UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08748 | |||||||

| ||||||||

Wanger Advisors Trust | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

227 W. Monroe Street Suite 3000 Chicago, IL |

| 60606 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Mary C. Moynihan Perkins Coie LLP 700 13th Street, NW Suite 600 Washington, DC 20005

Paul B. Goucher, Esq. Columbia Management Investment Advisers, LLC 100 Park Avenue New York, New York 10017

P. Zachary Egan Columbia Acorn Trust 227 West Monroe Street, Suite 3000 Chicago, Illinois 60606 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (312) 634-9200 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2015 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

ANNUAL REPORT

December 31, 2015

COLUMBIA WANGER FUNDS

Managed by Columbia Wanger Asset Management, LLC

WANGER INTERNATIONAL

Wanger International

2015 Annual Report

Table of Contents

| 2 | Understanding Your Expenses | ||||||

| 3 | Behavioral Economics | ||||||

| 6 | Performance Review | ||||||

| 8 | Statement of Investments | ||||||

| 17 | Statement of Assets and Liabilities | ||||||

| 17 | Statement of Operations | ||||||

| 18 | Statement of Changes in Net Assets | ||||||

| 19 | Financial Highlights | ||||||

| 20 | Notes to Financial Statements | ||||||

| 24 | Report of Independent Registered Public Accounting Firm | ||||||

| 25 | Federal Income Tax Information (Unaudited) | ||||||

| 26 | Board of Trustees and Management of Wanger Advisors Trust | ||||||

Columbia Wanger Asset Management, LLC (CWAM) is one of the leading global small- and mid-cap equity managers in the United States with over 40 years of small- and mid-cap investment experience. As of December 31, 2015, CWAM managed $20 billion in assets. CWAM is the investment manager to Wanger USA, Wanger International, Wanger Select and Wanger International Select (together, the Columbia Wanger Funds) and the Columbia Acorn Family of Funds.

An important note: Columbia Wanger Funds are available only through variable annuity contracts and variable life insurance policies issued by participating insurance companies or certain eligible retirement plans. Columbia Wanger Funds are not offered directly to the public and are not available in all contracts, policies or plans. Contact your financial advisor or insurance representative for more information. Columbia Wanger Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA, and are managed by CWAM.

Investors should carefully consider investment objectives, risks and expenses of the Fund before investing. For variable fund and variable contract prospectuses, which contain this and other important information, including the fees and expenses imposed under your contract, investors should contact their financial advisor or insurance representative. Read the prospectus for the Fund and your variable contract carefully before investing.

The views expressed in "Behavioral Economics" and in the Performance Review reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund. References to specific company securities should not be construed as a recommendation or investment advice.

1

Wanger International 2015 Annual Report

Understanding Your Expenses

As a shareholder, you incur three types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees. There are also ongoing costs, which generally include management fees and other expenses for Wanger International (the Fund). Lastly, there may be additional fees or charges imposed by the insurance company that sponsors your variable annuity and/or variable life insurance product. The following information is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to help you compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund's expenses

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in the Fund during the period. The actual and hypothetical information in the table below is based on an initial investment of $1,000 at the beginning of the period indicated and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using the Fund's actual operating expenses and total return for the period. You may use the Actual information, together with the amount invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the results by the expenses paid during the period under the Actual column. The amount listed in the "Hypothetical" column assumes a 5% annual rate of return before expenses (which is not the Fund's actual return) and then applies the Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See "Compare with other funds" below for details on how to use the hypothetical data.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing cost of investing in a fund only and do not reflect any transaction costs, such as sales charges, redemption or exchange fees. Therefore, the hypothetical calculations are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If transaction costs were included in these calculations, your costs would be higher.

July 1, 2015 – December 31, 2015

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during period ($) | Fund's annualized expense ratio (%)* | ||||||||||||||||||||||||||||

Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | ||||||||||||||||||||||||||

Wanger International | 1,000.00 | 1,000.00 | 951.80 | 1,019.41 | 5.66 | 5.85 | 1.15 | ||||||||||||||||||||||||

* Expenses paid during the period are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 365.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Fund. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate account. The hypothetical example provided is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

2

Wanger International 2015 Annual Report

Behavioral Economics

People Occasionally Behave Irrationally

Economists have traditionally assumed that people rationally optimize in their own self-interest. A free-market economy dominated by "homo economicus" prospers as producers of goods and services trade with each other, as if driven by an invisible hand. In the past few decades, however, behavioral economics has emerged, refuting the rational optimization assumption. Nobel Prize winning Princeton professor Daniel Kahneman's book Thinking, Fast and Slow explains the habits and biases that cause people to make predictable errors.

Illustrating that people tend to make quick, intuitive decisions rather than well thought out ones, Kahneman asked Ivy League students the following question: A bat and a ball cost $1.10. The bat costs $1.00 more than the ball. How much does the ball cost? Over half of students answered $0.10, though the correct answer is $0.05.

Kahneman also points out that people generally have a confirmation bias.1 Good scientific method calls for people to test a hypothesis by attempting to refute it, but instead people seek data that confirms their beliefs. We would rather keep our beliefs than seriously analyze and challenge them.

Individuals also exhibit an anchoring effect. Kahneman and his associate Amos Tversky devised several experiments that first provided a high or low number (from a rigged "wheel of fortune" or in a text) and then asked for best-guess estimates for unrelated data. Subjects who were provided high numbers gave high estimates and vice versa. People tend to "anchor" on an initial number provided and then move toward an unbiased estimate. When the Exploratorium Museum in San Francisco polled visitors about contributing to a particular cause without providing a suggested contribution amount, visitors on average said they would donate $64. When $5 was suggested as a donation, the average response was $20, and when $400 was suggested, the average jumped to $143.2 It seems as though many charities understand the anchoring effect.

Kahneman identified an availability bias. People base their knowledge, opinions and actions on small samples of information readily available to them. Estimates of causes of death are warped by media coverage. For example, strokes cause almost twice as many deaths as all accidents combined, but 80% of respondents said accidental deaths were more likely.3

Kahneman and Tversky did many behavioral studies, and their largest contribution to behavioral economics is their work on decision making in risky situations. Subjects were asked to make the following two choices concurrently:

Choose between:

A. a sure gain of $240

B. 25% chance to win $1,000 and a 75% chance to gain nothing

Choose between:

C. a sure loss of $750

D. 75% chance to lose $1,000 and a 25% chance to lose nothing

People are risk averse with respect to gains; 84% of subjects chose A, accepting a lower expected value than B.4 However, people are risk seeking with respect to losses. People hate to lose and will take a chance of a greater loss in exchange for a chance not to lose; 87% chose D.5

Despite the instructions, subjects appeared to make these choices sequentially rather than concurrently. They framed the exercise as two separate choices. Choosing A and D provides a net result of a 75% chance to lose $760 and a 25% chance of gaining $240. People solving the problems concurrently and rationally would have chosen C and B, which provides a net result of a 75% chance to lose $750 and a 25% chance to gain $250. Choosing C and B together results in the same odds, yet $10 more under either scenario.

Given our biases, how a choice is framed heavily influences our decisions. Would you accept a gamble that offers a 10% chance to win $95 and a 90% chance to lose $5? Would you pay $5 to participate in a lottery that offers a 10% chance to win $100 and a 90% chance to win nothing?

Many more people accept the second opportunity than the first, even though the choices are identical. The first clearly frames the $5 as a loss, while the second suggests the $5 is a sunk cost. 6

Kahneman and Tversky also did a study to determine values people assign to probabilities, what they called decision weights. People provided zero value to a zero probability and a value of 100 to a sure thing, but the values in between were interesting:7

Probability | 1 | % | 10 | % | 50 | % | 90 | % | 99 | % | |||||||||||||

| Decision Weight | 5.5 | 18.6 | 42.1 | 71.2 | 91.2 | ||||||||||||||||||

What the data shows is that people are often willing to overpay for small probabilities, a tendency known as the possibility effect. That is why lotteries exist. Yet people underpay relatively more for large but not certain probabilities. To eliminate those last bits of uncertainty, people are willing to pay a lot, a tendency known as the certainty effect.

Richard Thaler, a University of Chicago professor of behavioral science and economics, worked with Kahneman and Tversky on several studies. Jointly, they defined the endowment effect, which states that once someone owns something, he tends to place an irrationally high value on it. Thaler and Kahneman experimented by giving some subjects coffee mugs decorated with university insignia. Participants were asked to provide the prices at which they would sell. Other subjects were not given mugs and were asked what prices they would bid for the mugs. The average selling price was about double the average buying price!8

Thaler agrees with Kahneman's findings that people are risk seeking with respect to losses, both prospectively and retrospectively. People who are losing money at a racetrack tend to bet on longshots for the last race of the day, hoping to recoup losses, effectively driving the expected return of the last race even more against them!9 Financial institutions need to watch losing traders very closely, as rogue traders repeatedly double down in hopes of recouping losses.

