Exhibit (c)(14)

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Project Rushmore Discussion Materials

February 28th, 2019

TUDORPICKERING HOLT & CO ENERGY INVESTMENT & MERCHANT BANKING

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Table of Contents

I. Situation Overview

II. Status Quo Management Projections Overview III. Abe Financial Analysis IV. Ulysses Financial Analysis V. Transaction Analysis

Appendix

Cost of Capital

2

TUDORPICKERING HOLT & CO ENERGY INVESTMENT & MERCHANT BANKING

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

I. Situation Overview

3

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

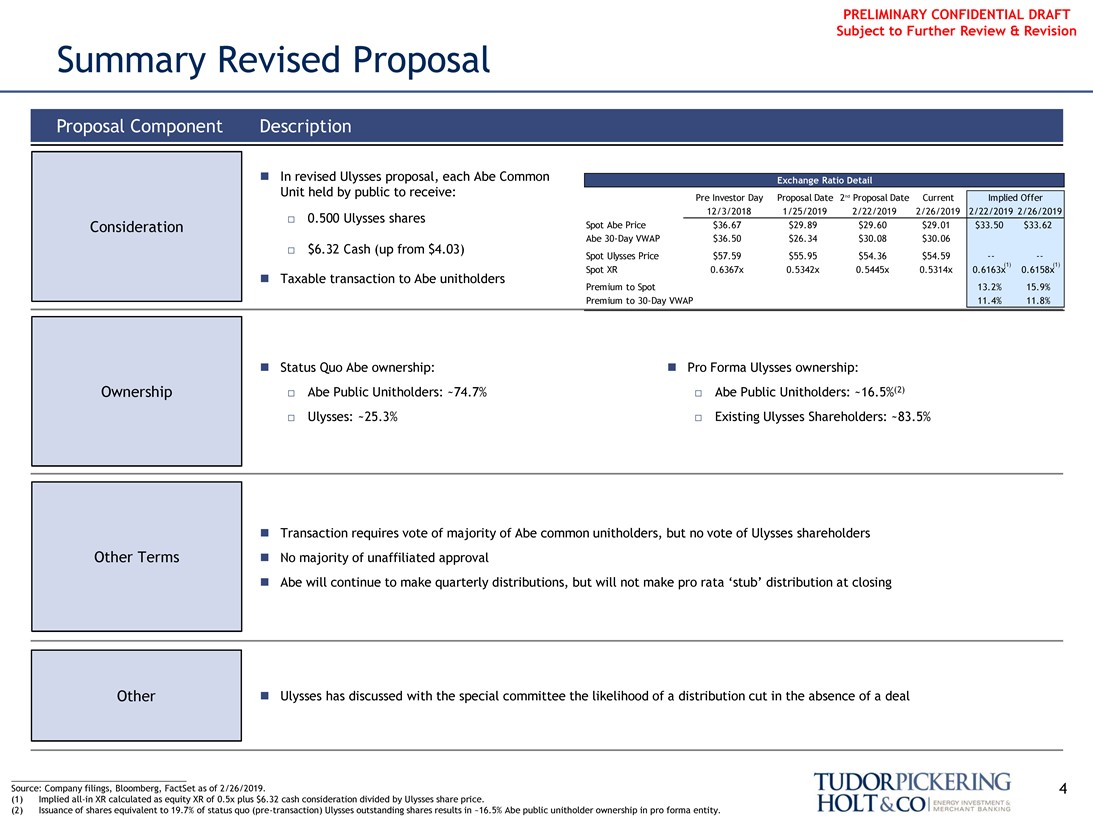

Summary Revised Proposal

∎ In revised Ulysses proposal, each Abe Common Unit held by public to receive:

Pre Investor Day Proposal Date 2 nd Proposal Date Current Implied Offer 12/3/2018 1/25/2019 2/22/2019 2/26/2019 2/22/2019 2/26/2019

â–¡ 0.500 Ulysses shares

Consideration Spot Abe Price $36.67 $29.89 $29.60 $29.01 $33.50 $33.62

â–¡ $6.32 Cash (up from $4.03) Abe30-Day VWAP $36.50 $26.34 $30.08 $30.06

Spot Ulysses Price $57.59 $55.95 $54.36 $54.59 -—-

(1) (1)

Spot XR 0.6367x 0.5342x 0.5445x 0.5314x 0.6163x 0.6158x

∎ Taxable transaction to Abe unitholders

Premium to Spot 13.2% 15.9% Premium to30-Day VWAP 11.4% 11.8%

∎ Status Quo Abe ownership:∎ Pro Forma Ulysses ownership:

Ownership Abe Public Unitholders: ~74.7% Abe Public Unitholders: ~16.5%(2)

Ulysses: ~25.3% Existing Ulysses Shareholders: ~83.5%

∎ Transaction requires vote of majority of Abe common unitholders, but no vote of Ulysses shareholders Other Terms∎ No majority of unaffiliated approval

∎ Abe will continue to make quarterly distributions, but will not make pro rata ‘stub’ distribution at closing

Other∎ Ulysses has discussed with the special committee the likelihood of a distribution cut in the absence of a deal

Source: Company filings, Bloomberg, FactSet as of 2/26/2019. 4 (1) Impliedall-in XR calculated as equity XR of 0.5x plus $6.32 cash consideration divided by Ulysses share price.

(2) Issuance of shares equivalent to 19.7% of status quo(pre-transaction) Ulysses outstanding shares results in ~16.5% Abe public unitholder ownership in pro forma entity.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

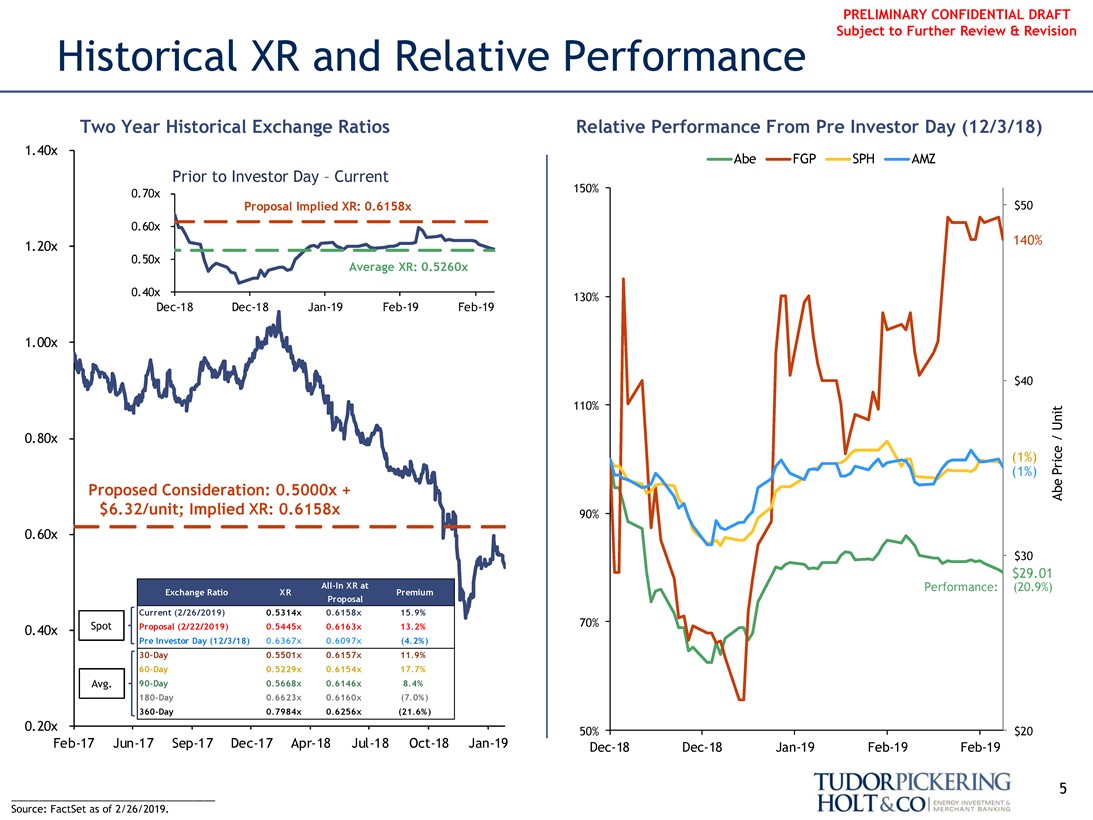

Historical XR and Relative Performance

Two Year Historical Exchange Ratios Relative Performance From Pre Investor Day (12/3/18)

1.40x

Abe FGP SPH AMZ

Prior to Investor Day – Current 150%

0.70x

Proposal Implied XR: 0.6158x $50

0.60x

1.20x 140%

0.50x

Average XR: 0.5260x

0.40x 130%Dec-18Dec-18Jan-19Feb-19Feb-19

1.00x

$40

110%

0.80x/ (1%) (1%) abe Price/unit

Proposed Consideration: 0.5000x + $6.32/unit; Implied XR: 0.6158x 90%

0.60x $30 $29.01

Performance: (20.9%)

Current (2/26/2019) 0.5314x 0.6158x 15.9% 70% 0.40x Spot Proposal (2/22/2019) 0.5445x 0.6163x 13.2% Pre Investor Day (12/3/18) 0.6367x 0.6097x (4.2%)30-Day 0.5501x 0.6157x 11.9%60-Day 0.5229x 0.6154x 17.7% Avg.90-Day 0.5668x 0.6146x 8.4%180-Day 0.6623x 0.6160x (7.0%)360-Day 0.7984x 0.6256x (21.6%)

0.20x 50% $20

Feb-17Jun-17Sep-17Dec-17Apr-18Jul-18Oct-18Jan-19Dec-18Dec-18Jan-19Feb-19Feb-19

5

_____________________________________ Source: FactSet as of 2/26/2019.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Post Investor Day Equity Analyst Commentary broker commentary

“With the challenging macro backdrop and leverage persistently above the Partnership’s 4.0x target, we believe the distribution at current levels is at risk… We revise our APU price target to $38 (from $42) based on our FY20e DPS of $3.80 and a target yield of 10.0% (vs. 9.0% previously).” – 11/12/2018

No distribution cut projected in model – 11/14/18

“That said, we do believe both our FY19 adjusted EBITDA estimate (which falls within the guidance range) and FY20 estimates are obtainable, and that distributions can meet our 2020 target of $3.82.” – 11/13/18

“On an independent basis, we see no need for APU to rein in its distribution and find its valuation attractive at present levels” – 11/30/2018 “Our FY19/FY20 distribution estimates of $3.80/$3.80 per unit yield coverage ratios of 1.04x/1.07x.” – 11/13/18 No distribution cut projected in model – 11/12/18 NA

NA

6

barclays wells fargo janney jefferies raymond james ubs j.p.morgan morningstar

_____________________________________ Source: Wall Street research.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Post Investor Day Equity Analyst Commentary broker commentary likely outcome stated

“As far as a potential APUbuy-in, we believe this remains a less likely scenario given UGI’s historical focus on a 50/50 split between its gas and LPG businesses, and the fact that an APUbuy-in would more heavily skew the company toward LPG. We also note that UGI’s investor base has traditionally been more heavily weighted toward utilities investors, as evidenced by the stock’s ~80$ weekly correlation

IDR Conversion with the XLU over the past three years (vs. ~10$ correlation between UGI/AMZ; APU is ~20$ correlated with the XLU and ~70% correlated with the AMZ), such that the valuation multiple might compress in abuy-in scenario. Lastly, abuy-in would also likely have tax consequences for legacy APU unitholders.” – 12/4/2018

“That said, with no clarity on the outcome of the distribution or even the MLP structure (and the market’s negative reaction to the aforementioned uncertainty), we expect the shares to trade at a higher yield until a decision on the aforementioned items is communicated.” – 12/13/2018

NA

“In terms of valuation, the units are currently yielding just over 12%, which appears to be pricing in some level of distribution cut. That may ultimately happen; then again it may not, particularly if the company hits its guidance range for the year.” – 2/7/2019

“Given the APU attributes noted previously (its improving financial position, lack of external pressure for a cut, etc.), the fact that a vote would likely be required as UGI’s LP ownership is only 26%, and the fact that units violently reacted to sell-side reports calling for a sharp distribution cut given the strategic review announced at the Investor Day, we believe any Committee negotiation would advocate for apre-Investor Day comparison of relative equity values” – 1/7/2019

Buy-In

“APU units fell >30% in the month following its Dec. 4th Investor Day as it was bumped from the Alerian MLP Index and several analysts have called for a distribution cut; we believe the calls for a cut are misguided and have created a uniquely compelling opportunity in APU units” – 1/7/2019

“APU has been under pressure since its analyst day in part due to a lack of resolution to its IDR structure… Further, we continue to believe that the outcome of the IDR structure review will result in an IDR conversion to units vs. a roll up given our view that UGI will IDR Conversion want to continue to be classified as a Utility vs. propane distributor (APU and Europe).” – 12/13/2018

NA NA NA

“We believe that a distribution cut remains a possibility and assume a 45% reduction (vs. 55% previously) in our model…We maintain Distribution Cut our Market Perform rating as the uncertainty of what action APU will undertake will likely continue to weigh on valuation, in our

view.” – 2/6/2019 barclays wells fargo janney jefferies raymond james ubs j.p.morgan morningstar

7

_____________________________________ Source: Wall Street research.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

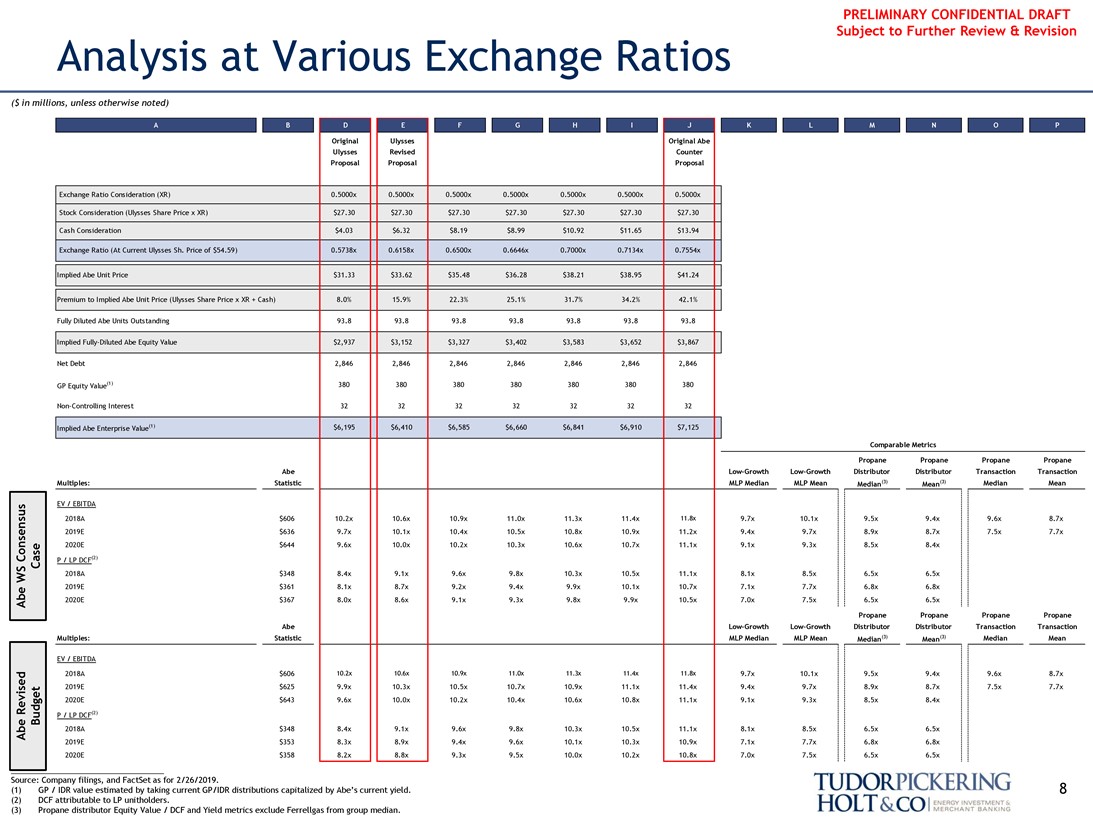

Analysis at Various Exchange Ratios

($ in millions, unless otherwise noted)

ABDEFGHIJKLMNOP

Original Ulysses Original Abe Ulysses Revised Counter Proposal Proposal Proposal

Exchange Ratio Consideration (XR) 0.5000x 0.5000x 0.5000x 0.5000x 0.5000x 0.5000x 0.5000x Stock Consideration (Ulysses Share Price x XR) $27.30 $27.30 $27.30 $27.30 $27.30 $27.30 $27.30 Cash Consideration $4.03 $6.32 $8.19 $8.99 $10.92 $11.65 $13.94 Exchange Ratio (At Current Ulysses Sh. Price of $54.59) 0.5738x 0.6158x 0.6500x 0.6646x 0.7000x 0.7134x 0.7554x

Implied Abe Unit Price $31.33 $33.62 $35.48 $36.28 $38.21 $38.95 $41.24 Premium to Implied Abe Unit Price (Ulysses Share Price x XR + Cash) 8.0% 15.9% 22.3% 25.1% 31.7% 34.2% 42.1% Fully Diluted Abe Units Outstanding 93.8 93.8 93.8 93.8 93.8 93.8 93.8 Implied Fully-Diluted Abe Equity Value $2,937 $3,152 $3,327 $3,402 $3,583 $3,652 $3,867 Net Debt 2,846 2,846 2,846 2,846 2,846 2,846 2,846

GP Equity Value(1) 380 380 380 380 380 380 380

Non-Controlling Interest 32 32 32 32 32 32 32

Implied Abe Enterprise Value(1) $6,195 $6,410 $6,585 $6,660 $6,841 $6,910 $7,125

Comparable Metrics

Propane Propane Propane Propane AbeLow-GrowthLow-Growth Distributor Distributor Transaction Transaction Multiples: Statistic MLP Median MLP Mean Median(3) Mean(3) Median Mean

EV / EBITDA

2018A $606 10.2x 10.6x 10.9x 11.0x 11.3x 11.4x 11.8x 9.7x 10.1x 9.5x 9.4x 9.6x 8.7x 2019E $636 9.7x 10.1x 10.4x 10.5x 10.8x 10.9x 11.2x 9.4x 9.7x 8.9x 8.7x 7.5x 7.7x 2020E $644 9.6x 10.0x 10.2x 10.3x 10.6x 10.7x 11.1x 9.1x 9.3x 8.5x 8.4x

Consensus P / LP DCF(2) Case

WS 2018A $348 8.4x 9.1x 9.6x 9.8x 10.3x 10.5x 11.1x 8.1x 8.5x 6.5x 6.5x 2019E $361 8.1x 8.7x 9.2x 9.4x 9.9x 10.1x 10.7x 7.1x 7.7x 6.8x 6.8x Abe 2020E $367 8.0x 8.6x 9.1x 9.3x 9.8x 9.9x 10.5x 7.0x 7.5x 6.5x 6.5x

Propane Propane Propane Propane AbeLow-GrowthLow-Growth Distributor Distributor Transaction Transaction Multiples: Statistic MLP Median MLP Mean Median(3) Mean(3) Median Mean

EV / EBITDA

2018A $606 10.2x 10.6x 10.9x 11.0x 11.3x 11.4x 11.8x 9.7x 10.1x 9.5x 9.4x 9.6x 8.7x 2019E $625 9.9x 10.3x 10.5x 10.7x 10.9x 11.1x 11.4x 9.4x 9.7x 8.9x 8.7x 7.5x 7.7x 2020E $643 9.6x 10.0x 10.2x 10.4x 10.6x 10.8x 11.1x 9.1x 9.3x 8.5x 8.4x

Revised P / LP DCF(2) Budget

Abe 2018A $348 8.4x 9.1x 9.6x 9.8x 10.3x 10.5x 11.1x 8.1x 8.5x 6.5x 6.5x 2019E $353 8.3x 8.9x 9.4x 9.6x 10.1x 10.3x 10.9x 7.1x 7.7x 6.8x 6.8x 2020E $358 8.2x 8.8x 9.3x 9.5x 10.0x 10.2x 10.8x 7.0x 7.5x 6.5x 6.5x

Source: Company filings, and FactSet as for 2/26/2019.

