II returned 21.02% for the six-month period ended April 30, 2011, underperforming its benchmark, the Russell 2000 Growth Index, which returned 27.07%, but outperforming the S&P 500 Index, which returned 16.36%, for the same period. Security selection in the Consumer Discretionary and Telecommunications Services sectors drove the strong performance but was offset relative to the benchmark with weaker security selection in the Information Technology and Financial sectors. The Fund’s overweight allocation to Industrials and underweight allocation to Information Technology also contributed to a lag in relative performance. The best performing stock in the Fund was IDT Corp (IDT), which was up over 100% due to better than expected Q1 ‘11 earnings released in December. The worst performing stock in the Fund was Lionbridge Technologies (LIOX), which was down nearly -33% after missing earnings estimates for Q3 ‘10.

PERFORMANCE REVIEW — HENNESSY CORNERSTONE GROWTH FUND, SERIES II

Hennessy Cornerstone Growth Fund, Series II

Institutional Class Shares (HINLX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | | Since Inception |

| | Months | One Year | (3/3/08) |

| Hennessy Cornerstone Growth | | | |

| Fund, Series II – Institutional Class | 21.36% | 20.10% | -3.25% |

| Russell 2000 Growth Index | 27.07% | 30.29% | 10.75% |

| S&P 500 Index | 16.36% | 17.22% | 3.02% |

Gross expense ratio: 1.40%. Net expense ratio: 0.98%. The expense ratio is contractually capped at 0.98% indefinitely.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced. The expense ratios presented are that from the most recent prospectus.

The Russell 2000 Growth Index and S&P 500 Index are unmanaged indices commonly used to measure the performance of U.S. Stocks. You cannot invest directly in an index. Small and medium-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies. Investments in foreign securities involve greater volatility and political, economic and currency risk and differences in accounting methods. References to specific securities should not be considered a recommendation to buy or sell any security. Fund holdings and sector allocations are subject to change. Please refer to the included Schedule of Investments.

HENNESSY FUNDS 1-800-966-4354

Hennessy Focus 30 Fund

Original Class Shares (HFTFX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | One | Five | Since Inception |

| | Months | Year | Years | (9/17/03) |

| Hennessy Focus 30 Fund – | | | | |

| Original Class | 22.72% | 29.43% | 3.82% | 11.63% |

| S&P Midcap 400 Index | 23.25% | 25.07% | 6.35% | 10.52% |

| S&P 500 Index | 16.36% | 17.22% | 2.95% | 5.90% |

Gross expense ratio: 1.40%

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. The gross expense ratio presented is that from the most recent prospectus.

PERFORMANCE NARRATIVE

While the Hennessy Focus 30 Fund returned 22.72% for the six-month period ended April 30, 2011, it slightly underperformed its benchmark, the S&P 400 Mid-cap Index, which returned 23.25%, but outperformed the S&P 500 Index, which returned 16.36%, for the same period. Security selection in the Industrials and Information Technology sectors hampered the Fund’s relative performance and offset positive security selection in the Consumer Discretionary and Health Care sectors. Even with the positive impact of sector allocation, including overweight positions in Materials and Consumer Discretionary sector and an underweight position in the Utilities sector, the Fund still marginally underperformed its benchmark. The best performing stock in the Fund over the six-month period was Ulta Salon Cosmetics & Fragrance (ULTA), up over 72% on strong earnings and sales, while the worst performing stock was US Airways Group (LCC), falling -23% amid contract disputes with their pilots and higher oil costs.

PERFORMANCE REVIEW — HENNESSY FOCUS 30 FUND

Hennessy Focus 30 Fund

Institutional Class Shares (HIFTX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | | Since Inception |

| | Months | One Year | (3/3/08) |

| Hennessy Focus 30 Fund – | | | |

| Institutional Class | 23.03% | 30.06% | 7.20% |

| S&P Midcap 400 Index | 23.25% | 25.07% | 9.99% |

| S&P 500 Index | 16.36% | 17.22% | 3.02% |

Gross expense ratio: 1.17%. Net expense ratio: 0.98%. The expense ratio is contractually capped at 0.98% indefinitely.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced. The expense ratios presented are that from the most recent prospectus.

The S&P 500 Index and S&P Midcap 400 Index are unmanaged indices commonly used to measure the performance of U.S. Stocks. You cannot invest directly in an index. Small and medium-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies. References to specific securities should not be considered a recommendation to buy or sell any security. Fund holdings and sector allocations are subject to change. Please refer to the included Schedule of Investments.

HENNESSY FUNDS 1-800-966-4354

Hennessy Cornerstone Large Growth Fund

Original Class Shares (HFLGX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | | Since Inception |

| | Months | One Year | (3/20/09) |

| Hennessy Cornerstone Large | | | |

| Growth Fund – Original Class* | 16.27% | 21.68% | 39.85% |

| Russell 1000 Index | 17.12% | 18.02% | 35.29% |

| S&P 500 Index | 16.36% | 17.22% | 33.88% |

Gross expense ratio: 1.30%.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. The gross expense ratio presented is that from the most recent prospectus.

| * | On March 20, 2009, the Tamarack Large Cap Growth Fund was reorganized into the Hennessy Cornerstone Large Growth Fund. At that time, the Fund began utilizing a purely quantitative formula to choose stocks for the portfolio, which differs from the investment strategy employed by the previous investment manager. Accordingly, performance is being reported for the period after the reorganization. |

PERFORMANCE NARRATIVE

The Hennessy Cornerstone Large Growth Fund returned 16.27% for the six-month period ended April 30, 2011, slightly underperforming its benchmark, the Russell 1000 Index, which returned 17.12%, and the S&P 500 Index, which returned 16.36%, for the same period. While the portfolio’s underweight position in the Information Technology, Utilities and Financials sectors were positive contributors to overall allocation effect, the underweight position in the Energy sector versus the benchmark effectively negated the positive allocation effect from the other sectors. The Fund had a positive effect from security selection during the period, with the major contributions coming from the Industrial and Financial sectors. The portfolio’s holdings within the Consumer Discretionary and Consumer Staples sectors had a negative selection effect, but that was not enough to offset the gains from the Industrials and Financials sectors. The best performing stock in the portfolio was Consol Energy (CNX), which gained nearly 48% on strong earnings and higher commodity prices. The worst performer was Best Buy (BBY), down nearly -27% for the period due to weaker earning reported for Q3 ‘10.

PERFORMANCE REVIEW — HENNESSY CORNERSTONE LARGE GROWTH FUND

Hennessy Cornerstone Large Growth Fund

Institutional Class Shares (HILGX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | | Since Inception |

| | Months | One Year | (3/20/09) |

| Hennessy Cornerstone Large | | | |

| Growth Fund – Institutional Class | 16.45% | 22.06% | 40.30% |

| Russell 1000 Index | 17.12% | 18.02% | 35.29% |

| S&P 500 Index | 16.36% | 17.22% | 33.88% |

Gross expense ratio: 1.16%. Net expense ratio: 0.98%. The expense ratio is contractually capped at 0.98% indefinitely.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced. The expense ratios presented are that from the most recent prospectus.

The S&P 500 and Russell 1000 are unmanaged indices commonly used to measure the performance of U.S. stocks. One cannot invest directly in an index. Medium-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies. Growth stocks typically are more volatile than value stocks; however value stocks have a lower expected growth rate in earnings and sales. References to specific securities should not be considered a recommendation to buy or sell any security. Fund holdings and sector allocations are subject to change. Please refer to the included Schedule of Investments.

HENNESSY FUNDS 1-800-966-4354

Hennessy Cornerstone Value Fund

Original Class Shares (HFCVX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | One | Five | Ten |

| | Months | Year | Years | Years |

| Hennessy Cornerstone | | | | |

| Value Fund – Original Class | 10.52% | 15.40% | 2.50% | 3.88% |

| Russell 1000 Value Index | 17.29% | 15.24% | 1.40% | 4.31% |

| S&P 500 Index | 16.36% | 17.22% | 2.95% | 2.82% |

Gross expense ratio: 1.30%

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. The gross expense ratio presented is that from the most recent prospectus.

