UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-07123 |

| |

| Advantage Funds, Inc. | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Bennett A. MacDougall, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6400 |

| |

Date of fiscal year end: | 08/31 | |

Date of reporting period: | 08/31/17 | |

| | | | | | | |

The following N-CSR relates only to the Registrant's series listed below and does not relate to any series of the Registrant with a different fiscal year end and, therefore, different N-CSR reporting requirements. A separate N-CSR will be filed for any series with a different fiscal year end, as appropriate.

Dreyfus Opportunistic Midcap Value Fund

Dreyfus Opportunistic Small Cap Fund

Dreyfus Strategic Value Fund

Dreyfus Structured Midcap Fund

Dreyfus Technology Growth Fund

FORM N-CSR

Item 1. Reports to Stockholders.

Dreyfus Opportunistic Midcap Value Fund

| | | |

| | ANNUAL REPORT

August 31, 2017 |

| |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes. |

| |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund. |

| |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

FOR MORE INFORMATION

Back Cover

| | | | |

| |

Dreyfus Opportunistic Midcap Value Fund

| | The Fund |

A LETTER FROM THE CEO OF DREYFUS

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Opportunistic Midcap Value Fund, covering the 12-month period from September 1, 2016 through August 31, 2017. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

Stocks set a series of new record highs and bonds produced mixed results over the past year in response to changing economic and political conditions. Financial markets during the final months of 2016 were dominated by the election of a new U.S. presidential administration. Equities surged higher in anticipation of more business-friendly regulatory, tax, and fiscal policies, but high-quality bonds generally lost value due to expectations of rising interest rates and accelerating inflation in a stronger economy. Despite a series of short-term interest-rate hikes, bonds recovered over the first eight months of 2017 when it became clearer that major tax and fiscal reforms would take time and political capital to enact. Stocks continued to rally, led by large growth-oriented companies, as corporate earnings grew and global economic conditions improved.

The markets’ recent strong performance has been supported by solid underlying fundamentals. While we currently expect these favorable conditions to persist, we remain watchful for economic and political developments that could derail the rallies. As always, we encourage you to discuss the risks and opportunities of today’s investment environment with your financial advisor.

Thank you for your continued confidence and support.

Sincerely,

Mark D. Santero

Chief Executive Officer

The Dreyfus Corporation

September 15, 2017

2

DISCUSSION OF FUND PERFORMANCE

For the period from September 1, 2016 through August 31, 2017, as provided by David A. Daglio, James Boyd, and Dale Dutile, Primary Portfolio Managers

Market and Fund Performance Overview

For the 12-month period ended August 31, 2017, Dreyfus Opportunistic Midcap Value Fund’s Class A shares produced a total return of 13.28%, Class C shares returned 12.44%, Class I shares returned 13.63%, and Class Y shares returned 13.71%.1 In comparison, the fund’s benchmark, the Russell Midcap® Value Index (the “Index”), produced a 10.82% total return for the same period.2

Stocks gained ground amid better-than-expected corporate earnings, improving economic prospects, and positive investor sentiment in the wake of the U.S. presidential election. Our security selection and sector allocation strategies in the financials, energy, real estate, and information technology sectors enabled the fund to outperform its benchmark.

The Fund’s Investment Approach

The fund seeks to surpass the performance of the Index by investing in mid-cap companies with market capitalizations between $1 billion and $25 billion at the time of purchase. The fund’s portfolio managers identify potential investments through extensive fundamental and quantitative research. The fund focuses on individual stock selection (a “bottom-up” approach), emphasizing three key factors: relative value, business health, and business momentum.

The fund’s portfolio managers use an opportunistic value approach to identify stocks whose current market prices trade at a large discount to their intrinsic value, as calculated by the portfolio managers. The opportunistic value style attempts to benefit from valuation inefficiencies and underappreciated fundamental prospects present in the marketplace. The portfolio managers use mid-cycle estimates, growth prospects, the identification of a revaluation catalyst and competitive advantages as some of the factors in the valuation assessment.

Rising Corporate Earnings Drove Markets Higher

While political uncertainties caused U.S. stocks to dip in the weeks before the 2016 presidential election, equity markets were reenergized in November and December when investors began to anticipate lower corporate taxes, reduced regulatory constraints on business, and increased infrastructure spending from a new presidential administration.

The market’s advance slowed in the spring when it became clearer that tax and fiscal reforms were far from certain, but the rally soon resumed in the midst of strong corporate earnings and encouraging economic data. However, market leadership shifted in the spring from smaller, value-oriented stocks to larger, more growth-oriented industry leaders. In this environment, mid-cap stocks generally produced lower returns than large-cap stocks, and value-oriented stocks lagged growth stocks for the reporting period overall.

Selection and Allocation Strategies Buoyed Fund Results

The fund outperformed the Index over the reporting period due in part to the success of our security selection strategy. In the financials sector, brokerage firms E*TRADE Financial, TD Ameritrade Holdings, and Raymond James Financial advanced after gaining market share. Student loans provider SLM benefited from higher origination volumes. Diversified financial company Leucadia National saw the start of cyclical earning recoveries in its Jefferies investment banking unit and its National Beef segment. Among banks, KeyCorp gained value in anticipation

3

DISCUSSION OF FUND PERFORMANCE (continued)

of a more business-friendly regulatory environment. In the information technology sector, favorable stock selections included commerce-enabling technology provider First Data, where a new management team boosted earnings. Semiconductor equipment maker Teradyne encountered rising demand for testing equipment and new “cobot” products, and Lam Research achieved strong order volumes. Electronic design and test solutions company Keysight Technologies received an acquisition offer at a premium to its stock price at the time.

The fund’s sector allocation strategy proved especially effective in the energy sector, as underweighted exposure to the lagging industry group bolstered relative results. Favorable stock selections—such as refiner Andeavor (formerly Tesoro)—also added value, enabling the fund to produce positive absolute returns in a market segment that weighed on the Index. Underweighted exposure to the real estate sector also helped cushion the impact of a relatively weak industry group.

Disappointments during the reporting period included the industrials sector, as car rental agency Hertz Global Holdings was hurt by declining used car prices, and distributor HD Supply Holdings encountered order handling difficulties. In the consumer discretionary sector, retailer Bed Bath & Beyond failed to execute effectively on its turnaround strategy, and specialty retailers such as Williams-Sonoma struggled in a generally challenging environment for brick-and-mortar stores.

Focusing on Individual Mid-Cap Value Companies

We expect to continue to choose investments one company at a time, according to their individual strengths and future prospects. Nonetheless, it is worth noting that, absent unexpected geopolitical shocks, fundamentals currently appear strong for mid-cap value companies. We recently trimmed holdings in the financials, industrials, and consumer discretionary sectors, and we redeployed those assets to other opportunities among information technology, materials, and health care companies. As of the reporting period’s end, the fund held overweighted exposure to the information technology, financials, materials and health care sectors, but we have identified relatively few opportunities in the energy, utilities, telecommunication services, and consumer discretionary sectors.

September 15, 2017

1 Total return includes reinvestment of dividends and any capital gains paid and does not take into consideration the maximum initial sales charge in the case of Class A shares, or the applicable contingent deferred sales charge imposed on redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: Lipper Inc. — The Russell Midcap® Value Index measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies that are considered more value-oriented relative to the overall market as defined by Russell’s leading style methodology. The Russell Midcap® Value Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap value market. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap value market. Investors cannot invest directly in any index.