(1) GP / IDR value estimated by taking current GP/IDR distributions capitalized by Abe’s current yield. 8

(2) DCF attributable to LP unitholders.

(3) Propane distributor Equity Value / DCF and Yield metrics exclude Ferrellgas from group median.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

II. Status Quo Management Projections Overview

9

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

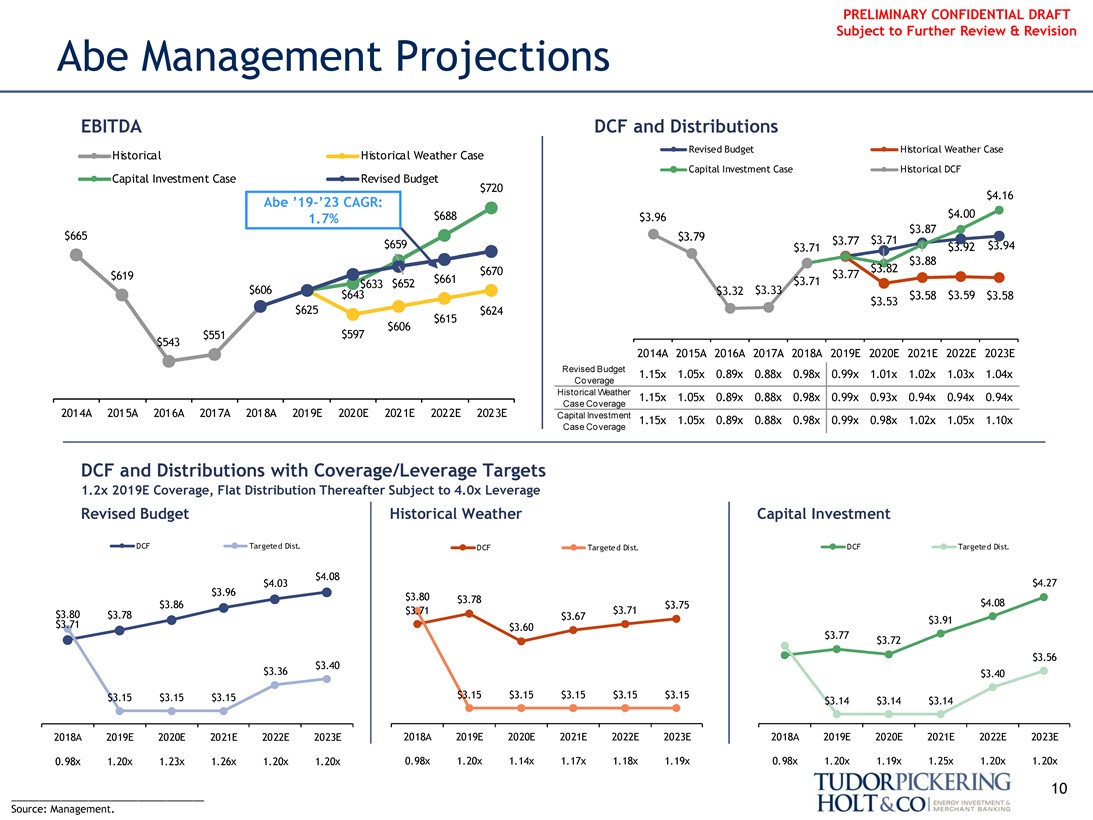

Abe Management Projections

EBITDA DCF and Distributions

Revised Budget Historical Weather Case

Historical Historical Weather Case

Capital Investment Case Revised Budget Capital Investment Case Historical DCF $720 $4.16

Abe’19-’23 CAGR: $4.00

1.7% $688 $3.96 $3.87 $665 $3.79 $3.77 $3.71 $659 $3.71 $3.92 $3.94 $3.88 $670 $3.82 $619 $661 $3.77 $633 $652 $3.71 $606 $643 $3.32 $3.33 $3.59 $3.58 $3.58 $3.53 $625 $624 $615 $606 $551 $597 $543 2014A 2015A 2016A 2017A 2018A 2019E 2020E 2021E 2022E 2023E

Revised Budget 1.15x 1.05x 0.89x 0.88x 0.98x 0.99x 1.01x 1.02x 1.03x 1.04x

Coverage

Historical Weather 1.15x 1.05x 0.89x 0.88x 0.98x 0.99x 0.93x 0.94x 0.94x 0.94x

2014A 2015A 2016A 2017A 2018A 2019E 2020E 2021E 2022E 2023E Case Coverage

Capital Investment 1.15x 1.05x 0.89x 0.88x 0.98x 0.99x 0.98x 1.02x 1.05x 1.10x

Case Coverage

DCF and Distributions with Coverage/Leverage Targets

1.2x 2019E Coverage, Flat Distribution Thereafter Subject to 4.0x Leverage

Revised Budget Historical Weather Capital Investment

DCF Targete d Dist. DCF Targete d Dist. DCF Targete d Dist.

$4.08 $3.96 $4.03 $4.27 $3.80 $3.78 $3.86 $3.75 $4.08 $3.80 $3.78 $3.71 $3.71 $3.67 $3.91 $3.71 $3.60 $3.77 $3.72 $3.56 $3.40 $3.36 $3.40 $3.15 $3.15 $3.15 $3.15 $3.15 $3.15 $3.15 $3.15 $3.14 $3.14 $3.14

2018A 2019E 2020E 2021E 2022E 2023E 2018A 2019E 2020E 2021E 2022E 2023E 2018A 2019E 2020E 2021E 2022E 2023E

0.98x 1.20x 1.23x 1.26x 1.20x 1.20x 0.98x 1.20x 1.14x 1.17x 1.18x 1.19x 0.98x 1.20x 1.19x 1.25x 1.20x 1.20x

10

___________________________________ Source: Management.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

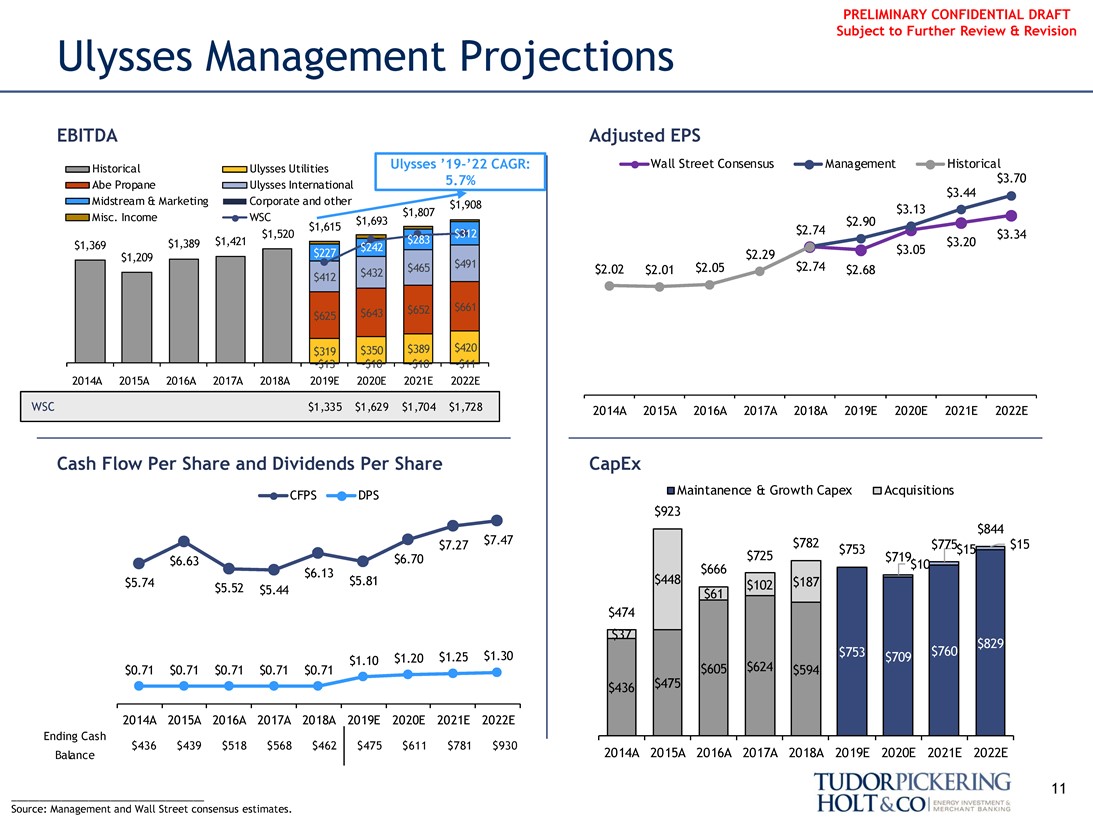

Ulysses Management Projections

EBITDA Adjusted EPS

Historical Ulysses Utilities Ulysses’19-’22 CAGR: Wall Street Consensus Management Historical 5.7% $3.70

Abe Propane Ulysses International $3.44

Midstream & Marketing Corporate and other $1,908 $1,807 $3.13 Misc. Income WSC $1,693 $2.90 $1,615 $2.74 $1,520 $3.34 $1,389 $1,421 $3.20 $1,369 $3.05 $1,209 $491 $2.29 $465 $2.02 $2.01 $2.05 $2.74 $2.68 $412 $432

$652 $661 $625 $643

$319 $350 $389 $420

-$13 -$10 -$10 -$11 2014A 2015A 2016A 2017A 2018A 2019E 2020E 2021E 2022E

WSC $1,335 $1,629 $1,704 $1,728 2014A 2015A 2016A 2017A 2018A 2019E 2020E 2021E 2022E

Cash Flow Per Share and Dividends Per Share CapEx

CFPS DPS Maintanence & Growth Capex Acquisitions $923 $844 $7.27 $7.47 $782 $775 $15 $753 $15 $6.63 $6.70 $725 $719 $666 $10 $6.13 $5.74 $5.81 $448 $102 $187 $5.52 $5.44 $61 $474 $37 $1.25 $1.30 $1.10 $1.20 $0.71 $0.71 $0.71 $0.71 $0.71 $605 $624 $594 $436 $475

2014A 2015A 2016A 2017A 2018A 2019E 2020E 2021E 2022E

Ending Cash $436 $439 $518 $568 $462 $475 $611 $781 $930

Balance 2014A 2015A 2016A 2017A 2018A 2019E 2020E 2021E 2022E

11

Source: Management and Wall Street consensus estimates.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

III. Abe Financial Analysis

12

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

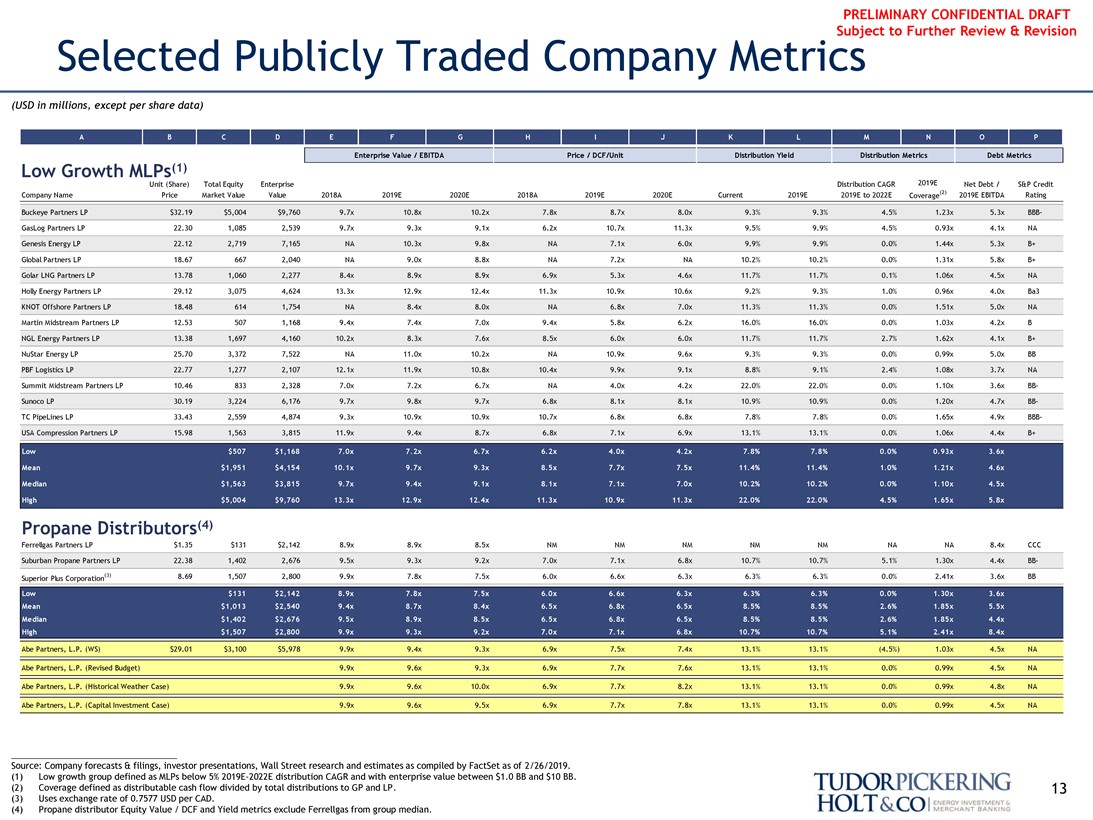

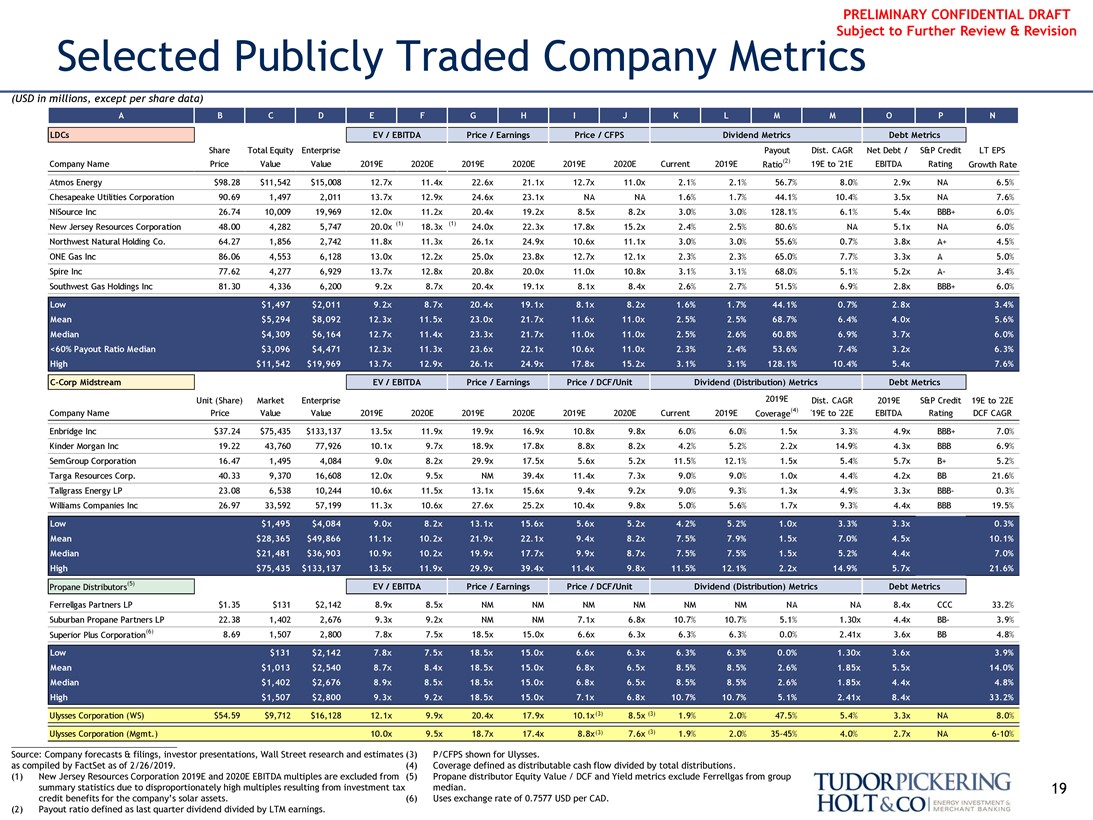

Selected Publicly Traded Company Metrics

(USD in millions, except per share data)

Enterprise Value / EBITDA Price / DCF/Unit Distribution Yield Distribution Metrics Debt Metrics

Low Growth MLPs(1)

Unit (Share) Total Equity Enterprise Distribution CAGR 2019E Net Debt / S&P Credit Company Name Price Market Value Value 2018A 2019E 2020E 2018A 2019E 2020E Current 2019E 2019E to 2022E Coverage(2) 2019E EBITDA Rating Buckeye Partners LP $32.19 $5,004 $9,760 9.7x 10.8x 10.2x 7.8x 8.7x 8.0x 9.3% 9.3% 4.5% 1.23x 5.3x BBB-

GasLog Partners LP 22.30 1,085 2,539 9.7x 9.3x 9.1x 6.2x 10.7x 11.3x 9.5% 9.9% 4.5% 0.93x 4.1x NA Genesis Energy LP 22.12 2,719 7,165 NA 10.3x 9.8x NA 7.1x 6.0x 9.9% 9.9% 0.0% 1.44x 5.3x B+ Global Partners LP 18.67 667 2,040 NA 9.0x 8.8x NA 7.2x NA 10.2% 10.2% 0.0% 1.31x 5.8x B+ Golar LNG Partners LP 13.78 1,060 2,277 8.4x 8.9x 8.9x 6.9x 5.3x 4.6x 11.7% 11.7% 0.1% 1.06x 4.5x NA Holly Energy Partners LP 29.12 3,075 4,624 13.3x 12.9x 12.4x 11.3x 10.9x 10.6x 9.2% 9.3% 1.0% 0.96x 4.0x Ba3 KNOT Offshore Partners LP 18.48 614 1,754 NA 8.4x 8.0x NA 6.8x 7.0x 11.3% 11.3% 0.0% 1.51x 5.0x NA Martin Midstream Partners LP 12.53 507 1,168 9.4x 7.4x 7.0x 9.4x 5.8x 6.2x 16.0% 16.0% 0.0% 1.03x 4.2x B NGL Energy Partners LP 13.38 1,697 4,160 10.2x 8.3x 7.6x 8.5x 6.0x 6.0x 11.7% 11.7% 2.7% 1.62x 4.1x B+ NuStar Energy LP 25.70 3,372 7,522 NA 11.0x 10.2x NA 10.9x 9.6x 9.3% 9.3% 0.0% 0.99x 5.0x BB PBF Logistics LP 22.77 1,277 2,107 12.1x 11.9x 10.8x 10.4x 9.9x 9.1x 8.8% 9.1% 2.4% 1.08x 3.7x NA Summit Midstream Partners LP 10.46 833 2,328 7.0x 7.2x 6.7x NA 4.0x 4.2x 22.0% 22.0% 0.0% 1.10x 3.6xBB-Sunoco LP 30.19 3,224 6,176 9.7x 9.8x 9.7x 6.8x 8.1x 8.1x 10.9% 10.9% 0.0% 1.20x 4.7xBB-TC PipeLines LP 33.43 2,559 4,874 9.3x 10.9x 10.9x 10.7x 6.8x 6.8x 7.8% 7.8% 0.0% 1.65x 4.9xBBB-USA Compression Partners LP 15.98 1,563 3,815 11.9x 9.4x 8.7x 6.8x 7.1x 6.9x 13.1% 13.1% 0.0% 1.06x 4.4x B+

low$507$1,1687.0x7.2x6.7x6.2x4.0x4.2x7.8%7.8%0.0%0.93x3.6xmean$1,951$4,15410.1x9.7x

9.3x8.5x7.7x7.5x11.4%11.4%1.0%1.21x4.6x

median$1,563 $3,815 9.7x 9.4x9.1x8.1x7.1x7.0x10.2%10.2%0.0%1.10x4.5x high$5,004 $9,760 13.3x 12.9x 12.4x

11.3x 10.9x 11.3x 22.0% 22.0% 4.5% 1.65x 5.8x Propane Distributors(4)

Ferrellgas Partners LP $1.35 $131 $2,142 8.9x 8.9x 8.5x NM NM NM NM NM NA NA 8.4x CCC

Suburban Propane Partners LP 22.38 1,402 2,676 9.5x 9.3x 9.2x 7.0x 7.1x 6.8x 10.7% 10.7% 5.1% 1.30x 4.4x BB-

Superior Plus Corporation(3) 8.69 1,507 2,800 9.9x 7.8x 7.5x 6.0x 6.6x 6.3x 6.3% 6.3% 0.0% 2.41x 3.6x BB

low $131 $2,142 8.9x 7.8x 7.5x 6.0x6.6x 6.3x6.3%.3%0.0%1.30X3.6X

MEAN$1,013 $2,5409.4X8.7X8.4x6.5x6.8x6.5x8.5%8.5%2.6%1.85x5.5x median $1,042$2,676 9.5x 8.9x 8.5x 6.5x 6.8x 6.5x 8.5% 8.5% 2.6% 1.85x 4.4x high $1,507 $2,800 9.9x 9.3x 9.2x 7.0x 7.1x 6.8x 10.7% 10.7% 5.1% 2.41x 8.4x

Abe Partners, L.P. (WS) $29.01 $3,100 $5,978 9.9x 9.4x 9.3x 6.9x 7.5x 7.4x 13.1% 13.1% (4.5%) 1.03x 4.5x NA Abe Partners, L.P. (Revised Budget) 9.9x 9.6x 9.3x 6.9x 7.7x 7.6x 13.1% 13.1% 0.0% 0.99x 4.5x NA Abe Partners, L.P. (Historical Weather Case) 9.9x 9.6x 10.0x 6.9x 7.7x 8.2x 13.1% 13.1% 0.0% 0.99x 4.8x NA Abe Partners, L.P. (Capital Investment Case) 9.9x 9.6x 9.5x 6.9x 7.7x 7.8x 13.1% 13.1% 0.0% 0.99x 4.5x NA

Source: Company forecasts & filings, investor presentations, Wall Street research and estimates as compiled by FactSet as of 2/26/2019. (1) Low growth group defined as MLPs below 5% 2019E-2022E distribution CAGR and with enterprise value between $1.0 BB and $10 BB.