PERFORMANCE NARRATIVE

The Hennessy Cornerstone Value Fund returned 10.52% for the six-month period ending April 30, 2011, underperforming its benchmark, the Russell 1000 Value, which returned 17.29%, and the S&P 500, which returned 16.36%, for the same period. The Fund’s underperformance was the result of security selection across a number of sectors, specifically Telecommunication Services, Energy and Industrials. The positive effects of security selection in the Consumer Discretionary, Financials and Information Technologies sectors were not enough to offset stock selections in other sectors. Sector allocation contributed slightly to overall performance and can be largely attributed to the Fund’s underweight position versus the benchmark in the Financials sector. The top performer in the portfolio was Chevron Corp. (CVX), up nearly 35%, which benefitted from strong oil prices. ConocoPhillips (COP) and Statoil ASA (STO) both also performed well while in the portfolio, with each stock gaining approximately 34%. The weakest performing stock in the portfolio was Nokia (NOK), which slid nearly -14% after its CEO outlined serious challenges in a memo to employees where he suggested that Nokia had made errors that left the firm “years behind” rivals such as Apple and Google.

PERFORMANCE REVIEW — HENNESSY CORNERSTONE VALUE FUND

Hennessy Cornerstone Value Fund

Institutional Class Shares (HICVX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | | Since Inception |

| | Months | One Year | (3/3/08) |

| Hennessy Cornerstone Value Fund – | | | |

| Institutional Class | 10.78% | 15.77% | 3.13% |

| Russell 1000 Value Index | 17.29% | 15.24% | 1.17% |

| S&P 500 Index | 16.36% | 17.22% | 3.02% |

Gross expense ratio: 1.11%. Net expense ratio: 0.98%. The expense ratio is contractually capped at 0.98% indefinitely.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced. The expense ratios presented are that from the most recent prospectus.

The Russell 1000 Value Index and S&P 500 Index are unmanaged indices commonly used to measure the performance of U.S. Stocks. You cannot invest directly in an index. The Fund may invest in medium-capitalization companies which tend to have limited liquidity and greater price volatility than large-capitalization companies. Investments in foreign securities involve greater volatility and political, economic and currency risk and differences in accounting methods. References to specific securities should not be considered a recommendation to buy or sell any security. Fund holdings and sector allocations are subject to change. Please refer to the included Schedule of Investments.

HENNESSY FUNDS 1-800-966-4354

Hennessy Total Return Fund

Original Class Shares (HDOGX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | One | Five | Ten |

| | Months | Year | Years | Years |

| Hennessy Total Return Fund | 10.60% | 16.84% | 2.68% | 3.00% |

| Dow Jones Industrial Average | 16.71% | 19.50% | 5.20% | 4.28% |

| S&P 500 Index | 16.36% | 17.22% | 2.95% | 2.82% |

Gross expense ratio: 1.34%

Expenses net of interest expense: 1.26%

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. The gross and net expense ratios presented is that from the most recent prospectus.

PERFORMANCE NARRATIVE

The Hennessy Total Return Fund returned 10.60% for the six-month period ended April 30, 2011, compared to the Dow Jones Industrial Average, which returned 16.71%, and the S&P 500 Index, which returned 16.36% for the same period. The Fund’s relative underperformance to its benchmark is due primarily to low yields on the Total Return Fund’s approximately 25% position in short-term Treasury Bills. A number of the “Dogs of the Dow” companies held in the portfolio performed well during the period, including Chevron (CVX), which gained nearly 35%, General Electric (GE), which gained nearly 30% and Pfizer (PFE), which gained 23% for the six-month period. Chevron was the top performing stock in the portfolio, while Merck (MRK) was the poorest performer, gaining just 1%. Many of these large companies increased their dividend during the period.

The Dow Jones Industrial Average and S&P 500 Index are unmanaged indices commonly used to measure the performance of U.S. Stocks. You cannot invest directly in an index. The Hennessy Total Return Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund, making it more exposed to individual stock volatility than a diversified fund. References to specific securities should not be considered a recommendation to buy or sell any security. Fund holdings are subject to change. Please refer to the included Schedule of Investments.

PERFORMANCE REVIEW — HENNESSY TOTAL RETURN FUND AND HENNESSY BALANCED FUND

Hennessy Balanced Fund

Original Class Shares (HBFBX)

AVERAGE ANNUAL TOTAL RETURN PERIODS ENDED APRIL 30, 2011

| | Six | One | Five | Ten |

| | Months | Year | Years | Years |

| Hennessy Balanced Fund | 7.53% | 11.98% | 3.17% | 2.39% |

| Dow Jones Industrial Average | 16.71% | 19.50% | 5.20% | 4.28% |

| S&P 500 Index | 16.36% | 17.22% | 2.95% | 2.82% |

Gross expense ratio: 1.66%

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.hennessyfunds.com. The gross expense ratio presented is that from the most recent prospectus.

PERFORMANCE NARRATIVE

The Hennessy Balanced Fund returned 7.53% for the six-month period ended April 30, 2011, compared to the Dow Jones Industrial Average, which returned 16.71%, and the S&P 500 Index, which returned 16.36%, for the same period. The Fund’s relative underperformance to its benchmark is due primarily to low yields on the Balanced Fund’s approximately 50% position in short-term Treasury Bills. A number of the “Dogs of the Dow” companies held in the portfolio performed well during the period, including Chevron (CVX), which gained nearly 35%, General Electric (GE), which gained nearly 30%, and Pfizer (PFE), which gained 23%. Chevron was the top performing stock in the portfolio, while Merck (MRK) was the poorest performer, gaining just 1%. Many of these large companies increased their dividend during the period.

The Dow Jones Industrial Average and S&P 500 Index are unmanaged indices commonly used to measure the performance of U.S. Stocks. You cannot invest directly in an index. The Hennessy Balanced Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund, making it more exposed to individual stock volatility than a diversified fund. References to specific securities should not be considered a recommendation to buy or sell any security. Fund holdings are subject to change. Please refer to the included Schedule of Investments.

HENNESSY FUNDS 1-800-966-4354

(This Page Intentionally Left Blank.)

SCHEDULE OF INVESTMENTS — HENNESSY CORNERSTONE GROWTH FUND

Schedules of Investments

HENNESSY CORNERSTONE GROWTH FUND

As of April 30, 2011 (Unaudited)

(% of Net Assets)

| TOP TEN EQUITY HOLDINGS | % of net assets |

| Sauer-Danfoss, Inc. | 3.23% |

| Atlas Energy LP | 3.10% |

| Mercer International, Inc. | 3.08% |

| Innospec, Inc. | 2.98% |

| Titan International, Inc. | 2.86% |

| Western Refining, Inc. | 2.74% |

| Atlas Pipeline Partners LP | 2.56% |

| TPC Group, Inc. | 2.42% |

| iStar Financial, Inc. | 2.37% |

| Buckeye Technologies, Inc. | 2.30% |

HENNESSY FUNDS 1-800-966-4354

| | COMMON STOCKS – 98.10% | | Number | | | | | | % of Net | |

| | | | of Shares | | | Value | | | Assets | |

| | Consumer Discretionary – 26.40% | | | | | | | | | |

| | Ann, Inc. (a) | | | 140,400 | | | $ | 4,381,884 | | | | 2.00 | % |

| | Borg Warner, Inc. (a) | | | 56,200 | | | | 4,340,888 | | | | 1.98 | % |

| | Cost Plus, Inc. (a) | | | 365,200 | | | | 3,977,028 | | | | 1.82 | % |

| | CPI Corp. | | | 131,600 | | | | 2,364,852 | | | | 1.08 | % |

| | Dillards, Inc. | | | 103,400 | | | | 4,965,268 | | | | 2.27 | % |

| | DineEquity, Inc. (a) | | | 67,700 | | | | 3,382,969 | | | | 1.55 | % |

| | Krispy Kreme Doughnuts, Inc. (a) | | | 514,600 | | | | 2,886,906 | | | | 1.32 | % |