3

Wanger International 2015 Annual Report

Thaler's work indicates that people create mental accounts, treating some money differently depending on its intended use. Cash accounts are for spending, other funds are for savings, and retirement accounts are sacrosanct.10 People may borrow at high interest rates on their charge cards while receiving low interest rates on savings, which appears irrational.

Thaler notes that Economics 101 classes typically teach that prices should rationally rise when there is an unanticipated increase in demand. I remember learning that it would be rational for merchants to raise the price of snow shovels after a blizzard and plywood before a hurricane. The products would be rationed by price to those most in need and capable of paying, and additional revenues would induce costly special increases in supply. Thaler's work, however, indicates that most people would consider such increases as unfair price gouging, and would later penalize those merchants.

Policy Implications

Public policies are often impacted by people's emotional reaction under the availability bias. Former Administrator of the White House Office of Information and Regulatory Affairs, Cass Sunstein, has analyzed resulting regulations and notes that poor regulations waste time and money. Rational weighting of costs and benefits would result in better regulations and improved outcomes.11

Kahneman points out that as an extension of the possibility effect, people tend to be confounded by exceptionally small probabilities,12 and either ignore them or give them way too much attention. The precautionary principle, which prohibits any action that might cause harm, is the result. Sunstein believes that many innovations including airplanes, antibiotics, automobiles, chlorination, vaccinations and x-rays would have not passed strict interpretation of the precautionary principle.13

Thaler's work explains one of the reasons why policy makers prefer modest inflation. People consider outright wage cuts as unfair, even when unemployment is high and the employer is

earning only a small profit. But a flat wage when there is inflation is not considered unfair, even though real wages drop.14 Therefore, the economy can more easily rationalize costs in a recession with some inflation rather than none.

Thaler devised a plan to induce people to contribute more to 401K plans called "Save More Tomorrow." Many people don't contribute to their 401K plan because that would mean an immediate take-home pay cut, frowned on by the endowment effect. Instead, the plan has people sign up now to contribute upon their next raise in pay. They then forgo some or the entire raise, but save for retirement without taking a pay cut. Employees of the first company that adopted the plan nearly quadrupled their savings rate after four annual raises.15

Thaler and Sunstein's book Nudge cites numerous ways that individuals can be "nudged" to make better decisions. For example, default options are considered standard and most people don't extend the effort to make a different choice. Germans need to opt in for organ donations, and only 12% do. Austrians need to opt out of organ donations, and 99% allow their organs to be donated.16

Investment Implications

Kahneman notes that experienced traders in financial markets tend to more rationally deal with risk aversion than individual investors. Most people weight losses twice as much as gains,17 and if each transaction is framed individually, irrational risk aversion results. By framing gains and losses over longer periods rather than individually, traders can accept individual rational risks. To mitigate this bias, Kahneman suggests that individual investors view the market prices of their investments less frequently.18

Thaler agrees, as he conducted an experiment simulating endowment management. Some subjects were shown results eight times per simulated calendar year, while others were shown results once per simulated year. Those seeing results more frequently chose to invest 41% in stocks and those seeing results just

once a year had 70% in stocks.19 Myopic risk aversion helps explain why stocks provided a 7% premium compound rate of return over risk-free securities for the last two centuries,20 a huge premium that cannot be otherwise explained by economic theory.21

Individuals tend to be terrible stock traders. One study indicated that stocks sold by individuals outperformed stocks they bought by 3.2% per year, before transactions costs. Individual investors tend to sell winners even though recent winners on average outperform recent losers in the short term. Individuals tend to keep losers, as they are averse to taking losses and have anchored on purchase prices as target sale prices for losers.22 Losers on average underperform in the short term.23

Mental accounts result in the house money effect for gamblers and investors. People are more prone to lose their risk aversion on gains when they are ahead. This can result in gamblers not knowing when to quit, and investors creating bubbles.24

Humans, including many professional money managers, seem to be hard wired to invest poorly, to "buy high and sell low." Behavioral economics helps explain why. One solution to offset this tendency is to own Columbia Thermostat Fund, which takes emotions out of investing and automatically invests more in stocks when the market drops and automatically sells stocks when the market rises.25

Charles P. McQuaid

Portfolio Manager, Analyst and Advisor

Columbia Wanger Asset Management, LLC

4

Wanger International 2015 Annual Report

The information and data provided in this analysis are derived from sources that we deem to be reliable and accurate. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. The views/opinions expressed here are those of the author and not of the Wanger Advisors Trust Board of Trustees, are subject to change at any time based upon economic, market or other conditions, may differ from views expressed by other Columbia Management associates and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund.

The author would like to thank Colin Moore, Global Chief Investment Officer of Columbia Threadneedle Investments, for suggesting Beyond Greed and Fear, which summarizes behavioral economics for investors. He would also like to thank recently retired Wanger Advisors Trust Chief Compliance Officer Robert Scales for suggesting Thinking, Fast and Slow.

1 Daniel Kahneman, Thinking, Fast and Slow (New York, Farrar, Straus and Giroux, 2011), p. 81.

2 Ibid., p. 125.

3 Ibid., p. 138.

4 Expected value is the sum of probabilities times dollars.

5 Kahneman, op. cit., p. 437.

6 Ibid., p. 364.

7 Ibid., p. 315.

8 Ibid., p. 295.

9 Richard H. Thaler, Misbehaving: The Making of Behavioral Economics (New York, W. W. Norton & Company, Inc., 2015), p. 80.

10 Ibid., p. 76.

11 Kahneman, op. cit., p. 141.

12 Somehow this one is not labelled as a particular bias or effect.

13 Kahneman, op. cit., p. 351.

14 Thaler, op. cit., p. 132.

15 Ibid., p. 318.

16 Richard H. Thaler and Cass R. Sunstein, Nudge: Improving Decisions About Health, Wealth, and Happiness (New Haven, Connecticut, Yale University Press, 2008), p. 178-179.

17 Kahneman, op. cit., p. 349.

18 Ibid., p. 339.

19 Thaler, op. cit., p. 197.

20 Hersh Shefrin, Beyond Greed and Fear: Understanding Behavioral Finance and the Psychology of Investing (New York, Oxford University Press, 2002), p. 37.

21 Thaler, op. cit., p. 192.

22 In Beyond Greed and Fear, Shefrin labels this as "Get-evenitis."

23 Kahneman, op. cit., p. 213-214.

24 Thaler, op. cit., p. 83.

25 If interested, please see Columbia Thermostat Fund's prospectus, which can be found at columbiathreadneedle.com/us.

5

Wanger International 2015 Annual Report

Performance Review Wanger International

|

| ||||||

| P. Zachary Egan Co-Portfolio Manager* | Louis J. Mendes Co-Portfolio Manager | ||||||

Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. International investing involves certain risks and volatility due to potential political, economic or currency instabilities and different, potentially less stringent, financial and accounting standards than those generally applicable to U.S. issuers. Risks are enhanced for emerging market issuers. Investments in small- and mid-cap companies involve risks and volatility and possible illiquidity greater than investments in larger, more established companies.

Wanger International ended the year up 0.10%, slightly behind the 0.21% gain of the Fund's primary benchmark, the S&P Global ex-U.S. Between $500M and $5B® Index.

Looking back on 2015, one of the major changes to the portfolio was the movement of assets from some emerging markets to Europe. At December 31, 2015, the Fund had a 30% exposure to Europe (excluding the UK), up about 10 percentage points from the end of 2014. Meanwhile, the Fund's emerging markets exposure was scaled back from 22% to 14%. There were several considerations behind these moves: European gross domestic product (GDP) growth remains positive, if anemic, while certain emerging markets, such as Brazil, are experiencing contraction and credit rating downgrades. Moreover, ongoing monetary easing policies in Europe support both credit expansion and equity valuations, which are above long-term historical levels, but that we believe are warranted by the long-term outlook for interest rates. Emerging market countries that export commodities, on the other hand, are suffering from slumping commodity prices, which is exerting pressure on their fiscal situations and currencies, with the latter effect raising borrowing costs for companies that fund themselves in U.S. dollars.

Notwithstanding the Fund's general reduction in emerging markets exposure, this is a heterogeneous space and, over the last year, the Fund has maintained its weight in India, and increased its weight in China. India remains largely insulated from commodity price turmoil and is a beneficiary of cheap oil, which was previously stressing both its current account and, through consumer fuel subsidies, its fiscal position. While we have concerns about China's slowdown and its impact on the global economy, we now see a reasonably clear policy framework in China that we believe is supportive of companies addressing the energy and environmental challenges that have accompanied the country's rise to a US$10 trillion economy, as well as companies addressing increasing demand for health care. Our increased exposure to China is focused in these sectors.