(2) Coverage defined as distributable cash flow divided by total distributions to GP and LP. 13 (3) Uses exchange rate of 0.7577 USD per CAD.

(4) Propane distributor Equity Value / DCF and Yield metrics exclude Ferrellgas from group median.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

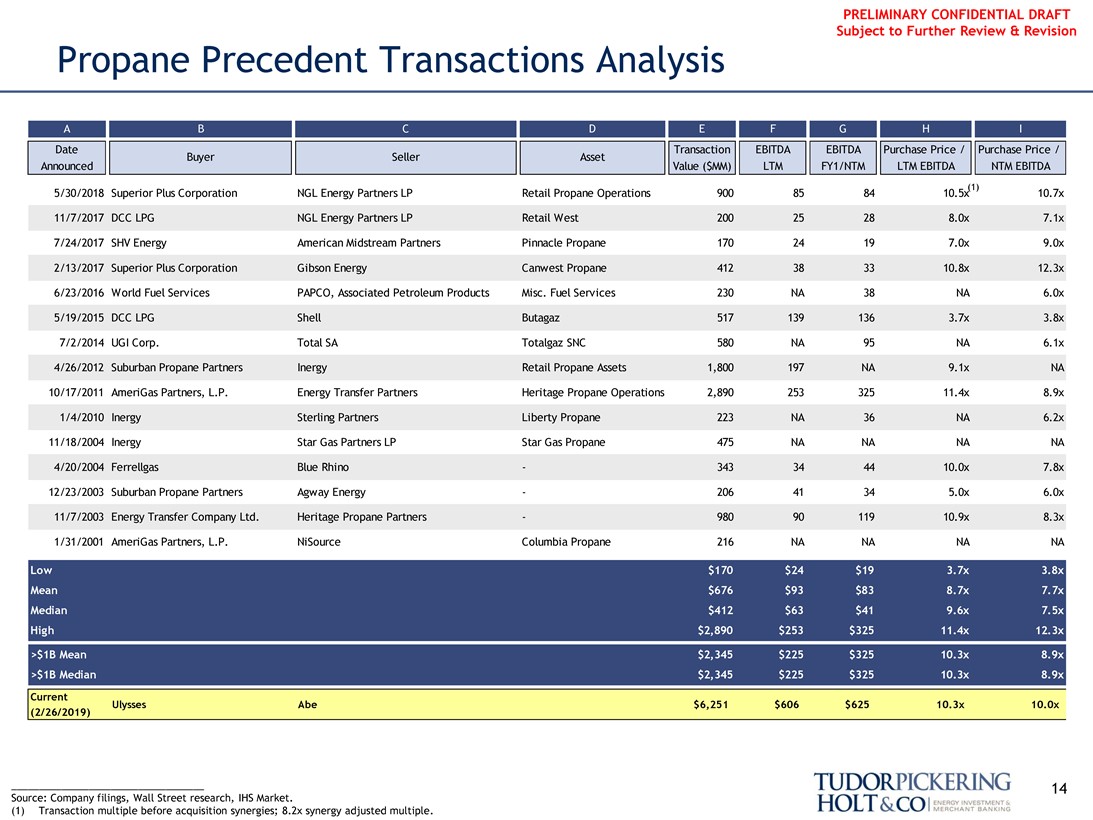

Propane Precedent Transactions Analysis

Date Transaction EBITDA EBITDA Purchase Price / Purchase Price / Buyer Seller Asset Announced Value ($MM) LTM FY1/NTM LTM EBITDA NTM EBITDA

(1)

5/30/2018 Superior Plus Corporation NGL Energy Partners LP Retail Propane Operations 900 85 84 10.5x 10.7x 11/7/2017 DCC LPG NGL Energy Partners LP Retail West 200 25 28 8.0x 7.1x 7/24/2017 SHV Energy American Midstream Partners Pinnacle Propane 170 24 19 7.0x 9.0x 2/13/2017 Superior Plus Corporation Gibson Energy Canwest Propane 412 38 33 10.8x 12.3x 6/23/2016 World Fuel Services PAPCO, Associated Petroleum Products Misc. Fuel Services 230 NA 38 NA 6.0x 5/19/2015 DCC LPG Shell Butagaz 517 139 136 3.7x 3.8x 7/2/2014 UGI Corp. Total SA Totalgaz SNC 580 NA 95 NA 6.1x 4/26/2012 Suburban Propane Partners Inergy Retail Propane Assets 1,800 197 NA 9.1x NA

10/17/2011 AmeriGas Partners, L.P. Energy Transfer Partners Heritage Propane Operations 2,890 253 325 11.4x 8.9x 1/4/2010 Inergy Sterling Partners Liberty Propane 223 NA 36 NA 6.2x 11/18/2004 Inergy Star Gas Partners LP Star Gas Propane 475 NA NA NA NA

4/20/2004 Ferrellgas Blue Rhino—343 34 44 10.0x 7.8x 12/23/2003 Suburban Propane Partners Agway Energy—206 41 34 5.0x 6.0x 11/7/2003 Energy Transfer Company Ltd. Heritage Propane Partners—980 90 119 10.9x 8.3x 1/31/2001 AmeriGas Partners, L.P. NiSource Columbia Propane 216 NA NA NA NA

Current Ulysses Abe $6,251 $606 $625 10.3x 10.0x (2/26/2019)

low $170 $24 $19 3.7x 3.8x Mean $676 93 $83 8.7x 7.7x Median $412 $63 $41 9.6x 7.5x High $2,890 $253 $325 11.4x 12.3x

>$1B Mean $2,345 $225 $325 10.3x 8.9x >$1B Median $2,345 $225 $325 10.3x 8.9x

___________________________________ 14 Source: Company filings, Wall Street research, IHS Market.

(1) Transaction multiple before acquisition synergies; 8.2x synergy adjusted multiple.

Tudorpickering Holt&co energy investment & merchant banking

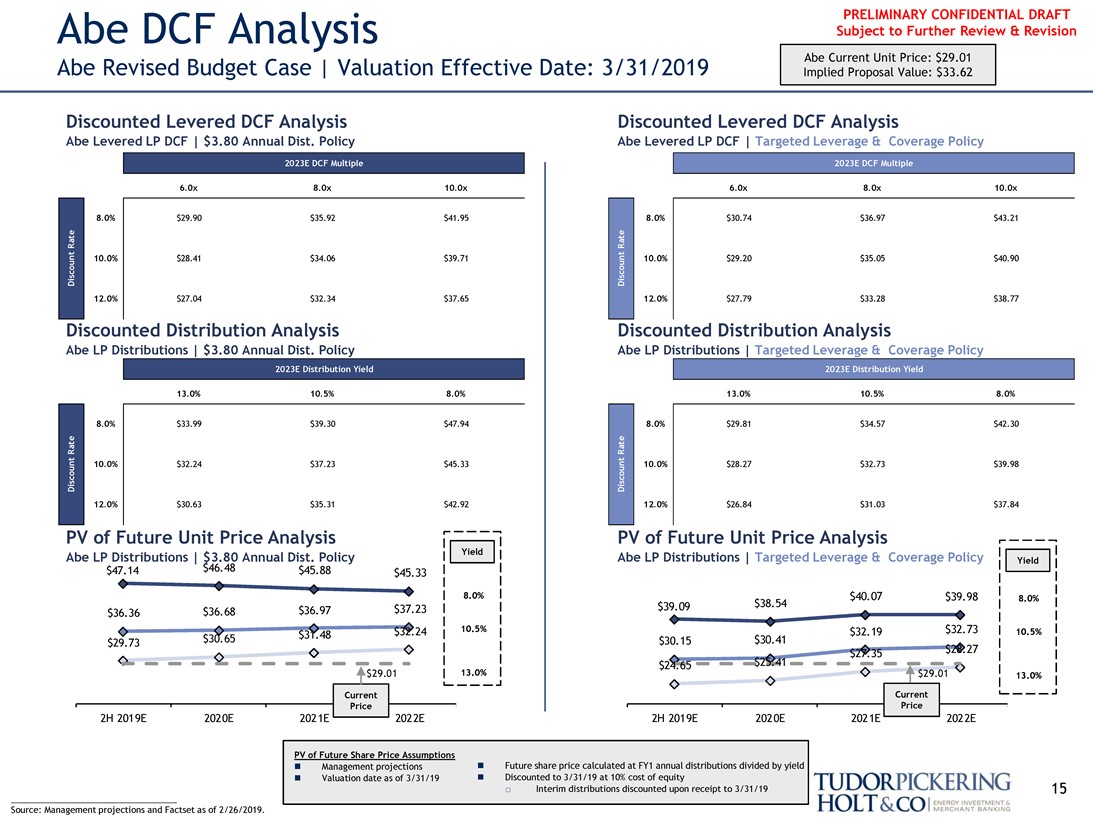

PRELIMINARY CONFIDENTIAL DRAFT Abe DCF Analysis Subject to Further Review & Revision

Abe Revised Budget Case | Valuation Effective Date: 3/31/2019 Abe Current Unit Price: $29.01

Implied Proposal Value: $33.62

Discounted Levered DCF Analysis Discounted Levered DCF Analysis

Abe Levered LP DCF | $3.80 Annual Dist. Policy Abe Levered LP DCF | Targeted Leverage & Coverage Policy

6.0x 8.0x 10.0x 6.0x 8.0x 10.0x

2023E DCF Multiple

Discount Rate

2023E Distribution Yield

Discount Rate

8.0% $29.90 $35.92 $41.95 8.0% $30.74 $36.97 $43.21 10.0% $28.41 $34.06 $39.71 10.0% $29.20 $35.05 $40.90 12.0% $27.04 $32.34 $37.65 12.0% $27.79 $33.28 $38.77

Discounted Distribution Analysis Discounted Distribution Analysis

Abe LP Distributions | $3.80 Annual Dist. Policy Abe LP Distributions | Targeted Leverage & Coverage Policy

13.0% 10.5% 8.0% 13.0% 10.5% 8.0%

8.0% $33.99 $39.30 $47.94 8.0% $29.81 $34.57 $42.30

10.0% $32.24 $37.23 $45.33 10.0% $28.27 $32.73 $39.98

12.0% $30.63 $35.31 $42.92 12.0% $26.84 $31.03 $37.84

PV of Future Unit Price Analysis PV of Future Unit Price Analysis

Abe LP Distributions | $3.80 Annual Dist. Policy Yield Abe LP Distributions | Targeted Leverage & Coverage Policy Yield $47.14 $46.48 $45.88 $45.33 8.0% $40.07 $39.98 8.0% $39.09 $38.54 $36.36 $36.68 $36.97 $37.23 $32.24 10.5% $32.19 $32.73 10.5% $30.65 $31.48 $30.41 $29.73 $30.15 $27.35 $28.27 $24.65 $25.41 $29.01 13.0% $29.01 13.0% Current Price Current Price

2H 2019E 2020E 2021E 2022E 2H 2019E 2020E 2021E 2022E

PV of Future Share Price Assumptions

∎ Management projections ∎ Future share price calculated at FY1 annual distributions divided by yield∎ Valuation date as of 3/31/19∎ Discounted to 3/31/19 at 10% cost of equity

Interim distributions discounted upon receipt to 3/31/19 15 Source: Management projections and Factset as of 2/26/2019.

Tudorpickering Holt&co energy investment & merchant banking

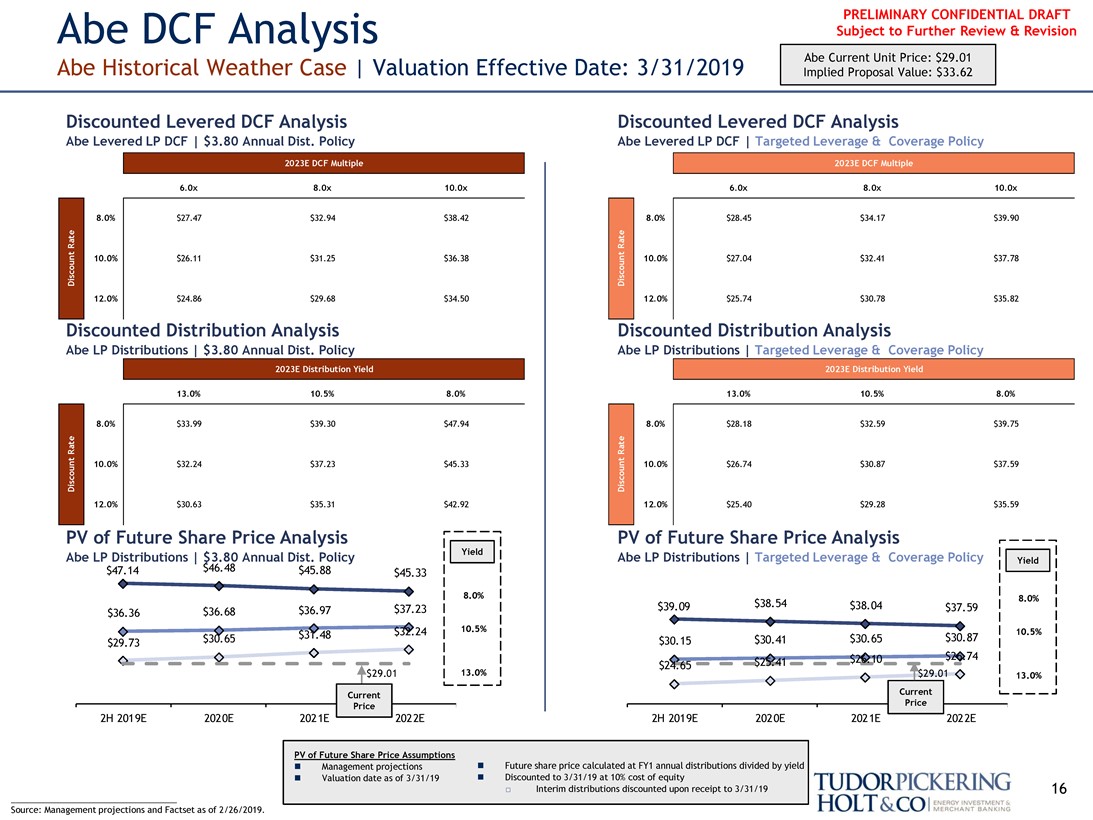

PRELIMINARY CONFIDENTIAL DRAFT Abe DCF Analysis Subject to Further Review & Revision

Abe Historical Weather Case | Valuation Effective Date: 3/31/2019 Abe Current Unit Price: $29.01

Implied Proposal Value: $33.62

Discounted Levered DCF Analysis Discounted Levered DCF Analysis

Abe Levered LP DCF | $3.80 Annual Dist. Policy Abe Levered LP DCF | Targeted Leverage & Coverage Policy

6.0x 8.0x 10.0x 6.0x 8.0x 10.0x

2023E DCF Multiple

Discount Rate

2023E Distribution Yield

Discount Rate

8.0% $27.47 $32.94 $38.42 8.0% $28.45 $34.17 $39.90 10.0% $26.11 $31.25 $36.38 10.0% $27.04 $32.41 $37.78 12.0% $24.86 $29.68 $34.50 12.0% $25.74 $30.78 $35.82

Discounted Distribution Analysis Discounted Distribution Analysis

Abe LP Distributions | $3.80 Annual Dist. Policy Abe LP Distributions | Targeted Leverage & Coverage Policy

13.0% 10.5% 8.0% 13.0% 10.5% 8.0%

8.0% $33.99 $39.30 $47.94 8.0% $28.18 $32.59 $39.75

10.0% $32.24 $37.23 $45.33 10.0% $26.74 $30.87 $37.59

12.0% $30.63 $35.31 $42.92 12.0% $25.40 $29.28 $35.59

PV of Future Share Price Analysis PV of Future Share Price Analysis

Abe LP Distributions | $3.80 Annual Dist. Policy Yield Abe LP Distributions | Targeted Leverage & Coverage Policy Yield $47.14 $46.48 $45.88 $45.33

8.0% 8.0% $39.09 $38.54 $38.04 $37.59 $36.36 $36.68 $36.97 $37.23 $32.24 10.5% 10.5% $30.65 $31.48 $30.41 $30.65 $30.87 $29.73 $30.15 $26.10 $26.74 $24.65 $25.41 $29.01 13.0% $29.01 13.0% Current Price Current Price

2H 2019E 2020E 2021E 2022E 2H 2019E 2020E 2021E 2022E

PV of Future Share Price Assumptions

∎ Management projections ∎ Future share price calculated at FY1 annual distributions divided by yield∎ Valuation date as of 3/31/19∎ Discounted to 3/31/19 at 10% cost of equity

Interim distributions discounted upon receipt to 3/31/19 16 Source: Management projections and Factset as of 2/26/2019.