Please note: the position in any security highlighted with italicized typeface was sold during the reporting period.

Stocks of small- and/or mid-cap companies often experience sharper price fluctuations than stocks of large-cap companies.

4

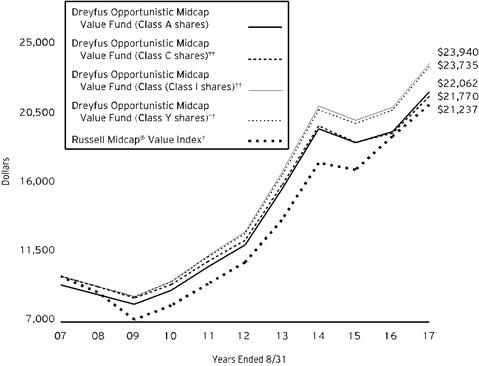

FUND PERFORMANCE

Comparison of change in value of $10,000 investment in Dreyfus Opportunistic Midcap Value Fund Class A shares, Class C shares, Class I shares and Class Y shares and the Russell Midcap® Value Index (the “Index”)

† Source: Lipper Inc.

†† The total return figures presented for Class C shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 5/30/08 (the inception date for Class C shares), not reflecting the applicable sales charges for Class A shares.

The total return figures presented for Class I shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 5/30/08 (the inception date for Class I shares), not reflecting the applicable sales charges for Class A shares.

The total return figures presented for Class Y shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 7/1/13 (the inception date for Class Y shares), not reflecting the applicable sales charges for Class A shares.

Past performance is not predictive of future performance.

The above graph compares a $10,000 investment made in each of the Class A, Class C, Class I and Class Y shares of Dreyfus Opportunistic Midcap Value Fund on 8/31/07 to a $10,000 investment made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses on all classes. The Index measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies that are considered more value-oriented relative to the overall market as defined by Russell’s leading style methodology. The Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap value market. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap value market. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

5

FUND PERFORMANCE (continued)

| | | | | | | | |

Average Annual Total Returns as of 8/31/17 | | | |

| | Inception

Date | 1 Year | 5 Years | | 10 Years | |

Class A shares | | | | | | |

with maximum sales charge (5.75%) | 9/29/95 | 6.75% | 11.51% | | 8.23% | |

without sales charge | 9/29/95 | 13.28% | 12.84% | | 8.88% | |

Class C shares | | | | | | |

with applicable redemption charge † | 5/30/08 | 11.44% | 12.00% | | 8.09%†† | |

without redemption | 5/30/08 | 12.44% | 12.00% | | 8.09%†† | |

Class I shares | | 5/30/08 | 13.63% | 13.12% | | 9.12%†† | |

Class Y shares | | 7/1/13 | 13.71% | 13.16%†† | | 9.03%†† | |

Russell Midcap® Value Index | 10.82% | 14.22% | | 7.82% | |

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

†† The total return performance figures presented for Class C shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 5/30/08 (the inception date for Class C shares), not reflecting the applicable sales charges for Class A shares.

The total return performance figures presented for Class I shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 5/30/08 (the inception date for Class I shares), not reflecting the applicable sales charges for Class A shares.

The total return performance figures presented for Class Y shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 7/1/13 (the inception date for Class Y shares), not reflecting the applicable sales charges for Class A shares.

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to Dreyfus.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In addition to the performance of Class A shares shown with and without a maximum sales charge, the fund’s performance shown in the table takes into account all other applicable fees and expenses on all classes.

6

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Opportunistic Midcap Value Fund from March 1, 2017 to August 31, 2017. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | | | | | | |

Expenses and Value of a $1,000 Investment | | |

assuming actual returns for the six months ended August 31, 2017 |

| | | | | | | | |

| | | | Class A | Class C | Class I | Class Y |

Expenses paid per $1,000† | | $5.82 | | $9.61 | | $4.47 | | $4.02 |

Ending value (after expenses) | | $989.30 | | $985.90 | | $990.70 | | $991.30 |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | | | | | | | |

Expenses and Value of a $1,000 Investment | | |

assuming a hypothetical 5% annualized return for the six months ended August 31, 2017 |

| | | | | | | | |

| | | | Class A | Class C | Class I | Class Y |

Expenses paid per $1,000† | | $5.90 | | $9.75 | | $4.53 | | $4.08 |

Ending value (after expenses) | | $1,019.36 | | $1,015.53 | | $1,020.72 | | $1,021.17 |

† Expenses are equal to the fund’s annualized expense ratio of 1.16% for Class A, 1.92% for Class C, .89% for Class I and .80% for Class Y, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