| | Libbey, Inc. (a) | | | 260,000 | | | | 4,433,000 | | | | 2.03 | % |

| | Pier 1 Imports, Inc. (a) | | | 356,900 | | | | 4,347,042 | | | | 1.98 | % |

| | Quiksilver, Inc. (a) | | | 740,500 | | | | 3,221,175 | | | | 1.47 | % |

| | Ruby Tuesday, Inc. (a) | | | 275,200 | | | | 2,892,352 | | | | 1.32 | % |

| | Tenneco, Inc. (a) | | | 91,000 | | | | 4,205,110 | | | | 1.92 | % |

| | Tractor Supply Co. | | | 78,900 | | | | 4,881,543 | | | | 2.23 | % |

| | TRW Automotive Holdings Corp. (a) | | | 71,800 | | | | 4,096,908 | | | | 1.87 | % |

| | Tuesday Morning Corp. (a) | | | 681,500 | | | | 3,407,500 | | | | 1.56 | % |

| | | | | | | | | 57,784,425 | | | | 26.40 | % |

| | Consumer Staples – 3.46% | | | | | | | | | | | | |

| | Pricesmart, Inc. | | | 97,300 | | | | 4,051,572 | | | | 1.85 | % |

| | SunOpta, Inc. (a)(b) | | | 500,200 | | | | 3,531,412 | | | | 1.61 | % |

| | | | | | | | | 7,582,984 | | | | 3.46 | % |

| | Energy – 8.40% | | | | | | | | | | | | |

| | Atlas Energy LP | | | 254,200 | | | | 6,776,972 | | | | 3.10 | % |

| | Atlas Pipeline Partners LP | | | 151,300 | | | | 5,592,048 | | | | 2.56 | % |

| | Western Refining, Inc. (a) | | | 354,200 | | | | 6,007,232 | | | | 2.74 | % |

| | | | | | | | | 18,376,252 | | | | 8.40 | % |

| | Financials – 7.72% | | | | | | | | | | | | |

| | Ashford Hospitality Trust, Inc. (a) | | | 368,800 | | | | 4,598,936 | | | | 2.10 | % |

| | Grupo Financiero Galicia SA – ADR (a)(b) | | | 243,200 | | | | 3,108,096 | | | | 1.42 | % |

| | iStar Financial, Inc. (a) | | | 539,000 | | | | 5,185,180 | | | | 2.37 | % |

| | Newcastle Investment Corp. (a) | | | 635,500 | | | | 4,010,005 | | | | 1.83 | % |

| | | | | | | | | 16,902,217 | | | | 7.72 | % |

| | Health Care – 1.71% | | | | | | | | | | | | |

| | MedCath Corp. (a) | | | 276,600 | | | | 3,736,866 | | | | 1.71 | % |

The accompanying notes are an integral part of these financial statements.

SCHEDULE OF INVESTMENTS — HENNESSY CORNERSTONE GROWTH FUND

| | COMMON STOCKS | | Number | | | | | | % of Net | |

| | | | of Shares | | | Value | | | Assets | |

| | Industrials – 25.88% | | | | | | | | | |

| | Air Transport Services Group, Inc. (a) | | | 470,800 | | | $ | 3,851,144 | | | | 1.76 | % |

| | Amerco (a) | | | 36,000 | | | | 3,661,920 | | | | 1.67 | % |

| | Commercial Vehicle Group, Inc. (a) | | | 214,500 | | | | 3,702,270 | | | | 1.69 | % |

| | Greenbrier Companies, Inc. (a) | | | 164,300 | | | | 4,447,601 | | | | 2.03 | % |

| | Interface, Inc. | | | 241,900 | | | | 4,509,016 | | | | 2.06 | % |

| | NACCO Industries, Inc. | | | 35,100 | | | | 3,693,573 | | | | 1.69 | % |

| | Sauer-Danfoss, Inc. (a) | | | 119,600 | | | | 7,057,596 | | | | 3.23 | % |

| | Timken Co. | | | 78,700 | | | | 4,437,893 | | | | 2.03 | % |

| | Titan International, Inc. | | | 202,800 | | | | 6,264,492 | | | | 2.86 | % |

| | Trimas Corp. (a) | | | 167,600 | | | | 3,889,996 | | | | 1.78 | % |

| | United Continental Holdings, Inc. (a) | | | 144,100 | | | | 3,288,362 | | | | 1.50 | % |

| | United Rentals, Inc. (a) | | | 160,000 | | | | 4,707,200 | | | | 2.15 | % |

| | US Airways Group, Inc. (a) | | | 344,200 | | | | 3,128,778 | | | | 1.43 | % |

| | | | | | | | | 56,639,841 | | | | 25.88 | % |

| | Information Technology – 6.68% | | | | | | | | | | | | |

| | DDi Corp. | | | 322,900 | | | | 3,103,069 | | | | 1.42 | % |

| | Kemet Corp. (a) | | | 292,300 | | | | 4,597,879 | | | | 2.10 | % |

| | Newport Corp. (a) | | | 220,100 | | | | 4,122,473 | | | | 1.88 | % |

| | Power One, Inc. (a) | | | 337,700 | | | | 2,789,402 | | | | 1.28 | % |

| | | | | | | | | 14,612,823 | | | | 6.68 | % |

| | Materials – 14.53% | | | | | | | | | | | | |

| | Buckeye Technologies, Inc. | | | 179,100 | | | | 5,043,456 | | | | 2.30 | % |

| | Innospec, Inc. (a) | | | 172,900 | | | | 6,511,414 | | | | 2.98 | % |

| | Materion Corp. (a) | | | 97,900 | | | | 4,088,304 | | | | 1.87 | % |

| | Mercer International, Inc. (a) | | | 554,000 | | | | 6,742,180 | | | | 3.08 | % |

| | Quaker Chem Corp. | | | 91,000 | | | | 4,111,380 | | | | 1.88 | % |

| | TPC Group, Inc. (a) | | | 134,400 | | | | 5,300,736 | | | | 2.42 | % |

| | | | | | | | | 31,797,470 | | | | 14.53 | % |

| | Telecommunication Services – 3.32% | | | | | | | | | | | | |

| | General Communication, Inc. (a) | | | 301,700 | | | | 3,469,550 | | | | 1.59 | % |

| | IDT Corp. | | | 130,600 | | | | 3,786,094 | | | | 1.73 | % |

| | | | | | | | | 7,255,644 | | | | 3.32 | % |

| | | | | | | | | | | | | | |

| | Total Common Stocks (Cost $188,353,254) | | | | | | | 214,688,522 | | | | 98.10 | % |

The accompanying notes are an integral part of these financial statements.

HENNESSY FUNDS 1-800-966-4354

| | SHORT-TERM INVESTMENTS – 0.00% | | Number of | | | | | | % of Net | |

| | | | Shares | | | Value | | | Assets | |

| | Money Market Funds – 0.00% | | | | | | | | | |

| | Fidelity Government Portfolio – | | | | | | | | | |

| | Institutional Class, 0.0100% (c) | | | 262 | | | $ | 262 | | | | 0.00 | % |

| | | | | | | | | | | | | | |

| | Total Money Market Funds | | | | | | | | | | | | |

| | (Cost $262) | | | | | | | 262 | | | | 0.00 | % |

| | | | | | | | | | | | | | |

| | Total Short-Term Investments | | | | | | | | | | | | |

| | (Cost $262) | | | | | | | 262 | | | | 0.00 | % |

| | | | | | | | | | | | | | |

| | Total Investments – 98.10% | | | | | | | | | | | | |

| | (Cost $188,353,516) | | | | | | | 214,688,784 | | | | 98.10 | % |

| | | | | | | | | | | | | | |

| | Other Assets in Excess of Liabilities – 1.90% | | | | | | | 4,157,216 | | | | 1.90 | % |

| | TOTAL NET ASSETS – 100.00% | | | | | | $ | 218,846,000 | | | | 100.00 | % |

Percentages are stated as a percent of net assets.