Tudorpickering Holt&co energy investment & merchant banking

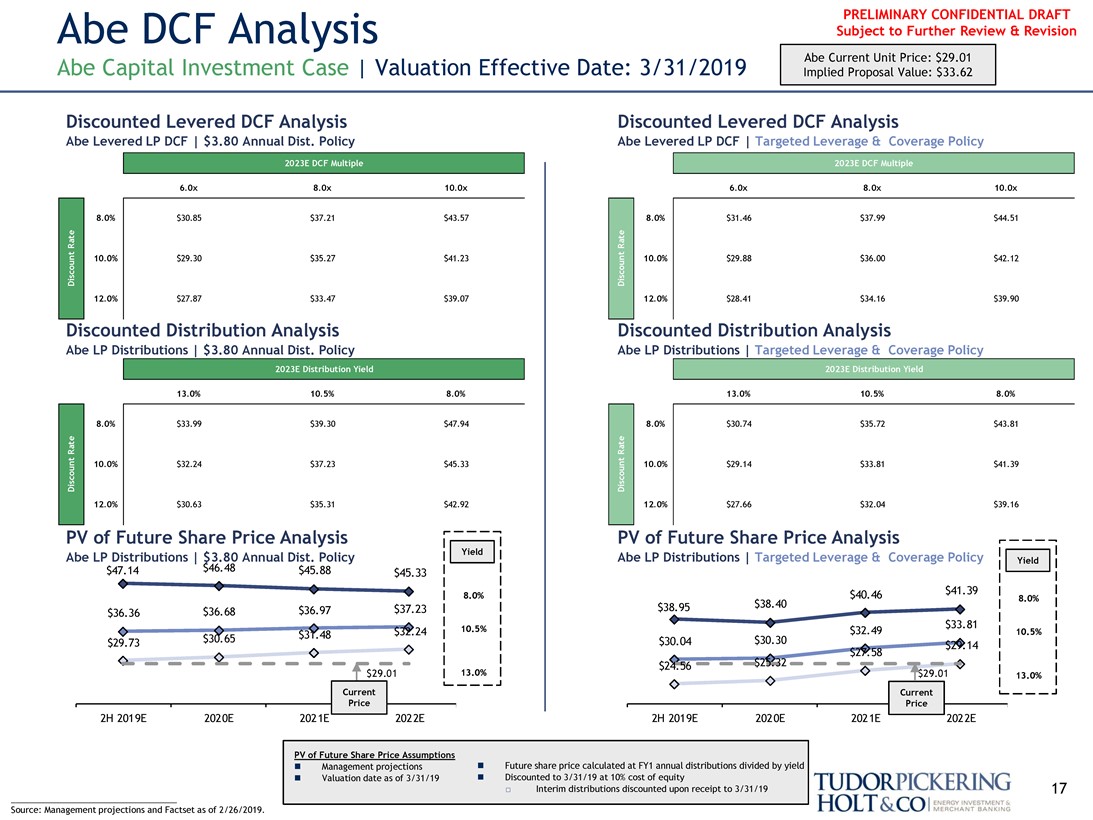

PRELIMINARY CONFIDENTIAL DRAFT Abe DCF Analysis Subject to Further Review & Revision

Abe Capital Investment Case | Valuation Effective Date: 3/31/2019 Abe Current Unit Price: $29.01

Implied Proposal Value: $33.62

Discounted Levered DCF Analysis Discounted Levered DCF Analysis

Abe Levered LP DCF | $3.80 Annual Dist. Policy Abe Levered LP DCF | Targeted Leverage & Coverage Policy

6.0x 8.0x 10.0x 6.0x 8.0x 10.0x

2023E DCF Multiple

Discount Rate

2023E Distribution Yield

Discount Rate

8.0% $30.85 $37.21 $43.57 8.0% $31.46 $37.99 $44.51 10.0% $29.30 $35.27 $41.23 10.0% $29.88 $36.00 $42.12 12.0% $27.87 $33.47 $39.07 12.0% $28.41 $34.16 $39.90

Discounted Distribution Analysis Discounted Distribution Analysis

Abe LP Distributions | $3.80 Annual Dist. Policy Abe LP Distributions | Targeted Leverage & Coverage Policy

13.0% 10.5% 8.0% 13.0% 10.5% 8.0%

8.0% $33.99 $39.30 $47.94 8.0% $30.74 $35.72 $43.81

10.0% $32.24 $37.23 $45.33 10.0% $29.14 $33.81 $41.39

12.0% $30.63 $35.31 $42.92 12.0% $27.66 $32.04 $39.16

PV of Future Share Price Analysis PV of Future Share Price Analysis

Abe LP Distributions | $3.80 Annual Dist. Policy Yield Abe LP Distributions | Targeted Leverage & Coverage Policy Yield $47.14 $46.48 $45.88 $45.33 $40.46 $41.39

8.0% 8.0% $37.23 $38.95 $38.40 $36.36 $36.68 $36.97 10.5% $33.81 $31.48 $32.24 $32.49 10.5% $29.73 $30.65 $30.04 $30.30 $29.14 $25.32 $27.58 $24.56 $29.01 13.0% $29.01 13.0% Current Current Price Price

2H 2019E 2020E 2021E 2022E 2H 2019E 2020E 2021E 2022E

PV of Future Share Price Assumptions

∎ Management projections ∎ Future share price calculated at FY1 annual distributions divided by yield∎ Valuation date as of 3/31/19∎ Discounted to 3/31/19 at 10% cost of equity

Interim distributions discounted upon receipt to 3/31/19 17 Source: Management projections and Factset as of 2/26/2019.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

IV. Ulysses Financial Analysis

18

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Selected Publicly Traded Company Metrics

(USD in millions, except per share data)

LDCs EV / EBITDA Price / Earnings Price / CFPS Dividend Metrics Debt Metrics

Share Total Equity Enterprise Payout Dist. CAGR Net Debt / S&P Credit LT EPS Company Name Price Value Value 2019E 2020E 2019E 2020E 2019E 2020E Current 2019E Ratio(2) 19E to ‘21E EBITDA Rating Growth Rate Atmos Energy $98.28 $11,542 $15,008 12.7x 11.4x 22.6x 21.1x 12.7x 11.0x 2.1% 2.1% 56.7% 8.0% 2.9x NA 6.5% Chesapeake Utilities Corporation 90.69 1,497 2,011 13.7x 12.9x 24.6x 23.1x NA NA 1.6% 1.7% 44.1% 10.4% 3.5x NA 7.6% NiSource Inc 26.74 10,009 19,969 12.0x 11.2x 20.4x 19.2x 8.5x 8.2x 3.0% 3.0% 128.1% 6.1% 5.4x BBB+ 6.0% New Jersey Resources Corporation 48.00 4,282 5,747 20.0x (1) 18.3x (1) 24.0x 22.3x 17.8x 15.2x 2.4% 2.5% 80.6% NA 5.1x NA 6.0% Northwest Natural Holding Co. 64.27 1,856 2,742 11.8x 11.3x 26.1x 24.9x 10.6x 11.1x 3.0% 3.0% 55.6% 0.7% 3.8x A+ 4.5% ONE Gas Inc 86.06 4,553 6,128 13.0x 12.2x 25.0x 23.8x 12.7x 12.1x 2.3% 2.3% 65.0% 7.7% 3.3x A 5.0% Spire Inc 77.62 4,277 6,929 13.7x 12.8x 20.8x 20.0x 11.0x 10.8x 3.1% 3.1% 68.0% 5.1% 5.2xA- 3.4% Southwest Gas Holdings Inc 81.30 4,336 6,200 9.2x 8.7x 20.4x 19.1x 8.1x 8.4x 2.6% 2.7% 51.5% 6.9% 2.8x BBB+ 6.0%

Low $1,497 $2,011 9.2x 8.7x 20.4x 19.1x 8.1x 8.2x 1.6% 1.7% 44.1% 0.7% 2.8x 3.4% Mean $5,294 $8,092 12.3x 11.5x 23.0x 21.7x 11.6x 11.0x 2.5% 2.5% 68.7% 6.4% 4.0x 5.6% Median $4,309 $6,164 12.7x 11.4x 23.3x 21.7x 11.0x 11.0x 2.5% 2.6% 60.8% 6.9% 3.7x 6.0% <60% Payout Ratio Median $3,096 $4,471 12.3x 11.3x 23.6x 22.1x 10.6x 11.0x 2.3% 2.4% 53.6% 7.4% 3.2x 6.3% High $11,542 $19,969 13.7x 12.9x 26.1x 24.9x 17.8x 15.2x 3.1% 3.1% 128.1% 10.4% 5.4x 7.6%

C-Corp Midstream EV / EBITDA Price / Earnings Price / DCF/Unit Dividend (Distribution) Metrics Debt Metrics

Unit (Share) Market Enterprise 2019E Dist. CAGR 2019E S&P Credit 19E to ‘22E Company Name Price Value Value 2019E 2020E 2019E 2020E 2019E 2020E Current 2019E Coverage(4) ‘19E to ‘22E EBITDA Rating DCF CAGR Enbridge Inc $37.24 $75,435 $133,137 13.5x 11.9x 19.9x 16.9x 10.8x 9.8x 6.0% 6.0% 1.5x 3.3% 4.9x BBB+ 7.0% Kinder Morgan Inc 19.22 43,760 77,926 10.1x 9.7x 18.9x 17.8x 8.8x 8.2x 4.2% 5.2% 2.2x 14.9% 4.3x BBB 6.9% SemGroup Corporation 16.47 1,495 4,084 9.0x 8.2x 29.9x 17.5x 5.6x 5.2x 11.5% 12.1% 1.5x 5.4% 5.7x B+ 5.2% Targa Resources Corp. 40.33 9,370 16,608 12.0x 9.5x NM 39.4x 11.4x 7.3x 9.0% 9.0% 1.0x 4.4% 4.2x BB 21.6% Tallgrass Energy LP 23.08 6,538 10,244 10.6x 11.5x 13.1x 15.6x 9.4x 9.2x 9.0% 9.3% 1.3x 4.9% 3.3xBBB- 0.3% Williams Companies Inc 26.97 33,592 57,199 11.3x 10.6x 27.6x 25.2x 10.4x 9.8x 5.0% 5.6% 1.7x 9.3% 4.4x BBB 19.5%

Low $1,495 $4,084 9.0x 8.2x 13.1x 15.6x 5.6x 5.2x 4.2% 5.2% 1.0x 3.3% 3.3x 0.3% Mean $28,365 $49,866 11.1x 10.2x 21.9x 22.1x 9.4x 8.2x 7.5% 7.9% 1.5x 7.0% 4.5x 10.1% Median $21,481 $36,903 10.9x 10.2x 19.9x 17.7x 9.9x 8.7x 7.5% 7.5% 1.5x 5.2% 4.4x 7.0% High $75,435 $133,137 13.5x 11.9x 29.9x 39.4x 11.4x 9.8x 11.5% 12.1% 2.2x 14.9% 5.7x 21.6%

Propane Distributors(5) EV / EBITDA Price / Earnings Price / DCF/Unit Dividend (Distribution) Metrics Debt Metrics

Ferrellgas Partners LP $1.35 $131 $2,142 8.9x 8.5x NM NM NM NM NM NM NA NA 8.4x CCC 33.2% Suburban Propane Partners LP 22.38 1,402 2,676 9.3x 9.2x NM NM 7.1x 6.8x 10.7% 10.7% 5.1% 1.30x 4.4xBB- 3.9% Superior Plus Corporation(6) 8.69 1,507 2,800 7.8x 7.5x 18.5x 15.0x 6.6x 6.3x 6.3% 6.3% 0.0% 2.41x 3.6x BB 4.8%

Low $131 $2,142 7.8x 7.5x 18.5x 15.0x 6.6x 6.3x 6.3% 6.3% 0.0% 1.30x 3.6x 3.9% Mean $1,013 $2,540 8.7x 8.4x 18.5x 15.0x 6.8x 6.5x 8.5% 8.5% 2.6% 1.85x 5.5x 14.0% Median $1,402 $2,676 8.9x 8.5x 18.5x 15.0x 6.8x 6.5x 8.5% 8.5% 2.6% 1.85x 4.4x 4.8% High $1,507 $2,800 9.3x 9.2x 18.5x 15.0x 7.1x 6.8x 10.7% 10.7% 5.1% 2.41x 8.4x 33.2%

Ulysses Corporation (WS) $54.59 $9,712 $16,128 12.1x 9.9x 20.4x 17.9x 10.1x(3) 8.5x (3) 1.9% 2.0% 47.5% 5.4% 3.3x NA 8.0% Ulysses Corporation (Mgmt.) 10.0x 9.5x 18.7x 17.4x 8.8x(3) 7.6x (3) 1.9% 2.0%35-45% 4.0% 2.7x NA6-10%

Source: Company forecasts & filings, investor presentations, Wall Street research and estimates (3) P/CFPS shown for Ulysses. as compiled by FactSet as of 2/26/2019. (4) Coverage defined as distributable cash flow divided by total distributions.

(1) New Jersey Resources Corporation 2019E and 2020E EBITDA multiples are excluded from (5) Propane distributor Equity Value / DCF and Yield metrics exclude Ferrellgas from group summary statistics due to disproportionately high multiples resulting from investment tax median. 19 credit benefits for the company’s solar assets. (6) Uses exchange rate of 0.7577 USD per CAD.

(2) Payout ratio defined as last quarter dividend divided by LTM earnings.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT

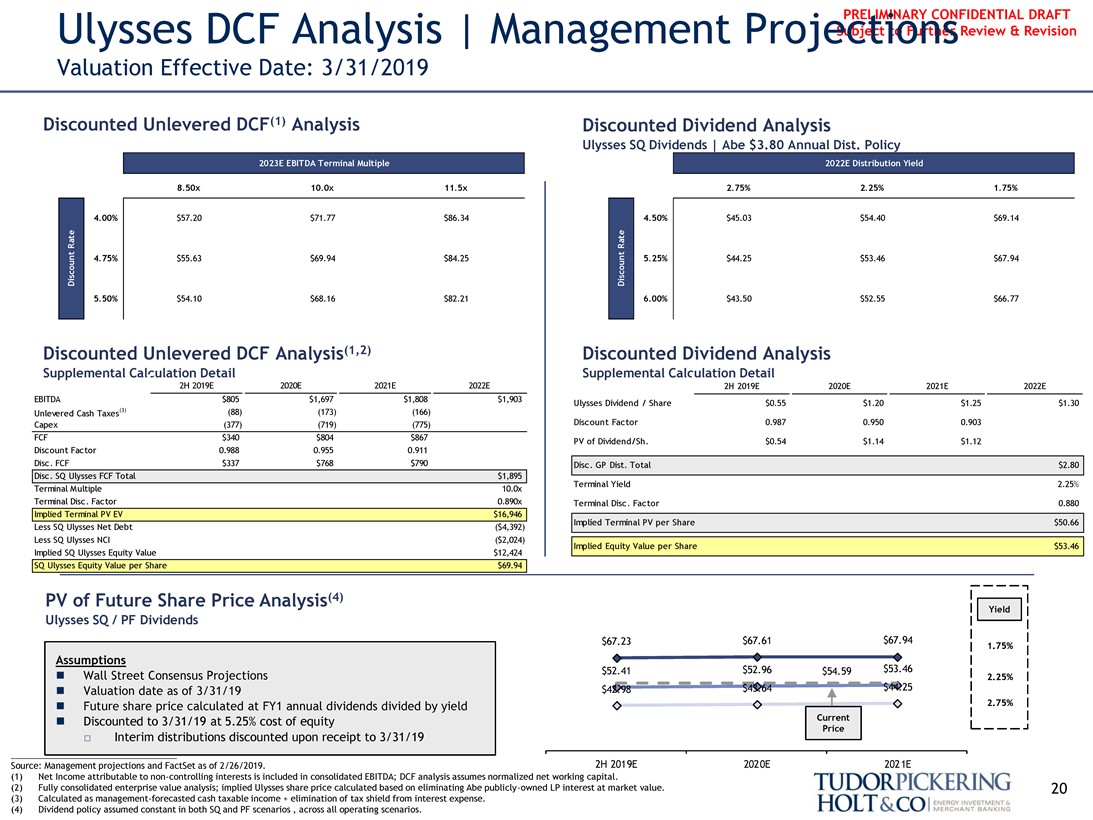

Ulysses DCF Analysis | Management Projections Subject to Further Review & Revision

Valuation Effective Date: 3/31/2019

Discounted Unlevered DCF(1) Analysis Discounted Dividend Analysis

Ulysses SQ Dividends | Abe $3.80 Annual Dist. Policy

8.50x 10.0x 11.5x 2.75% 2.25% 1.75%

4.00% $57.20 $71.77 $86.34 4.50% $45.03 $54.40 $69.14 4.75% $55.63 $69.94 $84.25 5.25% $44.25 $53.46 $67.94 5.50% $54.10 $68.16 $82.21 6.00% $43.50 $52.55 $66.77

Discounted Unlevered DCF Analysis(1,2) Discounted Dividend Analysis

Supplemental Calculation Detail Supplemental Calculation Detail

2H 2019E 2020E 2021E 2022E 2H 2019E 2020E 2021E

2022E EBITDA Terminal Multiple

Discount Rate

$805 $1,697 $1,808 $1,903 Ulysses Dividend / Share $0.55 $1.20 $1.25 $1.30

Unlevered Cash Taxes(3) (88) (173) (166)

Capex (377) (719) (775) Discount Factor 0.987 0.950 0.903 FCF $340 $804 $867 PV of Dividend/Sh. $0.54 $1.14 $1.12

Discount Factor 0.988 0.955 0.911

Disc. FCF $337 $768 $790 Disc. GP Dist. Total $2.80

Disc. SQ Ulysses FCF Total $1,895 Terminal Yield 2.25% Terminal Multiple 10.0x Terminal Disc. Factor 0.890x Terminal Disc. Factor 0.880

Implied Terminal PV EV $16,946 Implied Terminal PV per Share $50.66

Less SQ Ulysses Net Debt ($4,392) Less SQ Ulysses NCI ($2,024)

Implied Equity Value per Share $53.46

Implied SQ Ulysses Equity Value $12,424 SQ Ulysses Equity Value per Share $69.94

PV of Future Share Price Analysis(4)

Ulysses SQ / PF Dividends Yield $67.23 $67.61 $67.94

1.75%

Assumptions $52.41 $52.96 $54.59 $53.46

2022E Distribution Yield

Discount Rate

∎ Wall Street Consensus Projections 2.25%∎ Valuation date as of 3/31/19 $42.98 $43.64 $44.25 ∎ Future share price calculated at FY1 annual dividends divided by yield 2.75%

∎ Discounted to 3/31/19 at 5.25% cost of equity Current

Price

Interim distributions discounted upon receipt to 3/31/19

Source: Management projections and FactSet as of 2/26/2019. 2H 2019E 2020E 2021E (1) Net Income attributable tonon-controlling interests is included in consolidated EBITDA; DCF analysis assumes normalized net working capital.

(2) Fully consolidated enterprise value analysis; implied Ulysses share price calculated based on eliminating Abe publicly-owned LP interest at market value. 20 (3) Calculated as management-forecasted cash taxable income + elimination of tax shield from interest expense.

(4) Dividend policy assumed constant in both SQ and PF scenarios , across all operating scenarios.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

V. Transaction Analysis

21

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT

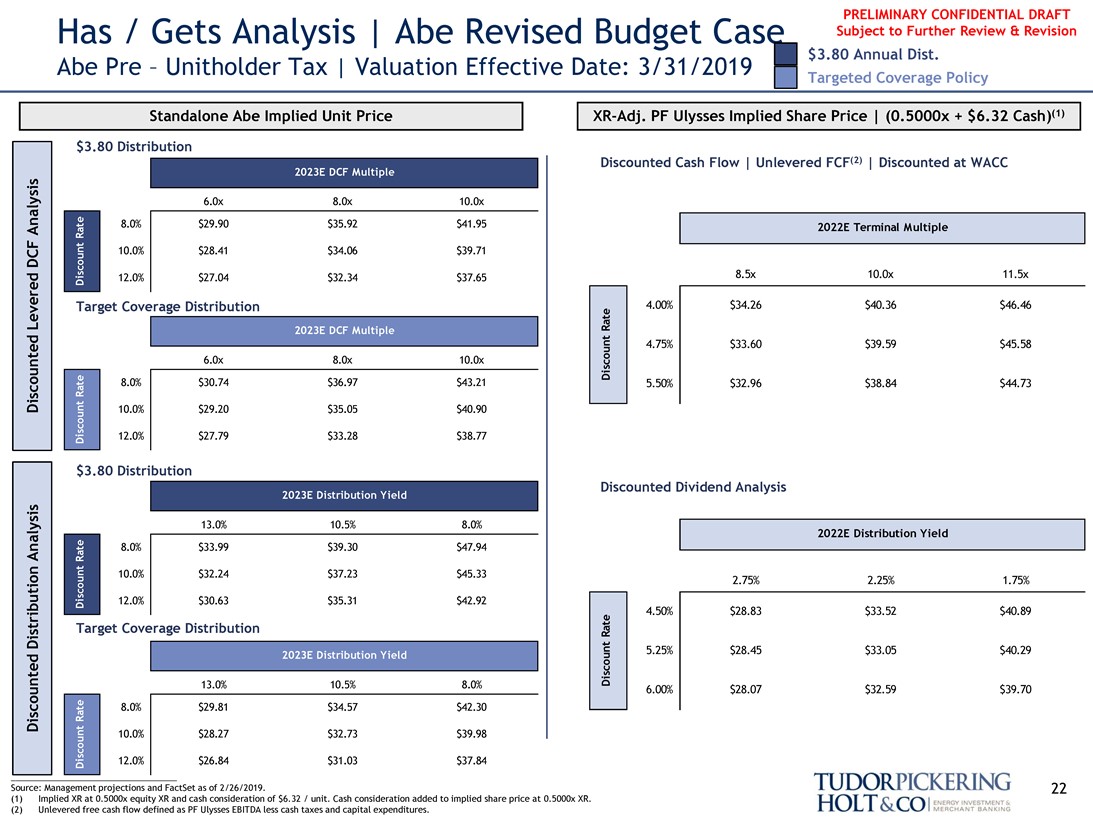

Has / Gets Analysis | Abe Revised Budget Case Subject to Further Review & Revision

Abe Pre – Unitholder Tax | Valuation Effective Date: 3/31/2019 $3.80 Annual Dist.