Stock selection in Europe was positive for Fund performance in the year. SimCorp, a Danish company that produces software for the financial services sector, and the Fund's largest position at the end of the year, was a top contributor to performance in an environment of improving demand from large asset managers. An investment initiated in 2010, SimCorp fits into our "regulation" theme. Under this theme, we have worked to identify companies benefiting from increasingly stringent regulatory standards, typically around health, safety and the environment, but extending to the

financial realm in the wake of the 2008 financial crisis. SimCorp's products help investment managers meet new compliance requirements in a cost-effective way. Its stock gained 117% for the year.

The Fund's single largest country weight at the end of 2015 was Japan. At 21% of assets at year end, this weighting is up slightly year over year. As with Europe, loose Japanese monetary policy is supportive of valuations, and we are encouraged by increasing sensitivity among corporates in general toward capital efficiency, which is underpinned by explicit financial sector regulation. Ariake Japan, a maker of commercial soup and sauce extracts, was a top contributor for the year, gaining 130%.

As part of our repositioning of the Fund regionally, we have taken the opportunity to reduce the number of names in the portfolio in order to ensure that our highest conviction ideas have a meaningful impact on returns. At the end of 2015, Wanger International had 174 positions, down from 240 at the end of 2014.

Detractors for the year included South African fund manager Coronation Fund Managers, down 64%. Poor performance and asset outflows significantly reduced the firm's performance-based fees and negatively impacted its stock. Spotless, an Australian facility management and catering company, was hurt by an earnings downgrade, as integration of new acquisitions has taken longer than expected and new business growth has slowed. Its stock was down 45% for the year.

2015 was a challenging year for international investors. The bifurcation of performance between developed and emerging markets was more pronounced than it has been in recent years, and was compounded by currency weakness against the strong U.S. dollar. As the second-largest economy in the world and with a contribution to global GDP of around 15%, China's slowdown raised concerns and cast a shadow over many emerging economies. In developed markets, investors were willing to pay more for companies showing growth in anticipation of higher earnings in the future. But these names were few and far between.

*Effective January 1, 2016, P. Zachary Egan replaced Christopher J. Olson as co-portfolio manager of Wanger International. Mr. Mendes continues in his role as co-portfolio manager of the Fund. Mr. Egan is the President and Global Chief Investment Officer of CWAM, and also serves as a co-portfolio manager on two of the largest Columbia Acorn Funds. Mr. Egan did not serve as a co-portfolio manager of the Fund during 2015.

Fund holdings are as of the date given, are subject to change at any time, and are not recommendations to buy or sell any security.

6

Wanger International 2015 Annual Report

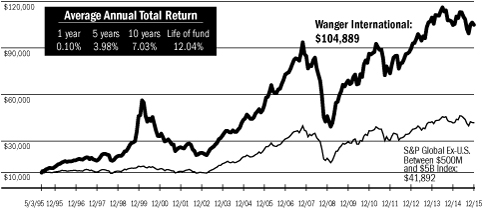

Growth of a $10,000 Investment in Wanger International

May 3, 1995 (inception date) through December 31, 2015

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment manager and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. For most recent month-end performance updates, please visit columbiathreadneedle.com/us.

This graph compares the results of $10,000 invested in Wanger International on May 3, 1995 (the date the Fund began operations) through December 31, 2015, to the S&P Global Ex-U.S. Between $500M and $5B Index with dividends and capital gains reinvested. Although the index is provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the index.

Top 10 Holdings

As a percentage of net assets, as of 12/31/15

| 1. SimCorp (Denmark) Software for Investment Managers | 1.6 | % | |||||

| 2. Wirecard (Germany) Online Payment Processing & Risk Management | 1.5 | ||||||

| 3. CCL Industries (Canada) Global Label Converter | 1.5 | ||||||

| 4. Distribuidora Internacional de Alimentación (Spain) Discount Retailer in Spain & Latin America | 1.4 | ||||||

| 5. Unibet (Sweden) European Online Gaming Operator | 1.4 | ||||||

| 6. Domino's Pizza Enterprises (Australia) Domino's Pizza Operator in Australia & New Zealand | 1.4 | ||||||

| 7. Zee Entertainment Enterprises (India) Indian Programmer of Pay Television Content | 1.3 | ||||||

| 8. Rightmove (United Kingdom) Internet Real Estate Listings | 1.3 | ||||||

| 9. Charles Taylor (United Kingdom) Insurance Services | 1.2 | ||||||

| 10. Aurelius (Germany) European Turnaround Investor | 1.2 | ||||||

Top holdings exclude short-term holdings and cash, if applicable.

Top 5 Countries

As a percentage of net assets, as of 12/31/15

Japan | 20.9 | % | |||||

United Kingdom | 13.0 | ||||||

Germany | 5.6 | ||||||

Sweden | 5.4 | ||||||

Canada | 4.8 | ||||||

Results as of December 31, 2015

4th quarter* | 1 year | 5 years | 10 years | ||||||||||||||||

Wanger International | 5.52 | % | 0.10 | % | 3.98 | % | 7.03 | % | |||||||||||

| S&P Global Ex-U.S. Between $500M and $5B Index** | 4.87 | 0.21 | 2.63 | 5.36 | |||||||||||||||

MSCI EAFE Index (Net) | 4.71 | -0.81 | 3.60 | 3.03 | |||||||||||||||

NAV as of 12/31/15: $26.32

* Not annualized.

** The Fund's primary benchmark as of December 31, 2015. Effective January 1, 2016, the primary benchmark for Wanger International was changed to the MSCI ACWI Ex USA Small Cap Index (Net).

Performance numbers reflect all Fund expenses but do not include any fees and expenses imposed under your variable annuity contract or life insurance policy or qualified pension or retirement plan. If performance numbers included the effect of these additional charges, they would be lower.

The Fund's annual operating expense ratio of 1.05% is stated as of the Fund's prospectus dated May 1, 2015, and differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and/or expense reimbursements as well as different time periods used in calculating the ratios.

All results shown assume reinvestment of distributions.

The S&P Global Ex-U.S. Between $500M and $5B Index is a subset of the broad market selected by the index sponsor representing the mid- and small-cap developed and emerging markets, excluding the United States. The MSCI Europe, Australasia, Far East (EAFE) Index (Net) is a capitalization-weighted index that tracks the total return of common stocks in 21 developed-market countries within Europe, Australasia and the Far East. The returns of the MSCI EAFE Index (Net) are presented net of the withholding tax rate applicable to foreign non-resident institutional investors in the foreign companies included in the index who do not benefit from double taxation treaties. The performance of the MSCI EAFE Index (Net) is provided to show how the Fund's performance compares to a widely recognized broad-based index of foreign market performance. Indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings.

7

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

| Number of Shares | Value | ||||||||||

Equities – 97.2% | |||||||||||

Europe – 43.3% | |||||||||||

United Kingdom – 13.0% | |||||||||||

124,807 | Rightmove Internet Real Estate Listings | $ | 7,584,524 | ||||||||

1,862,635 | Charles Taylor Insurance Services | 7,139,331 | |||||||||

1,277,005 | Polypipe Manufacturer of Plastic Piping & Fittings | 6,570,137 | |||||||||

223,482 | WH Smith Newsprint, Books & General Stationery Retailer | 5,806,940 | |||||||||

1,164,000 | Regus Rental of Office Space in Full Service Business Centers | 5,719,398 | |||||||||

105,487 | Spirax Sarco Steam Systems for Manufacturing & Process Industries | 5,101,643 | |||||||||

369,000 | Halma Health & Safety Sensor Technology | 4,698,731 | |||||||||

254,860 | Domino's Pizza UK & Ireland Pizza Delivery in the UK, Ireland & Germany | 3,950,077 | |||||||||

1,365,000 | Rentokil Initial Pest Control, Washroom & Workwear Service Provider | 3,202,619 | |||||||||

201,000 | Babcock International Public Sector Outsourcer | 3,007,996 | |||||||||

1,210,014 | Connect Group Newspaper & Magazine Distributor | 2,995,104 | |||||||||

3,545,000 | Assura UK Primary Health Care Property Developer | 2,890,000 | |||||||||

491,000 | DS Smith (a) Packaging | 2,872,137 | |||||||||

264,067 | Abcam Online Sales of Antibodies | 2,586,748 | |||||||||

521,400 | Halfords UK Retailer of Leisure Goods & Auto Parts | 2,569,149 | |||||||||

170,000 | Shaftesbury London Prime Retail REIT | 2,290,225 | |||||||||

1,676,773 | Cable and Wireless Telecommunications Service Provider in the Caribbean | 1,834,421 | |||||||||