ADR American Depository Receipt

(a)Non-income producing security.

(b)Foreign issued security.

(c)The rate listed is the Fund’s 7-day yield as of April 30, 2011.

Summary of Fair Value Exposure at April 30, 2011

The Fund has adopted authoritative fair valuation accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion in changes in valuation techniques and related inputs during the period. These inputs are summarized in the three broad levels listed below.

Securities which are traded on a national or recognized stock exchange are valued at the last sale price on the securities exchange on which such securities are primarily traded. Exchange-traded securities for which there were no transactions that day and debt securities are valued at the most recent bid prices. Instruments with a remaining maturity of 60 days or less are valued on an amortized cost basis. When a price for an underlying security is not readily available or if a significant event has occurred that indicates the closing price of a security no longer represents the true value of that security, fair value pricing procedures have been adopted by the Board of Directors of the Funds. Fair value pricing determinations are made in good faith in accordance with these procedures. There are numerous criteria that will be given consideration in determining a fair value of a security. Some of these criteria are: trading volume of security and markets, value of other like securities and news events with direct bearing to security or market. Fair value pricing results in an estimated price that reasonably reflects the current market conditions in order to rate the portfolio holdings such that shareholder transactions receive a fair net asset value.

The accompanying notes are an integral part of these financial statements.

SCHEDULE OF INVESTMENTS — HENNESSY CORNERSTONE GROWTH FUND

The Fund has performed an analysis of all existing investments to determine the significance and character of all inputs to their fair value determination.

| | Level 1 – | Quoted unadjusted prices for identical instruments in active markets to which the Fund has access at the date of measurement. |

| | Level 2 – | Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets. Level 2 inputs are those in markets for which there are few transactions, the prices are not current, little public information exists or instances where prices vary substantially over time or among brokered market makers. |

| | Level 3 – | Model derived valuations in which one or more significant inputs or significant value drivers are unobservable. Unobservable inputs are those inputs that reflect the Fund’s own assumptions that market participants would use to price the asset or liability based on the best available information. |

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s net assets as of April 30, 2011:

| | Common Stock | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | Consumer Discretionary | | $ | 57,784,425 | | | $ | — | | | $ | — | | | $ | 57,784,425 | |

| | Consumer Staples | | | 7,582,984 | | | | — | | | | — | | | | 7,582,984 | |

| | Energy | | | 18,376,252 | | | | — | | | | — | | | | 18,376,252 | |

| | Financials | | | 16,902,217 | | | | — | | | | — | | | | 16,902,217 | |

| | Health Care | | | 3,736,866 | | | | — | | | | — | | | | 3,736,866 | |

| | Industrials | | | 56,639,841 | | | | — | | | | — | | | | 56,639,841 | |

| | Information Technology | | | 14,612,823 | | | | — | | | | — | | | | 14,612,823 | |

| | Materials | | | 31,797,470 | | | | — | | | | — | | | | 31,797,470 | |

| | Telecommunication Services | | | 7,255,644 | | | | — | | | | — | | | | 7,255,644 | |

| | Total Common Stock | | $ | 214,688,522 | | | $ | — | | | $ | — | | | $ | 214,688,522 | |

| | Short-Term Investments | | $ | 262 | | | $ | — | | | $ | — | | | $ | 262 | |

| | Total Investments in Securities | | $ | 214,688,784 | | | $ | — | | | $ | — | | | $ | 214,688,784 | |

Transfers between levels are recognized at the end of the reporting period. During the period ended April 30, 2011, the Fund recognized no significant transfers between levels.

The accompanying notes are an integral part of these financial statements.

HENNESSY FUNDS 1-800-966-4354

HENNESSY CORNERSTONE

GROWTH FUND, SERIES II

As of April 30, 2011 (Unaudited)

(% of Net Assets)

| TOP TEN EQUITY HOLDINGS | % of net assets |

| IDT Corp. | 4.54% |

| Ulta Salon Cosmetics & Fragrance, Inc. | 3.27% |

| Trimas Corp. | 3.04% |

| TRW Automotive Holdings Corp. | 2.87% |

| Macquarie Infrastructure Co. LLC | 2.76% |

| Gardner Denver, Inc. | 2.71% |

| Crocs, Inc. | 2.70% |

| Sinclair Broadcast Group, Inc. | 2.65% |

| Loral Space & Communications, Inc. | 2.58% |

| Cardtronics, Inc. | 2.58% |

SCHEDULE OF INVESTMENTS — HENNESSY CORNERSTONE GROWTH FUND, SERIES II

| | COMMON STOCKS – 95.71% | | Number | | | | | | % of Net | |

| | | | of Shares | | | Value | | | Assets | |

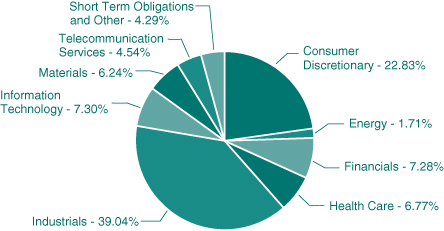

| | Consumer Discretionary – 22.83% | | | | | | | | | |

| | Brown Shoe, Inc. | | | 30,100 | | | $ | 380,765 | | | | 1.16 | % |

| | Crocs, Inc. (a) | | | 44,100 | | | | 886,851 | | | | 2.70 | % |

| | Libbey, Inc. (a) | | | 37,200 | | | | 634,260 | | | | 1.93 | % |

| | Lifetime Brands, Inc. (a) | | | 31,700 | | | | 504,664 | | | | 1.54 | % |

| | Media General, Inc. (a) | | | 46,600 | | | | 251,174 | | | | 0.77 | % |

| | Select Comfort Corp. (a) | | | 53,000 | | | | 841,110 | | | | 2.56 | % |

| | Sinclair Broadcast Group, Inc. | | | 75,700 | | | | 869,793 | | | | 2.65 | % |

| | Skechers USA, Inc. (a) | | | 12,600 | | | | 240,030 | | | | 0.73 | % |

| | TRW Automotive Holdings Corp. (a) | | | 16,500 | | | | 941,490 | | | | 2.87 | % |

| | Ulta Salon Cosmetics & Fragrance, Inc. (a) | | | 20,200 | | | | 1,074,438 | | | | 3.27 | % |

| | Valassis Communications, Inc. (a) | | | 14,500 | | | | 418,035 | | | | 1.28 | % |

| | Whirlpool Corp. | | | 5,200 | | | | 448,136 | | | | 1.37 | % |

| | | | | | | | | 7,490,746 | | | | 22.83 | % |

| | Energy – 1.71% | | | | | | | | | | | | |

| | Callon Petroleum Co. (a) | | | 82,000 | | | | 561,700 | | | | 1.71 | % |

| | | | | | | | | | | | | | |

| | Financials – 7.28% | | | | | | | | | | | | |

| | American International Group, Inc. (a) | | | 13,600 | | | | 423,640 | | | | 1.29 | % |

| | Banco Macro SA – ADR (b) | | | 16,300 | | | | 602,937 | | | | 1.84 | % |

| | Cardtronics, Inc. (a) | | | 39,800 | | | | 845,750 | | | | 2.58 | % |

| | Zions Bancorporation | | | 21,100 | | | | 515,895 | | | | 1.57 | % |

| | | | | | | | | 2,388,222 | | | | 7.28 | % |

| | Health Care – 6.77% | | | | | | | | | | | | |

| | Hill-Rom Holdings, Inc. | | | 16,100 | | | | 724,661 | | | | 2.21 | % |

| | SXC Health Solutions Corp. (a)(b) | | | 13,700 | | | | 755,692 | | | | 2.30 | % |