Targeted Coverage Policy

Standalone Abe Implied Unit PriceXR-Adj. PF Ulysses Implied Share Price | (0.5000x + $6.32 Cash)(1) $3.80 Distribution Discounted Cash Flow | Unlevered FCF(2) | Discounted at WACC

6.0x 8.0x 10.0x

Analysis 8.0% $29.90 $35.92 $41.95 2022E Terminal Multiple DCF 10.0% $28.41 $34.06 $39.71

8.5x 10.0x 11.5x

12.0% $27.04 $32.34 $37.65

2023E DCF Multiple

Discounted Levered Analysis

Target Coverage Distribution 4.00% $34.26 $40.36 $46.46

4.75% $33.60 $39.59 $45.58

6.0x 8.0x 10.0x

8.0% $30.74 $36.97 $43.21 5.50% $32.96 $38.84 $44.73

10.0% $29.20 $35.05 $40.90 12.0% $27.79 $33.28 $38.77

$3.80 Distribution

Discounted Dividend Analysis

13.0% 10.5% 8.0%

2022E Distribution Yield

8.0% $33.99 $39.30 $47.94 10.0% $32.24 $37.23 $45.33

2.75% 2.25% 1.75%

12.0% $30.63 $35.31 $42.92

4.50% $28.83 $33.52 $40.89

Target Coverage Distribution

Distribution Rate

2022E Terminal Multiple

5.25% $28.45 $33.05 $40.29

13.0% 10.5% 8.0% 6.00% $28.07 $32.59 $39.70

8.0% $29.81 $34.57 $42.30

Discounted

10.0% $28.27 $32.73 $39.98

12.0% $26.84 $31.03 $37.84

Source: Management projections and FactSet as of 2/26/2019. 22 (1) Implied XR at 0.5000x equity XR and cash consideration of $6.32 / unit. Cash consideration added to implied share price at 0.5000x XR.

(2) Unlevered free cash flow defined as PF Ulysses EBITDA less cash taxes and capital expenditures.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT

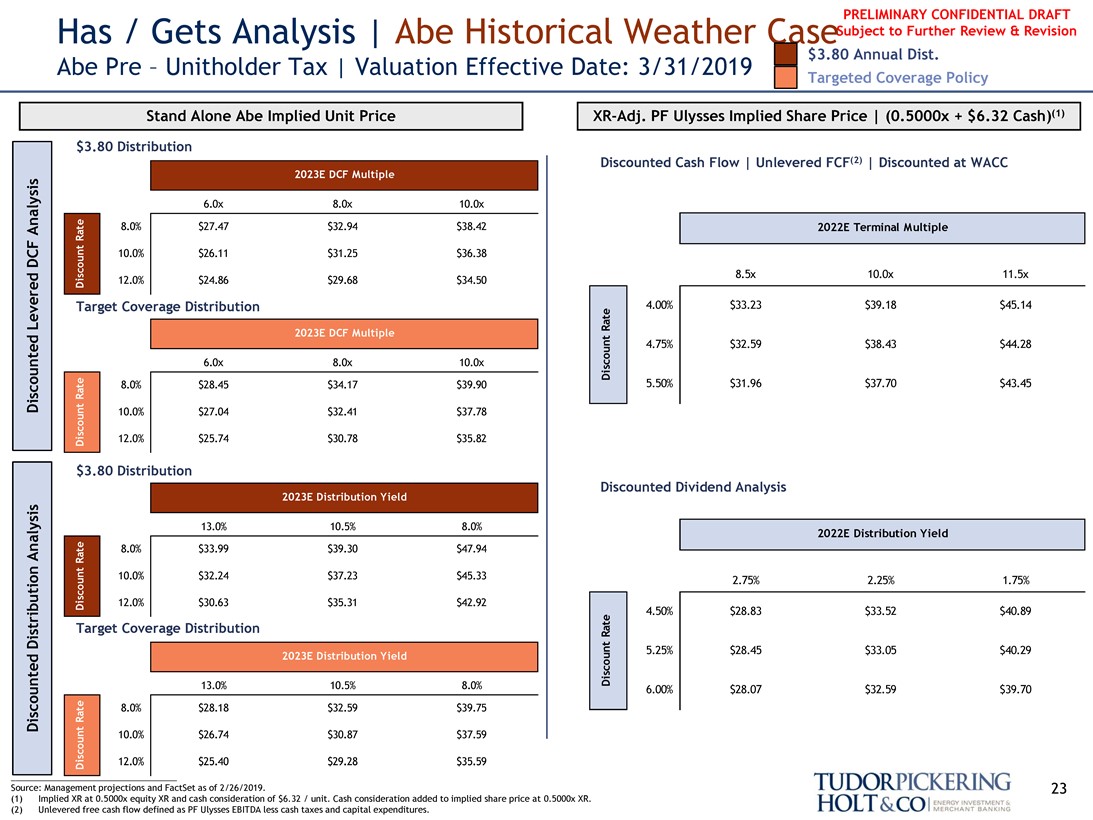

Has / Gets Analysis | Abe Historical Weather Case Subject to Further Review & Revision

Abe Pre – Unitholder Tax | Valuation Effective Date: 3/31/2019 $3.80 Annual Dist.

Targeted Coverage Policy

Stand Alone Abe Implied Unit PriceXR-Adj. PF Ulysses Implied Share Price | (0.5000x + $6.32 Cash)(1) $3.80 Distribution Discounted Cash Flow | Unlevered FCF(2) | Discounted at WACC

6.0x 8.0x 10.0x

Analysis 8.0% $27.47 $32.94 $38.42 2022E Terminal Multiple

DCF 10.0% $26.11 $31.25 $36.38 8.5x 10.0x 11.5x

12.0% $24.86 $29.68 $34.50

Levered Target Coverage Distribution 4.00% $33.23 $39.18 $45.14

4.75% $32.59 $38.43 $44.28

6.0x 8.0x 10.0 x 8.0% $28.45 $34.17 $39.90 5.50% $31.96 $37.70 $43.45

Discounted

10.0% $27.04 $32.41 $37.78 12.0% $25.74 $30.78 $35.82 $3.80 Distribution

Discounted Dividend Analysis

2023E DCF Multiple

13.0% 10.5% 8.0%

2022E Distribution Yield

Analysis 8.0% $33.99 $39.30 $47.94 10.0% $32.24 $37.23 $45.33 2.75% 2.25% 1.75% 12.0% $30.63 $35.31 $42.92

4.50% $28.83 $33.52 $40.89

Target Coverage Distribution

Distribution Rate

2022E Terminal Multiple

5.25% $28.45 $33.05 $40.29

13.0% 10.5% 8.0%

6.00% $28.07 $32.59 $39.70

8.0% $28.18 $32.59 $39.75

Discounted

10.0% $26.74 $30.87 $37.59

12.0% $25.40 $29.28 $35.59

Source: Management projections and FactSet as of 2/26/2019. 23 (1) Implied XR at 0.5000x equity XR and cash consideration of $6.32 / unit. Cash consideration added to implied share price at 0.5000x XR.

(2) Unlevered free cash flow defined as PF Ulysses EBITDA less cash taxes and capital expenditures.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT

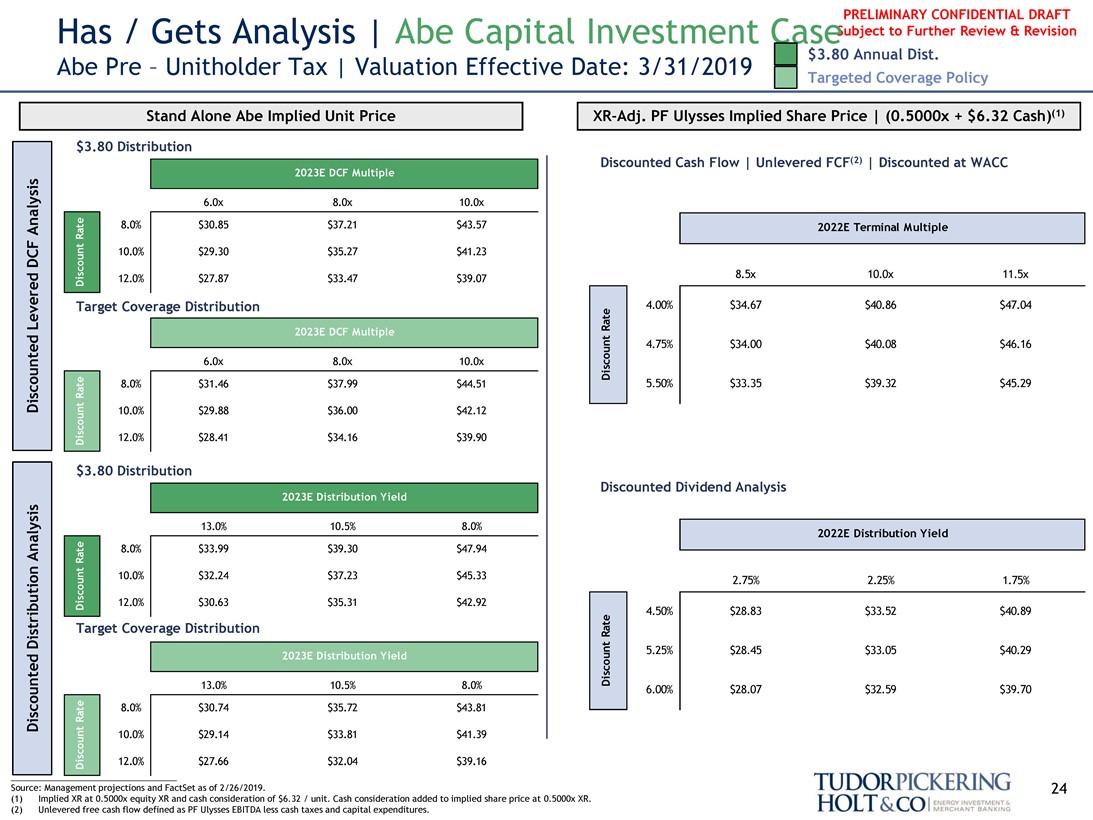

Has / Gets Analysis | Abe Capital Investment Case Subject to Further Review & Revision

Abe Pre – Unitholder Tax | Valuation Effective Date: 3/31/2019 $3.80 Annual Dist.

Targeted Coverage Policy

Stand Alone Abe Implied Unit PriceXR-Adj. PF Ulysses Implied Share Price | (0.5000x + $6.32 Cash)(1) $3.80 Distribution Discounted Cash Flow | Unlevered FCF(2) | Discounted at WACC

6.0x 8.0x 10.0x

Analysis 8.0% $30.85 $37.21 $43.57 2022E Terminal Multiple 10.0% $29.30 $35.27 $41.23

DCF

12.0% $27.87 $33.47 $39.07 8.5x 10.0x 11.5x

Levered Target Coverage Distribution 4.00% $34.67 $40.86 $47.04

4.75% $34.00 $40.08 $46.16

6.0x 8.0x 10.0x

8.0% $31.46 $37.99 $44.51 5.50% $33.35 $39.32 $45.29

Discounted

10.0% $29.88 $36.00 $42.12 12.0% $28.41 $34.16 $39.90

$3.80

2022E DCF Multiple

Distribution Rate

Discounted Dividend Analysis

13.0% 10.5% 8.0%

2022E Distribution Yield

Analysis 8.0% $33.99 $39.30 $47.94 10.0% $32.24 $37.23 $45.33 2.75% 2.25% 1.75%

12.0% $30.63 $35.31 $42.92

4.50% $28.83 $33.52 $40.89

Target Coverage Distribution

Distribution Rate

5.25% $28.45 $33.05 $40.29

13.0% 10.5% 8.0%

6.00% $28.07 $32.59 $39.70

8.0% $30.74 $35.72 $43.81

Discounted

10.0% $29.14 $33.81 $41.39

12.0% $27.66 $32.04 $39.16

Source: Management projections and FactSet as of 2/26/2019. 24 (1) Implied XR at 0.5000x equity XR and cash consideration of $6.32 / unit. Cash consideration added to implied share price at 0.5000x XR.

(2) Unlevered free cash flow defined as PF Ulysses EBITDA less cash taxes and capital expenditures.

Tudorpickering Holt&co energy investment & merchant banking

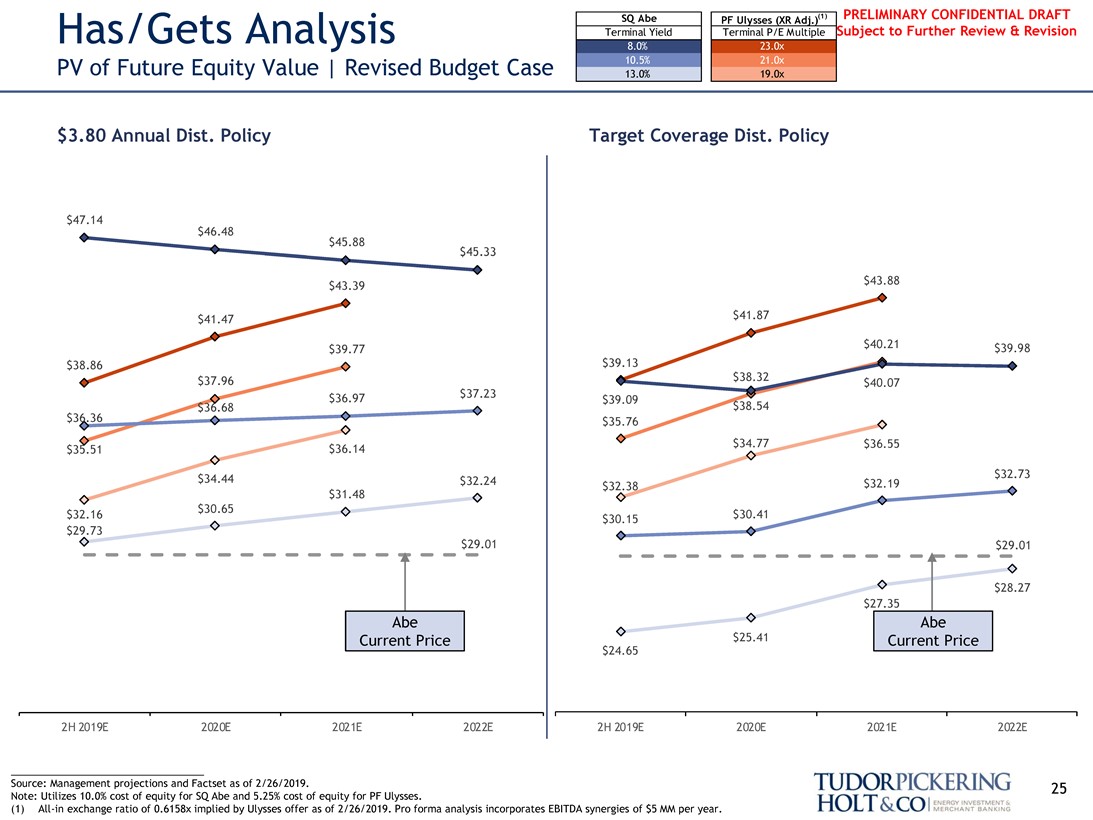

PRELIMINARY CONFIDENTIAL DRAFT Has/Gets Analysis SQ Abe Terminal Yield PF Ulysses Terminal P/E Multiple Subject to Further Review & Revision

PV of Future Equity Value | Revised Budget Case

8.0%

10.5%

23.0x

21.0x

13.0%

19.0x

$3.80 Annual Dist. Policy Target Coverage Dist. Policy

$47.14 $46.48 $45.88 $45.33

$43.39 $43.88 $41.47 $41.87 $39.77 $40.21 $39.98 $38.86 $39.13 $37.96 $38.32 $37.23 $40.07 $36.97 $39.09 $36.68 $38.54 $36.36 $35.76 $34.77 $36.55 $35.51 $36.14 $34.44 $32.73 $32.24 $32.38 $32.19 $31.48 $30.65 $32.16 $30.15 $30.41 $29.73 $29.01 $29.01

$28.27 $27.35

Abe Abe Current Price $25.41 Current Price

$24.65

2H 2019E 2020E 2021E 2022E 2H 2019E 2020E 2021E 2022E

Source: Management projections and Factset as of 2/26/2019. 25 Note: Utilizes 10.0% cost of equity for SQ Abe and 5.25% cost of equity for PF Ulysses.

(1)All-in exchange ratio of 0.6158x implied by Ulysses offer as of 2/26/2019. Pro forma analysis incorporates EBITDA synergies of $5 MM per year.