7

STATEMENT OF INVESTMENTS

August 31, 2017

| | | | | | | | |

| |

Description | | | | Shares | | Value ($) | |

Common Stocks - 99.2% | | | | | |

Automobiles & Components - .9% | | | | | |

Visteon | | | | 83,463 | a | 9,634,969 | |

Banks - 2.5% | | | | | |

Huntington Bancshares | | | | 926,641 | | 11,666,410 | |

KeyCorp | | | | 909,959 | | 15,660,394 | |

| | | | | 27,326,804 | |

Capital Goods - 3.4% | | | | | |

Hubbell | | | | 159,830 | | 18,027,226 | |

PACCAR | | | | 278,555 | | 18,476,553 | |

| | | | | 36,503,779 | |

Commercial & Professional Services - 1.4% | | | | | |

Nielsen Holdings | | | | 397,643 | | 15,448,431 | |

Consumer Services - .5% | | | | | |

Caesars Entertainment | | | | 442,583 | a | 5,133,963 | |

Diversified Financials - 23.7% | | | | | |

Capital One Financial | | | | 452,720 | | 36,041,039 | |

E*TRADE Financial | | | | 1,030,918 | a | 42,277,947 | |

Eaton Vance | | | | 199,682 | | 9,500,870 | |

Franklin Resources | | | | 480,732 | | 20,782,044 | |

Leucadia National | | | | 1,491,058 | | 35,308,253 | |

Raymond James Financial | | | | 330,773 | | 25,906,141 | |

SLM | | | | 3,519,972 | a | 35,798,115 | |

Synchrony Financial | | | | 951,149 | | 29,285,878 | |

TD Ameritrade Holding | | | | 506,512 | | 21,942,100 | |

| | | | | 256,842,387 | |

Energy - 3.6% | | | | | |

Andeavor | | | | 241,823 | | 24,218,573 | |

Cheniere Energy | | | | 337,603 | a | 14,446,032 | |

| | | | | 38,664,605 | |

Exchange-Traded Funds - .3% | | | | | |

SPDR S&P MidCap 400 ETF Trust | | | | 10,277 | | 3,243,216 | |

Food & Staples Retailing - 1.2% | | | | | |

US Foods Holding | | | | 472,091 | a | 12,958,898 | |

Food, Beverage & Tobacco - 3.3% | | | | | |

Archer-Daniels-Midland | | | | 865,054 | | 35,744,031 | |

Health Care Equipment & Services - 5.4% | | | | | |

Boston Scientific | | | | 381,157 | a | 10,500,875 | |

8

| | | | | | | | |

| |

Description | | | | Shares | | Value ($) | |

Common Stocks - 99.2% (continued) | | | | | |

Health Care Equipment & Services - 5.4% (continued) | | | | | |

Humana | | | | 69,424 | | 17,885,011 | |

Zimmer Biomet Holdings | | | | 266,980 | | 30,507,805 | |

| | | | | 58,893,691 | |

Insurance - 1.0% | | | | | |

Athene Holding, Cl. A | | | | 203,974 | | 10,914,649 | |

Materials - 12.0% | | | | | |

Freeport-McMoRan | | | | 2,013,723 | a | 29,762,826 | |

International Paper | | | | 581,930 | | 31,348,569 | |

Methanex | | | | 261,551 | | 13,365,256 | |

Newmont Mining | | | | 821,604 | | 31,500,297 | |

Westlake Chemical | | | | 315,610 | | 24,273,565 | |

| | | | | 130,250,513 | |

Media - 2.7% | | | | | |

CBS, Cl. B | | | | 48,388 | | 3,099,735 | |

Sinclair Broadcast Group, Cl. A | | | | 856,439 | | 25,907,280 | |

| | | | | 29,007,015 | |

Pharmaceuticals, Biotechnology & Life Sciences - 7.4% | | | | | |

Alexion Pharmaceuticals | | | | 267,661 | a | 38,117,603 | |

Jazz Pharmaceuticals | | | | 228,369 | a | 34,109,194 | |

Sage Therapeutics | | | | 96,180 | a | 7,910,805 | |

| | | | | 80,137,602 | |

Semiconductors & Semiconductor Equipment - 6.5% | | | | | |

Maxim Integrated Products | | | | 527,026 | | 24,591,033 | |

Microsemi | | | | 314,038 | a | 15,821,234 | |

Teradyne | | | | 749,320 | | 26,683,285 | |

United Microelectronics, ADR | | | | 1,576,067 | | 3,940,168 | |

| | | | | 71,035,720 | |

Software & Services - 10.8% | | | | | |

Broadridge Financial Solutions | | | | 117,920 | | 9,213,090 | |

DXC Technology | | | | 140,895 | | 11,976,075 | |

eBay | | | | 135,015 | a | 4,878,092 | |

First Data, Cl. A | | | | 2,216,477 | a | 40,805,342 | |

Nuance Communications | | | | 1,300,551 | a | 20,899,855 | |

Teradata | | | | 910,792 | a | 29,072,481 | |

| | | | | 116,844,935 | |

Technology Hardware & Equipment - 7.7% | | | | | |

Ciena | | | | 766,662 | a | 16,567,566 | |

Hewlett Packard Enterprise | | | | 870,684 | | 15,724,553 | |

9

STATEMENT OF INVESTMENTS (continued)

| | | | | | | | |

| |

Description | | | | Shares | | Value ($) | |

Common Stocks - 99.2% (continued) | | | | | |

Technology Hardware & Equipment - 7.7% (continued) | | | | | |

Viavi Solutions | | | | 1,937,008 | a | 19,447,560 | |

Xerox | | | | 637,085 | | 20,558,733 | |

Zebra Technologies, Cl. A | | | | 104,437 | a | 10,766,410 | |

| | | | | 83,064,822 | |

Transportation - 4.3% | | | | | |

J.B. Hunt Transport Services | | | | 124,227 | | 12,284,808 | |

Norfolk Southern | | | | 79,448 | | 9,575,073 | |

Swift Transportation | | | | 886,019 | a | 24,852,833 | |

| | | | | 46,712,714 | |

Utilities - .6% | | | | | |

Calpine | | | | 430,234 | a | 6,324,440 | |

Total Common Stocks (cost $908,108,980) | | | | 1,074,687,184 | |

| | | | | | | | |

Other Investment - .2% | | | | | |

Registered Investment Company; | | | | | |

Dreyfus Institutional Preferred Government Plus Money Market Fund

(cost $2,081,600) | | | | 2,081,600 | b | 2,081,600 | |

Total Investments (cost $910,190,580) | | 99.4% | | 1,076,768,784 | |

Cash and Receivables (Net) | | .6% | | 6,558,269 | |

Net Assets | | 100.0% | | 1,083,327,053 | |

ADR—American Depository Receipt

ETF—Exchange-Traded Fund

SPDR—Standard & Poor's Depository Receipt

aNon-income producing security.

bInvestment in affiliated money market mutual fund.

10

| | |

Portfolio Summary (Unaudited) † | Value (%) |

Diversified Financials | 23.7 |

Materials | 12.0 |

Software & Services | 10.8 |

Technology Hardware & Equipment | 7.7 |

Pharmaceuticals, Biotechnology & Life Sciences | 7.4 |

Semiconductors & Semiconductor Equipment | 6.5 |

Health Care Equipment & Services | 5.4 |

Transportation | 4.3 |

Energy | 3.6 |

Capital Goods | 3.4 |

Food, Beverage & Tobacco | 3.3 |

Media | 2.7 |

Banks | 2.5 |

Commercial & Professional Services | 1.4 |

Food & Staples Retailing | 1.2 |

Insurance | 1.0 |

Automobiles & Components | .9 |

Utilities | .6 |

Consumer Services | .5 |

Exchange-Traded Funds | .3 |

Money Market Investment | .2 |

| | 99.4 |

† Based on net assets.

See notes to financial statements.

11

STATEMENT OF INVESTMENTS IN AFFILIATED ISSUERS

| | | | | | | |

Registered Investment Companies | Value

8/31/2016 ($) | Purchases ($) | Sales ($) | Value

8/31/2017 ($) | Net

Assets (%) | Dividends/

Distributions ($) |

Dreyfus Institutional Cash

Advantage Fund,

Institutional Shares | 18,406,000 | 14,777,168 | 33,183,168 | - | - | - |

Dreyfus Institutional Preferred Government Plus Money Market Fund | 3,006,949 | 461,355,858 | 462,281,207 | 2,081,600 | .2 | 52,082 |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares | - | 162,939,590 | 162,939,590 | - | - | - |

Total | 21,412,949 | 639,072,616 | 658,403,965 | 2,081,600 | .2 | 52,082 |

See notes to financial statements.