396,510 | Ocado (a) Online Grocery Retailer | 1,771,499 | |||||||||

474,031 | Elementis Specialty Chemicals | 1,596,407 | |||||||||

| Number of Shares | Value | ||||||||||

262,952 | PureCircle (a) | $ | 1,561,235 | ||||||||

Natural Sweeteners | |||||||||||

13,956 | Fidessa Group Software for Financial Trading Systems | 412,096 | |||||||||

76,160,417 | |||||||||||

Germany – 5.6% | |||||||||||

180,820 | Wirecard Online Payment Processing & Risk Management | 9,038,294 | |||||||||

135,696 | Aurelius European Turnaround Investor | 7,043,671 | |||||||||

58,205 | MTU Aero Engines Airplane Engine Components & Services | 5,672,951 | |||||||||

89,629 | NORMA Group Clamps for Automotive & Industrial Applications | 4,953,928 | |||||||||

130,083 | Elringklinger Automobile Components | 3,302,191 | |||||||||

6,449 | Rational Commercial Ovens | 2,927,277 | |||||||||

32,938,312 | |||||||||||

Sweden – 5.4% | |||||||||||

81,762 | Unibet European Online Gaming Operator | 8,336,885 | |||||||||

314,000 | Recipharm (b) Contract Development Manufacturing Organization | 4,705,471 | |||||||||

275,730 | Sweco (b) Engineering Consultants | 4,058,479 | |||||||||

177,076 | Mekonomen (b) Nordic Integrated Wholesaler/Retailer of Automotive Parts & Service | 3,624,238 | |||||||||

95,417 | Hexagon Design, Measurement & Visualization Software & Equipment | 3,529,745 | |||||||||

81,106 | Swedish Match Swedish Snus | 2,866,076 | |||||||||

89,256 | Modern Times Group Nordic TV Broadcaster | 2,279,043 | |||||||||

See accompanying notes to financial statements.

8

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

| Number of Shares | Value | ||||||||||

Sweden – 5.4% (cont) | |||||||||||

108,000 | Trelleborg Manufacturer of Sealing, Dampening & Protective Solutions for Industry | $ | 2,096,044 | ||||||||

31,495,981 | |||||||||||

Denmark – 3.7% | |||||||||||

169,227 | SimCorp Software for Investment Managers | 9,541,934 | |||||||||

136,724 | Novozymes Industrial Enzymes | 6,546,193 | |||||||||

59,000 | William Demant Holding (a) Manufacture & Distribution of Hearing Aids & Diagnostic Equipment | 5,620,016 | |||||||||

21,708,143 | |||||||||||

Netherlands – 3.5% | |||||||||||

181,144 | Aalberts Industries Flow Control & Heat Treatment | 6,241,451 | |||||||||

54,000 | Gemalto (b) Digital Security Solutions | 3,240,110 | |||||||||

161,387 | Brunel Temporary Specialist & Energy Staffing | 2,939,316 | |||||||||

26,669 | Core Labs (b) Oil & Gas Reservoir Consulting | 2,899,987 | |||||||||

130,843 | Arcadis Engineering Consultants | 2,630,380 | |||||||||

60,905 | Vopak Operator of Petroleum & Chemical Storage Terminals | 2,622,863 | |||||||||

20,574,107 | |||||||||||

Spain – 3.0% | |||||||||||

1,430,718 | Distribuidora Internacional de Alimentación Discount Retailer in Spain & Latin America | 8,438,508 | |||||||||

716,279 | Prosegur Security Guards | 3,298,747 | |||||||||

53,000 | Viscofan Sausage Casings Maker | 3,197,097 | |||||||||

83,000 | Bolsas y Mercados Españoles Spanish Stock Markets | 2,797,054 | |||||||||

17,731,406 | |||||||||||

| Number of Shares | Value | ||||||||||

France – 2.3% | |||||||||||

333,000 | Elior Contract Catering & Concession Services | $ | 6,976,557 | ||||||||

127,392 | Eutelsat Fixed Satellite Services | 3,814,174 | |||||||||

8,328 | Eurofins Scientific Food, Pharmaceuticals & Materials Screening & Testing | 2,904,975 | |||||||||

13,695,706 | |||||||||||

Switzerland – 2.2% | |||||||||||

18,384 | Partners Group (b) Private Markets Asset Management | 6,611,515 | |||||||||

10,581 | INFICON Gas Detection Instruments | 3,373,451 | |||||||||

26,700 | Panalpina Welttransport Holding Air & Sea Freight Forwarding | 2,980,971 | |||||||||

12,965,937 | |||||||||||

Finland – 1.9% | |||||||||||

325,189 | Tikkurila Decorative & Industrial Paint in Scandinavia, Central & Eastern Europe | 5,693,259 | |||||||||

116,251 | Konecranes (b) Manufacture & Service of Industrial Cranes & Port Handling Equipment | 2,877,296 | |||||||||

651,561 | Sponda Office, Retail & Logistics Properties | 2,767,573 | |||||||||

11,338,128 | |||||||||||

Norway – 1.3% | |||||||||||

610,594 | Atea Nordic IT Hardware/Software Reseller & Integrator | 5,042,974 | |||||||||

336,507 | Orkla Food & Brands, Aluminum, Chemicals Conglomerate | 2,654,677 | |||||||||

7,697,651 | |||||||||||

Italy – 0.9% | |||||||||||

59,000 | Industria Macchine Automatiche (b) Food & Drugs Packaging & Machinery | 3,062,561 | |||||||||

750,000 | Hera Northern Italian Utility | 1,987,648 | |||||||||

5,050,209 | |||||||||||

See accompanying notes to financial statements.

9

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

| Number of Shares | Value | ||||||||||

Kazakhstan – 0.4% | |||||||||||

432,778 | Halyk Savings Bank of Kazakhstan – GDR Retail Bank & Insurer in Kazakhstan | $ | 2,142,251 | ||||||||

Belgium – 0.1% | |||||||||||

22,378 | EVS Broadcast Equipment Digital Live Mobile Production Software & Systems | 705,259 | |||||||||

Total Europe | 254,203,507 | ||||||||||

Asia – 41.2% | |||||||||||

Japan – 20.9% | |||||||||||

157,520 | Milbon Hair Products for Salons | 6,431,532 | |||||||||

120,400 | FamilyMart Convenience Store Operator | 5,602,799 | |||||||||

281,100 | Aeon Mall Suburban Shopping Mall Developer, Owner & Operator | 4,821,462 | |||||||||

153,000 | Glory Currency Handling Systems & Related Equipment | 4,697,360 | |||||||||

229,000 | Doshisha Consumer Goods Wholesaler | 4,619,046 | |||||||||

90,700 | Seria 100 Yen Discount Stores | 4,393,593 | |||||||||

305,000 | Ushio Industrial Light Sources | 4,205,916 | |||||||||

71,240 | Ariake Japan Commercial Soup & Sauce Extracts | 3,941,258 | |||||||||

230,000 | Daiseki Waste Disposal & Recycling | 3,666,466 | |||||||||

1,320,000 | IHI Industrial Conglomerates | 3,643,858 | |||||||||

89,000 | Nakanishi Dental Tools & Machinery | 3,468,836 | |||||||||

208,200 | Santen Pharmaceutical Specialty Pharma (Ophthalmic Medicine) | 3,427,684 | |||||||||

25,150 | Hirose Electric Electrical Connectors | 3,044,966 | |||||||||

66,000 | Asahi Intecc Medical Guidewires for Surgery | 3,032,964 | |||||||||

| Number of Shares | Value | ||||||||||

123,000 | Park24 | $ | 2,979,974 | ||||||||

Parking Lot Operator | |||||||||||

244,000 | Yamaguchi Financial Group Regional Bank in Yamaguchi, Fukuoka & Hiroshima | 2,890,719 | |||||||||

78,000 | JIN (b) Eyeglasses Retailer | 2,876,963 | |||||||||

821,000 | Aozora Bank Commercial Bank | 2,865,145 | |||||||||

602,000 | Ebara Pumps, Compressors, Turbines & Related Products & Services | 2,860,792 | |||||||||

362,000 | NOF Specialty Chemicals, Life Science & Rocket Fuels | 2,784,774 | |||||||||

28,900 | Disco Semiconductor Dicing & Grinding Equipment | 2,721,556 | |||||||||

119,000 | NGK Insulators Ceramic Products for Auto, Power & Electronics | 2,682,283 | |||||||||

99,300 | NGK Spark Plug Automobile Parts | 2,614,417 | |||||||||

47,400 | OBIC Computer Software | 2,509,102 | |||||||||

515 | Kenedix Office Investment Tokyo Mid-size Office REIT | 2,407,640 | |||||||||

544,000 | Seven Bank ATM Processing Services | 2,385,711 | |||||||||

105,000 | Aeon Financial Service Diversified Consumer-related Finance Company in Japan | 2,345,566 | |||||||||

33,200 | Nippon Shokubai Producer of Acrylic Acid & Super Absorbent Polymers Used in Disposable Diapers | 2,310,224 | |||||||||

130,200 | Kintetsu World Express Airfreight Logistics | 2,291,157 | |||||||||

63,500 | Toto Toilets & Bathroom Fittings | 2,230,884 | |||||||||

90,692 | Capcom Packaged, Online & Mobile Games | 2,186,926 | |||||||||

432 | Industrial & Infrastructure Fund Industrial REIT in Japan | 2,061,426 | |||||||||

102,700 | OSG Consumable Cutting Tools | 1,941,545 | |||||||||

See accompanying notes to financial statements.