Tudorpickering Holt&co energy investment & merchant banking

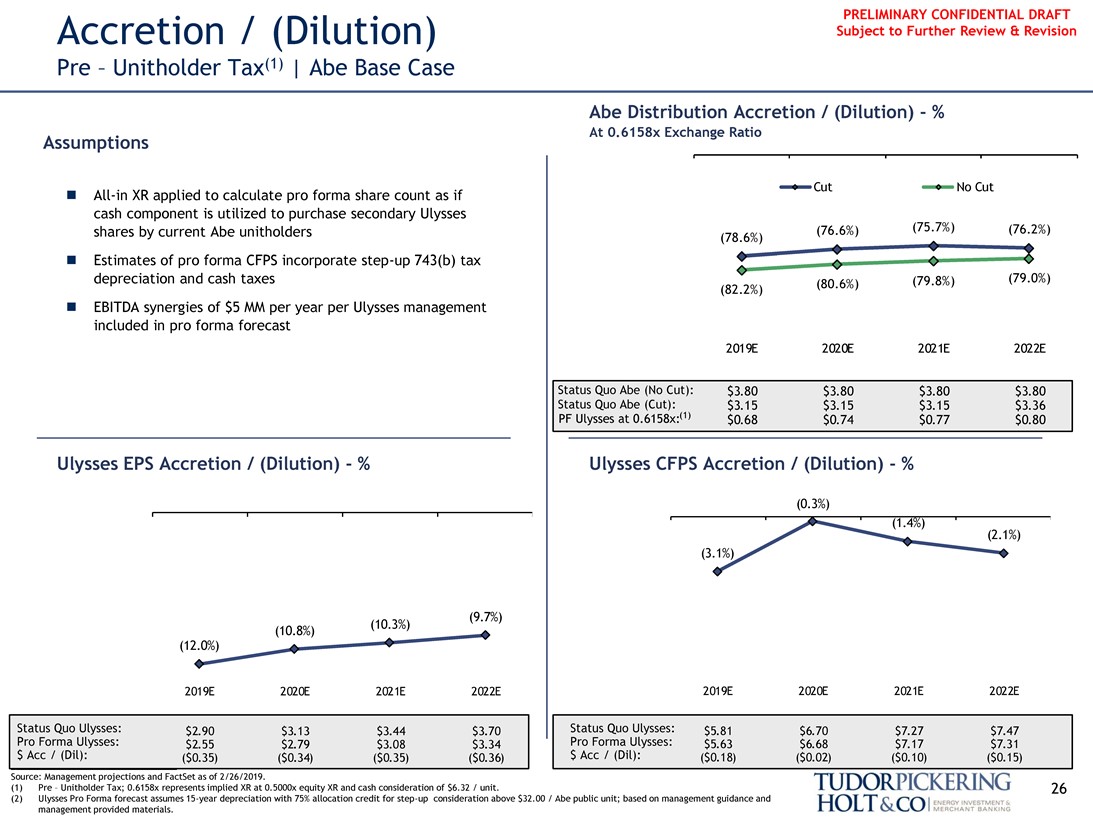

PRELIMINARY CONFIDENTIAL DRAFT Accretion / (Dilution) Subject to Further Review & Revision

Pre - Unitholder Tax(1) | Abe Base Case

Abe Distribution Accretion / (Dilution) - %

At 0.6158x Exchange Ratio

Assumptions

Cut No Cut

∎All-in XR applied to calculate pro forma share count as if cash component is utilized to purchase secondary Ulysses shares by current Abe unitholders (76.6%) (75.7%) (76.2%) (78.6%)

∎ Estimates of pro forma CFPS incorporatestep-up 743(b) tax depreciation and cash taxes (82.2%) (80.6%) (79.8%) (79.0%)∎ EBITDA synergies of $5 MM per year per Ulysses management included in pro forma forecast

2019E 2020E 2021E 2022E

Status Quo Abe (No Cut): $3.80 $3.80 $3.80 $3.80

Status Quo Abe (Cut): $3.15 $3.15 $3.15 $3.36

PF Ulysses at 0.6158x:(1) $0.68 $0.74 $0.77 $0.80

Ulysses EPS Accretion / (Dilution) - % Ulysses CFPS Accretion / (Dilution) - %

(0.3%)

(1.4%) (2.1%) (3.1%)

(9.7%) (10.3%) (10.8%) (12.0%)

2019E 2020E 2021E 2022E 2019E 2020E 2021E 2022E

Status Quo Ulysses: $2.90 $3.13 $3.44 $3.70 Status Quo Ulysses: $5.81 $6.70 $7.27 $7.47 Pro Forma Ulysses: $2.55 $2.79 $3.08 $3.34 Pro Forma Ulysses: $5.63 $6.68 $7.17 $7.31 $ Acc / (Dil): ($0.35) ($0.34) ($0.35) ($0.36) $ Acc / (Dil): ($0.18) ($0.02) ($0.10) ($0.15)

Source: Management projections and FactSet as of 2/26/2019.

(1) Pre – Unitholder Tax; 0.6158x represents implied XR at 0.5000x equity XR and cash consideration of $6.32 / unit. 26 (2) Ulysses Pro Forma forecast assumes15-year depreciation with 75% allocation credit for step-up consideration above $32.00 / Abe public unit; based on management guidance and management provided materials.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

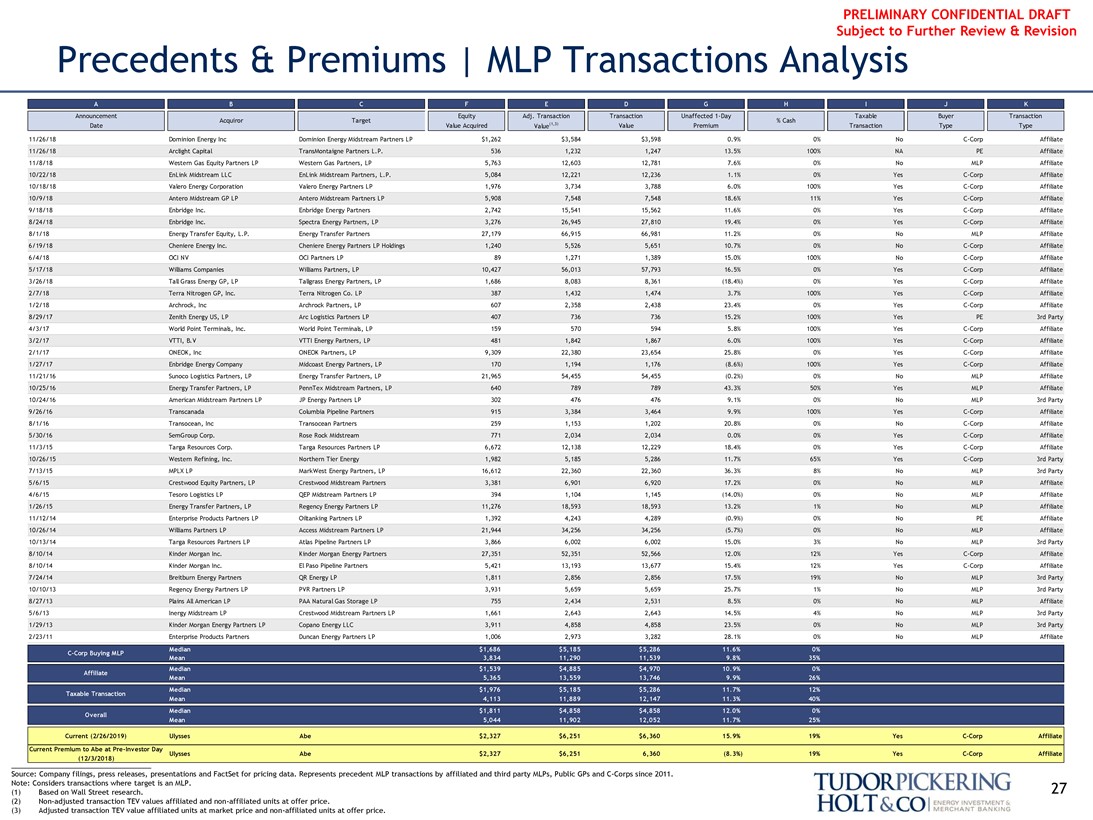

Precedents & Premiums | MLP Transactions Analysis

Announcement Equity Adj. Transaction Transaction Unaffected1-Day Taxable Buyer Transaction Acquiror Target % Cash Date Value Acquired Value(1,3) Value Premium Transaction Type Type

11/26/18 Dominion Energy Inc Dominion Energy Midstream Partners LP $1,262 $3,584 $3,598 0.9% 0% NoC-Corp Affiliate 11/26/18 Arclight Capital TransMontaigne Partners L.P. 536 1,232 1,247 13.5% 100% NA PE Affiliate 11/8/18 Western Gas Equity Partners LP Western Gas Partners, LP 5,763 12,603 12,781 7.6% 0% No MLP Affiliate 10/22/18 EnLink Midstream LLC EnLink Midstream Partners, L.P. 5,084 12,221 12,236 1.1% 0% YesC-Corp Affiliate 10/18/18 Valero Energy Corporation Valero Energy Partners LP 1,976 3,734 3,788 6.0% 100% YesC-Corp Affiliate 10/9/18 Antero Midstream GP LP Antero Midstream Partners LP 5,908 7,548 7,548 18.6% 11% YesC-Corp Affiliate 9/18/18 Enbridge Inc. Enbridge Energy Partners 2,742 15,541 15,562 11.6% 0% YesC-Corp Affiliate 8/24/18 Enbridge Inc. Spectra Energy Partners, LP 3,276 26,945 27,810 19.4% 0% YesC-Corp Affiliate 8/1/18 Energy Transfer Equity, L.P. Energy Transfer Partners 27,179 66,915 66,981 11.2% 0% No MLP Affiliate 6/19/18 Cheniere Energy Inc. Cheniere Energy Partners LP Holdings 1,240 5,526 5,651 10.7% 0% NoC-Corp Affiliate 6/4/18 OCI NV OCI Partners LP 89 1,271 1,389 15.0% 100% NoC-Corp Affiliate 5/17/18 Williams Companies Williams Partners, LP 10,427 56,013 57,793 16.5% 0% YesC-Corp Affiliate 3/26/18 Tall Grass Energy GP, LP Tallgrass Energy Partners, LP 1,686 8,083 8,361 (18.4%) 0% YesC-Corp Affiliate 2/7/18 Terra Nitrogen GP, Inc. Terra Nitrogen Co. LP 387 1,432 1,474 3.7% 100% YesC-Corp Affiliate 1/2/18 Archrock, Inc Archrock Partners, LP 607 2,358 2,438 23.4% 0% YesC-Corp Affiliate 8/29/17 Zenith Energy US, LP Arc Logistics Partners LP 407 736 736 15.2% 100% Yes PE 3rd Party 4/3/17 World Point Terminals, Inc. World Point Terminals, LP 159 570 594 5.8% 100% YesC-Corp Affiliate 3/2/17 VTTI, B.V VTTI Energy Partners, LP 481 1,842 1,867 6.0% 100% YesC-Corp Affiliate 2/1/17 ONEOK, Inc ONEOK Partners, LP 9,309 22,380 23,654 25.8% 0% YesC-Corp Affiliate 1/27/17 Enbridge Energy Company Midcoast Energy Partners, LP 170 1,194 1,176 (8.6%) 100% YesC-Corp Affiliate 11/21/16 Sunoco Logistics Partners, LP Energy Transfer Partners, LP 21,965 54,455 54,455 (0.2%) 0% No MLP Affiliate 10/25/16 Energy Transfer Partners, LP PennTex Midstream Partners, LP 640 789 789 43.3% 50% Yes MLP Affiliate 10/24/16 American Midstream Partners LP JP Energy Partners LP 302 476 476 9.1% 0% No MLP 3rd Party 9/26/16 Transcanada Columbia Pipeline Partners 915 3,384 3,464 9.9% 100% YesC-Corp Affiliate 8/1/16 Transocean, Inc Transocean Partners 259 1,153 1,202 20.8% 0% NoC-Corp Affiliate 5/30/16 SemGroup Corp. Rose Rock Midstream 771 2,034 2,034 0.0% 0% YesC-Corp Affiliate 11/3/15 Targa Resources Corp. Targa Resources Partners LP 6,672 12,138 12,229 18.4% 0% YesC-Corp Affiliate 10/26/15 Western Refining, Inc. Northern Tier Energy 1,982 5,185 5,286 11.7% 65% YesC-Corp 3rd Party 7/13/15 MPLX LP MarkWest Energy Partners, LP 16,612 22,360 22,360 36.3% 8% No MLP 3rd Party 5/6/15 Crestwood Equity Partners, LP Crestwood Midstream Partners 3,381 6,901 6,920 17.2% 0% No MLP Affiliate 4/6/15 Tesoro Logistics LP QEP Midstream Partners LP 394 1,104 1,145 (14.0%) 0% No MLP Affiliate 1/26/15 Energy Transfer Partners, LP Regency Energy Partners LP 11,276 18,593 18,593 13.2% 1% No MLP Affiliate 11/12/14 Enterprise Products Partners LP Oiltanking Partners LP 1,392 4,243 4,289 (0.9%) 0% No PE Affiliate 10/26/14 Williams Partners LP Access Midstream Partners LP 21,944 34,256 34,256 (5.7%) 0% No MLP Affiliate 10/13/14 Targa Resources Partners LP Atlas Pipeline Partners LP 3,866 6,002 6,002 15.0% 3% No MLP 3rd Party 8/10/14 Kinder Morgan Inc. Kinder Morgan Energy Partners 27,351 52,351 52,566 12.0% 12% YesC-Corp Affiliate 8/10/14 Kinder Morgan Inc. El Paso Pipeline Partners 5,421 13,193 13,677 15.4% 12% YesC-Corp Affiliate 7/24/14 Breitburn Energy Partners QR Energy LP 1,811 2,856 2,856 17.5% 19% No MLP 3rd Party 10/10/13 Regency Energy Partners LP PVR Partners LP 3,931 5,659 5,659 25.7% 1% No MLP 3rd Party 8/27/13 Plains All American LP PAA Natural Gas Storage LP 755 2,434 2,531 8.5% 0% No MLP Affiliate 5/6/13 Inergy Midstream LP Crestwood Midstream Partners LP 1,661 2,643 2,643 14.5% 4% No MLP 3rd Party 1/29/13 Kinder Morgan Energy Partners LP Copano Energy LLC 3,911 4,858 4,858 23.5% 0% No MLP 3rd Party 2/23/11 Enterprise Products Partners Duncan Energy Partners LP 1,006 2,973 3,282 28.1% 0% No MLP Affiliate

Current (2/26/2019) Ulysses Abe $2,327 $6,251 $6,360 15.9% 19% YesC-Corp Affiliate Current Premium to Abe atPre-Investor Day Ulysses Abe $2,327 $6,251 6,360 (8.3%) 19% YesC-Corp Affiliate

___________________________________ (12/3/2018)

Source: Company filings, press releases, presentations and FactSet for pricing data. Represents precedent MLP transactions by affiliated and third party MLPs, Public GPs andC-Corps since 2011.

Note: Considers transactions where target is an MLP. 27 (1) Based on Wall Street research.

(2)Non-adjusted transaction TEV values affiliated andnon-affiliated units at offer price.

(3) Adjusted transaction TEV value affiliated units at market price andnon-affiliated units at offer price.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Supplemental Analysis

28

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

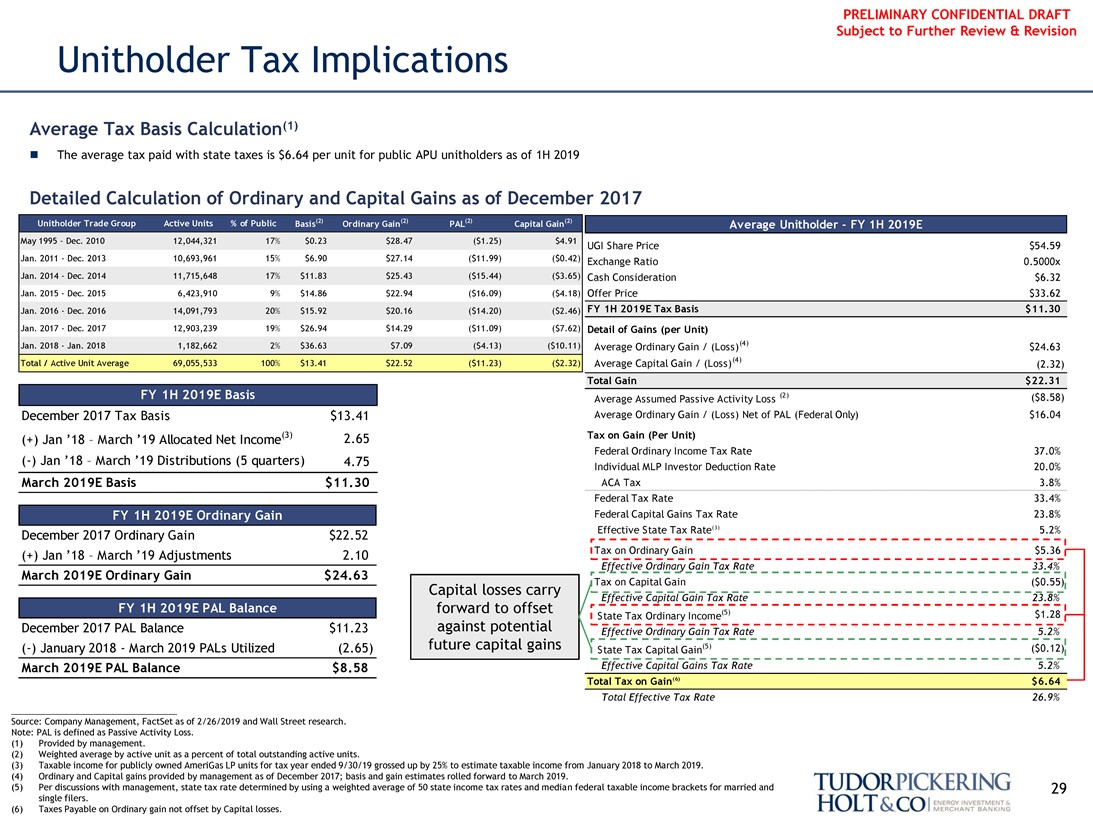

Unitholder Tax Implications

Average Tax Basis Calculation(1)

∎ The average tax paid with state taxes is $6.64 per unit for public APU unitholders as of 1H 2019

Detailed Calculation of Ordinary and Capital Gains as of December 2017

May 1995—Dec. 2010 12,044,321 17% $0.23 $28.47 ($1.25) $4.91 UGI Share Price $54.59 Jan. 2011—Dec. 2013 10,693,961 15% $6.90 $27.14 ($11.99) ($0.42) Exchange Ratio 0.5000x Jan. 2014—Dec. 2014 11,715,648 17% $11.83 $25.43 ($15.44) ($3.65) Cash Consideration $6.32 Jan. 2015—Dec. 2015 6,423,910 9% $14.86 $22.94 ($16.09) ($4.18) Offer Price $33.62 Jan. 2016—Dec. 2016 14,091,793 20% $15.92 $20.16 ($14.20) ($2.46) FY 1H 2019E Tax Basis $11.30 Jan. 2017—Dec. 2017 12,903,239 19% $26.94 $14.29 ($11.09) ($7.62) Detail of Gains (per Unit) Jan. 2018—Jan. 2018 1,182,662 2% $36.63 $7.09 ($4.13) ($10.11) Average Ordinary Gain / (Loss)(4) $24.63 Total / Active Unit Average 69,055,533 100% $13.41 $22.52 ($11.23) ($2.32) Average Capital Gain / (Loss)(4) (2.32)

Total Gain $22.31

Unitholder Trade Group Active Units % of Public Basis(2) Ordinary Gain(2) PAL(2) Capital Gain(2)

Average Unitholder - FY 1H 2019E

Average Assumed Passive Activity Loss (2) ($8.58) December 2017 Tax Basis $13.41 Average Ordinary Gain / (Loss) Net of PAL (Federal Only) $16.04

(+) Jan ’18 – March ’19 Allocated Net Income(3) 2.65 Tax on Gain (Per Unit)

Federal Ordinary Income Tax Rate 37.0%

(-) Jan ’18 – March ’19 Distributions (5 quarters) 4.75

Individual MLP Investor Deduction Rate 20.0%

March 2019E Basis $11.30 ACA Tax 3.8% Federal Tax Rate 33.4% Federal Capital Gains Tax Rate 23.8% Effective State Tax Rate(3) 5.2%

FY 1H 2019E Bsisi

FY 1H 2019E Ordinary Gain

FY 1H 2019E PAL Balance

December 2017 Ordinary Gain $22.52

(+) Jan ’18 – March ’19 Adjustments 2.10 Tax on Ordinary Gain $5.36

Effective Ordinary Gain Tax Rate 33.4%

March 2019E Ordinary Gain $24.63

Capital losses carry forward to offset against potential future capital gains

Tax on Capital Gain ($0.55)

Effective Capital Gain Tax Rate 23.8% (5)

State Tax Ordinary Income $1.28

December 2017 PAL Balance $11.23 Effective Ordinary Gain Tax Rate 5.2%

(-) January 2018—March 2019 PALs Utilized (2.65) State Tax Capital Gain(5) ($0.12)

March 2019E PAL Balance $8.58 Effective Capital Gains Tax Rate 5.2%

Total Tax on Gain(6) $6.64

Total Effective Tax Rate 26.9%

Source: Company Management, FactSet as of 2/26/2019 and Wall Street research. Note: PAL is defined as Passive Activity Loss.

(1) Provided by management.

(2) Weighted average by active unit as a percent of total outstanding active units.

(3) Taxable income for publicly owned AmeriGas LP units for tax year ended 9/30/19 grossed up by 25% to estimate taxable income from January 2018 to March 2019. (4) Ordinary and Capital gains provided by management as of December 2017; basis and gain estimates rolled forward to March 2019.

(5) Per discussions with management, state tax rate determined by using a weighted average of 50 state income tax rates and median federal taxable income brackets for married and 29 single filers.

(6) Taxes Payable on Ordinary gain not offset by Capital losses.