| | Universal American Corp. | | | 32,100 | | | | 741,510 | | | | 2.26 | % |

| | | | | | | | | 2,221,863 | | | | 6.77 | % |

| | Industrials – 39.04% | | | | | | | | | | | | |

| | Air Transport Services Group, Inc. (a) | | | 96,100 | | | | 786,098 | | | | 2.39 | % |

| | Alamo Group, Inc. | | | 22,300 | | | | 638,003 | | | | 1.94 | % |

| | Alaska Air Group, Inc. (a) | | | 10,600 | | | | 698,222 | | | | 2.13 | % |

| | Cascade Corp. | | | 12,800 | | | | 586,240 | | | | 1.79 | % |

| | Commercial Vehicle Group, Inc. (a) | | | 43,000 | | | | 742,180 | | | | 2.26 | % |

| | Consolidated Graphics, Inc. (a) | | | 10,800 | | | | 606,420 | | | | 1.85 | % |

The accompanying notes are an integral part of these financial statements.

HENNESSY FUNDS 1-800-966-4354

| | COMMON STOCKS | | Number | | | | | | % of Net | |

| | | | of Shares | | | Value | | | Assets | |

| | Industrials (Continued) | | | | | | | | | |

| | Esterline Technologies Corp. (a) | | | 9,900 | | | $ | 710,820 | | | | 2.17 | % |

| | Gardner Denver, Inc. | | | 10,300 | | | | 890,023 | | | | 2.71 | % |

| | Interface, Inc. | | | 41,500 | | | | 773,560 | | | | 2.36 | % |

| | Macquarie Infrastructure Co. LLC (a) | | | 36,100 | | | | 906,110 | | | | 2.76 | % |

| | Meritor, Inc. (a) | | | 33,600 | | | | 578,256 | | | | 1.76 | % |

| | NACCO Industries, Inc. | | | 5,200 | | | | 547,196 | | | | 1.67 | % |

| | Owens Corning (a) | | | 15,600 | | | | 590,304 | | | | 1.80 | % |

| | Pacer International, Inc. (a) | | | 70,000 | | | | 419,300 | | | | 1.28 | % |

| | Standex International Corp. | | | 18,900 | | | | 690,984 | | | | 2.11 | % |

| | Tennant Co. | | | 14,600 | | | | 598,892 | | | | 1.82 | % |

| | Trimas Corp. (a) | | | 43,000 | | | | 998,030 | | | | 3.04 | % |

| | United Continental Holdings, Inc. (a) | | | 24,100 | | | | 549,962 | | | | 1.68 | % |

| | US Airways Group, Inc. (a) | | | 55,000 | | | | 499,950 | | | | 1.52 | % |

| | | | | | | | | 12,810,550 | | | | 39.04 | % |

| | Information Technology – 7.30% | | | | | | | | | | | | |

| | Lionbridge Technologies, Inc. (a) | | | 100,100 | | | | 337,337 | | | | 1.03 | % |

| | Loral Space & Communications, Inc. (a) | | | 12,100 | | | | 845,790 | | | | 2.58 | % |

| | Power One, Inc. (a) | | | 67,700 | | | | 559,202 | | | | 1.70 | % |

| | Ultra Clean Holdings, Inc. (a) | | | 56,800 | | | | 652,632 | | | | 1.99 | % |

| | | | | | | | | 2,394,961 | | | | 7.30 | % |

| | Materials – 6.24% | | | | | | | | | | | | |

| | Clearwater Paper Corp. (a) | | | 8,500 | | | | 667,080 | | | | 2.03 | % |

| | Neenah Paper, Inc. | | | 25,800 | | | | 601,914 | | | | 1.83 | % |

| | Quaker Chem Corp. | | | 17,300 | | | | 781,614 | | | | 2.38 | % |

| | | | | | | | | 2,050,608 | | | | 6.24 | % |

| | Telecommunication Services – 4.54% | | | | | | | | | | | | |

| | IDT Corp. | | | 51,400 | | | | 1,490,086 | | | | 4.54 | % |

| | | | | | | | | | | | | | |

| | Total Common Stocks (Cost $23,162,513) | | | | | | | 31,408,736 | | | | 95.71 | % |

| | | | | | | | | | | | | | |

| | WARRANTS – 0.00% | | | | | | | | | | | | |

| | American International Group, Inc.(a) | | | | | | | | | | | | |

| | Expiration: January, 2021, Exercise Price: $45.00 | | | 0.004 | | | | 0 | | | | 0.00 | % |

| | | | | | | | | | | | | | |

| | Total Warrants (Cost $0) | | | | | | | 0 | | | | 0.00 | % |

The accompanying notes are an integral part of these financial statements.

SCHEDULE OF INVESTMENTS — HENNESSY CORNERSTONE GROWTH FUND, SERIES II

| | SHORT-TERM INVESTMENTS – 4.52% | | Principal | | | | | | % of Net | |

| | | | Value | | | Value | | | Assets | |

| | Demand Notes# – 4.52% | | | | | | | | | |

| | American Family Financial Services, 0.1001% | | $ | 1,484,155 | | | $ | 1,484,155 | | | | 4.52 | % |

| | | | | | | | | | | | | | |

| | Total Demand Notes | | | | | | | | | | | | |

| | (Cost $1,484,155) | | | | | | | 1,484,155 | | | | 4.52 | % |

| | | | | | | | | | | | | | |

| | Total Short-Term Investments | | | | | | | | | | | | |

| | (Cost $1,484,155) | | | | | | | 1,484,155 | | | | 4.52 | % |

| | | | | | | | | | | | | | |

| | Total Investments – 100.23% | | | | | | | | | | | | |

| | (Cost $24,646,668) | | | | | | | 32,892,891 | | | | 100.23 | % |

| | | | | | | | | | | | | | |

| | Liabilities in Excess of Other Assets – (0.23)% | | | | | | | (75,117 | ) | | | (0.23 | )% |

| | TOTAL NET ASSETS – 100.00% | | | | | | $ | 32,817,774 | | | | 100.00 | % |

Percentages are stated as a percent of net assets.

ADR American Depository Receipt

(a) Non-income producing security.

(b) Foreign issued security.

# Variable rate demand notes are considered short-term obligations and are payable on demand. Interest rates change periodically on specified dates. Interest rates listed are as of April 30, 2011.

Summary of Fair Value Exposure at April 30, 2011

The Fund has adopted authoritative fair valuation accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion in changes in valuation techniques and related inputs during the period. These inputs are summarized in the three broad levels listed below.

Securities which are traded on a national or recognized stock exchange are valued at the last sale price on the securities exchange on which such securities are primarily traded. Exchange-traded securities for which there were no transactions that day and debt securities are valued at the most recent bid prices. Instruments with a remaining maturity of 60 days or less are valued on an amortized cost basis. When a price for an underlying security is not readily available or if a significant event has occurred that indicates the closing price of a security no longer represents the true value of that security, fair value pricing procedures have been adopted by the Board of Directors of the Funds. Fair value pricing determinations are made in good faith in accordance with these procedures. There are numerous criteria that will be given consideration in determining a fair value of a security. Some of these criteria are: trading volume of security and markets, value of other like securities and news events with direct bearing to security or market. Fair value pricing results in an estimated price that reasonably reflects the current market conditions in order to rate the portfolio holdings such that shareholder transactions receive a fair net asset value.

The Fund has performed an analysis of all existing investments to determine the significance and character of all inputs to their fair value determination.

The accompanying notes are an integral part of these financial statements.