12

STATEMENT OF ASSETS AND LIABILITIES

August 31, 2017

| | | | | | | |

| | | | | | |

| | | Cost | | Value | |

Assets ($): | | | | |

Investments in securities—See Statement of Investments: | | | | |

Unaffiliated issuers | | 908,108,980 | | 1,074,687,184 | |

Affiliated issuers | | 2,081,600 | | 2,081,600 | |

Cash | | | | | 142,582 | |

Receivable for investment securities sold | | | | | 14,973,938 | |

Dividends receivable | | | | | 1,554,307 | |

Receivable for shares of Common Stock subscribed | | | | | 172,506 | |

Prepaid expenses | | | | | 45,536 | |

| | | | | 1,093,657,653 | |

Liabilities ($): | | | | |

Due to The Dreyfus Corporation and affiliates—Note 3(c) | | | | | 902,193 | |

Payable for investment securities purchased | | | | | 6,638,452 | |

Payable for shares of Common Stock redeemed | | | | | 2,500,038 | |

Interest payable—Note 2 | | | | | 110 | |

Accrued expenses | | | | | 289,807 | |

| | | | | 10,330,600 | |

Net Assets ($) | | | 1,083,327,053 | |

Composition of Net Assets ($): | | | | |

Paid-in capital | | | | | 825,157,931 | |

Accumulated undistributed investment income—net | | | | | 2,115,370 | |

Accumulated net realized gain (loss) on investments | | | | | 89,475,548 | |

Accumulated net unrealized appreciation (depreciation)

on investments | | | | 166,578,204 | |

Net Assets ($) | | | 1,083,327,053 | |

| | | | | | |

Net Asset Value Per Share | Class A | Class C | Class I | Class Y | |

Net Assets ($) | 509,760,936 | 62,608,447 | 501,820,923 | 9,136,747 | |

Shares Outstanding | 14,831,161 | 2,039,450 | 14,644,657 | 266,077 | |

Net Asset Value Per Share ($) | 34.37 | 30.70 | 34.27 | 34.34 | |

| | | | | | |

See notes to financial statements. | | | | | |

13

STATEMENT OF OPERATIONS

Year Ended August 31, 2017

| | | | | | | |

| | | | | | |

| | | | | | |

Investment Income ($): | | | | |

Income: | | | | |

Cash dividends (net of $50,437 foreign taxes withheld at source): | | | | |

Unaffiliated issuers | | | 15,754,115 | |

Affiliated issuers | | | 52,082 | |

Income from securities lending—Note 1(b) | | | 40,802 | |

Total Income | | | 15,846,999 | |

Expenses: | | | | |

Management fee—Note 3(a) | | | 9,226,463 | |

Shareholder servicing costs—Note 3(c) | | | 3,372,924 | |

Distribution fees—Note 3(b) | | | 536,320 | |

Directors’ fees and expenses—Note 3(d) | | | 90,375 | |

Custodian fees—Note 3(c) | | | 87,234 | |

Registration fees | | | 85,360 | |

Professional fees | | | 81,854 | |

Prospectus and shareholders’ reports | | | 77,763 | |

Loan commitment fees—Note 2 | | | 35,460 | |

Interest expense—Note 2 | | | 10,663 | |

Miscellaneous | | | 33,008 | |

Total Expenses | | | 13,637,424 | |

Less—reduction in fees due to earnings credits—Note 3(c) | | | (8,455) | |

Net Expenses | | | 13,628,969 | |

Investment Income—Net | | | 2,218,030 | |

Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | | |

Net realized gain (loss) on investments | 135,298,858 | |

Net unrealized appreciation (depreciation) on investments | | | 31,898,736 | |

Net Realized and Unrealized Gain (Loss) on Investments | | | 167,197,594 | |

Net Increase in Net Assets Resulting from Operations | | 169,415,624 | |

| | | | | | | |

See notes to financial statements. | | | | | |

14

STATEMENT OF CHANGES IN NET ASSETS

| | | | | | | | | | |

| | | | Year Ended August 31, |

| | | | 2017 | | | | 2016 | |

Operations ($): | | | | | | | | |

Investment income—net | | | 2,218,030 | | | | 2,846,092 | |

Net realized gain (loss) on investments | | 135,298,858 | | | | 33,387,974 | |

Net unrealized appreciation (depreciation)

on investments | | 31,898,736 | | | | (9,528,738) | |

Net Increase (Decrease) in Net Assets

Resulting from Operations | 169,415,624 | | | | 26,705,328 | |

Distributions to Shareholders from ($): | | | | | | | | |

Investment income—net: | | | | | | | | |

Class A | | | (150,447) | | | | - | |

Class I | | | (1,718,638) | | | | (378,487) | |

Class Y | | | (41,145) | | | | (201,480) | |

Net realized gain on investments: | | | | | | | | |

Class A | | | (34,720,829) | | | | (163,514,213) | |

Class C | | | (3,672,816) | | | | (18,133,204) | |

Class I | | | (21,342,132) | | | | (95,819,995) | |

Class Y | | | (376,578) | | | | (12,858,708) | |

Total Distributions | | | (62,022,585) | | | | (290,906,087) | |

Capital Stock Transactions ($): | | | | | | | | |

Net proceeds from shares sold: | | | | | | | | |

Class A | | | 75,094,482 | | | | 144,471,285 | |

Class C | | | 6,613,135 | | | | 9,703,250 | |

Class I | | | 284,476,355 | | | | 141,009,615 | |

Class Y | | | 6,198,203 | | | | 9,901,433 | |

Distributions reinvested: | | | | | | | | |

Class A | | | 32,052,598 | | | | 148,969,232 | |

Class C | | | 3,049,663 | | | | 14,641,322 | |

Class I | | | 22,018,042 | | | | 88,032,264 | |

Class Y | | | 312,777 | | | | 12,714,335 | |

Cost of shares redeemed: | | | | | | | | |

Class A | | | (452,533,679) | | | | (424,844,330) | |

Class C | | | (28,803,314) | | | | (46,692,551) | |

Class I | | | (340,780,615) | | | | (562,111,303) | |

Class Y | | | (15,338,617) | | | | (69,663,961) | |

Increase (Decrease) in Net Assets

from Capital Stock Transactions | (407,640,970) | | | | (533,869,409) | |

Total Increase (Decrease) in Net Assets | (300,247,931) | | | | (798,070,168) | |

Net Assets ($): | | | | | | | | |

Beginning of Period | | | 1,383,574,984 | | | | 2,181,645,152 | |

End of Period | | | 1,083,327,053 | | | | 1,383,574,984 | |

Undistributed investment income—net | 2,115,370 | | | | 1,905,676 | |

15

STATEMENT OF CHANGES IN NET ASSETS (continued)

| | | | | | | | | | |

| | | | Year Ended August 31, |

| | | | 2017 | | | | 2016 | |

Capital Share Transactions (Shares): | | | | | | | | |

Class A | | | | | | | | |

Shares sold | | | 2,248,398 | | | | 4,722,794 | |

Shares issued for distributions reinvested | | | 966,313 | | | | 5,163,578 | |

Shares redeemed | | | (13,502,201) | | | | (13,754,633) | |

Net Increase (Decrease) in Shares Outstanding | (10,287,490) | | | | (3,868,261) | |

Class Ca | | | | | | | | |

Shares sold | | | 218,979 | | | | 346,788 | |

Shares issued for distributions reinvested | | | 102,372 | | | | 558,402 | |

Shares redeemed | | | (963,162) | | | | (1,629,615) | |

Net Increase (Decrease) in Shares Outstanding | (641,811) | | | | (724,425) | |

Class Ia | | | | | | | | |

Shares sold | | | 8,483,733 | | | | 4,618,348 | |

Shares issued for distributions reinvested | | | 667,011 | | | | 3,065,191 | |

Shares redeemedb | | | (10,075,991) | | | | (16,927,149) | |

Net Increase (Decrease) in Shares Outstanding | (925,247) | | | | (9,243,610) | |