10

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

| Number of Shares | Value | ||||||||||

Japan – 20.9% (cont) | |||||||||||

74,300 | Yonex (b) Branded Sporting Goods Manufacturer | $ | 1,909,523 | ||||||||

219,900 | Relia Call Center Operator | 1,886,780 | |||||||||

95,100 | Aica Kogyo Laminated Sheets, Building Materials & Chemical Adhesives | 1,868,754 | |||||||||

27,000 | Hoshizaki Electric Commercial Kitchen Equipment | 1,678,463 | |||||||||

37,000 | Japan Airport Terminal Airport Terminal Operator at Haneda | 1,637,955 | |||||||||

92,700 | iStyle Cosmetics Review Portal & Retailer | 1,637,783 | |||||||||

174,000 | Sega Sammy Holdings Gaming Software/Hardware & Leisure Facilities | 1,627,482 | |||||||||

23,600 | Hikari Tsushin Office IT/Mobiles/Insurance Distribution | 1,607,156 | |||||||||

70,800 | Tamron Camera Lenses | 1,306,192 | |||||||||

36,300 | Icom Two Way Radio Communication Equipment | 754,485 | |||||||||

122,859,117 | |||||||||||

China – 3.6% | |||||||||||

2,284,000 | CAR Inc (a) (b) Consolidator of Chinese Auto Rental Sector | 3,763,676 | |||||||||

107,039 | BitAuto – ADR (a) Automotive Information Website for Buyers & Dealers | 3,027,063 | |||||||||

1,804,000 | TravelSky Technology Chinese Air Travel Transaction Processor | 2,953,690 | |||||||||

7,180,000 | Sihuan Pharmaceutical Holdings Group (c) Chinese Generic Drug Manufacturer | 2,776,146 | |||||||||

93,000 | 51job – ADR (a) (b) Integrated Human Resource Services | 2,739,780 | |||||||||

4,536,000 | NewOcean Energy Southern China Liquefied Petroleum Gas Distributor | 1,767,107 | |||||||||

8,300,000 | Jiangnan Group Cable & Wire Manufacturer | 1,621,744 | |||||||||

| Number of Shares | Value | ||||||||||

3,188,000 | AMVIG Holdings | $ | 1,324,554 | ||||||||

Chinese Tobacco Packaging Material Supplier | |||||||||||

945,000 | Phoenix Healthcare Group Private Hospital Management Group | 1,100,441 | |||||||||

21,074,201 | |||||||||||

Taiwan – 3.5% | |||||||||||

400,203 | Voltronic Power Uninterruptible Power Supply Products | 5,935,369 | |||||||||

1,900,000 | Far EasTone Telecom Mobile Operator in Taiwan | 3,904,890 | |||||||||

320,000 | Silergy Chinese Provider of Analog & Mixed Digital Integrated Circuits | 3,275,760 | |||||||||

160,000 | St. Shine Optical Disposable Contact Lens Original Equipment Manufacturer | 3,202,276 | |||||||||

170,000 | Ginko International Contact Lens Maker in China | 2,239,811 | |||||||||

302,349 | Advantech Industrial PC & Components | 1,936,180 | |||||||||

20,494,286 | |||||||||||

Korea – 3.1% | |||||||||||

191,600 | Koh Young Technology Inspection Systems for Printed Circuit Boards | 6,263,456 | |||||||||

11,707 | KCC Paint & Housing Material Manufacturer | 4,129,872 | |||||||||

16,771 | CJ Corp Holding Company of Korean Consumer Conglomerate | 3,562,282 | |||||||||

72,398 | Korea Investment Holdings Brokerage & Asset Management | 3,025,390 | |||||||||

51,770 | LF Corp Apparel Design & Retail | 1,186,032 | |||||||||

18,167,032 | |||||||||||

India – 2.6% | |||||||||||

1,150,794 | Zee Entertainment Enterprises Indian Programmer of Pay Television Content | 7,586,015 | |||||||||

129,000 | Container Corporation of India Railway Cargo Services | 2,556,783 | |||||||||

158,970 | United Breweries Indian Brewer | 2,270,317 | |||||||||

See accompanying notes to financial statements.

11

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

| Number of Shares | Value | ||||||||||

India – 2.6% (cont) | |||||||||||

152,560 | Colgate Palmolive India Consumer Products in Oral Care | $ | 2,238,398 | ||||||||

43,941 | Amara Raja Indian Maker of Auto & Industrial Batteries, Mostly for the Replacement Market | 570,438 | |||||||||

15,221,951 | |||||||||||

Hong Kong – 2.5% | |||||||||||

3,000,000 | Vitasoy International Hong Kong Soy Food Brand | 6,154,799 | |||||||||

5,000,000 | Value Partners Mutual Fund Management | 5,811,747 | |||||||||

994,000 | Samsonite International Mass Market Luggage & Travel Accessories | 2,978,997 | |||||||||

14,945,543 | |||||||||||

Singapore – 2.5% | |||||||||||

950,000 | Singapore Exchange Singapore Equity & Derivatives Market Operator | 5,137,998 | |||||||||

8,400,000 | China Everbright Water (a) Waste Water Treatment Operator | 3,632,581 | |||||||||

3,300,000 | Mapletree Commercial Trust Retail & Office Property Landlord | 3,021,333 | |||||||||

2,900,000 | SIIC Environment (a) Waste Water Treatment Operator | 1,561,574 | |||||||||

707,000 | Petra Foods Chocolate Manufacturer in Southeast Asia | 1,046,151 | |||||||||

14,399,637 | |||||||||||

Indonesia – 0.9% | |||||||||||

1,260,900 | Matahari Department Store Department Store Chain in Indonesia | 1,596,216 | |||||||||

4,169,000 | Link Net (a) Fixed Broadband & Cable TV Service Provider | 1,200,611 | |||||||||

5,185,021 | Surya Citra Media Free to Air TV Station in Indonesia | 1,156,182 | |||||||||

2,431,000 | Tower Bersama Infrastructure (a) Communications Towers | 1,028,356 | |||||||||

4,859,200 | MNC Sky Vision (a) Satellite Pay TV Operator in Indonesia | 470,586 | |||||||||

5,451,951 | |||||||||||

| Number of Shares | Value | ||||||||||

Thailand – 0.6% | |||||||||||

357,000 | Airports of Thailand Airport Operator of Thailand | $ | 3,413,152 | ||||||||

Philippines – 0.6% | |||||||||||

2,504,000 | Puregold Price Club Supermarket Operator in the Philippines | 1,846,537 | |||||||||

812,000 | Robinsons Retail Holdings Multi-format Retailer in the Philippines | 1,087,903 | |||||||||

7,468,300 | Melco Crown (Philippines) Resorts (a) Integrated Resort Operator in Manila | 361,485 | |||||||||

3,295,925 | |||||||||||

Cambodia – 0.4% | |||||||||||

3,946,000 | Nagacorp Casino & Entertainment Complex in Cambodia | 2,485,580 | |||||||||

Total Asia | 241,808,375 | ||||||||||

Other Countries – 11.0% | |||||||||||

Canada – 4.8% | |||||||||||

53,446 | CCL Industries Global Label Converter | 8,666,387 | |||||||||

129,000 | Vermilion Energy (b) Canadian Exploration & Production Company | 3,506,316 | |||||||||

268,267 | CAE Flight Simulator Equipment & Training Centers | 2,976,005 | |||||||||

101,000 | Keyera (b) Integrated Supply of Hydrocarbon Processing, Transport & Storage | 2,938,686 | |||||||||

41,250 | Onex Capital Private Equity | 2,528,601 | |||||||||

159,000 | PrairieSky Royalty (b) Canadian Owner of Oil & Gas Mineral Interests | 2,518,812 | |||||||||

104,849 | ShawCor Oil & Gas Pipeline Products | 2,126,987 | |||||||||

190,995 | Rona Canadian Home Improvement Retailer | 1,704,696 | |||||||||

46,170 | Ag Growth Manufacturer of Augers & Grain Handling Equipment | 1,109,455 | |||||||||

28,075,945 | |||||||||||

See accompanying notes to financial statements.