Tudorpickering Holt&co energy investment & merchant banking

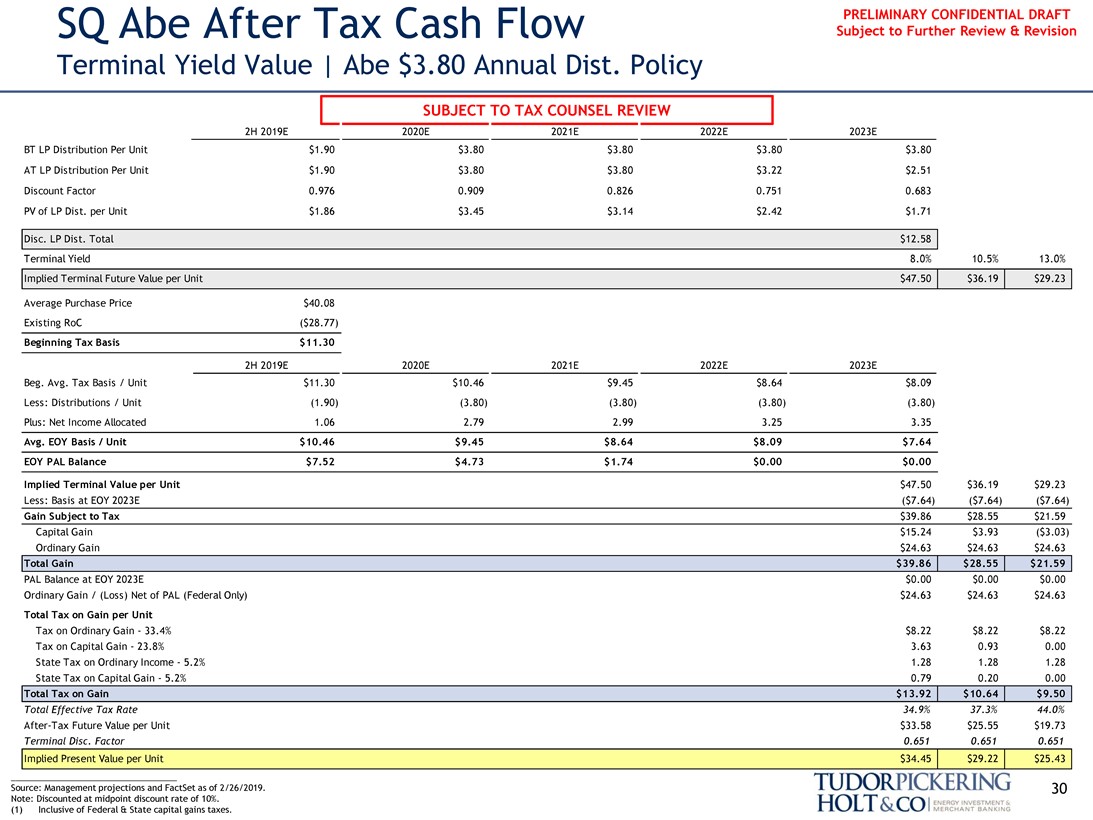

PRELIMINARY CONFIDENTIAL DRAFT SQ Abe After Tax Cash Flow Subject to Further Review & Revision

Terminal Yield Value | Abe $3.80 Annual Dist. Policy

SUBJECT TO TAX COUNSEL REVIEW

2H 2019E 2020E 2021E 2022E 2023E

BT LP Distribution Per Unit $1.90 $3.80 $3.80 $3.80 $3.80 AT LP Distribution Per Unit $1.90 $3.80 $3.80 $3.22 $2.51 Discount Factor 0.976 0.909 0.826 0.751 0.683 PV of LP Dist. per Unit $1.86 $3.45 $3.14 $2.42 $1.71

Disc. LP Dist. Total $12.58

Terminal Yield 8.0% 10.5% 13.0% Implied Terminal Future Value per Unit $47.50 $36.19 $29.23

Average Purchase Price $40.08 Existing RoC ($28.77)

Beginning Tax Basis $11.30

2H 2019E 2020E 2021E 2022E 2023E

Beg. Avg. Tax Basis / Unit $11.30 $10.46 $9.45 $8.64 $8.09 Less: Distributions / Unit (1.90) (3.80) (3.80) (3.80) (3.80) Plus: Net Income Allocated 1.06 2.79 2.99 3.25 3.35

Avg. EOY Basis / Unit $10.46 $9.45 $8.64 $8.09 $7.64 EOY PAL Balance $7.52 $4.73 $1.74 $0.00 $0.00

Implied Terminal Value per Unit $47.50 $36.19 $29.23 Less: Basis at EOY 2023E ($7.64) ($7.64) ($7.64) Gain Subject to Tax $39.86 $28.55 $21.59 Capital Gain $15.24 $3.93 ($3.03) Ordinary Gain $24.63 $24.63 $24.63

Total Gain $39.86 $28.55 $21.59

PAL Balance at EOY 2023E $0.00 $0.00 $0.00 Ordinary Gain / (Loss) Net of PAL (Federal Only) $24.63 $24.63 $24.63

Total Tax on Gain per Unit

Tax on Ordinary Gain—33.4% $8.22 $8.22 $8.22 Tax on Capital Gain—23.8% 3.63 0.93 0.00 State Tax on Ordinary Income—5.2% 1.28 1.28 1.28 State Tax on Capital Gain—5.2% 0.79 0.20 0.00

Total Tax on Gain $13.92 $10.64 $9.50

Total Effective Tax Rate 34.9% 37.3% 44.0%

After-Tax Future Value per Unit $33.58 $25.55 $19.73

Terminal Disc. Factor 0.651 0.651 0.651

Implied Present Value per Unit $34.45 $29.22 $25.43

Source: Management projections and FactSet as of 2/26/2019. 30 Note: Discounted at midpoint discount rate of 10%.

(1) Inclusive of Federal & State capital gains taxes.

Tudorpickering Holt&co energy investment & merchant banking

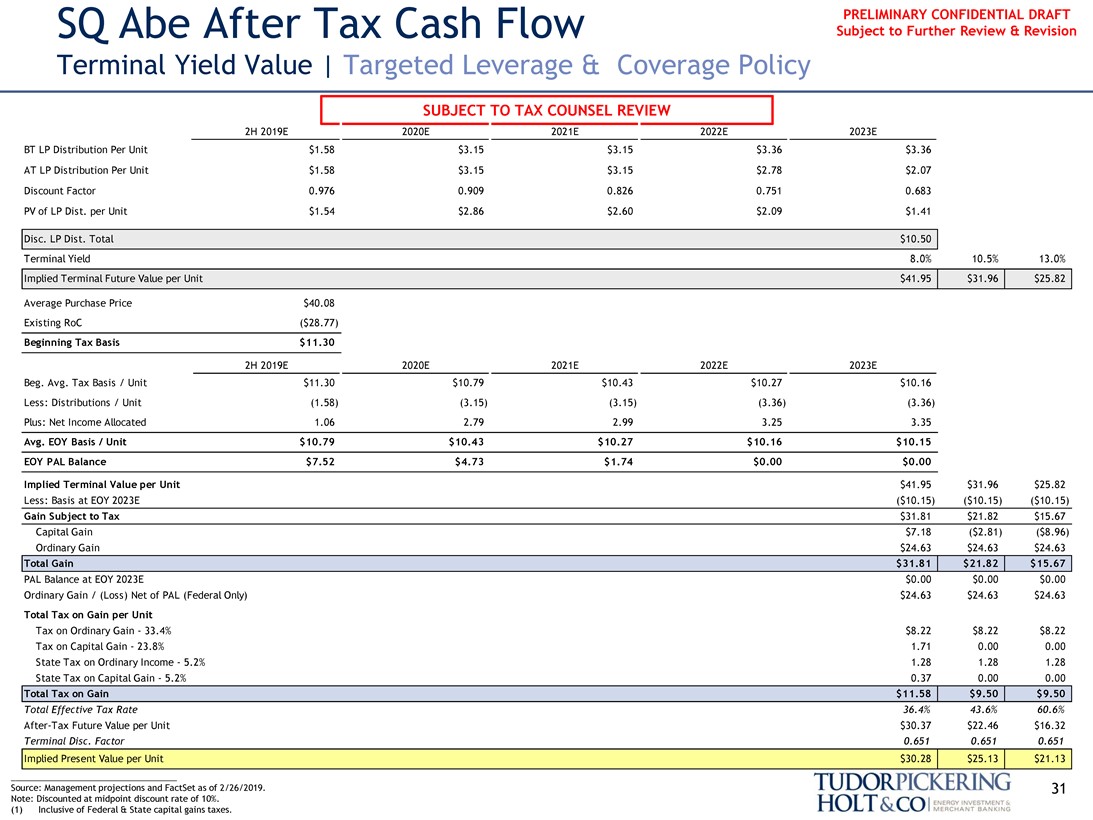

PRELIMINARY CONFIDENTIAL DRAFT SQ Abe After Tax Cash Flow Subject to Further Review & Revision

Terminal Yield Value | Targeted Leverage & Coverage Policy

SUBJECT TO TAX COUNSEL REVIEW

2H 2019E 2020E 2021E 2022E 2023E

BT LP Distribution Per Unit $1.58 $3.15 $3.15 $3.36 $3.36 AT LP Distribution Per Unit $1.58 $3.15 $3.15 $2.78 $2.07 Discount Factor 0.976 0.909 0.826 0.751 0.683 PV of LP Dist. per Unit $1.54 $2.86 $2.60 $2.09 $1.41

Disc. LP Dist. Total $10.50

Terminal Yield 8.0% 10.5% 13.0% Implied Terminal Future Value per Unit $41.95 $31.96 $25.82

Average Purchase Price $40.08 Existing RoC ($28.77)

Beginning Tax Basis $11.30

2H 2019E 2020E 2021E 2022E 2023E

Beg. Avg. Tax Basis / Unit $11.30 $10.79 $10.43 $10.27 $10.16 Less: Distributions / Unit (1.58) (3.15) (3.15) (3.36) (3.36) Plus: Net Income Allocated 1.06 2.79 2.99 3.25 3.35

Avg. EOY Basis / Unit $10.79 $10.43 $10.27 $10.16 $10.15 EOY PAL Balance $7.52 $4.73 $1.74 $0.00 $0.00

Implied Terminal Value per Unit $41.95 $31.96 $25.82 Less: Basis at EOY 2023E ($10.15) ($10.15) ($10.15) Gain Subject to Tax $31.81 $21.82 $15.67 Capital Gain $7.18 ($2.81) ($8.96) Ordinary Gain $24.63 $24.63 $24.63

Total Gain $31.81 $21.82 $15.67

PAL Balance at EOY 2023E $0.00 $0.00 $0.00 Ordinary Gain / (Loss) Net of PAL (Federal Only) $24.63 $24.63 $24.63

Total Tax on Gain per Unit

Tax on Ordinary Gain—33.4% $8.22 $8.22 $8.22 Tax on Capital Gain—23.8% 1.71 0.00 0.00 State Tax on Ordinary Income—5.2% 1.28 1.28 1.28 State Tax on Capital Gain—5.2% 0.37 0.00 0.00

Total Tax on Gain $11.58 $9.50 $9.50

Total Effective Tax Rate 36.4% 43.6% 60.6%

After-Tax Future Value per Unit $30.37 $22.46 $16.32

Terminal Disc. Factor 0.651 0.651 0.651

Implied Present Value per Unit $30.28 $25.13 $21.13

Source: Management projections and FactSet as of 2/26/2019. 31 Note: Discounted at midpoint discount rate of 10%.

(1) Inclusive of Federal & State capital gains taxes.

Tudorpickering Holt&co energy investment & merchant banking

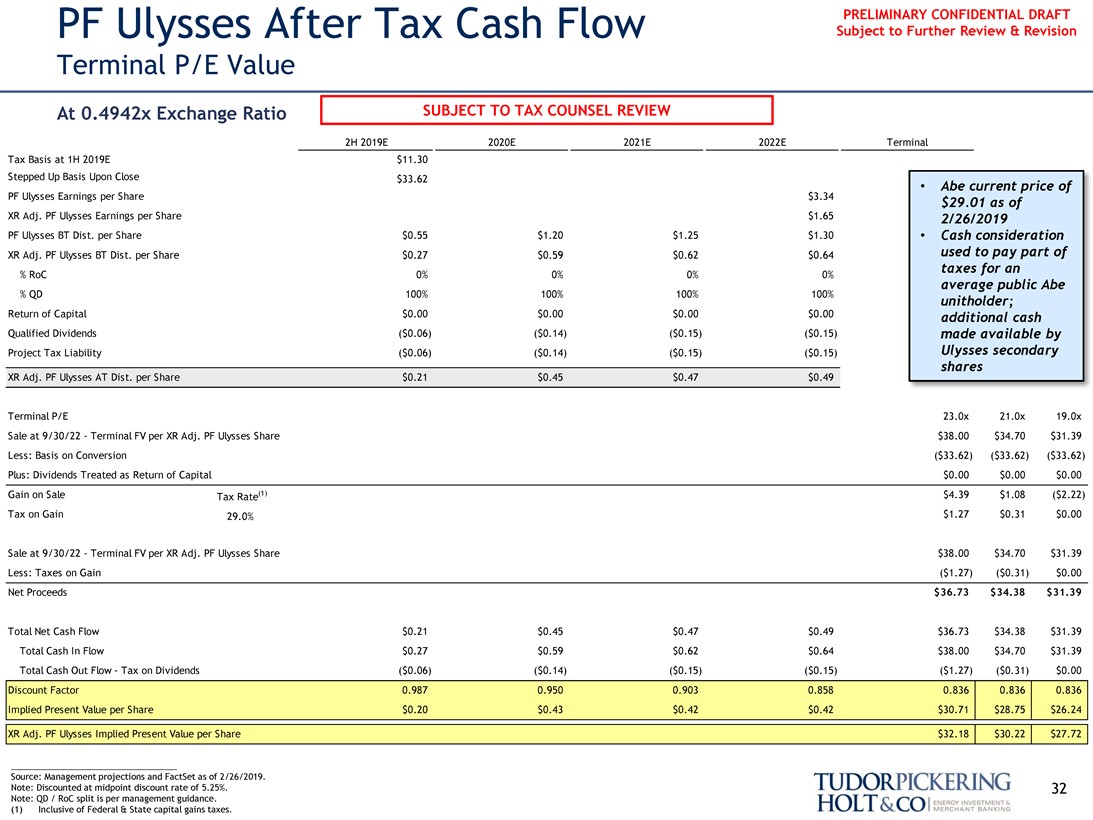

PRELIMINARY CONFIDENTIAL DRAFT PF Ulysses After Tax Cash Flow Subject to Further Review & Revision

Terminal P/E Value

At 0.4942x Exchange Ratio SUBJECT TO TAX COUNSEL REVIEW

2H 2019E 2020E 2021E 2022E Terminal Tax Basis at 1H 2019E $11.30 Stepped Up Basis Upon Close $33.62

PF Ulysses Earnings per Share $3.34 • Abe current price of

$29.01 as of

XR Adj. PF Ulysses Earnings per Share $1.65 2/26/2019

PF Ulysses BT Dist. per Share $0.55 $1.20 $1.25 $1.30 • Cash consideration XR Adj. PF Ulysses BT Dist. per Share $0.27 $0.59 $0.62 $0.64 used to pay part of

taxes for an

% RoC 0% 0% 0% 0%

average public Abe

% QD 100% 100% 100% 100% unitholder; Return of Capital $0.00 $0.00 $0.00 $0.00 additional cash Qualified Dividends ($0.06) ($0.14) ($0.15) ($0.15) made available by Project Tax Liability ($0.06) ($0.14) ($0.15) ($0.15) Ulysses secondary XR Adj. PF Ulysses AT Dist. per Share $0.21 $0.45 $0.47 $0.49 shares

Terminal P/E 23.0x 21.0x 19.0x Sale at 9/30/22 - Terminal FV per XR Adj. PF Ulysses Share $38.00 $34.70 $31.39 Less: Basis on Conversion ($33.62) ($33.62) ($33.62) Plus: Dividends Treated as Return of Capital $0.00 $0.00 $0.00 Gain on Sale Tax Rate(1) $4.39 $1.08 ($2.22) Tax on Gain 29.0% $1.27 $0.31 $0.00

Sale at 9/30/22 - Terminal FV per XR Adj. PF Ulysses Share $38.00 $34.70 $31.39 Less: Taxes on Gain ($1.27) ($0.31) $0.00 Net Proceeds $36.73 $34.38 $31.39

Total Net Cash Flow $0.21 $0.45 $0.47 $0.49 $36.73 $34.38 $31.39 Total Cash In Flow $0.27 $0.59 $0.62 $0.64 $38.00 $34.70 $31.39 Total Cash Out Flow - Tax on Dividends ($0.06) ($0.14) ($0.15) ($0.15) ($1.27) ($0.31) $0.00 Discount Factor 0.987 0.950 0.903 0.858 0.836 0.836 0.836 Implied Present Value per Share $0.20 $0.43 $0.42 $0.42 $30.71 $28.75 $26.24

XR Adj. PF Ulysses Implied Present Value per Share $32.18 $30.22 $27.72

Source: Management projections and FactSet as of 2/26/2019.

Note: Discounted at midpoint discount rate of 5.25%. 32 Note: QD / RoC split is per management guidance.

(1) Inclusive of Federal & State capital gains taxes.