Class Y | | | | | | | | |

Shares sold | | | 186,843 | | | | 335,763 | |

Shares issued for distributions reinvested | | | 9,464 | | | | 442,084 | |

Shares redeemed | | | (475,970) | | | | (2,381,985) | |

Net Increase (Decrease) in Shares Outstanding | (279,663) | | | | (1,604,138) | |

| | | | | | | | | | |

a | During the period ended August 31, 2017, 348 Class C shares representing $10,555 were exchanged for 313 Class I shares and during the period ended August 31, 2016, 164 Class C shares representing $5,387 were exchanged for 152 Class I shares. | |

b | During the period ended August 31, 2016, 6,020,293 shares amounting to $216,790,748 were redeemed-in-kind resulting in a net realized gain on investments of $10,278,766.

| |

See notes to financial statements. | | | | | | | | |

16

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated. All information (except portfolio turnover rate) reflects financial results for a single fund share. Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions. These figures have been derived from the fund’s financial statements.

| | | | | | | | | | | |

| | | | | | |

| | |

| | Year Ended August 31, |

Class A Shares | | 2017 | 2016 | 2015 | 2014 | 2013 |

Per Share Data ($): | | | | | | |

Net asset value, beginning of period | | 31.72 | 36.97 | 43.17 | 38.27 | 29.47 |

Investment Operations: | | | | | | |

Investment income (loss)—net a | | .03 | .03 | (.02) | .05 | .03 |

Net realized and unrealized gain

(loss) on investments | | 4.13 | .82 | (1.79) | 9.10 | 8.83 |

Total from Investment Operations | | 4.16 | .85 | (1.81) | 9.15 | 8.86 |

Distributions: | | | | | �� | |

Dividends from investment

income—net | | (.01) | - | (.05) | - | (.06) |

Dividends from net realized gain

on investments | | (1.50) | (6.10) | (4.34) | (4.25) | - |

Total Distributions | | (1.51) | (6.10) | (4.39) | (4.25) | (.06) |

Net asset value, end of period | | 34.37 | 31.72 | 36.97 | 43.17 | 38.27 |

Total Return (%)b | | 13.28 | 3.95 | (4.72) | 25.32 | 30.11 |

Ratios/Supplemental Data (%): | | | | | | |

Ratio of total expenses to

average net assets | | 1.17 | 1.21 | 1.18 | 1.15 | 1.18 |

Ratio of net expenses to

average net assets | | 1.17 | 1.21 | 1.18 | 1.15 | 1.18 |

Ratio of net investment income (loss)

to average net assets | | .10 | .11 | (.05) | .12 | .08 |

Portfolio Turnover Rate | | 104.51 | 101.68 | 74.05 | 67.49 | 91.31 |

Net Assets, end of period ($ x 1,000) | | 509,761 | 796,686 | 1,071,713 | 1,417,535 | 1,079,346 |

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

17

FINANCIAL HIGHLIGHTS (continued)

| | | | | | | | | |

| | | | | | |

| | |

| | Year Ended August 31, |

Class C Shares | | | 2017 | 2016 | 2015 | 2014 | 2013 |

Per Share Data ($): | | | | | | | |

Net asset value, beginning of period | | | 28.68 | 34.26 | 40.55 | 36.44 | 28.22 |

Investment Operations: | | | | | | | |

Investment (loss)—net a | | | (.19) | (.18) | (.29) | (.26) | (.24) |

Net realized and unrealized gain

(loss) on investments | | | 3.71 | .70 | (1.66) | 8.62 | 8.46 |

Total from Investment Operations | | | 3.52 | .52 | (1.95) | 8.36 | 8.22 |

Distributions: | | | | | | | |

Dividends from net realized gain

on investments | | | (1.50) | (6.10) | (4.34) | (4.25) | - |

Net asset value, end of period | | | 30.70 | 28.68 | 34.26 | 40.55 | 36.44 |

Total Return (%)b | | | 12.44 | 3.19 | (5.41) | 24.35 | 29.13 |

Ratios/Supplemental Data (%): | | | | | | | |

Ratio of total expenses to

average net assets | | | 1.92 | 1.94 | 1.90 | 1.92 | 1.97 |

Ratio of net expenses to

average net assets | | | 1.92 | 1.94 | 1.90 | 1.92 | 1.97 |

Ratio of net investment (loss)

to average net assets | | | (.65) | (.62) | (.77) | (.66) | (.72) |

Portfolio Turnover Rate | | | 104.51 | 101.68 | 74.05 | 67.49 | 91.31 |

Net Assets, end of period ($ x 1,000) | | | 62,608 | 76,886 | 116,683 | 114,179 | 46,708 |

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

18

| | | | | | | | | | |

| | | | | | |

| | | | |

| | Year Ended August 31, |

Class I Shares | | | 2017 | 2016 | 2015 | 2014 | 2013 |

Per Share Data ($): | | | | | | | |

Net asset value, beginning of period | | | 31.64 | 36.83 | 43.01 | 38.12 | 29.38 |

Investment Operations: | | | | | | | |

Investment income—neta | | | .14 | .12 | .09 | .15 | .10 |

Net realized and unrealized gain

(loss) on investments | | | 4.11 | .81 | (1.78) | 9.07 | 8.77 |

Total from Investment Operations | | | 4.25 | .93 | (1.69) | 9.22 | 8.87 |

Distributions: | | | | | | | |

Dividends from investment

income—net | | | (.12) | (.02) | (.15) | (.08) | (.13) |

Dividends from net realized gain

on investments | | | (1.50) | (6.10) | (4.34) | (4.25) | - |

Total Distributions | | | (1.62) | (6.12) | (4.49) | (4.33) | (.13) |

Net asset value, end of period | | | 34.27 | 31.64 | 36.83 | 43.01 | 38.12 |

Total Return (%) | | | 13.63 | 4.23 | (4.43) | 25.62 | 30.26 |

Ratios/Supplemental Data (%): | | | | | | | |

Ratio of total expenses to

average net assets | | | .90 | .90 | .89 | .90 | .97 |

Ratio of net expenses to

average net assets | | | .90 | .90 | .89 | .90 | .97 |

Ratio of net investment income

to average net assets | | | .42 | .39 | .22 | .37 | .27 |

Portfolio Turnover Rate | | | 104.51 | 101.68 | 74.05 | 67.49 | 91.31 |

Net Assets, end of period ($ x 1,000) | | | 501,821 | 492,694 | 913,852 | 1,282,578 | 856,830 |

a Based on average shares outstanding.

See notes to financial statements.

19

FINANCIAL HIGHLIGHTS (continued)

| | | | | | | | |

| | | | | | |

| | | | |

| | Year Ended August 31, |

Class Y Shares | 2017 | 2016 | 2015 | 2014 | 2013a |

Per Share Data ($): | | | | | |

Net asset value, beginning of period | 31.72 | 36.93 | 43.12 | 38.12 | 37.48 |

Investment Operations: | | | | | |

Investment income—netb | .15 | .16 | .13 | .19 | .02 |

Net realized and unrealized gain

(loss) on investments | 4.13 | .83 | (1.78) | 9.17 | .62 |

Total from Investment Operations | 4.28 | .99 | (1.65) | 9.36 | .64 |

Distributions: | | | | | |

Dividends from investment

income—net | (.16) | (.10) | (.20) | (.11) | - |

Dividends from net realized gain

on investments | (1.50) | (6.10) | (4.34) | (4.25) | - |

Total Distributions | (1.66) | (6.20) | (4.54) | (4.36) | - |

Net asset value, end of period | 34.34 | 31.72 | 36.93 | 43.12 | 38.12 |

Total Return (%) | 13.71 | 4.40 | (4.34) | 26.02 | 1.74c |

Ratios/Supplemental Data (%): | | | | | |

Ratio of total expenses to

average net assets | .80 | .78 | .80 | .83 | .80d |

Ratio of net expenses to

average net assets | .80 | .78 | .80 | .83 | .80d |

Ratio of net investment income to average net assets | .49 | .53 | .30 | .50 | .33d |

Portfolio Turnover Rate | 104.51 | 101.68 | 74.05 | 67.49 | 91.31 |

Net Assets, end of period ($ x 1,000) | 9,137 | 17,308 | 79,397 | 25,147 | 1 |

a From July 1, 2013 (commencement of initial offering) to August 31, 2013.

b Based on average shares outstanding.

c Not annualized.

d Annualized.