12

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

| Number of Shares | Value | ||||||||||

Australia – 3.8% | |||||||||||

190,000 | Domino's Pizza Enterprises Domino's Pizza Operator in Australia & New Zealand | $ | 7,927,454 | ||||||||

5,300,000 | Spotless Facility Management & Catering Company | 4,152,780 | |||||||||

1,001,381 | IAG General Insurance Provider | 4,021,558 | |||||||||

279,000 | Amcor Global Leader in Flexible & Rigid Packaging | 2,710,551 | |||||||||

340,000 | Estia Health Residential Aged Care Operator | 1,795,401 | |||||||||

230,000 | Challenger Financial Annuity Provider in Australia | 1,449,548 | |||||||||

22,057,292 | |||||||||||

South Africa – 0.8% | |||||||||||

710,581 | Coronation Fund Managers South African Fund Manager | 2,433,696 | |||||||||

935,177 | Rand Merchant Insurance Directly Sold Property & Casualty Insurance; Holdings in other Insurers | 2,337,749 | |||||||||

4,771,445 | |||||||||||

New Zealand – 0.6% | |||||||||||

900,000 | Auckland International Airport Auckland Airport Operator | 3,530,797 | |||||||||

Egypt – 0.5% | |||||||||||

627,736 | Commercial International Bank of Egypt Private Universal Bank in Egypt | 3,053,680 | |||||||||

United States – 0.5% | |||||||||||

110,000 | Bladex Latin American Trade Financing House | 2,852,300 | |||||||||

Total Other Countries | 64,341,459 | ||||||||||

Latin America – 1.7% | |||||||||||

Mexico – 0.9% | |||||||||||

25,000 | Grupo Aeroportuario del Sureste – ADR Mexican Airport Operator | 3,516,750 | |||||||||

1,121,000 | Qualitas (a) Auto Insurer in Mexico & Central America | 1,412,755 | |||||||||

4,929,505 | |||||||||||

| Number of Shares | Value | ||||||||||

Brazil – 0.3% | |||||||||||

300,000 | Localiza Rent a Car Car Rental | $ | 1,882,085 | ||||||||

Guatemala – 0.3% | |||||||||||

195,010 | Tahoe Resources Silver & Gold Projects in Guatemala & Peru | 1,686,977 | |||||||||

Uruguay – 0.2% | |||||||||||

230,870 | Union Agriculture Group (a) (c) (d) Farmland Operator in Uruguay | 1,172,819 | |||||||||

Total Latin America | 9,671,386 | ||||||||||

| Total Equities (Cost: $477,584,893) – 97.2% | 570,024,727 | (e) | |||||||||

Short-Term Investments – 2.9% | |||||||||||

17,415,390 | JPMorgan U.S. Government Money Market Fund, IM Shares (7 day yield of 0.01%) | 17,415,390 | |||||||||

| Total Short-Term Investments (Cost: $17,415,390) – 2.9% | 17,415,390 | ||||||||||

Securities Lending Collateral – 3.9% | |||||||||||

22,917,951 | Dreyfus Government Cash Management Fund, Institutional Shares (7 day yield of 0.03%) (f) | 22,917,951 | |||||||||

| Total Securities Lending Collateral (Cost: $22,917,951) – 3.9% | 22,917,951 | ||||||||||

| Total Investments (Cost: $517,918,234) (g) – 104.0% | 610,358,068 | ||||||||||

| Obligation to Return Collateral for Securities Loaned – (3.9)% | (22,917,951 | ) | |||||||||

Cash and Other Assets Less Liabilities – (0.1)% | (811,310 | ) | |||||||||

Net Assets – 100.0% | $ | 586,628,807 | |||||||||

ADR – American Depositary Receipts

GDR – Global Depositary Receipts

REIT – Real Estate Investment Trust

See accompanying notes to financial statements.

13

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

Notes to Statement of Investments

(a) Non-income producing security.

(b) All or a portion of this security was on loan at December 31, 2015. The total market value of securities on loan at December 31, 2015 was $21,850,755.

(c) Illiquid security.

(d) Denotes a restricted security, which is subject to restrictions on resale under federal securities laws. This security is valued at fair value determined in good faith under consistently applied procedures established by the Fund's Board of Trustees. At December 31, 2015, the market value of this security amounted to $1,172,819, which represented 0.20% of total net assets. Additional information on this security is as follows:

Security | Acquisition Dates | Shares | Cost | Value | |||||||||||||||

Union Agriculture Group | 12/8/10 - 6/27/12 | 230,870 | $ | 2,649,999 | $ | 1,172,819 | |||||||||||||

(e) On December 31, 2015, the Fund's total equity investments were denominated in currencies as follows:

Currency | Value | Percentage of Net Assets | |||||||||

Japanese Yen | $ | 122,859,117 | 20.9 | ||||||||

Euro | 99,133,140 | 16.9 | |||||||||

British Pound | 76,160,417 | 13.0 | |||||||||

Hong Kong Dollar | 32,738,481 | 5.6 | |||||||||

Swedish Krona | 31,495,981 | 5.4 | |||||||||

Canadian Dollar | 29,762,922 | 5.1 | |||||||||

| Other currencies less than 5% of total net assets | 177,874,669 | 30.3 | |||||||||

Total Equities | $ | 570,024,727 | 97.2 | ||||||||

(f) Investment made with cash collateral received from securities lending activity.

(g) At December 31, 2015, for federal income tax purposes, the cost of investments was $522,809,006 and net unrealized appreciation was $87,549,062 consisting of gross unrealized appreciation of $129,446,972 and gross unrealized depreciation of $41,897,910.

Fair Value Measurements

Various inputs are used in determining the value of the Fund's investments, following the input prioritization hierarchy established by accounting principles generally accepted in the United States of America (GAAP). These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical securities

• Level 2 – prices determined using other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk and others)

• Level 3 – prices determined using significant unobservable inputs where quoted prices or observable inputs are unavailable or less reliable (including management's own assumptions about the factors market participants would use in pricing an investment)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Examples of the types of securities in which the Fund would typically invest and how they are classified within this hierarchy are as follows. Typical Level 1 securities include exchange traded domestic equities, mutual funds whose NAVs are published each day and exchange traded foreign equities that are not statistically fair valued. Typical Level 2 securities include exchange traded foreign equities that are statistically fair valued, forward foreign currency exchange contracts and short-term investments valued at amortized cost. Additionally, securities fair valued by CWAM's Valuation Committee (the Committee) that rely on significant observable inputs are also included in Level 2. Typical Level 3 securities include any security fair valued by the Committee that relies on significant uunobservable inputs.

The Committee is responsible for applying the Trust's Portfolio Pricing Policy and the CWAM pricing procedures (the Policies), which are approved by and subject to the oversight of the Board.

The Committee meets as necessary, and no less frequently than quarterly, to determine fair values for securities for which market quotations are not readily available or for which the investment manager believes that available market quotations are unreliable. The Committee also reviews the continuing appropriateness of the Policies. In circumstances where a security has been fair valued, the Committee will also review the continuing appropriateness of the current value of the security. The Policies address, among other things: circumstances under which market quotations will be deemed readily available; selection of third party pricing vendors; appropriate pricing methodologies; events that require fair valuation and fair value techniques; circumstances under which securities will be deemed to pose a potential for stale pricing, including when securities are illiquid, restricted, or in default; and certain delegations of authority to determine fair values to the Fund's investment manager. The Committee may also meet to discuss additional valuation matters, which may include review of back-testing results, review of time-sensitive information or approval of other valuation related actions, and to review the appropriateness of the Policies.

For investments categorized as Level 3, the significant unobservable inputs used in the fair value measurement of the Fund's securities may include: (i) data specific to the issuer or comparable issuers, (ii) general market or specific sector news and (iii) quoted prices and specific or similar security transactions. The Committee considers this data and any changes from prior periods in order to assess the reasonableness of observable and unobservable inputs, any assumptions or internal models used to value those securities and changes in fair value. Significant changes in any of these factors could result in lower or higher fair value measurements. Various factors impact the frequency of monitoring (which may occur as often as daily), however the Committee may determine that changes to inputs, assumptions and models are not required with the same frequency.

See accompanying notes to financial statements.