HENNESSY FUNDS 1-800-966-4354

| | Level 1 – | Quoted unadjusted prices for identical instruments in active markets to which the Fund has access at the date of measurement. |

| | Level 2 – | Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets. Level 2 inputs are those in markets for which there are few transactions, the prices are not current, little public information exists or instances where prices vary substantially over time or among brokered market makers. |

| | Level 3 – | Model derived valuations in which one or more significant inputs or significant value drivers are unobservable. Unobservable inputs are those inputs that reflect the Fund’s own assumptions that market participants would use to price the asset or liability based on the best available information. |

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s net assets as of April 30, 2011:

| | Common Stock | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | Consumer Discretionary | | $ | 7,490,746 | | | $ | — | | | $ | — | | | $ | 7,490,746 | |

| | Energy | | | 561,700 | | | | — | | | | — | | | | 561,700 | |

| | Financials | | | 2,388,222 | | | | — | | | | — | | | | 2,388,222 | |

| | Health Care | | | 2,221,863 | | | | — | | | | — | | | | 2,221,863 | |

| | Industrials | | | 12,810,550 | | | | — | | | | — | | | | 12,810,550 | |

| | Information Technology | | | 2,394,961 | | | | — | | | | — | | | | 2,394,961 | |

| | Materials | | | 2,050,608 | | | | — | | | | — | | | | 2,050,608 | |

| | Telecommunication Services | | | 1,490,086 | | | | — | | | | — | | | | 1,490,086 | |

| | Total Common Stock | | $ | 31,408,736 | | | $ | — | | | $ | — | | | $ | 31,408,736 | |

| | Warrants | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| | Short-Term Investments | | $ | — | | | $ | 1,484,155 | | | $ | — | | | $ | 1,484,155 | |

| | Total Investments in Securities | | $ | 31,408,736 | | | $ | 1,484,155 | | | $ | — | | | $ | 32,892,891 | |

Transfers between levels are recognized at the end of the reporting period. During the period ended April 30, 2011, the Fund recognized no significant transfers between levels.

The accompanying notes are an integral part of these financial statements.

SCHEDULE OF INVESTMENTS — HENNESSY FOCUS 30 FUND

HENNESSY FOCUS 30 FUND

As of April 30, 2011 (Unaudited)

(% of Net Assets)

| TOP TEN EQUITY HOLDINGS | % of net assets |

| Ulta Salon Cosmetics & Fragrance, Inc. | 4.82% |

| Rockwood Holdings, Inc. | 4.59% |

| Healthspring, Inc. | 4.54% |

| Amerigroup Corp. | 4.48% |

| Crocs, Inc. | 4.38% |

| Tenneco, Inc. | 4.21% |

| Tractor Supply Co. | 4.09% |

| Borg Warner, Inc. | 4.08% |

| Complete Production Services Co. | 4.01% |

| TRW Automotive Holdings Corp. | 4.00% |

HENNESSY FUNDS 1-800-966-4354

| | COMMON STOCKS – 98.97% | | Number | | | | | | % of Net | |

| | | | of Shares | | | Value | | | Assets | |

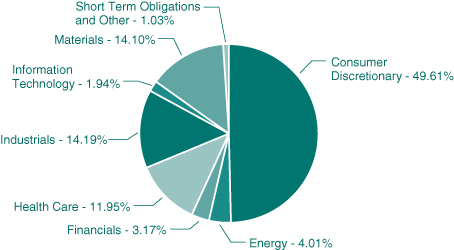

| | Consumer Discretionary – 49.61% | | | | | | | | | |

| | Advance Auto Parts, Inc. | | | 71,400 | | | $ | 4,673,844 | | | | 2.83 | % |

| | Autoliv, Inc. | | | 68,400 | | | | 5,480,892 | | | | 3.32 | % |

| | Borg Warner, Inc. (a) | | | 87,300 | | | | 6,743,052 | | | | 4.08 | % |

| | Crocs, Inc. (a) | | | 359,800 | | | | 7,235,578 | | | | 4.38 | % |

| | Dollar Tree, Inc. (a) | | | 87,200 | | | | 5,014,000 | | | | 3.04 | % |

| | Family Dollar Stores, Inc. | | | 96,100 | | | | 5,209,581 | | | | 3.16 | % |

| | HSN, Inc. (a) | | | 138,000 | | | | 4,578,840 | | | | 2.77 | % |

| | Tenneco, Inc. (a) | | | 150,600 | | | | 6,959,226 | | | | 4.21 | % |

| | Tractor Supply Co. | | | 109,200 | | | | 6,756,204 | | | | 4.09 | % |

| | TRW Automotive Holdings Corp. (a) | | | 115,900 | | | | 6,613,254 | | | | 4.00 | % |

| | Ulta Salon Cosmetics & Fragrance, Inc. (a) | | | 149,600 | | | | 7,957,224 | | | | 4.82 | % |

| | Valassis Communications, Inc. (a) | | | 124,800 | | | | 3,597,984 | | | | 2.18 | % |

| | Williams Sonoma, Inc. | | | 135,200 | | | | 5,869,032 | | | | 3.55 | % |

| | Wyndham Worldwide Corp. | | | 151,600 | | | | 5,246,876 | | | | 3.18 | % |

| | | | | | | | | 81,935,587 | | | | 49.61 | % |

| | Energy – 4.01% | | | | | | | | | | | | |

| | Complete Production Services Co. (a) | | | 195,100 | | | | 6,621,694 | | | | 4.01 | % |

| | | | | | | | | | | | | | |

| | Financials – 3.17% | | | | | | | | | | | | |

| | Jones Lang Lasalle, Inc. | | | 51,200 | | | | 5,241,856 | | | | 3.17 | % |

| | | | | | | | | | | | | | |

| | Health Care – 11.95% | | | | | | | | | | | | |

| | Amerigroup Corp. (a) | | | 108,200 | | | | 7,390,060 | | | | 4.48 | % |

| | Healthspring, Inc. (a) | | | 180,900 | | | | 7,505,541 | | | | 4.54 | % |

| | Magellan Health Services, Inc. (a) | | | 93,000 | | | | 4,837,860 | | | | 2.93 | % |

| | | | | | | | | 19,733,461 | | | | 11.95 | % |

| | Industrials – 14.19% | | | | | | | | | | | | |

| | Applied Industrial Technologies, Inc. | | | 140,300 | | | | 4,946,978 | | | | 3.00 | % |

| | Meritor, Inc. (a) | | | 288,500 | | | | 4,965,085 | | | | 3.01 | % |

| | Toro Co. | | | 74,400 | | | | 5,052,504 | | | | 3.06 | % |

| | United Continental Holdings, Inc. (a) | | | 188,400 | | | | 4,299,288 | | | | 2.60 | % |

| | US Airways Group, Inc. (a) | | | 458,600 | | | | 4,168,674 | | | | 2.52 | % |

| | | | | | | | | 23,432,529 | | | | 14.19 | % |

| | Information Technology – 1.94% | | | | | | | | | | | | |

| | Lexmark International (a) | | | 99,400 | | | | 3,205,650 | | | | 1.94 | % |

The accompanying notes are an integral part of these financial statements.