Tudorpickering Holt&co energy investment & merchant banking

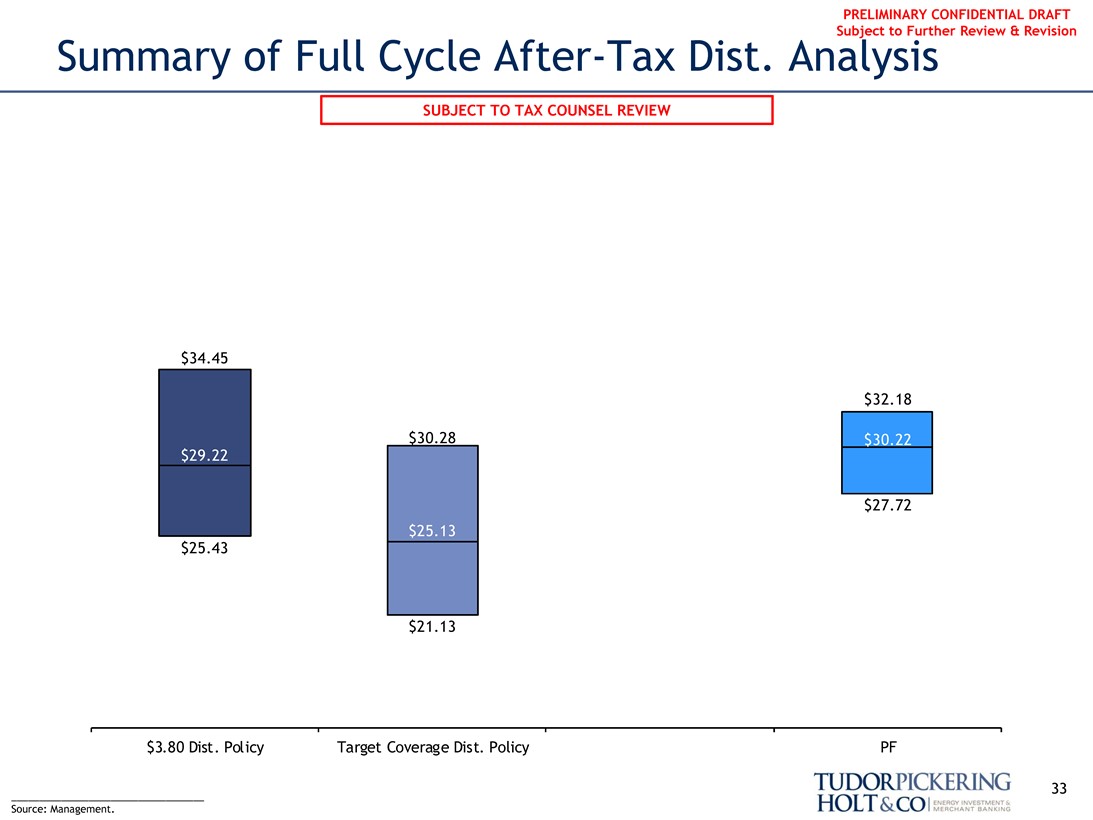

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Summary of Full CycleAfter-Tax Dist. Analysis

SUBJECT TO TAX COUNSEL REVIEW

$29.22

$25.13

$34.45

$32.18

$30.28

$27.72 $25.43

$21.13

$3.80 Dist. Policy Target Coverage Dist. Policy PF

33

Source: Management.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Summary of Material Changes Subject to Further Review & Revision

Updates since 2/14/2019 Materials

∎ Adjusted select Premiums to Unaffected Date figures for MLP Precedents & Premiums analysis∎ Adjusted terminal value discounting for PV of future share price analysis

∎ Adjusted terminal EBITDA multiple range to 8.5x – 11.5x for Ulysses Unlevered DCF analysis (from February 12 materials)

34

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Appendix

35

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

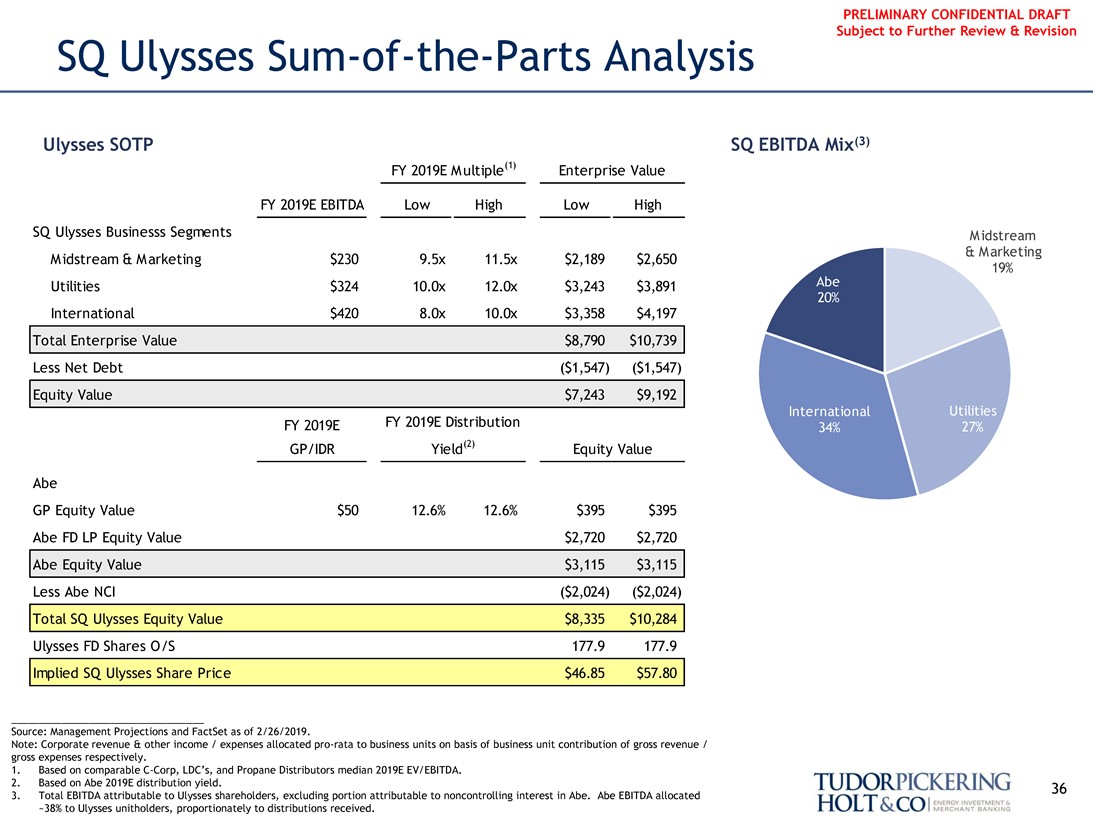

SQ UlyssesSum-of-the-Parts Analysis

Ulysses SOTP SQ EBITDA Mix(3)

FY 2019E M ultiple(1) Enterprise Value

FY 2019E EBITDA Low High Low High

SQ Ulysses Businesss Segments M idstream

& M arketing

M idstream & M arketing $230 9.5x 11.5x $2,189 $2,650

19%

Utilities $324 10.0x 12.0x $3,243 $3,891

International $420 8.0x 10.0x $3,358 $4,197 Total Enterprise Value $8,790 $10,739 Less Net Debt ($1,547) ($1,547) Equity Value $7,243 $9,192

FY 2019E FY 2019E Distribution GP/IDR Yield(2) Equity Value

Abe

GP Equity Value $50 12.6% 12.6% $395 $395 Abe FD LP Equity Value $2,720 $2,720 Abe Equity Value $3,115 $3,115 Less Abe NCI ($2,024) ($2,024) Total SQ Ulysses Equity Value $8,335 $10,284 Ulysses FD Shares O/S 177.9 177.9 Implied SQ Ulysses Share Price $46.85 $57.80

Source: Management Projections and FactSet as of 2/26/2019.

Note: Corporate revenue & other income / expenses allocatedpro-rata to business units on basis of business unit contribution of gross revenue / gross expenses respectively.

1. Based on comparableC-Corp, LDC’s, and Propane Distributors median 2019E EV/EBITDA.

2. Based on Abe 2019E distribution yield. 36

3. Total EBITDA attributable to Ulysses shareholders, excluding portion attributable to noncontrolling interest in Abe. Abe EBITDA allocated ~38% to Ulysses unitholders, proportionately to distributions received.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Cost of Capital

37

Tudorpickering Holt&co energy investment & merchant banking

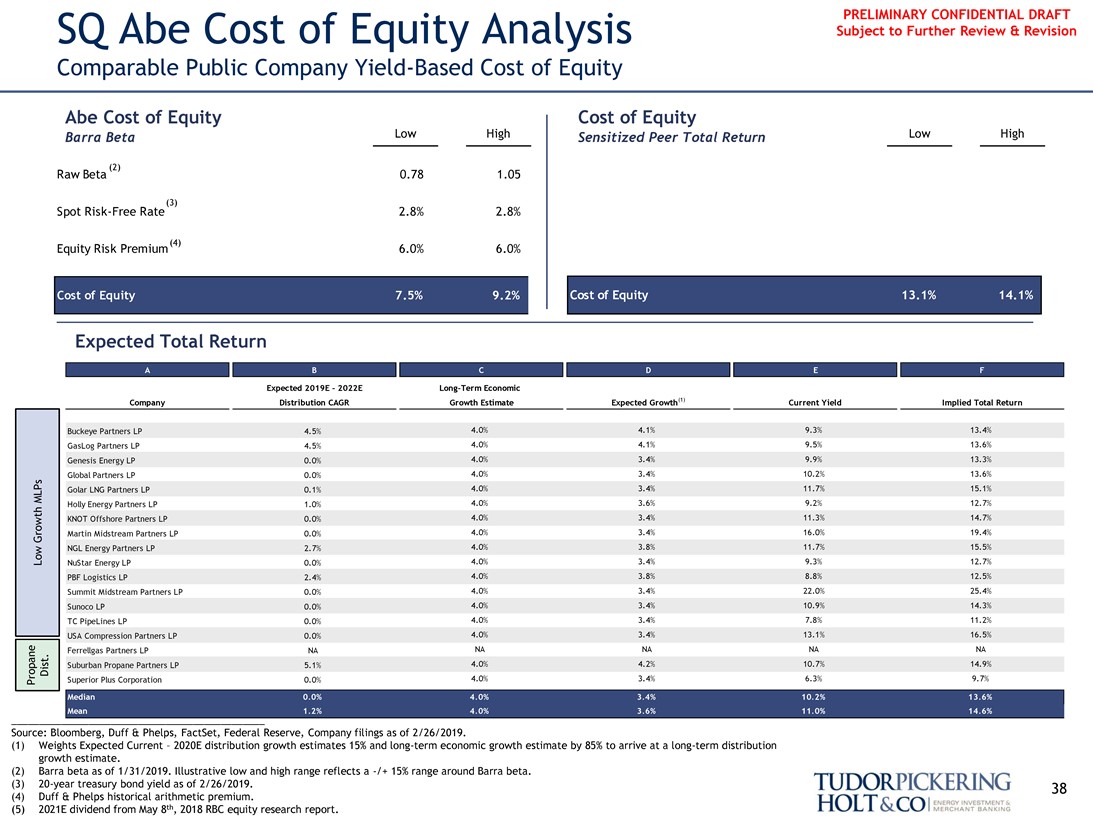

PRELIMINARY CONFIDENTIAL DRAFT SQ Abe Cost of Equity Analysis Subject to Further Review & Revision

Comparable Public Company Yield-Based Cost of Equity

Abe Cost of Equity Cost of Equity

Barra Beta Low High Sensitized Peer Total Return Low High

(2)

Raw Beta 0.78 1.05

(3)

Spot Risk-Free Rate 2.8% 2.8%

(4)

Equity Risk Premium 6.0% 6.0%

Expected Total Return

Expected 2019E - 2022E Long-Term Economic

Company Distribution CAGR Growth Estimate Expected Growth(1) Current Yield Implied Total Return

Buckeye Partners LP 4.5% 4.0% 4.1% 9.3% 13.4% GasLog Partners LP 4.5% 4.0% 4.1% 9.5% 13.6% Genesis Energy LP 0.0% 4.0% 3.4% 9.9% 13.3% Global Partners LP 0.0% 4.0% 3.4% 10.2% 13.6% MLPs Golar LNG Partners LP 0.1% 4.0% 3.4% 11.7% 15.1% Holly Energy Partners LP 1.0% 4.0% 3.6% 9.2% 12.7% KNOT Offshore Partners LP 0.0% 4.0% 3.4% 11.3% 14.7% Growth Martin Midstream Partners LP 0.0% 4.0% 3.4% 16.0% 19.4% NGL Energy Partners LP 2.7% 4.0% 3.8% 11.7% 15.5% Low NuStar Energy LP 0.0% 4.0% 3.4% 9.3% 12.7% PBF Logistics LP 2.4% 4.0% 3.8% 8.8% 12.5% Summit Midstream Partners LP 0.0% 4.0% 3.4% 22.0% 25.4% Sunoco LP 0.0% 4.0% 3.4% 10.9% 14.3% TC PipeLines LP 0.0% 4.0% 3.4% 7.8% 11.2% USA Compression Partners LP 0.0% 4.0% 3.4% 13.1% 16.5% Ferrellgas Partners LP NA NA NA NA NA

Dist. Suburban Propane Partners LP 5.1% 4.0% 4.2% 10.7% 14.9% Propane Superior Plus Corporation 0.0% 4.0% 3.4% 6.3% 9.7%

Source: Bloomberg, Duff & Phelps, FactSet, Federal Reserve, Company filings as of 2/26/2019.

(1) Weights Expected Current – 2020E distribution growth estimates 15% and long-term economic growth estimate by 85% to arrive at a long-term distribution growth estimate.

(2) Barra beta as of 1/31/2019. Illustrative low and high range reflects a -/+ 15% range around Barra beta.

(3)20-year treasury bond yield as of 2/26/2019. 38 (4) Duff & Phelps historical arithmetic premium.

(5) 2021E dividend from May 8th, 2018 RBC equity research report.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

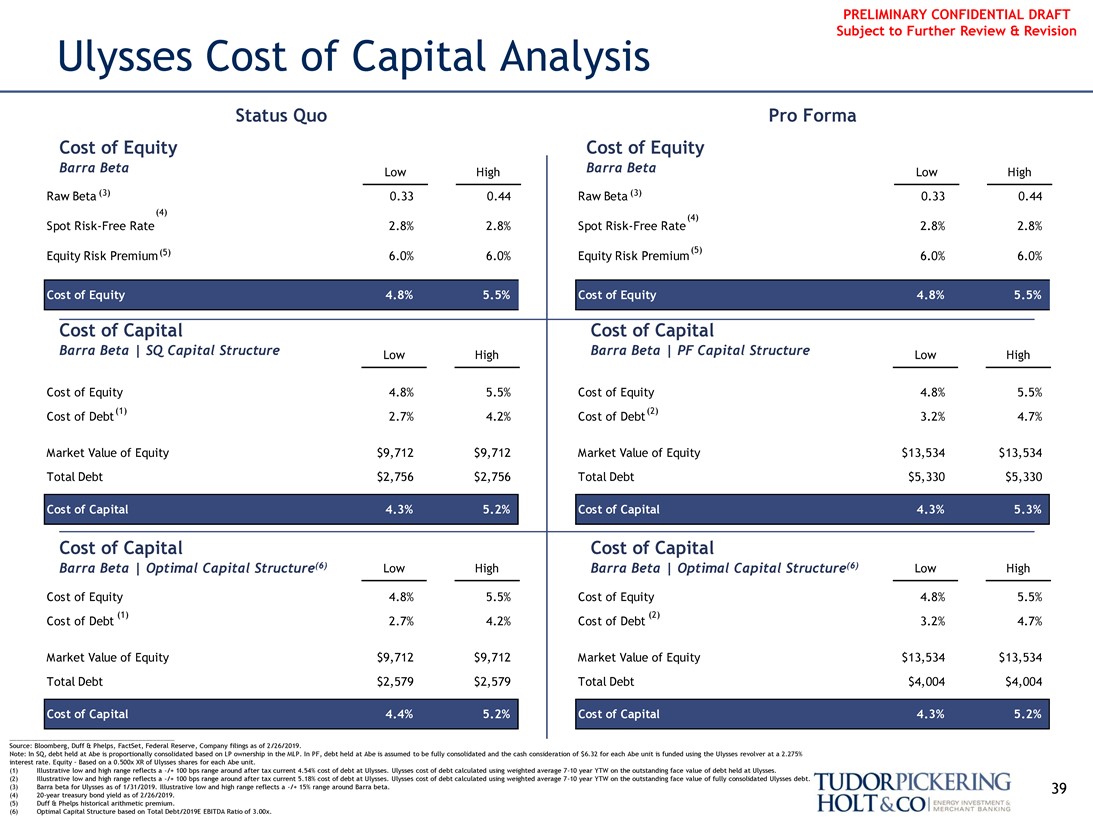

Ulysses Cost of Capital Analysis

Status Quo Pro Forma Cost of Equity Cost of Equity

Barra Beta Low High Barra Beta Low High Raw Beta (3) 0.33 0.44 Raw Beta (3) 0.33 0.44

(4)

(4)

Spot Risk-Free Rate 2.8% 2.8% Spot Risk-Free Rate 2.8% 2.8%

Equity Risk Premium(5) 6.0% 6.0% Equity Risk Premium(5) 6.0% 6.0%

Cost of Capital Cost of Capital

Barra Beta | SQ Capital Structure Low High Barra Beta | PF Capital Structure Low High

Cost of Equity 4.8% 5.5% Cost of Equity 4.8% 5.5% Cost of Debt(1) 2.7% 4.2% Cost of Debt(2) 3.2% 4.7%

Market Value of Equity $9,712 $9,712 Market Value of Equity $13,534 $13,534 Total Debt $2,756 $2,756 Total Debt $5,330 $5,330

Cost of Capital Cost of Capital

Barra Beta | Optimal Capital Structure(6) Low High Barra Beta | Optimal Capital Structure(6) Low High

Cost of Equity 4.8% 5.5% Cost of Equity 4.8% 5.5%

(1) (2)

Cost of Debt 2.7% 4.2% Cost of Debt 3.2% 4.7%

Market Value of Equity $9,712 $9,712 Market Value of Equity $13,534 $13,534 Total Debt $2,579 $2,579 Total Debt $4,004 $4,004

Source: Bloomberg, Duff & Phelps, FactSet, Federal Reserve, Company filings as of 2/26/2019.

Note: In SQ, debt held at Abe is proportionally consolidated based on LP ownership in the MLP. In PF, debt held at Abe is assumed to be fully consolidated and the cash consideration of $6.32 for each Abe unit is funded using the Ulysses revolver at a 2.275% interest rate. Equity – Based on a 0.500x XR of Ulysses shares for each Abe unit.

(1) Illustrative low and high range reflects a -/+ 100 bps range around after tax current 4.54% cost of debt at Ulysses. Ulysses cost of debt calculated using weighted average7-10 year YTW on the outstanding face value of debt held at Ulysses.

(2) Illustrative low and high range reflects a -/+ 100 bps range around after tax current 5.18% cost of debt at Ulysses. Ulysses cost of debt calculated using weighted average7-10 year YTW on the outstanding face value of fully consolidated Ulysses debt.

(3) Barra beta for Ulysses as of 1/31/2019. Illustrative low and high range reflects a -/+ 15% range around Barra beta. 39 (4)20-year treasury bond yield as of 2/26/2019.

(5) Duff & Phelps historical arithmetic premium.

(6) Optimal Capital Structure based on Total Debt/2019E EBITDA Ratio of 3.00x.

Tudorpickering Holt&co energy investment & merchant banking

PRELIMINARY CONFIDENTIAL DRAFT Subject to Further Review & Revision

Tudorpickering Holt&co energy investment & merchant banking

About The Firm

Tudor, Pickering, Holt & Co. is an integrated energy investment and merchant bank, providing high quality advice and services to institutional and corporate clients. Through the company’s two broker-dealer units, Tudor, Pickering, Holt & Co. Securities, Inc. (TPHCSI) and Tudor Pickering Holt & Co Advisors LP (TPHCA), members FINRA, together with affiliates in the United Kingdom and Canada, the company offers securities and investment banking services to the energy community. Perella Weinberg Partners Capital Management LP is an SEC registered investment adviser that delivers a suite of energy investment strategies.

The firm, headquartered in Houston, Texas, has approximately 170 employees and offices in Calgary, Canada; Denver, Colorado; New York, New York; and London, England.

Contact Us

Houston (Research, Sales and Trading): 713-333-2960 Houston (Investment Banking): 713-333-7100 Houston (Asset Management): 713-337-3999 Denver (Sales): 303-300-1900 Denver (Investment Banking): 303-300-1900

New York (Investment Banking): 212-610-1660

New York (Research, Sales): 212-610-1600 London: +011 44(0) 20 7268 2800 Calgary: 403-705-7830

www.TPHco.com

Copyright 2019 — Tudor, Pickering, Holt & Co.

Disclosure Statement

Tudor, Pickering, Holt & Co. does not provide accounting, tax or legal advice. This presentation does not constitute a tax opinion and cannot be used by any taxpayer for the purpose of avoiding tax penalties. We (i) make no conclusion on the valuation or pricing for tax purposes or the effects of federal income tax laws on any party and (ii) have assumed that the party’s intended tax treatment will be respected. Each person should seek legal, regulatory, accounting and tax advice based on his, her or its particular circumstances from independent advisors regarding the evaluation and impact of any transactions or matters described herein.

The information contained herein is confidential (except for information relating to United States tax issues) and may not be reproduced in whole or in part except as set forth in a written agreement between the Audit Committee of the Board of Directors of AmeriGas Propane, Inc. and Tudor, Pickering, Holt & Co.

Tudor, Pickering, Holt & Co. assumes no responsibility for independent verification of third-party information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance (including estimates of potential cost savings and synergies) prepared by, reviewed or discussed with the managements of your company and/ or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). These materials were designed for use by specific persons familiar with the business and the affairs of your company and Tudor, Pickering, Holt & Co. materials.

Under no circumstances is this presentation to be used or considered as an offer to sell or a solicitation of any offer to buy, any security. Prior to making any trade, you should discuss with your professional tax, accounting, or regulatory advisers how such particular trade(s) affect you. This brief statement does not disclose all of the risks and other significant aspects of entering into any particular transaction.

Tudor, Pickering, Holt & Co. operates in the United Kingdom under the trading name Perella Weinberg Partners UK LLP (authorized and regulated by the Financial Conduct Authority), and in Canada through its affiliate, Tudor, Pickering, Holt & Co. Securities

– Canada, ULC, located in Calgary, Alberta.

40