14

Wanger International 2015 Annual Report

Wanger International

Statement of Investments, December 31, 2015

The following table summarizes the inputs used, as of December 31, 2015, in valuing the Fund's assets:

Investment Type | Quoted Prices (Level 1) | Other Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | |||||||||||||||

Equities | |||||||||||||||||||

Europe | $ | 2,899,987 | $ | 251,303,520 | $ | — | $ | 254,203,507 | |||||||||||

Asia | 5,766,843 | 233,265,386 | 2,776,146 | 241,808,375 | |||||||||||||||

Other Countries | 30,928,245 | 33,413,214 | — | 64,341,459 | |||||||||||||||

Latin America | 8,498,567 | — | 1,172,819 | 9,671,386 | |||||||||||||||

Total Equities | 48,093,642 | 517,982,120 | 3,948,965 | 570,024,727 | |||||||||||||||

| Total Short-Term Investments | 17,415,390 | — | — | 17,415,390 | |||||||||||||||

| Total Securities Lending Collateral | 22,917,951 | — | — | 22,917,951 | |||||||||||||||

Total Investments | $ | 88,426,983 | $ | 517,982,120 | $ | 3,948,965 | $ | 610,358,068 | |||||||||||

The Fund's assets assigned to the Level 2 input category are generally valued using a market approach, in which a security's value is determined through its correlation to prices and information from observable market transactions for similar or identical assets. Foreign equities are generally valued at the last sale price on the foreign exchange or market on which they trade. The Fund may use a statistical fair valuation model, in accordance with the policy adopted by the Board, provided by an independent third party to value securities principally traded in foreign markets in order to adjust for possible stale pricing that may occur between the close of the foreign exchanges and the time for valuation. These models take into account available market data including intraday index, ADR, and ETF movements.

There were no transfers of financial assets between Levels 1 and 2 during the period.

The Fund does not hold any significant investments (greater than one percent of net assets) categorized as Level 3.

Financial assets were transferred from Level 2 to Level 3 as trading halted during the period. As a result, as of period end, the Committee determined to value the security(s) under consistently applied procedures established by and under the general supervision of the Board.

The following table shows transfers between Level 2 and Level 3 of the fair value hierarchy:

Transfers In | Transfers Out | ||||||||||||||

| Level 2 | Level 3 | Level 2 | Level 3 | ||||||||||||

| $ | — | $ | 4,496,473 | $ | 4,496,473 | $ | — | ||||||||

Transfers into and/or out of Level 3 are determined based on the fair value at the beginning of the period for security positions held throughout the period.

Certain securities classified as Level 3 are fair valued by the Committee using a market approach, as determined in good faith under consistently applied procedures established by and under the general supervision of the Board. To determine fair value for these securities, for which no market exists, the Committee utilizes the valuation technique it deems most appropriate in the circumstances, using some unobservable inputs, which may include, but are not limited to estimated earnings of the company and the position of the security within the company's capital structure. The Committee also may use some observable inputs, which may include, but are not limited to, trades of similar securities and market

multiples derived from a set of comparable companies. Significant increases or decreases to any of these inputs could result in a significantly lower or higher fair value measurement.

See accompanying notes to financial statements.

15

Wanger International 2015 Annual Report

Wanger International (Unaudited)

Portfolio Diversification, December 31, 2015

At December 31, 2015, the Fund's portfolio investments as a percentage of net assets were diversified as follows:

Value | Percentage of Net Assets | ||||||||||

Industrial Goods & Services | |||||||||||

Machinery | $ | 38,227,630 | 6.5 | ||||||||

Industrial Materials & Specialty Chemicals | 34,362,823 | 5.9 | |||||||||

Other Industrial Services | 32,392,244 | 5.5 | |||||||||

Outsourcing Services | 22,320,857 | 3.8 | |||||||||

Conglomerates | 19,502,082 | 3.3 | |||||||||

Electrical Components | 11,554,909 | 2.0 | |||||||||

Construction | 6,570,137 | 1.1 | |||||||||

Water | 5,194,155 | 0.9 | |||||||||

170,124,837 | 29.0 | ||||||||||

Consumer Goods & Services | |||||||||||

Retail | 42,956,825 | 7.3 | |||||||||

Food & Beverage | 21,036,932 | 3.6 | |||||||||

Restaurants | 18,854,087 | 3.2 | |||||||||

Nondurables | 15,097,919 | 2.6 | |||||||||

Casinos & Gaming | 12,811,432 | 2.2 | |||||||||

Consumer Goods Distribution | 11,459,704 | 2.0 | |||||||||

Travel | 5,645,761 | 1.0 | |||||||||

Leisure Products | 4,888,519 | 0.8 | |||||||||

Other Durable Goods | 3,184,855 | 0.5 | |||||||||

Consumer Electronics | 1,306,192 | 0.2 | |||||||||

Apparel | 1,186,032 | 0.2 | |||||||||

138,428,258 | 23.6 | ||||||||||

Information | |||||||||||

Business Software | 18,946,567 | 3.2 | |||||||||

Financial Processors | 14,176,292 | 2.4 | |||||||||

Internet Related | 13,351,367 | 2.3 | |||||||||

Computer Hardware & Related Equipment | 11,816,919 | 2.0 | |||||||||

Instrumentation | 10,962,186 | 1.9 | |||||||||

Entertainment Programming | 7,586,015 | 1.3 | |||||||||

Semiconductors & Related Equipment | 5,997,316 | 1.0 | |||||||||

Mobile Communications | 5,687,730 | 1.0 | |||||||||

Computer Services | 5,042,974 | 0.9 | |||||||||

Satellite Broadcasting & Services | 4,284,760 | 0.7 | |||||||||

TV Broadcasting | 3,435,224 | 0.6 | |||||||||

Consumer Software | 2,186,925 | 0.4 | |||||||||

Business Information & Marketing Services | 1,886,780 | 0.3 | |||||||||

Telephone & Data Services | 1,834,421 | 0.3 | |||||||||

Cable TV | 1,200,611 | 0.2 | |||||||||

108,396,087 | 18.5 | ||||||||||

Value | Percentage of Net Assets | ||||||||||

Finance | |||||||||||

Banks | $ | 18,535,372 | 3.2 | ||||||||

Insurance | 16,360,942 | 2.8 | |||||||||

Brokerage & Money Management | 14,856,958 | 2.5 | |||||||||

Diversified Financial Companies | 3,025,390 | 0.5 | |||||||||

Financial Processors | 2,797,053 | 0.5 | |||||||||

Finance Companies | 2,528,601 | 0.4 | |||||||||

58,104,316 | 9.9 | ||||||||||

Other Industries | |||||||||||

Real Estate | 20,259,658 | 3.5 | |||||||||

Transportation | 14,655,437 | 2.5 | |||||||||

Containers & Packaging | 2,872,137 | 0.5 | |||||||||

Regulated Utilities | 1,987,648 | 0.3 | |||||||||

39,774,880 | 6.8 | ||||||||||

Health Care | |||||||||||

Medical Equipment & Devices | 12,121,816 | 2.0 | |||||||||

Pharmaceuticals | 10,909,301 | 1.9 | |||||||||

Medical Supplies | 8,028,834 | 1.4 | |||||||||

Health Care Services | 1,795,402 | 0.3 | |||||||||

Hospital Management | 1,100,441 | 0.2 | |||||||||

33,955,794 | 5.8 | ||||||||||

Energy & Minerals | |||||||||||

Oil Refining, Marketing & Distribution | 7,328,657 | 1.2 | |||||||||

Oil & Gas Producers | 6,025,128 | 1.0 | |||||||||

Mining | 4,586,964 | 0.8 | |||||||||

Oil Services | 2,126,987 | 0.4 | |||||||||

Agricultural Commodities | 1,172,819 | 0.2 | |||||||||

21,240,555 | 3.6 | ||||||||||

Total Equities: | 570,024,727 | 97.2 | |||||||||

Short-Term Investments: | 17,415,390 | 2.9 | |||||||||

Securities Lending Collateral: | 22,917,951 | 3.9 | |||||||||

Total Investments: | 610,358,068 | 104.0 | |||||||||

| Obligation to Return Collateral for Securities Loaned: | (22,917,951 | ) | (3.9 | ) | |||||||

| Cash and Other Assets Less Liabilities: | (811,310 | ) | (0.1 | ) | |||||||

Net Assets: | $ | 586,628,807 | 100.0 | % | |||||||

See accompanying notes to financial statements.