SCHEDULE OF INVESTMENTS — HENNESSY FOCUS 30 FUND

| | COMMON STOCKS | | Number | | | | | | % of Net | |

| | | | of Shares | | | Value | | | Assets | |

| | Materials – 14.10% | | | | | | | | | |

| | Ferro Corp. (a) | | | 336,000 | | | $ | 5,040,000 | | | | 3.05 | % |

| | Lubrizol Corp. | | | 39,400 | | | | 5,300,088 | | | | 3.21 | % |

| | Polyone Corp. | | | 370,500 | | | | 5,364,840 | | | | 3.25 | % |

| | Rockwood Holdings, Inc. (a) | | | 133,500 | | | | 7,574,790 | | | | 4.59 | % |

| | | | | | | | | 23,279,718 | | | | 14.10 | % |

| | | | | | | | | | | | | | |

| | Total Common Stocks (Cost $120,199,778) | | | | | | | 163,450,495 | | | | 98.97 | % |

| | | | | | | | | | | | | | |

| | SHORT-TERM INVESTMENTS – 1.18% | | | | | | | | | | | | |

| | Money Market Funds – 1.18% | | | | | | | | | | | | |

| | Fidelity Government Portfolio – | | | | | | | | | | | | |

| | Institutional Class, 0.0100% (b) | | | 1,951,280 | | | | 1,951,280 | | | | 1.18 | % |

| | | | | | | | | | | | | | |

| | Total Money Market Funds | | | | | | | | | | | | |

| | (Cost $1,951,280) | | | | | | | 1,951,280 | | | | 1.18 | % |

| | | | | | | | | | | | | | |

| | Total Short-Term Investments | | | | | | | | | | | | |

| | (Cost $1,951,280) | | | | | | | 1,951,280 | | | | 1.18 | % |

| | | | | | | | | | | | | | |

| | Total Investments – 100.15% | | | | | | | | | | | | |

| | (Cost $122,151,058) | | | | | | | 165,401,775 | | | | 100.15 | % |

| | | | | | | | | | | | | | |

| | Liabilities in Excess of Other Assets – (0.15)% | | | | | | | (255,596 | ) | | | (0.15 | )% |

| | TOTAL NET ASSETS – 100.00% | | | | | | $ | 165,146,179 | | | | 100.00 | % |

Percentages are stated as a percent of net assets.

(a)Non-income producing security.

(b)The rate listed is the Fund’s 7-day yield as of April 30, 2011.

Summary of Fair Value Exposure at April 30, 2011

The Fund has adopted authoritative fair valuation accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion in changes in valuation techniques and related inputs during the period. These inputs are summarized in the three broad levels listed below.

Securities which are traded on a national or recognized stock exchange are valued at the last sale price on the securities exchange on which such securities are primarily traded. Exchange-traded securities for which there were no transactions that day and debt securities are valued at the most recent bid prices. Instruments with a remaining maturity of 60 days or less are valued on an amortized cost basis. When a price for an underlying security is not

The accompanying notes are an integral part of these financial statements.

HENNESSY FUNDS 1-800-966-4354

readily available or if a significant event has occurred that indicates the closing price of a security no longer represents the true value of that security, fair value pricing procedures have been adopted by the Board of Directors of the Funds. Fair value pricing determinations are made in good faith in accordance with these procedures. There are numerous criteria that will be given consideration in determining a fair value of a security. Some of these criteria are: trading volume of security and markets, value of other like securities and news events with direct bearing to security or market. Fair value pricing results in an estimated price that reasonably reflects the current market conditions in order to rate the portfolio holdings such that shareholder transactions receive a fair net asset value.

The Fund has performed an analysis of all existing investments to determine the significance and character of all inputs to their fair value determination.

| | Level 1 – | Quoted unadjusted prices for identical instruments in active markets to which the Fund has access at the date of measurement. |

| | Level 2 – | Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets. Level 2 inputs are those in markets for which there are few transactions, the prices are not current, little public information exists or instances where prices vary substantially over time or among brokered market makers. |

| | Level 3 – | Model derived valuations in which one or more significant inputs or significant value drivers are unobservable. Unobservable inputs are those inputs that reflect the Fund’s own assumptions that market participants would use to price the asset or liability based on the best available information. |

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s net assets as of April 30, 2011:

| | Common Stock | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | Consumer Discretionary | | $ | 81,935,587 | | | $ | — | | | $ | — | | | $ | 81,935,587 | |

| | Energy | | | 6,621,694 | | | | — | | | | — | | | | 6,621,694 | |

| | Financials | | | 5,241,856 | | | | — | | | | — | | | | 5,241,856 | |

| | Health Care | | | 19,733,461 | | | | — | | | | — | | | | 19,733,461 | |

| | Industrials | | | 23,432,529 | | | | — | | | | — | | | | 23,432,529 | |

| | Information Technology | | | 3,205,650 | | | | — | | | | — | | | | 3,205,650 | |

| | Materials | | | 23,279,718 | | | | — | | | | — | | | | 23,279,718 | |

| | Total Common Stock | | $ | 163,450,495 | | | $ | — | | | $ | — | | | $ | 163,450,495 | |

| | Short-Term Investments | | $ | 1,951,280 | | | $ | — | | | $ | — | | | $ | 1,951,280 | |

| | Total Investments in Securities | | $ | 165,401,775 | | | $ | — | | | $ | — | | | $ | 165,401,775 | |

Transfers between levels are recognized at the end of the reporting period. During the period ended April 30, 2011, the Fund recognized no significant transfers between levels.

The accompanying notes are an integral part of these financial statements.

SCHEDULE OF INVESTMENTS — HENNESSY FOCUS 30 FUND

Level 3 Reconciliation Disclosure

Following is a reconciliation of Level 3 assets for which significant unobservable inputs were used to determine fair value.

| | | | Warrants(1) | |

| | Balance as of 10/31/10 | | $ | — | |

| | Accrued discounts/premiums | | | — | |

| | Realized gain (loss) | | | — | |

| | Change in unrealized appreciation (depreciation) | | | — | |

| | Purchases | | | — | |

| | (Sales) | | | — | |

| | Transfer in and/or out of Level 3 | | | — | |

| | Balance as of 4/30/11 | | $ | — | |

| | Change in unrealized appreciation/depreciation during | | | | |

| | the period for level 3 investments held at April 30, 2011 | | $ | — | |

(1) The Lantronix, Inc. warrants held at October 31, 2010 expired in February, 2011.

The accompanying notes are an integral part of these financial statements.

HENNESSY FUNDS 1-800-966-4354

HENNESSY CORNERSTONE

LARGE GROWTH FUND

As of April 30, 2011 (Unaudited)

(% of Net Assets)

| | TOP TEN EQUITY HOLDINGS | % of net assets |

| | Humana, Inc. | 2.81% |

| | Liberty Global, Inc. | 2.73% |

| | Joy Global, Inc. | 2.69% |

| | Moody’s Corp. | 2.54% |

| | AutoZone, Inc. | 2.51% |

| | Lubrizol Corp. | 2.39% |

| | CIGNA Corp. | 2.33% |

| | Freeport-McMoRan Copper & Gold, Inc. | 2.32% |

| | Philip Morris International, Inc. | 2.31% |

| | Dollar Tree, Inc. | 2.27% |

SCHEDULE OF INVESTMENTS — HENNESSY CORNERSTONE LARGE GROWTH FUND

| | COMMON STOCKS – 97.64% | | Number | | | | | | % of | |

| | | | of Shares | | | Value | | | Net Assets | |

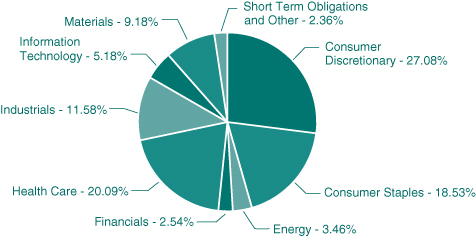

| | Consumer Discretionary – 27.08% | | | | | | | | | |

| | Apollo Group, Inc. (a) | | | 23,200 | | | $ | 928,696 | | | | 1.04 | % |

| | AutoZone, Inc. (a) | | | 7,900 | | | | 2,230,802 | | | | 2.51 | % |

| | Best Buy Co., Inc. | | | 30,800 | | | | 961,576 | | | | 1.08 | % |

| | DIRECTV (a) | | | 39,800 | | | | 1,933,882 | | | | 2.17 | % |

| | Dish Network Corp. (a) | | | 65,100 | | | | 1,630,104 | | | | 1.83 | % |

| | Dollar Tree, Inc. (a) | | | 35,100 | | | | 2,018,250 | | | | 2.27 | % |

| | Family Dollar Stores, Inc. | | | 36,500 | | | | 1,978,665 | | | | 2.23 | % |

| | Liberty Global, Inc. (a) | | | 52,300 | | | | 2,431,950 | | | | 2.73 | % |

| | Mattel, Inc. | | | 61,600 | | | | 1,645,952 | | | | 1.85 | % |

| | Ross Stores, Inc. | | | 25,100 | | | | 1,849,619 | | | | 2.08 | % |

| | The Gap, Inc. | | | 57,000 | | | | 1,324,680 | | | | 1.49 | % |

| | The McGraw-Hill Companies, Inc. | | | 42,600 | | | | 1,724,022 | | | | 1.94 | % |