See notes to financial statements.

20

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Opportunistic Midcap Value Fund (the “fund”) is a separate diversified series of Advantage Funds, Inc. (the “Company”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering nine series, including the fund. The fund’s investment objective is to seek to surpass the performance of the Russell Midcap® Value Index. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

Effective March 31, 2017, the fund authorized the issuance of Class T shares, but, as of the date of this report, the fund did not offer Class T shares for purchase. The fund authorized 100 million Class T shares which resulted in the fund’s total authorized shares increasing from 700 million to 800 million.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of Dreyfus, is the distributor of the fund’s shares. The fund is authorized to issue 800 million shares of $.001 par value Common Stock. The fund currently has authorized five classes of shares: Class A (350 million shares authorized), Class C (125 million shares authorized), Class I (125 million shares authorized), Class T (100 million shares authorized) and Class Y (100 million shares authorized). Class A and Class T shares generally are subject to a sales charge imposed at the time of purchase. Class C shares are subject to a contingent deferred sales charge (“CDSC”) imposed on Class C shares redeemed within one year of purchase. Class I and Class Y shares are sold at net asset value per share generally to institutional investors. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs, and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Company accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive

21

NOTES TO FINANCIAL STATEMENTS (continued)

releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The Company enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown. The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements. These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

22

Investments in securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. For open short positions, asked prices are used for valuation purposes. Bid price is used when no asked price is available. Registered investment companies that are not traded on an exchange are valued at their net asset value. All of the preceding securities are generally categorized within Level 1 of the fair value hierarchy.

Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices. These securities are generally categorized within Level 2 of the fair value hierarchy.

Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securities and other appropriate indicators, such as prices of relevant ADRs and futures. Utilizing these techniques may result in transfers between Level 1 and Level 2 of the fair value hierarchy.

When market quotations or official closing prices are not readily available, or are determined not to reflect accurately fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded (for example, a foreign exchange or market), but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Company’s Board of Directors (the “Board”). Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers. These securities are either categorized within Level 2 or 3 of the fair value hierarchy depending on the relevant inputs used.

For restricted securities where observable inputs are limited, assumptions about market activity and risk are used and are generally categorized within Level 3 of the fair value hierarchy.

The following is a summary of the inputs used as of August 31, 2017 in valuing the fund’s investments:

23

NOTES TO FINANCIAL STATEMENTS (continued)

| | | | | | |

| | Level 1 -

Unadjusted

Quoted Prices | Level 2 - Other

Significant

Observable

Inputs | Level 3

-Significant

Unobservable

Inputs | Total |

Assets ($) | | | | |

Investments in Securities: | | | |

Equity Securities - Domestic Common Stocks† | 1,054,138,544 | - | - | 1,054,138,544 |

Equity Securities - Foreign Common Stocks† | 17,305,424 | - | - | 17,305,424 |

Exchange Traded Funds | 3,243,216 | - | - | 3,243,216 |

Registered Investment Company | 2,081,600 | - | - | 2,081,600 |

† See Statement of Investments for additional detailed categorizations.

At August 31, 2017, there were no transfers between levels of the fair value hierarchy.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

Pursuant to a securities lending agreement with The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus, the fund may lend securities to qualified institutions. It is the fund’s policy that, at origination, all loans are secured by collateral of at least 102% of the value of U.S. securities loaned and 105% of the value of foreign securities loaned. Collateral equivalent to at least 100% of the market value of securities on loan is maintained at all times. Collateral is either in the form of cash, which can be invested in certain money market mutual funds managed by Dreyfus, or U.S. Government and Agency securities. The fund is entitled to receive all dividends, interest and distributions on securities loaned, in addition to income earned as a result of the lending transaction. Should a borrower fail to return the securities in a timely manner, The Bank of New York Mellon is required to replace the securities for the benefit of the fund or credit the fund with the market value of the unreturned securities and is subrogated to the fund’s rights against the borrower and the collateral. Additionally, the contractual maturity of security lending transactions are on an overnight and continuous basis.

24

During the period ended August 31, 2017, The Bank of New York Mellon earned $8,143 from lending portfolio securities, pursuant to the securities lending agreement.

(c) Affiliated issuers: Investments in other investment companies advised by Dreyfus are defined as “affiliated” under the Act.

(d) Dividends and distributions to shareholders: Dividends and distributions are recorded on the ex-dividend date. Dividends from investment income-net and dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”). To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended August 31, 2017, the fund did not have any liabilities for any uncertain tax positions. The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period ended August 31, 2017, the fund did not incur any interest or penalties.

Each tax year in the four-year period ended August 31, 2017 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At August 31, 2017, the components of accumulated earnings on a tax basis were as follows: undistributed ordinary income $24,844,384, undistributed capital gains $79,794,187 and unrealized appreciation $153,530,551.

The tax character of distributions paid to shareholders during the fiscal periods ended August 31, 2017 and August 31, 2016 were as follows: ordinary income $11,170,930 and $27,165,334, and long-term capital gains $50,851,655 and $263,740,753, respectively.

During the period ended August 31, 2017, as a result of permanent book to tax differences, primarily due to the tax treatment for limited partnerships, the fund decreased accumulated undistributed investment

25

NOTES TO FINANCIAL STATEMENTS (continued)

income-net by $98,106 and increased accumulated net realized gain (loss) on investments by the same amount. Net assets and net asset value per share were not affected by this reclassification.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in an $810 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon (each, a “Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions. Prior to October 5, 2016, the unsecured credit facility with Citibank, N.A. was $555 million. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing.

The average amount of borrowings outstanding under the Facilities during the period ended August 31, 2017, was approximately $654,800 with a related weighted average annualized interest rate of 1.63%.

NOTE 3—Management Fee and Other Transactions with Affiliates:

(a) Pursuant to a management agreement with Dreyfus, the management fee is computed at the annual rate of .75% of the value of the fund's average daily net assets and is payable monthly.

During the period ended August 31, 2017, the Distributor retained $19,203 from commissions earned on sales of the fund’s Class A shares and $1,818 from CDSCs on redemptions of the fund’s Class C shares.

(b) Under the Distribution Plan adopted pursuant to Rule 12b-1 under the Act, Class C shares pay the Distributor for distributing its shares at an annual rate of .75% of the value of its average daily net assets. During the period ended August 31, 2017, Class C shares were charged $536,320 pursuant to the Distribution Plan.