16

Wanger International 2015 Annual Report

Statement of Assets and Liabilities

December 31, 2015

Assets: | |||||||

Investments, at cost | $ | 517,918,234 | |||||

| Investments, at value (including securities on loan of $21,850,755) | $ | 610,358,068 | |||||

Foreign currency (cost of $262,041) | 261,777 | ||||||

Receivable for: | |||||||

Investments sold | 415,459 | ||||||

Fund shares sold | 52,867 | ||||||

Securities lending income | 25,629 | ||||||

Dividends | 612,531 | ||||||

Foreign tax reclaims | 371,153 | ||||||

Regulatory Settlements (Note 8) | 131,912 | ||||||

Trustees' deferred compensation plan | 161,437 | ||||||

Prepaid expenses | 9,877 | ||||||

Total Assets | 612,400,710 | ||||||

Liabilities: | |||||||

Collateral on securities loaned | 22,917,951 | ||||||

Payable for: | |||||||

Investments purchased | 322,974 | ||||||

Fund shares redeemed | 2,149,917 | ||||||

Investment advisory fee | 15,097 | ||||||

Administration fee | 811 | ||||||

Transfer agent fee | 2 | ||||||

Trustees' fees | 2,682 | ||||||

Custody fee | 66,493 | ||||||

Reports to shareholders | 61,261 | ||||||

Chief compliance officer expenses | 5,690 | ||||||

Trustees' deferred compensation plan | 161,437 | ||||||

Other liabilities | 67,588 | ||||||

Total Liabilities | 25,771,903 | ||||||

Net Assets | $ | 586,628,807 | |||||

Composition of Net Assets: | |||||||

Paid-in capital | $ | 453,175,972 | |||||

Overdistributed net investment income | (1,515,320 | ) | |||||

Accumulated net realized gain | 42,564,991 | ||||||

Net unrealized appreciation (depreciation) on: | |||||||

Investments | 92,439,834 | ||||||

Foreign currency translations | (36,670 | ) | |||||

Net Assets | $ | 586,628,807 | |||||

Fund Shares Outstanding | 22,288,698 | ||||||

| Net asset value, offering price and redemption price per share | $ | 26.32 | |||||

Statement of Operations

For the Year Ended December 31, 2015

Investment Income: | |||||||

Dividends (net foreign taxes withheld of $1,569,158) | $ | 14,023,167 | |||||

Interest | 113,574 | ||||||

Income from securities lending—net | 221,271 | ||||||

Total Investment Income | 14,358,012 | ||||||

Expenses: | |||||||

Investment advisory fee | 5,931,518 | ||||||

Transfer agent fees | 520 | ||||||

Administration fee | 322,282 | ||||||

Trustees' fees | 48,828 | ||||||

Custody fees | 264,957 | ||||||

Reports to shareholders | 351,278 | ||||||

Audit fees | 71,031 | ||||||

Legal fees | 111,432 | ||||||

Chief compliance officer expenses | 29,572 | ||||||

Commitment fee for line of credit (Note 5) | 15,900 | ||||||

Other expenses | 45,149 | ||||||

Total Expenses | 7,192,467 | ||||||

Net Investment Income | 7,165,545 | ||||||

Net Realized and Unrealized Gain (Loss) on Investments: | |||||||

Net realized gain (loss) on: | |||||||

Investments | 50,409,289 | ||||||

Foreign currency translations | (346,363 | ) | |||||

Net realized gain | 50,062,926 | ||||||

| Net change in unrealized appreciation (depreciation) on: | |||||||

Investments | (55,119,081 | ) | |||||

Foreign currency translations | 29,388 | ||||||

Net change in unrealized depreciation | (55,089,693 | ) | |||||

Net realized and unrealized loss | (5,026,767 | ) | |||||

Net Increase in Net Assets from Operations | $ | 2,138,778 | |||||

See accompanying notes to financial statements.

17

Wanger International 2015 Annual Report

Statements of Changes in Net Assets

Year Ended December 31, | |||||||||||

Increase (Decrease) in Net Assets | 2015 | 2014 | |||||||||

Operations: | |||||||||||

Net investment income | $ | 7,165,545 | $ | 8,213,120 | |||||||

Net realized gain (loss) on: | |||||||||||

Investments | 50,409,289 | 63,453,238 | |||||||||

Foreign currency translations | (346,363 | ) | (389,212 | ) | |||||||

Net change in unrealized appreciation (depreciation) on: | |||||||||||

Investments | (55,119,081 | ) | (101,516,032 | ) | |||||||

Foreign currency translations | 29,388 | (90,874 | ) | ||||||||

Options | — | (269,054 | ) | ||||||||

Net Increase (Decrease) in Net Assets from Operations | 2,138,778 | (30,598,814 | ) | ||||||||

Distributions to Shareholders From: | |||||||||||

Net investment income | (9,178,114 | ) | (10,651,101 | ) | |||||||

Net realized gains | (56,072,696 | ) | (82,758,323 | ) | |||||||

Total Distributions to Shareholders | (65,250,810 | ) | (93,409,424 | ) | |||||||

Share Transactions: | |||||||||||

Subscriptions | 12,302,455 | 23,205,601 | |||||||||

Distributions reinvested | 65,250,810 | 93,409,424 | |||||||||

Redemptions | (94,967,225 | ) | (110,560,733 | ) | |||||||

Net Increase (Decrease) from Share Transactions | (17,413,960 | ) | 6,054,292 | ||||||||

Proceeds from regulatory settlements (Note 8) | 131,912 | — | |||||||||

Total Decrease in Net Assets | (80,394,080 | ) | (117,953,946 | ) | |||||||

Net Assets: | |||||||||||

Beginning of period | 667,022,887 | 784,976,833 | |||||||||

End of period | $ | 586,628,807 | $ | 667,022,887 | |||||||

Overdistributed net investment income | $ | (1,515,320 | ) | $ | (5,231,819 | ) | |||||

See accompanying notes to financial statements.

18

Wanger International 2015 Annual Report

Financial Highlights

The following table is intended to help you understand the Fund's financial performance. Certain information reflects financial results for a single share held for the periods shown. Per share net investment income (loss) amounts are calculated based on average shares outstanding during the period. Total return assumes reinvestment of all dividends and distributions, if any. Total return does not reflect payment of the expenses that apply to the variable accounts or contract charges, if any. Total return and portfolio turnover are not annualized for periods of less than one year. The portfolio turnover rate is calculated without regard to purchase and sales transactions of short-term instruments and certain derivatives, if any. If such transactions were included, the Fund's portfolio turnover rate may be higher.

Year Ended December 31, | |||||||||||||||||||||||

Selected data for a share outstanding throughout each period | 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||||

Net Asset Value, Beginning of Period | $ | 29.07 | $ | 34.55 | $ | 31.19 | $ | 28.79 | $ | 36.16 | |||||||||||||

Income from Investment Operations: | |||||||||||||||||||||||

Net investment income | 0.31 | 0.36 | 0.39 | 0.46 | 0.42 | ||||||||||||||||||

Net realized and unrealized gain (loss) | (0.09 | ) | (1.56 | ) | 6.18 | 5.27 | (5.31 | ) | |||||||||||||||

Reimbursement from affiliate | — | — | — | — | 0.00 | (a) | |||||||||||||||||

Total from Investment Operations | 0.22 | (1.20 | ) | 6.57 | 5.73 | (4.89 | ) | ||||||||||||||||

Less Distributions to Shareholders: | |||||||||||||||||||||||

Net investment income | (0.41 | ) | (0.48 | ) | (0.88 | ) | (0.38 | ) | (1.64 | ) | |||||||||||||

Net realized gains | (2.57 | ) | (3.80 | ) | (2.33 | ) | (2.95 | ) | (0.84 | ) | |||||||||||||

Total Distributions to Shareholders | (2.98 | ) | (4.28 | ) | (3.21 | ) | (3.33 | ) | (2.48 | ) | |||||||||||||

Proceeds from regulatory settlements | 0.01 | — | — | — | — | ||||||||||||||||||

Net Asset Value, End of Period | $ | 26.32 | $ | 29.07 | $ | 34.55 | $ | 31.19 | $ | 28.79 | |||||||||||||

Total Return | 0.10 | %(c) | (4.40 | )% | 22.37 | % | 21.56 | %(b) | (14.62 | )%(b) | |||||||||||||

Ratios to Average Net Assets/Supplemental Data: | |||||||||||||||||||||||

Total gross expenses (d) | 1.12 | % | 1.05 | % | 1.07 | % | 1.08 | % | 1.06 | % | |||||||||||||

Total net expenses (d) | 1.12 | % | 1.05 | % | 1.07 | % | 1.05 | %(e) | 1.00 | %(e) | |||||||||||||

Net investment income | 1.11 | % | 1.10 | % | 1.19 | % | 1.51 | % | 1.25 | % | |||||||||||||

Portfolio turnover rate | 53 | % | 28 | % | 44 | % | 34 | % | 36 | % | |||||||||||||

Net assets, end of period (000s) | $ | 586,629 | $ | 667,023 | $ | 784,977 | $ | 702,667 | $ | 682,217 | |||||||||||||

Notes to Financial Highlights

(a) Rounds to zero.