| | TJX Companies, Inc. | | | 30,500 | | | | 1,635,410 | | | | 1.84 | % |

| | Yum Brands, Inc. | | | 33,500 | | | | 1,796,940 | | | | 2.02 | % |

| | | | | | | | | 24,090,548 | | | | 27.08 | % |

| | Consumer Staples – 18.53% | | | | | | | | | | | | |

| | Altria Group, Inc. | | | 68,500 | | | | 1,838,540 | | | | 2.07 | % |

| | Campbell Soup Co. | | | 40,800 | | | | 1,370,472 | | | | 1.54 | % |

| | Clorox Co. | | | 22,500 | | | | 1,567,350 | | | | 1.76 | % |

| | General Mills, Inc. | | | 41,300 | | | | 1,593,354 | | | | 1.79 | % |

| | H.J. Heinz Co. | | | 31,500 | | | | 1,613,745 | | | | 1.81 | % |

| | Kellogg Co. | | | 27,300 | | | | 1,563,471 | | | | 1.76 | % |

| | Kimberly – Clark Corp. | | | 23,600 | | | | 1,559,016 | | | | 1.75 | % |

| | Lorillard, Inc. | | | 18,500 | | | | 1,970,250 | | | | 2.22 | % |

| | Philip Morris International, Inc. | | | 29,600 | | | | 2,055,424 | | | | 2.31 | % |

| | Sysco Corp. | | | 46,800 | | | | 1,352,988 | | | | 1.52 | % |

| | | | | | | | | 16,484,610 | | | | 18.53 | % |

| | Energy – 3.46% | | | | | | | | | | | | |

| | Consol Energy, Inc. | | | 33,100 | | | | 1,790,379 | | | | 2.01 | % |

| | Diamond Offshore Drilling | | | 17,000 | | | | 1,289,790 | | | | 1.45 | % |

| | | | | | | | | 3,080,169 | | | | 3.46 | % |

| | Financials – 2.54% | | | | | | | | | | | | |

| | Moody’s Corp. | | | 57,700 | | | | 2,258,378 | | | | 2.54 | % |

The accompanying notes are an integral part of these financial statements.

HENNESSY FUNDS 1-800-966-4354

| | COMMON STOCKS | | Number | | | | | | % of | |

| | | | of Shares | | | Value | | | Net Assets | |

| | Health Care – 20.09% | | | | | | | | | |

| | Baxter International, Inc. | | | 30,200 | | | $ | 1,718,380 | | | | 1.93 | % |

| | Becton, Dickinson & Co. | | | 18,900 | | | | 1,624,266 | | | | 1.83 | % |

| | Bristol-Myers Squibb Co. | | | 59,200 | | | | 1,663,520 | | | | 1.87 | % |

| | Cardinal Health, Inc. | | | 40,200 | | | | 1,756,338 | | | | 1.97 | % |

| | CIGNA Corp. | | | 44,300 | | | | 2,074,569 | | | | 2.33 | % |

| | Eli Lilly & Co. | | | 41,100 | | | | 1,521,111 | | | | 1.71 | % |

| | Forest Laboratories, Inc. (a) | | | 53,000 | | | | 1,757,480 | | | | 1.98 | % |

| | Humana, Inc. (a) | | | 32,900 | | | | 2,504,348 | | | | 2.81 | % |

| | Johnson & Johnson | | | 22,300 | | | | 1,465,556 | | | | 1.65 | % |

| | Laboratory Corp. of America Holdings (a) | | | 18,500 | | | | 1,784,695 | | | | 2.01 | % |

| | | | | | | | | 17,870,263 | | | | 20.09 | % |

| | Industrials – 11.58% | | | | | | | | | | | | |

| | Flowserve Corp. | | | 12,400 | | | | 1,570,088 | | | | 1.77 | % |

| | Fluor Corp. | | | 27,400 | | | | 1,916,356 | | | | 2.15 | % |

| | Honeywell International, Inc. | | | 30,500 | | | | 1,867,515 | | | | 2.10 | % |

| | Joy Global, Inc. | | | 23,700 | | | | 2,392,515 | | | | 2.69 | % |

| | Lockheed Martin Corp. | | | 17,000 | | | | 1,347,250 | | | | 1.51 | % |

| | Raytheon Co. | | | 24,900 | | | | 1,208,895 | | | | 1.36 | % |

| | | | | | | | | 10,302,619 | | | | 11.58 | % |

| | Information Technology – 5.18% | | | | | | | | | | | | |

| | International Business Machines Corp. | | | 11,100 | | | | 1,893,438 | | | | 2.13 | % |

| | SAIC, Inc. (a) | | | 79,600 | | | | 1,385,040 | | | | 1.55 | % |

| | Western Digital Corp. (a) | | | 33,500 | | | | 1,333,300 | | | | 1.50 | % |

| | | | | | | | | 4,611,778 | | | | 5.18 | % |

| | Materials – 9.18% | | | | | | | | | | | | |

| | Crown Holdings, Inc. (a) | | | 53,200 | | | | 1,989,680 | | | | 2.24 | % |

| | FMC Corp. | | | 22,500 | | | | 1,986,300 | | | | 2.23 | % |

| | Freeport-McMoRan Copper & Gold, Inc. | | | 37,600 | | | | 2,069,128 | | | | 2.32 | % |

| | Lubrizol Corp. | | | 15,800 | | | | 2,125,416 | | | | 2.39 | % |

| | | | | | | | | 8,170,524 | | | | 9.18 | % |

| | | | | | | | | | | | | | |

| | Total Common Stocks (Cost $65,740,257) | | | | | | | 86,868,889 | | | | 97.64 | % |

The accompanying notes are an integral part of these financial statements.

SCHEDULE OF INVESTMENTS — HENNESSY CORNERSTONE LARGE GROWTH FUND

| | SHORT-TERM INVESTMENTS – 2.42% | | Number | | | | | | % of | |

| | | | of Shares | | | Value | | | Net Assets | |

| | Money Market Funds – 2.42% | | | | | | | | | |

| | Fidelity Government Portfolio – | | | | | | | | | |

| | Institutional Class, 0.0100% (b) | | | 2,152,938 | | | $ | 2,152,938 | | | | 2.42 | % |

| | | | | | | | | | | | | | |

| | Total Short-Term Investments | | | | | | | | | | | | |

| | (Cost $2,152,938) | | | | | | | 2,152,938 | | | | 2.42 | % |

| | | | | | | | | | | | | | |

| | Total Investments – 100.06% | | | | | | | | | | | | |

| | (Cost $67,893,195) | | | | | | | 89,021,827 | | | | 100.06 | % |

| | | | | | | | | | | | | | |

| | Liabilities in Excess of Other Assets – (0.06)% | | | | | | | (52,945 | ) | | | (0.06 | )% |

| | TOTAL NET ASSETS – 100.00% | | | | | | $ | 88,968,882 | | | | 100.00 | % |

Percentages are stated as a percent of net assets.

(a)Non-income producing security.

(b)The rate listed is the Fund’s 7-day yield as of April 30, 2011.

Summary of Fair Value Exposure at April 30, 2011

The Fund has adopted authoritative fair valuation accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion in changes in valuation techniques and related inputs during the period.