(c) Under the Shareholder Services Plan, Class A and Class C shares pay the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services. The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. The Distributor may make payments to Service Agents (securities dealers, financial institutions or other industry professionals) with respect to these services. The Distributor determines

26

the amounts to be paid to Service Agents. During the period ended August 31, 2017, Class A and Class C shares were charged $1,700,463 and $178,773, respectively, pursuant to the Shareholder Services Plan.

The fund has arrangements with the transfer agent and the custodian whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset transfer agency and custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates Dreyfus Transfer, Inc., a wholly-owned subsidiary of Dreyfus, under a transfer agency agreement for providing transfer agency and cash management services for the fund. The majority of transfer agency fees are comprised of amounts paid on a per account basis, while cash management fees are related to fund subscriptions and redemptions. During the period ended August 31, 2017, the fund was charged $103,681 for transfer agency services and $8,513 for cash management services. These fees are included in Shareholder servicing costs in the Statement of Operations. Cash management fees were partially offset by earnings credits of $8,395.

The fund compensates The Bank of New York Mellon under a custody agreement for providing custodial services for the fund. These fees are determined based on net assets, geographic region and transaction activity. During the period ended August 31, 2017, the fund was charged $87,234 pursuant to the custody agreement. These fees were partially offset by earnings credits of $60.

During the period ended August 31, 2017, the fund was charged $11,281 for services performed by the Chief Compliance Officer and his staff.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $687,883, Distribution Plan fees $40,128, Shareholder Services Plan fees $121,894, custodian fees $28,000, Chief Compliance Officer fees $4,670 and transfer agency fees $19,618.

(d) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities, during the period ended August 31, 2017, amounted to $1,280,677,993 and $1,750,493,984, respectively.

27

NOTES TO FINANCIAL STATEMENTS (continued)

At August 31, 2017, the cost of investments for federal income tax purposes was $923,238,233; accordingly, accumulated net unrealized appreciation on investments was $153,530,551, consisting of $175,853,649 gross unrealized appreciation and $22,323,098 gross unrealized depreciation.

28

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

Shareholders and Board of Directors

Dreyfus Opportunistic Midcap Value Fund

We have audited the accompanying statement of assets and liabilities, including the statements of investments and investments in affiliated issuers, of Dreyfus Opportunistic Midcap Value Fund (one of the series comprising Advantage Funds, Inc.) as of August 31, 2017, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of August 31, 2017 by correspondence with the custodian and others. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus Opportunistic Midcap Value Fund at August 31, 2017, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the indicated periods, in conformity with U.S. generally accepted accounting principles.

New York, New York

October 26, 2017

29

IMPORTANT TAX INFORMATION (Unaudited)

For federal tax purposes, the fund hereby reports 52.17% of the ordinary dividends paid during the fiscal year ended August 31, 2017 as qualifying for the corporate dividends received deduction. Also, certain dividends paid by the fund may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. Of the distributions paid during the fiscal year, $11,170,930 represents the maximum amount that may be considered qualified dividend income. The fund also hereby reports $.2311 per share as a short-term capital gain distribution and $1.2690 per share as a long-term capital gain distribution paid on December 13, 2016. Shareholders will receive notification in early 2018 of the percentage applicable to the preparation of their 2017 income tax returns.

30

INFORMATION ABOUT THE RENEWAL OF THE FUND’S MANAGEMENT AGREEMENT (Unaudited)

At a meeting of the fund’s Board of Directors held on March 9-10, 2017, the Board considered the renewal of the fund’s Management Agreement pursuant to which Dreyfus provides the fund with investment advisory and administrative services (the “Agreement”). The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from Dreyfus representatives. In considering the renewal of the Agreement, the Board considered all factors that it believed to be relevant, including those discussed below. The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund. The Board considered information provided to them at the meeting and in previous presentations from Dreyfus representatives regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex (such as retail direct or intermediary, in which intermediaries typically are paid by the fund and/or Dreyfus) and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each intermediary or distribution channel, as applicable to the fund.

The Board also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements. The Board also considered Dreyfus’ extensive administrative, accounting and compliance infrastructures. The Board also considered portfolio management’s brokerage policies and practices (including policies and practices regarding soft dollars) and the standards applied in seeking best execution.

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio. The Board reviewed reports prepared by Broadridge Financial Solutions, Inc. (“Broadridge”), an independent provider of investment company data, which included information comparing (1) the fund’s performance with the performance of a group of comparable funds (the “Performance Group”) and with a broader group of funds (the “Performance Universe”), all for various periods ended January 31, 2017 and (2) the fund’s actual and contractual management fees and total expenses with those of a group of comparable funds (the “Expense Group”) and with a broader group of funds (the “Expense Universe”), the information for which was derived in part from fund financial statements available to Broadridge as of the date of its analysis. Dreyfus previously had furnished the Board with a description of the methodology Broadridge used to select the Performance Group and Performance Universe and the Expense Group and Expense Universe.

31

INFORMATION ABOUT THE RENEWAL OF THE FUND’S MANAGEMENT AGREEMENT (Unaudited) (continued)

Dreyfus representatives stated that the usefulness of performance comparisons may be affected by a number of factors, including different investment limitations that may be applicable to the fund and comparison funds. The Board discussed with representatives of Dreyfus and/or its affiliates the results of the comparisons and considered that the fund’s total return performance was at or above the Performance Group median for all periods (highest in the one- and ten-year periods) except the three- and four- year periods when it was below the median, and the fund’s performance was above or only one basis point below the Performance Universe median for all periods except for the three- and four-year periods when it was below the median. Dreyfus also provided a comparison of the fund’s calendar year total returns to the returns of the fund’s benchmark index.

The Board also reviewed the range of actual and contractual management fees and total expenses of the Expense Group and Expense Universe funds and discussed the results of the comparisons. The Board considered that the fund’s contractual management fee was above the Expense Group median and the fund’s actual management fee and total expenses were above the Expense Group and Expense Universe medians.

Dreyfus representatives reviewed with the Board the management or investment advisory fees (1) paid by funds advised or administered by Dreyfus that are in the same Broadridge category as the fund and (2) paid to Dreyfus or the Dreyfus-affiliated primary employer of the fund’s primary portfolio manager(s) for advising any separate accounts and/or other types of client portfolios that are considered to have similar investment strategies and policies as the fund (the “Similar Clients”), and explained the nature of the Similar Clients. They discussed differences in fees paid and the relationship of the fees paid in light of any differences in the services provided and other relevant factors. The Board considered the relevance of the fee information provided for the Similar Clients to evaluate the appropriateness of the fund’s management fee.

Analysis of Profitability and Economies of Scale. Dreyfus representatives reviewed the expenses allocated and profit received by Dreyfus and its affiliates and the resulting profitability percentage for managing the fund and the aggregate profitability percentage to Dreyfus and its affiliates for managing the funds in the Dreyfus fund complex, and the method used to determine the expenses and profit. The Board concluded that the profitability results were not unreasonable, given the services rendered and service levels provided by Dreyfus. The Board also had been provided with information prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the profitability of, individual funds and the entire Dreyfus fund complex. The consulting firm also had analyzed where any economies of scale might emerge in connection with the management of a fund.

The Board considered, on the advice of its counsel, the profitability analysis (1) as part of its evaluation of whether the fees under the Agreement, considered in relation to the mix of services provided by Dreyfus, including the nature, extent and quality of such services, supported the renewal of the Agreement and (2) in light of the relevant circumstances for the fund and the extent to which economies of scale would be realized if the fund grows and whether fee levels reflect these economies of scale for the

32

benefit of fund shareholders. Dreyfus representatives stated that a discussion of economies of scale is predicated on a fund having achieved a substantial size with increasing assets and that, if a fund’s assets had been stable or decreasing, the possibility that Dreyfus may have realized any economies of scale would be less. Dreyfus representatives also stated that, as a result of shared and allocated costs among funds in the Dreyfus fund complex, the extent of economies of scale could depend substantially on the level of assets in the complex as a whole, so that increases and decreases in complex-wide assets can affect potential economies of scale in a manner that is disproportionate to, or even in the opposite direction from, changes in the fund’s asset level. The Board also considered potential benefits to Dreyfus from acting as investment adviser and took into consideration the soft dollar arrangements in effect for trading the fund’s investments.

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to the renewal of the Agreement. Based on the discussions and considerations as described above, the Board concluded and determined as follows.

· The Board concluded that the nature, extent and quality of the services provided by Dreyfus are adequate and appropriate.

· The Board was satisfied with the fund’s improved performance in recent periods.

· The Board concluded that the fee paid to Dreyfus supported the renewal of the Agreement in light of the considerations described above.

· The Board determined that the economies of scale which may accrue to Dreyfus and its affiliates in connection with the management of the fund had been adequately considered by Dreyfus in connection with the fee rate charged to the fund pursuant to the Agreement and that, to the extent in the future it were determined that material economies of scale had not been shared with the fund, the Board would seek to have those economies of scale shared with the fund.

In evaluating the Agreement, the Board considered these conclusions and determinations and also relied on its previous knowledge, gained through meetings and other interactions with Dreyfus and its affiliates, of Dreyfus and the services provided to the fund by Dreyfus. The Board also relied on information received on a routine and regular basis throughout the year relating to the operations of the fund and the investment management and other services provided under the Agreement, including information on the investment performance of the fund in comparison to similar mutual funds and benchmark performance indices; general market outlook as applicable to the fund; and compliance reports. In addition, the Board’s consideration of the contractual fee arrangements for this fund had the benefit of a number of years of reviews of the Agreement for the fund, or substantially similar agreements for other Dreyfus funds that the Board oversees, during which lengthy discussions took place between the Board and Dreyfus representatives. Certain aspects of the arrangements may receive greater scrutiny in some years than in others, and the Board’s conclusions

33

INFORMATION ABOUT THE RENEWAL OF THE FUND’S MANAGEMENT AGREEMENT (Unaudited) (continued)

may be based, in part, on their consideration of the fund’s arrangements, or similar arrangements for other Dreyfus funds that the Board oversees, in prior years. The Board determined to renew the Agreement.

34

BOARD MEMBERS INFORMATION (Unaudited)

INDEPENDENT BOARD MEMBERS

Joseph S. DiMartino (73)

Chairman of the Board (1995)

Principal Occupation During Past 5 Years:

· Corporate Director and Trustee (1995-present)

Other Public Company Board Memberships During Past 5 Years:

· CBIZ (formerly, Century Business Services, Inc.), a provider of outsourcing functions for small and medium size companies, Director (1997-present)

No. of Portfolios for which Board Member Serves: 130

———————

Peggy C. Davis (74)

Board Member (2006)

Principal Occupation During Past 5 Years:

· Shad Professor of Law, New York University School of Law (1983-present)

No. of Portfolios for which Board Member Serves: 47

———————

David P. Feldman (77)

Board Member (1996)

Principal Occupation During Past 5 Years:

· Corporate Director and Trustee (1985-present)

Other Public Company Board Memberships During Past 5 Years:

· BBH Mutual Funds Group (5 registered mutual funds), Director (1992-2014)

No. of Portfolios for which Board Member Serves: 33

———————

Joan Gulley (69)

Board Member (2017)

Principal Occupation During Past 5 Years:

· PNC Financial Services Group, Inc.(1993-2014)

· Executive Vice President and Chief Human Resources Officer and Executive Committee Member (2008-2014)

No. of Portfolios for which Board Member Serves: 33

———————

35

BOARD MEMBERS INFORMATION (Unaudited) (continued)

INDEPENDENT BOARD MEMBERS (continued)

Ehud Houminer (77)

Board Member (1993)

Principal Occupation During Past 5 Years:

· Board of Overseers at the Columbia Business School, Columbia University (1992-present)

· Trustee, Ben Gurion University

Other Public Company Board Memberships During Past 5 Years:

· Avnet, Inc., an electronics distributor, Director (1993-2012)

No. of Portfolios for which Board Member Serves: 54

———————

Lynn Martin (77)

Board Member (2012)

Principal Occupation During Past 5 Years:

· President of The Martin Hall Group LLC, a human resources consulting firm (2005-2012)

Other Public Company Board Memberships During Past 5 Years:

· AT&T, Inc., a telecommunications company, Director (1999-2012)

· Ryder System, Inc., a supply chain and transportation management company, Director (1993-2012)

No. of Portfolios for which Board Member Serves: 33

———————

Robin A. Melvin (53)

Board Member (2012)

Principal Occupation During Past 5 Years:

· Co-chairman, Illinois Mentoring Partnership, non-profit organization dedicated to increasing the quantity and quality of mentoring services in Illinois; (2014-present; board member since 2013)

· Director, Boisi Family Foundation, a private family foundation that supports youth-serving organizations that promote the self sufficiency of youth from disadvantaged circumstances (1995-2012)

No. of Portfolios for which Board Member Serves: 102

———————

36

Dr. Martin Peretz (78)

Board Member (2006)

Principal Occupation During Past 5 Years:

· Editor-in-Chief Emeritus of The New Republic Magazine (2011-2012) (previously,

Editor-in-Chief, 1974-2011)

· Lecturer at Harvard University (1969-2012)

No. of Portfolios for which Board Member Serves: 33

———————

Once elected all Board Members serve for an indefinite term, but achieve Emeritus status upon reaching age 80. The address of the Board Members and Officers is c/o The Dreyfus Corporation, 200 Park Avenue, New York, New York 10166. Additional information about the Board Members is available in the fund’s Statement of Additional Information which can be obtained from Dreyfus free of charge by calling this toll free number: 1-800-DREYFUS.

James F. Henry, Emeritus Board Member

Philip L. Toia, Emeritus Board Member

37

OFFICERS OF THE FUND (Unaudited)

BRADLEY J. SKAPYAK, President since January 2010.

Chief Operating Officer and a director of the Manager since June 2009, Chairman of Dreyfus Transfer, Inc., an affiliate of the Manager and the transfer agent of the funds, since May 2011 and Chief Executive Officer of MBSC Securities Corporation since August 2016. He is an officer of 63 investment companies (comprised of 130 portfolios) managed by the Manager. He is 58 years old and has been an employee of the Manager since February 1988.

BENNETT A. MACDOUGALL, Chief Legal Officer since October 2015.